Chapter 03: Risk and Return: Part II

Copyright Cengage Learning. Powered by Cognero.

Page 14

POINTS:

1

Difficulty: Moderate

QUESTION TYPE:

False

IFMG.DAVE.19.03.05 – LO: 3-5

NATIONAL STANDARDS:

United States – AK – DISC: Risk and return

LOCAL STANDARDS:

Required rate of return

OTHER:

10/30/2017 8:03 PM

DATE MODIFIED:

27. Consider the information below for Postman Builders Inc. Suppose that the expected inflation rate and thus the

inflation premium increase by 2.0 percentage points, and Postman acquires risky assets that increase its beta by the

indicated percentage. What is the firm’s new required rate of return?

Beta:

1.50

Required return (rs)

10.20%

RPM:

6.00%

Percentage increase in beta:

20%

a.

14.00%

b.

14.70%

c.

15.44%

d.

16.21%

e.

17.02%

The following graph shows that United’s returns are perfectly correlated with the market.

POINTS:

1

Difficulty: Moderate

Multiple Choice

HAS VARIABLES:

False

IFMG.DAVE.19.03.05 – LO: 3-5

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

United States – AK – DISC: Risk and return

LOCAL STANDARDS:

United States – OH – Default City – TBA

Required rate of return

OTHER:

TYPE: Multiple Choice: Problem

10/30/2017 8:03 PM

DATE MODIFIED:

1/6/2018 12:09 PM

28. Assume that the market is in equilibrium and that stock betas can be estimated with historical data. The returns on the

market, the returns on United Fund (UF), the risk-free rate, and the required return on the United Fund are shown below.

Based on this information, what is the required return on the market, rM?

Year

Market

UF

2011

−9%

−14%

2012

11%

16%

2013

15%

22%

2014

5%

7%

2015

−1%

−2%

rRF: 7.00%;

rUnited: 15.00%

a.

10.57%

b.

11.13%

c.

11.72%

d.

12.33%

e.

12.95%

ANSWER:

d

Copyright Cengage Learning. Powered by Cognero.

Page 16

POINTS:

1

HAS VARIABLES:

False

NATIONAL STANDARDS:

TOPICS:

OTHER:

29. You are given the following returns on “the market” and Stock F during the last three years. We could calculate beta

using data for Years 1 and 2 and then, after Year 3, calculate a new beta for Years 2 and 3. How different are those two

betas, i.e., what’s the value of beta 2 − beta 1? (Hint: You can find betas using the Rise-Over-Run method, or using your

calculator’s regression function.)

Year

Market

Stock F

1

6.10%

6.50%

1

DIFFICULTY:

Difficulty: Moderate

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.03.02 – LO: 3-2

2

12.90%

−3.70%

3

16.20%

21.71%

a.

7.89

b.

8.30

c.

8.74

d.

9.20

e.

9.66

ANSWER:

d

POINTS:

1

DIFFICULTY:

Difficulty: Moderate

Multiple Choice

HAS VARIABLES:

False

IFMG.DAVE.19.03.05 – LO: 3-5

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – AK – DISC: Risk and return

United States – OH – Default City – TBA

TOPICS:

Beta’s sensitivity to the base year

OTHER:

TYPE: Multiple Choice: Problem

10/30/2017 8:03 PM

DATE MODIFIED:

1/6/2018 12:09 PM

30. For markets to be in equilibrium (that is, for there to be no strong pressure for prices to depart from their current

levels),

a.

The past realized rate of return must be equal to the expected rate of return; that is, .

b.

The required rate of return must equal the realized rate of return; that is, r = .

c.

All companies must pay dividends.

d.

No companies can be in danger of declaring bankruptcy.

e.

The expected rate of return must be equal to the required rate of return; that is, = r.

ANSWER:

e

31. Assume an economy in which there are three securities: Stock A with rA = 10% and σA = 10%; Stock B with rB =

15% and σB = 20%; and a riskless asset with rRF = 7%. Stocks A and B are uncorrelated (rAB = 0). Which of the

following statements is most CORRECT?

a.

The expected return on the investor’s portfolio will probably have an expected return that is somewhat below

10% and a standard deviation (SD) of approximately 10%.

b.

The expected return on the investor’s portfolio will probably have an expected return that is somewhat below

15% and a standard deviation (SD) that is between 10% and 20%.

c.

The investor’s risk/return indifference curve will be tangent to the CML at a point where the expected return is

in the range of 7% to 10%.

d.

Since the two stocks have a zero correlation coefficient, the investor can form a riskless portfolio whose

expected return is in the range of 10% to 15%.

e.

The expected return on the investor’s portfolio will probably have an expected return that is somewhat above

15% and a standard deviation (SD) of approximately 20%.

ANSWER:

b

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

United States – AK – DISC: Risk and return

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Market equilibrium

OTHER:

TYPE: Multiple Choice: Conceptual

10/30/2017 8:03 PM

DATE MODIFIED:

1/6/2018 12:09 PM

Copyright Cengage Learning. Powered by Cognero.

Page 19

32. Which of the following statements is CORRECT?

a.

Richard Roll has argued that it is possible to test the CAPM to see if it is correct.

b.

Tests have shown that the risk/return relationship appears to be linear, but the slope of the relationship is

greater than that predicted by the CAPM.

c.

Tests have shown that the betas of individual stocks are stable over time, but that the betas of large portfolios

are much less stable.

d.

The most widely cited study of the validity of the CAPM is one performed by Modigliani and Miller.

e.

Tests have shown that the betas of individual stocks are unstable over time, but that the betas of large

portfolios are reasonably stable over time.

ANSWER:

e

DIFFICULTY:

Multiple Choice

LEARNING OBJECTIVES:

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – OH – Default City – TBA

Tests of the CAPM

KEYWORDS:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

1/6/2018 12:09 PM

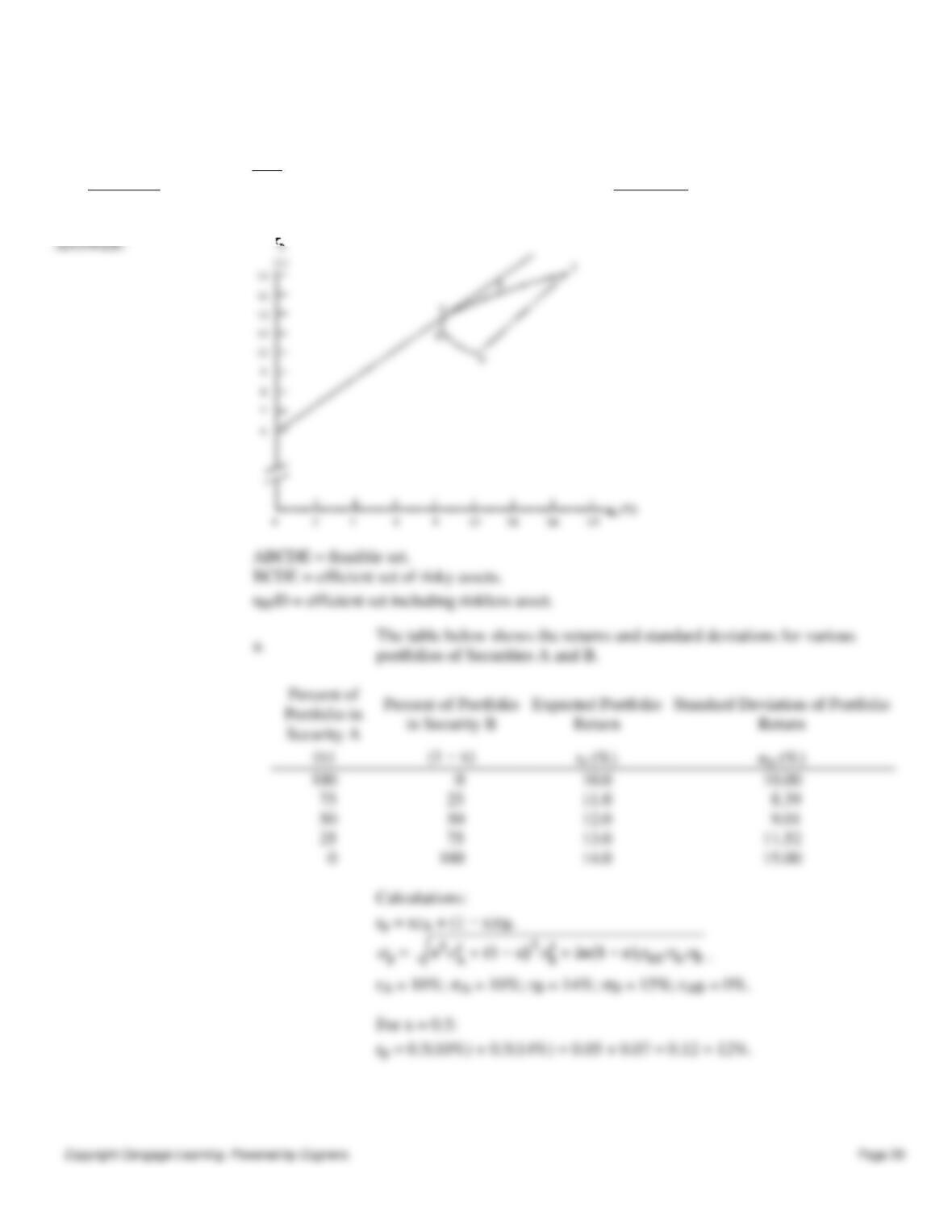

33. Stock A has an expected return rA = 10% and σA = 10%. Stock B has rB = 14% and σB = 15%. rAB = 0. The rate of

return on riskless assets is 6%.

a.

Construct a graph that shows the feasible and efficient sets, giving consideration to the

POINTS:

Difficulty: Challenging

QUESTION TYPE:

IFMG.DAVE.19.03.02 – LO: 3-2

NATIONAL STANDARDS:

United States – AK – DISC: Risk and return

LOCAL STANDARDS:

Portfolios and risk

OTHER:

10/30/2017 8:03 PM

DATE MODIFIED:

Chapter 03: Risk and Return: Part II

For x = 0.5:

existence of the riskless asset.

b.

Explain what would happen to the CML if the two stocks had (a) a positive correlation

coefficient or (b) a negative correlation coefficient.

c.

Suppose these were the only three securities (A, B, and riskless) in the economy, and

everyone’s indifference curves were such that they were tangent to the CML to the right of

the point where the CML was tangent to the efficient set of risky assets. Would this represent

a stable equilibrium? If not, how would an equilibrium be produced?

ANSWER:

Copyright Cengage Learning. Powered by Cognero.

Page 21

34. You plan to invest in Stock X, Stock Y, or some combination of the two. The expected return for X is 10% and σX =

5%. The expected return for Y is 12% and σY = 6%. The correlation coefficient, rXY, is 0.75.

a.

Calculate rp and σp for 100%, 75%, 50%, 25%, and 0% in Stock X.

b.

Use the values you calculated for rp and σp to graph the attainable set of portfolios. Which

part of the attainable set is efficient? Also, draw in a set of hypothetical indifference curves

to show how an investor might select a portfolio comprised of Stocks X and Y. Let an

indifference curve be tangent to the efficient set at the point where rp = 11%.

Chapter 03: Risk and Return: Part II

Copyright Cengage Learning. Powered by Cognero.

Page 22

c.

Now suppose we add a riskless asset to the investment possibilities. What effects will this

have on the construction of portfolios?

d.

Suppose rM = 12%, σM = 4%, and rRF = 6%. What would be the required and expected

return on a portfolio with σP = 10%?

e.

Suppose the correlation of Stock X with the market, rXM, is 0.8, while rYM = 0.9. Use this

information, along with data given previously, to determine Stock X’s and Stock Y‘s beta

coefficients.

f.

What is the required rate of return on Stocks X and Y? Do these stocks appear to be in

equilibrium? If not, what would happen to bring about an equilibrium?

Chapter 03: Risk and Return: Part II

.

POINTS:

1

Security A’s contribution to the portfolio risk is, therefore, higher than that of B.

portfolio, A is riskier.

b.

Beta coefficients of A and B are calculated as follows:

35. Security A has an expected return of 12.4% with a standard deviation of 15%, and a correlation with the market of

0.85. Security B has an expected return of −0.73% with a standard deviation of 20%, and a correlation with the market of

−0.67. The standard deviation of rM is 12%.

a.

To someone who acts in accordance with the CAPM, which security is more risky, A or B?

Why? (Hint: No calculations are necessary to answer this question; it is easy.)

b.

What are the beta coefficients of A and B? Calculations are necessary.

c.

If the risk-free rate is 6%, what is the value of rM?

ANSWER:

Difficulty: Challenging

Subjective Short Answer

False

United States – AK – DISC: Risk and return

United States – OH – Default City – TBA

TYPE: Short Answer: Problem

10/30/2017 8:03 PM

1/6/2018 12:09 PM

Copyright Cengage Learning. Powered by Cognero.

Page 25