3-1

Chapter 3

Answers to Review Problems

Finance For Executives – 4th Edition

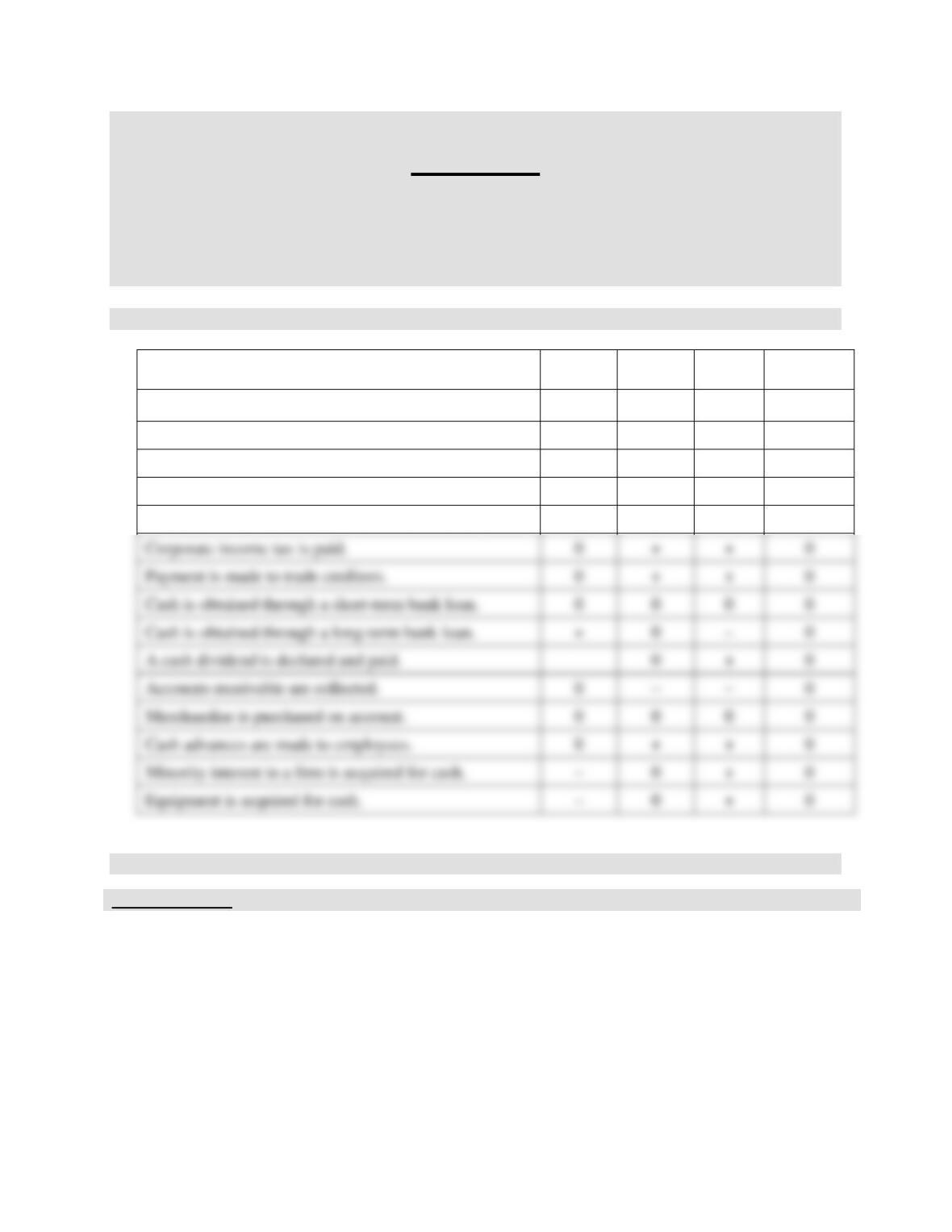

1. Transactions.

NLF

WCR

NSF

NET

PROFIT

Shares are issued for cash.

+

0

–

0

Goods for inventory are sold for cash.

+

–

–

+

Goods from inventory are sold on account.

+

+

0

+

A fixed asset is sold for cash for less than book value.

+

0

–

–

A fixed asset is sold for cash for more than book value.

+

0

–

+

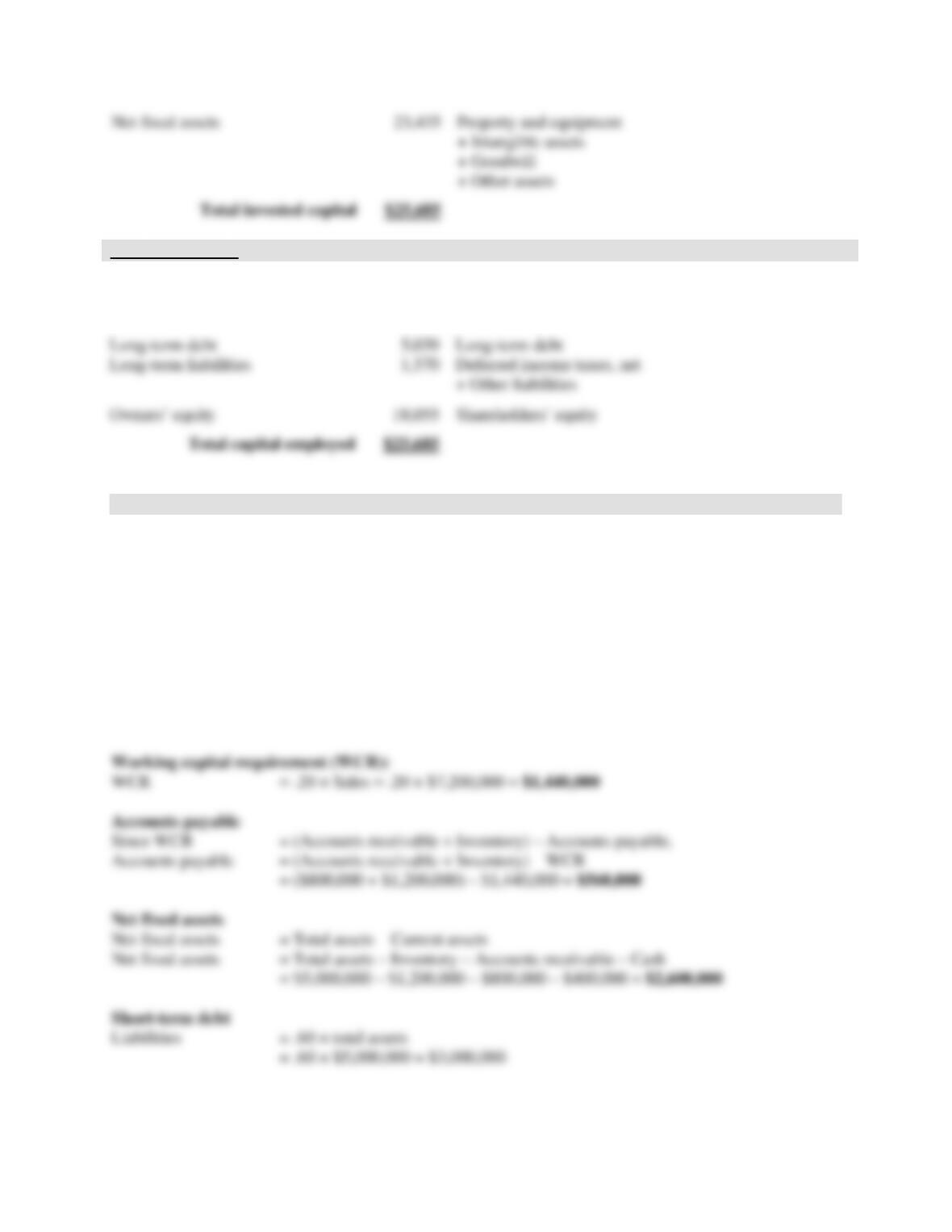

2. Constructing a managerial balance sheet.

Invested Capital

In millions

Cash

$661

Cash and cash equivalents + Short-term investment

Working Capital Requirement

1,589

Merchandise inventories

+ Deferred income taxes

+ Other current assets

– Accounts payable

– Accrued compensation and employees benefits

– Self-insurance liabilities – Deferred revenue

– Other current liabilities

Corporate income tax is paid.

0

+

Payment is made to trade creditors.

0

+

Cash is obtained through a short-term bank loan.

0

0

0

Cash is obtained through a long-term bank loan.

+

0

–

A cash dividend is declared and paid.

–

0

Accounts receivable are collected.

0

–

–

Merchandise is purchased on account.

0

0

0

Cash advances are made to employees.

0

+

Minority interest in a firm is acquired for cash.

–

0

Equipment is acquired for cash.

–

0

3-2

3. Reconstructing a balance sheet.

Sales

20 days of sales = $400,000

360 days of sales = ($400,000/20) × 360 = $7,200,000

Accounts receivable

40 days of sales = ($7,200,000/360) × 40 = $800,000

Inventory

Inventory = Sales/6

= $7,200,000/6 = $1,200,000

Capital employed

In millions

Short-term debt

$1,021

Short-term borrowing

+ Current portion of long-term debt

3-3

Balance Sheet

4. Effect of transactions on working capital requirement.

a. Decrease

b. Decrease

c. Increase

5. Managing liquidity.

a. Wrong.

From where would the cash come from to repurchase shares or reimburse short-term debt?

The relationship is a tautology. As such, it cannot be used for causality relations.

Assets

Liabilities

Cash

$ 400,000

Short-term debt

$ 244,000

Accounts receivable

800,000

Accounts payable

560,000

Inventory

1,200,000

3-4

6. The cash-to-cash conversion period.

Cash-to-cash conversion period = Inventory period + Collection period – Payment period

Collection period =

365/sales Net

receivableAccounts

Payment period =

s)/365inventoriein Change sold goods of Cost(

payableAccounts

365/Purchases

payableAccounts

+

=

7. Industry effect on the working capital requirement.

a.

in millions

Firm 1

Firm 2

Firm 3

Firm 4

Firm 5

Revenue

$428

$3,498

$27,235

$21,870

$166,809

Accounts Receivable

78

63

–

5,385

1,341

Inventories

299

84

–

3,463

19,793

100

–

1,366

3-5

Firm 1

WCR = $78 + $299 + $4 + $0 – $25 – $7 – $14 = $335

Working capital requirement-to-revenue ratio

= $335/$428 = .78

Firm 2

WCR = $63 + $84 + $100 + $0 – $196 – $262 – $741 = ($952)

Working capital requirement-to-revenue ratio

= ($952)/$3,498 = (.27)

3-6

Firm 3

WCR = $5,385 + $3,463 + $0 + $108 – $2,272 – $1,905 – $2,037 = $2,742

Firm 4

WCR = $1,341 + $19,793 + $1,366 + $0 – $13,105 – $7,290 – $0 = $2,105

Working capital requirement-to-revenue ratio

= $2,105/$166,809 = .0126

3-7

b.

Firm 1 is The Robert Mondavi Corporation: Inventory turnover is low, reflecting aging wine. The

amount of accounts payable is low reflecting a low level of purchases, which is not surprising since most

of the raw material needed to grow grapes (air, sun, and rain) is free. As a result, working capital

requirement is high relative to sales (78 cents out of one dollar of sales is locked in the firm’s operating

cycle).

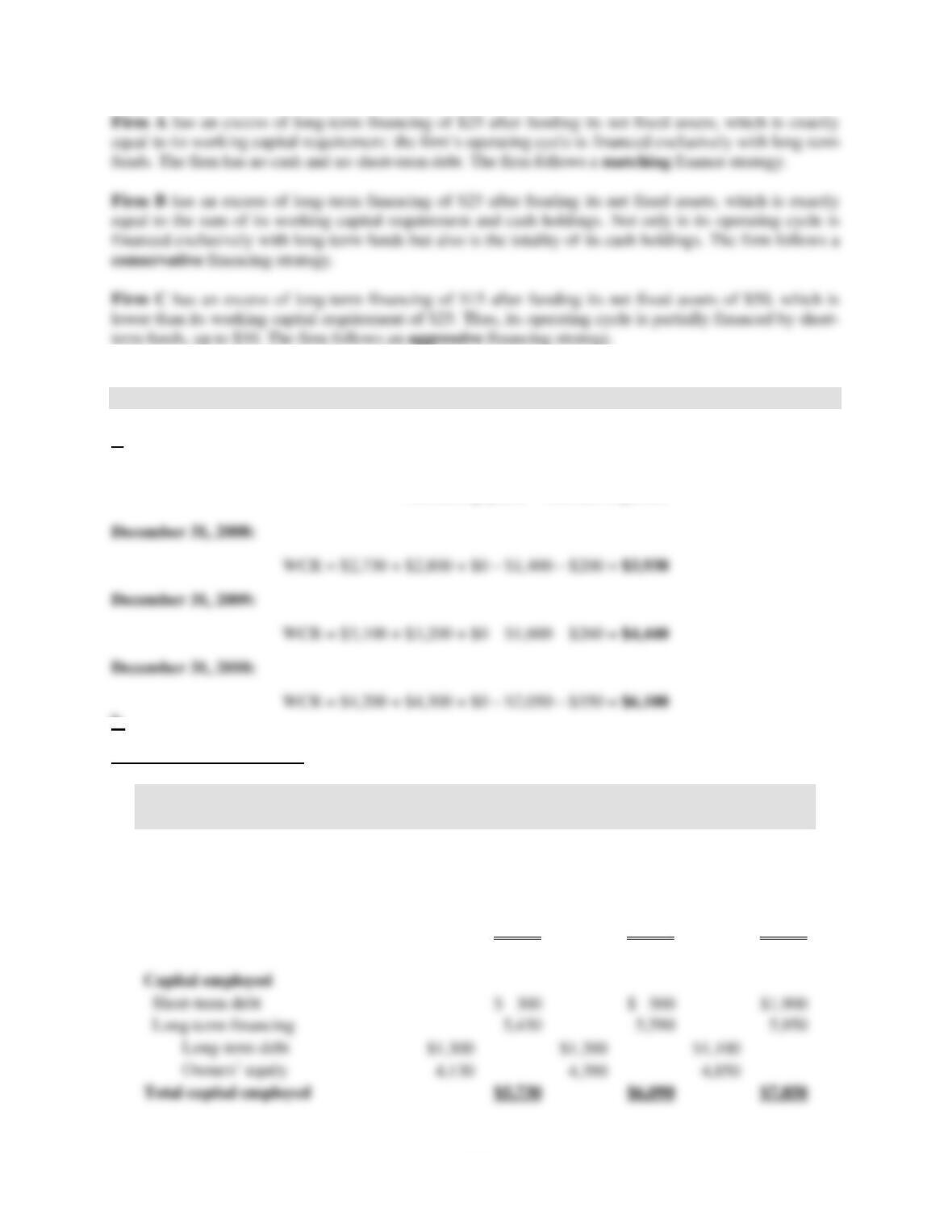

8. Financing strategies.

The managerial balance sheet of the three firms can be directly constructed from the data with

Working capital requirement = Accounts receivable + Inventories – Accounts payable:

Firm A

Firm B

Firm C

Invested capital

Cash

$ 0

$10

$ 0

Working capital requirement

25

15

25

Net fixed assets

50

50

50

Total invested capital

$75

$75

$75

Capital employed

Short-term debt

$ 0

Long-term financing

75

75

65

Total capital employed

$75

$75

$75

Firm A

Firm B

Firm C

Net long-term financing

[Long-term financing – Net fixed assets]

$25

$ 25

$15

Net short-term financing

[Short-term debt – Cash]

0

(10)

10

3-8

9. The financial effect of the management of the operating cycle.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

b.

Managerial balance sheets

in thousands

December 31,

2008

December 31,

2009

December 31,

2010

Invested capital

Cash

$ 600

$ 350

$ 300

Working capital requirement (WCR)

3,930

4,440

6,100

Net fixed assets

1,200

1,300

1,450

Total invested capital

$5,730

$6,090

$7,850

Capital employed

Short-term debt

$ 300

$ 500

Long-term financing

Long-term debt

Total capital employed

$5,730

$6,090

$7,850

3-9

c.

Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets

December 31, 2008: NLF = $1,300 + $4,130 – $1,200 = $4,230

Net short-term financing (NSF) = Short-term debt – Cash

December 31, 2008: NSF = $300 – $600 = ($300)

Note that net short-term financing (NSF) went up drastically from December 31, 2008, to December 31,

2010. In the third year, the firm’s financing strategy changed from a matching one to a very aggressive

one. During that year, each extra dollar invested in the operating cycle which was not financed either by

retained earnings or long-term debt was funded by short-term debt

d.

Pro forma working capital requirement (WCR)12/31/10

Accounts receivable12/31/10 =

days30

365

salesNet

3-10

Accounts payable12/31/10 =

days33

365

sinventorieinChangesoldgoodsofCost

days33

365

Purchases

+

=

Pro forma managerial balance sheet

in thousands

December 31,

2010

Invested capital

Cash

$1,379

Working capital requirement (WCR)

3,121

Net fixed assets

1,450

Total invested capital

$5,950

Capital employed

Short-term debt

Long-term financing

Long-term debt

Owners’ equity

Note that the amount of long-term financing ($5,950) would have been higher than the investment in

fixed assets and in the operating cycle ($1,450 + $3,121 = $4,571). Sentec Inc. would not have needed

any short-term debt, and would have $1,379 million (5,950 – $44,571) in cash.

Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets

NLF = $1,100 + $4,850 – $1,450 = $4,500

3-11

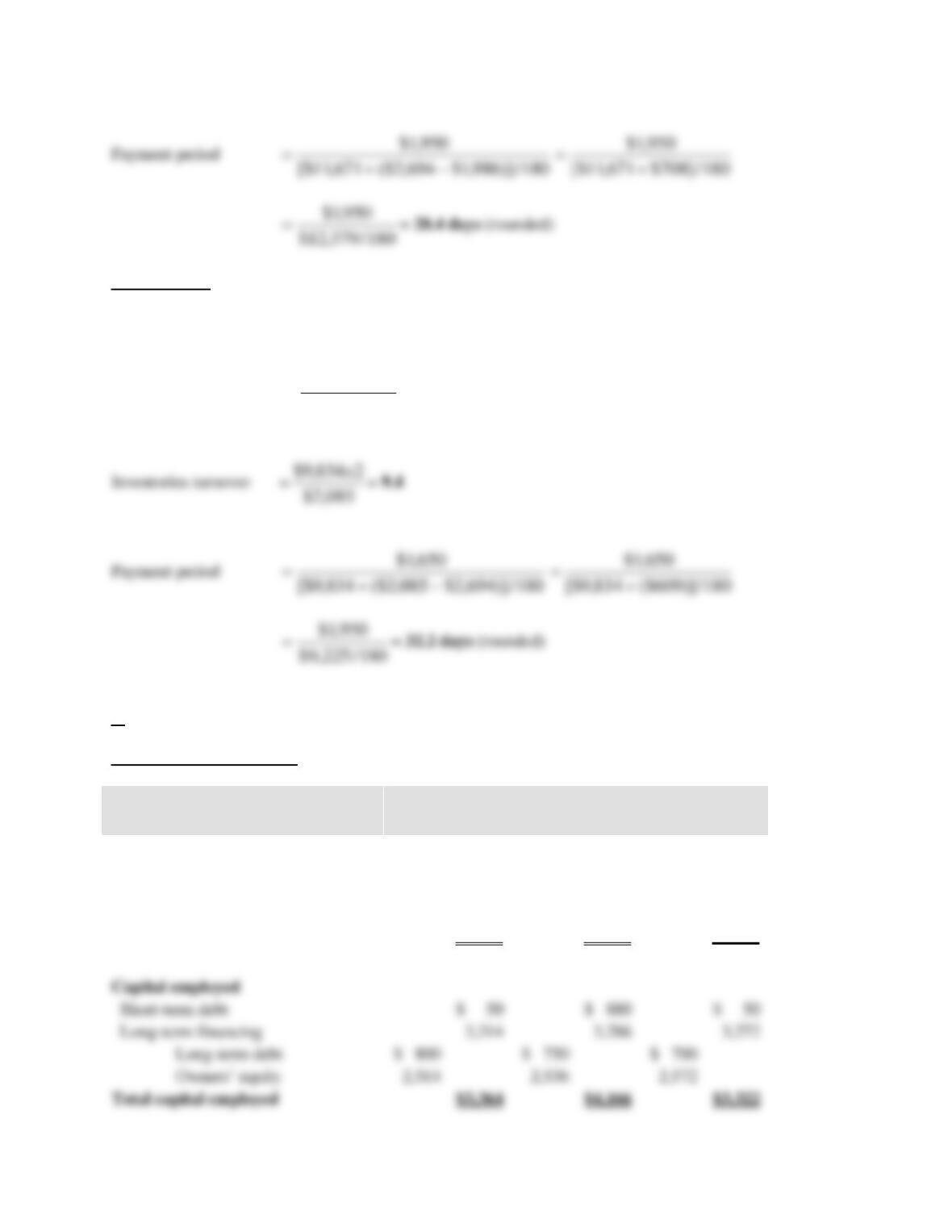

10. Seasonal business.

a.

Working capital requirement (WCR) = Inventories + Accounts receivable + Prepaid expenses

– Accounts payable – Accrued expenses

June 30, 2009

WCR = $1,986 + $1,953 + $80 – $1,450 – $98 = $2,471

December 31, 2009

WCR = $2,694 + $2,616 + $42 – $1,950 – $114 = $3,288

Collection period days =

180/851,13$

616,2$

= 34 days (rounded)

3-12

June 30, 2010

WCR = $2,085 + $2,100 + $25 – $1,650 – $138 = $2,422

Collection period days =

180/720,11$

100,2$

= 32.3 days (rounded)

b.

Managerial balance sheet

in thousands

June 30,

2009

December 31,

2009

June 30,

2010

Invested capital

Cash

$ 160

$ 60

$ 70

Working capital requirement (WCR)

((WC(WCR)

2,471

3,288

2,422

Net fixed assets

733

818

830

Total invested capital

$3,364

$4,166

$3,322

Capital employed

Short-term debt

$ 50

$ 880

$ 50

Long-term financing

3,314

3,286

3,272

Long-term debt

$ 800

$ 750

$ 700

Owners’ equity

2,514

2,536

2,572

Total capital employed

$3,364

$4,166

$3,322

3-13

c.

Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets

June 30, 2009: NLF = $800 + $2,514 – $733 = $2,581

Net short-term financing (NSF) = Short-term debt – Cash

June 30, 2009: NSF = $50 – $160 = ($110)

Mars Electronics has a matching strategy since its short-term financing needs are funded with short-term

debt and its permanent financing needs are funded with long-term debt and equity. The firm has a

seasonal activity: its sales and working capital requirement are larger in the second part of the year than in

the first part of the year. During the first part of the year, net short-term financing is negative since there