Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 28: Time Value of Money

QUESTION TYPE:

Multiple Choice

102. Which of the following statements regarding a 30-year monthly payment amortized mortgage with a nominal interest

rate of 8% is CORRECT?

a.

Exactly 8% of the first monthly payment represents interest.

b.

The monthly payments will decline over time.

c.

A smaller proportion of the last monthly payment will be interest, and a larger proportion will be principal,

than for the first monthly payment.

d.

The total dollar amount of principal being paid off each month gets smaller as the loan approaches maturity.

e.

The amount representing interest in the first payment would be higher if the nominal interest rate were 6%

rather than 8%.

ANSWER:

c

Copyright Cengage Learning. Powered by Cognero.

Page 62

103. Which of the following statements regarding a 20-year monthly payment amortized mortgage with a nominal interest

rate of 10% is CORRECT?

a.

Exactly 10% of the first monthly payment represents interest.

b.

The monthly payments will increase over time.

c.

A larger proportion of the first monthly payment will be interest, and a smaller proportion will be principal,

than for the last monthly payment.

d.

The total dollar amount of interest being paid off each month gets larger as the loan approaches maturity.

e.

The amount representing interest in the first payment would be higher if the nominal interest rate were 7%

rather than 10%.

ANSWER:

c

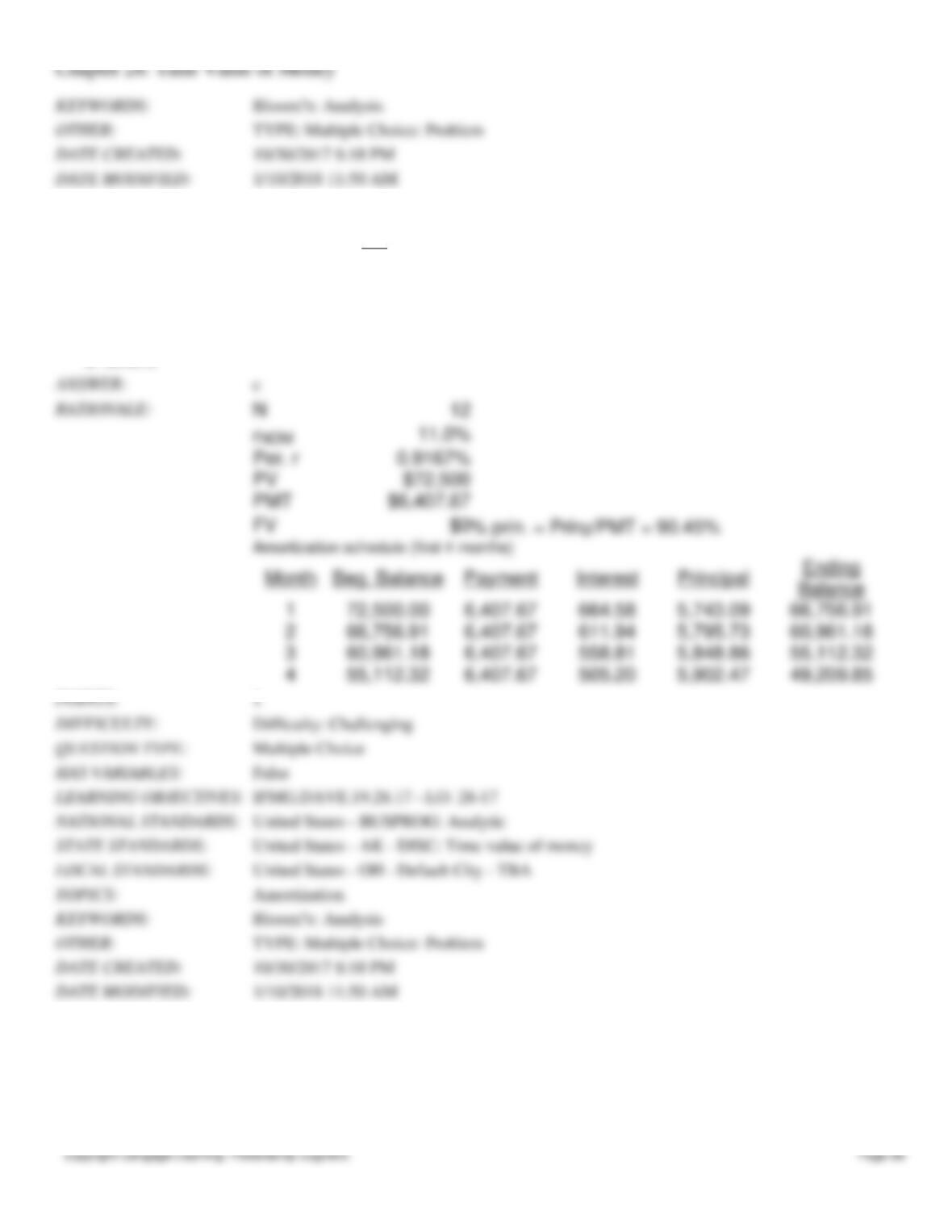

104. Suppose you borrowed $12,000 at a rate of 9.0% and must repay it in 4 equal installments at the end of each of the

next 4 years. How large would your payments be?

a.

$3,704.02

b.

$3,889.23

c.

$4,083.69

Chapter 28: Time Value of Money

d.

$4,287.87

e.

$4,502.26

ANSWER:

a

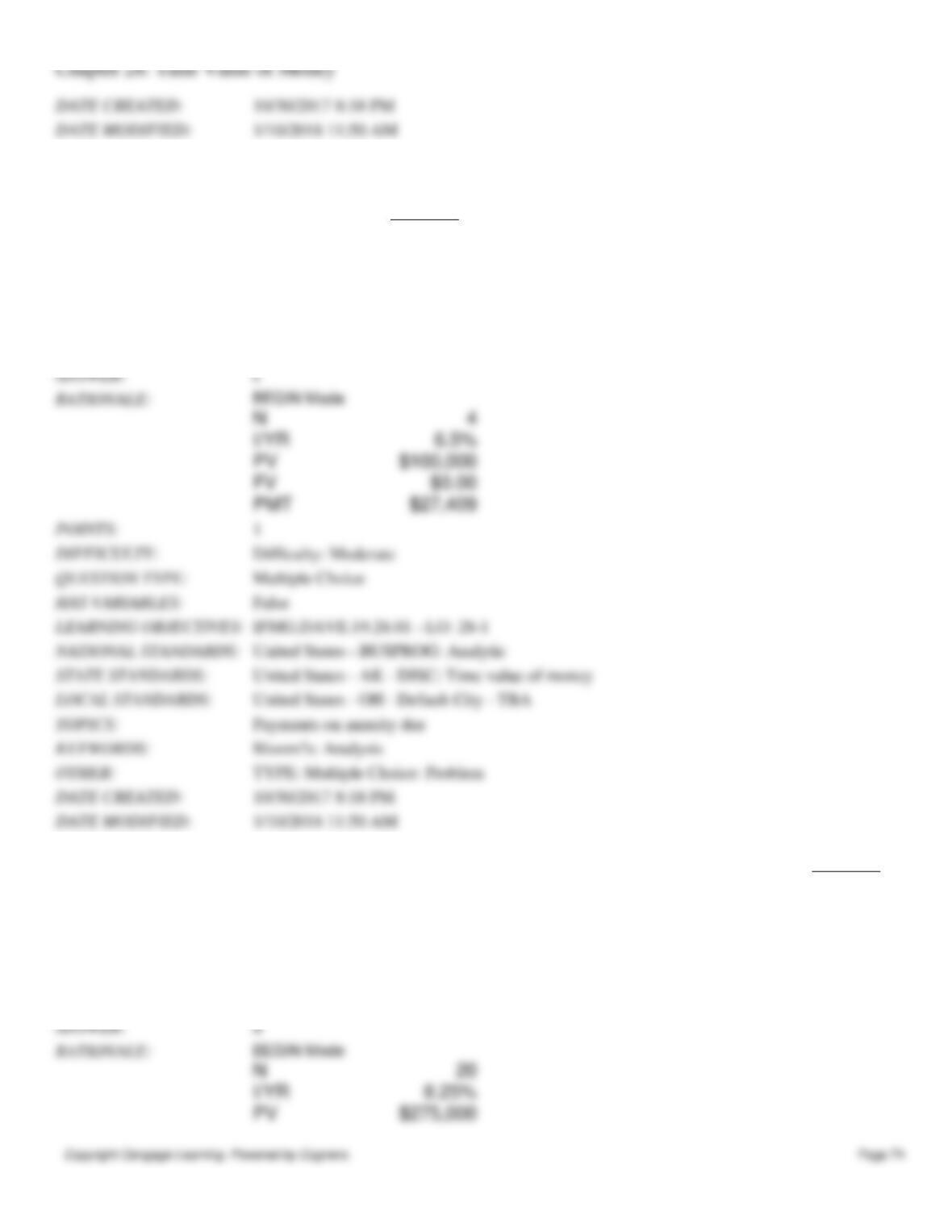

105. Suppose you are buying your first home for $145,000, and you have $15,000 for your down payment. You have

arranged to finance the remainder with a 30-year, monthly payment, amortized mortgage at a 6.5% nominal interest rate,

with the first payment due in one month. What will your monthly payments be?

a.

$741.57

b.

$780.60

c.

$821.69

d.

$862.77

e.

$905.91

ANSWER:

c

106. Your cousin will sell you his coffee shop for $250,000, with "seller financing," at a 6.0% nominal annual rate. The

terms of the loan would require you to make 12 equal end-of-month payments per year for 4 years, and then make an

additional final (balloon) payment of $50,000 at the end of the last month. What would your equal monthly payments be?

a.

$4,029.37

b.

$4,241.44

c.

$4,464.67

d.

$4,699.66

e.

$4,947.01

ANSWER:

e

107. Suppose you borrowed $14,000 at a rate of 10.0% and must repay it in 5 equal installments at the end of each of the

next 5 years. How much interest would you have to pay in the first year?

a.

$1,200.33

b.

$1,263.50

c.

$1,330.00

d.

$1,400.00

e.

$1,470.00

ANSWER:

d

108. You plan to borrow $35,000 at a 7.5% annual interest rate. The terms require you to amortize the loan with 7 equal

end-of-year payments. How much interest would you be paying in Year 2?

a.

$1,994.49

b.

$2,099.46

c.

$2,209.96

d.

$2,326.27

e.

$2,442.59

POINTS:

1

109. Your bank offers to lend you $100,000 at an 8.5% annual interest rate to start your new business. The terms require

you to amortize the loan with 10 equal end-of-year payments. How much interest would you be paying in Year 2?

a.

$7,531

b.

$7,927

c.

$8,323

d.

$8,740

e.

$9,177

POINTS:

1

110. Suppose you borrowed $15,000 at a rate of 8.5% and must repay it in 5 equal installments at the end of each of the

next 5 years. By how much would you reduce the amount you owe in the first year?

a.

$2,404.91

b.

$2,531.49

c.

$2,658.06

d.

$2,790.96

e.

$2,930.51

ANSWER:

b

111. Suppose you borrowed $15,000 at a rate of 8.5% and must repay it in 5 equal installments at the end of each of the

next 5 years. How much would you still owe at the end of the first year, after you have made the first payment?

a.

$10,155.68

b.

$10,690.19

c.

$11,252.83

d.

$11,845.09

e.

$12,468.51

ANSWER:

e

Copyright Cengage Learning. Powered by Cognero.

Page 68

112. Your business has just taken out a 1-year installment loan for $72,500 at a nominal rate of 11.0% but with equal end-

of-month payments. What percentage of the 2nd monthly payment will go toward the repayment of principal?

a.

73.67%

b.

77.55%

c.

81.63%

d.

85.93%

e.

90.45%

POINTS:

1

113. On January 1, 2016, your sister's pet supplies business obtained a 30-year amortized mortgage loan for $250,000 at a

nominal annual rate of 7.0%, with 360 end-of-month payments. The firm can deduct the interest paid for tax purposes.

What will the interest tax deduction be for 2016?

a.

$17,419.55

b.

$17,593.75

Chapter 28: Time Value of Money

Copyright Cengage Learning. Powered by Cognero.

Page 69

c.

$17,769.68

d.

$17,947.38

e.

$18,126.85

ANSWER:

a

114. Which of the following statements is CORRECT?

a.

Some of the cash flows shown on a time line can be in the form of annuity payments, but none can be uneven

amounts.

b.

A time line is not meaningful unless all cash flows occur annually.

c.

Time lines are useful for visualizing complex problems prior to doing actual calculations.

d.

Time lines cannot be constructed in situations where some of the cash flows occur annually but others occur

quarterly.

e.

Time lines cannot be constructed for annuities where the payments occur at the beginning of the periods.

Chapter 28: Time Value of Money

ANSWER:

c

115. Which of the following statements is CORRECT?

a.

Some of the cash flows shown on a time line can be in the form of annuity payments, but none can be uneven

amounts.

b.

A time line is not meaningful unless all cash flows occur annually.

c.

Time lines are not useful for visualizing complex problems prior to doing actual calculations.

d.

Time lines cannot be constructed in situations where some of the cash flows occur annually but others occur

quarterly.

e.

Time lines can be constructed for annuities where the payments occur at either the beginning or the end of the

periods.

ANSWER:

e

116. Which of the following statements is CORRECT?

a.

Time lines cannot be constructed where some of the payments constitute an annuity but others are unequal and

thus are not part of the annuity.

b.

A time line is not meaningful unless all cash flows occur annually.

c.

Time lines are not useful for visualizing complex problems prior to doing actual calculations.

d.

Time lines can be constructed to deal with situations where some of the cash flows occur annually but others

occur quarterly.

e.

Time lines can only be constructed for annuities where the payments occur at the end of the periods, i.e., for

ordinary annuities.

ANSWER:

d

117. Which of the following statements is CORRECT?

a.

A time line is not meaningful unless all cash flows occur annually.

b.

Time lines are not useful for visualizing complex problems prior to doing actual calculations.

c.

Time lines cannot be constructed to deal with situations where some of the cash flows occur annually but

others occur quarterly.

d.

Time lines can only be constructed for annuities where the payments occur at the end of the periods, i.e., for

ordinary annuities.

e.

Time lines can be constructed where some of the payments constitute an annuity but others are unequal and

thus are not part of the annuity.

ANSWER:

e

118. Suppose you earned a $275,000 bonus this year and invested it at 8.25% per year. How much could you withdraw at

the end of each of the next 20 years?

a.

$28,532

b.

$29,959

c.

$31,457

d.

$33,030

e.

$34,681

ANSWER:

a

119. Your aunt wants to retire and has $375,000. She expects to live for another 25 years and to earn 7.5% on her invested

funds. How much could she withdraw at the end of each of the next 25 years and end up with zero in the account?

a.

$28,843.38

b.

$30,361.46

c.

$31,959.43

d.

$33,641.50

e.

$35,323.58

ANSWER:

d

120. Your aunt wants to retire and has $375,000. She expects to live for another 25 years, and she also expects to earn

7.5% on her invested funds. How much could she withdraw at the beginning of each of the next 25 years and end up with

zero in the account?

a.

$28,243.21

b.

$29,729.70

c.

$31,294.42

d.

$32,859.14

e.

$34,502.10

ANSWER:

c

121. You were left $100,000 in a trust fund set up by your grandfather. The fund pays 6.5% interest. You must spend the

money on your college education, and you must withdraw the money in 4 equal installments, beginning immediately.

How much could you withdraw today and at the beginning of each of the next 3 years and end up with zero in the

account?

a.

$24,736

b.

$26,038

c.

$27,409

d.

$28,779

e.

$30,218

ANSWER:

c

122. Suppose you inherited $275,000 and invested it at 8.25% per year. How much could you withdraw at the beginning

of each of the next 20 years?

a.

$22,598.63

b.

$23,788.03

c.

$25,040.03

d.

$26,357.92

e.

$27,675.82

ANSWER:

d

123. Your uncle just won the weekly lottery, receiving $375,000, which he invested at a 7.5% annual rate. He now has

decided to retire, and he wants to withdraw $35,000 at the end of each year, starting at the end of this year. What is the

maximum number of whole payments that can be withdrawn before the account is exhausted, i.e., before the account

balance would become negative? (Hint: Round down to the nearest whole number.)

a.

22

b.

23

c.

24

d.

25

e.

26

POINTS:

1

Copyright Cengage Learning. Powered by Cognero.

Page 76

124. Your uncle has $300,000 invested at 7.5%, and he now wants to retire. He wants to withdraw $35,000 at the end of

each year, beginning at the end of this year. He also wants to have $25,000 left to give you when he ceases to withdraw

funds from the account. What is the maximum number of $35,000 withdrawals that he can make and still have at least

$25,000 left in the account? (Hint: If your solution for N is not an integer, round down to the nearest whole number.)

a.

12

b.

13

c.

14

d.

15

e.

16

POINTS:

1

125. Your Aunt Elsa has $500,000 invested at 6.5%, and she plans to retire. She wants to withdraw $40,000 at the

beginning of each year, starting immediately. What is the maximum number of whole payments that can be withdrawn

before the account is exhausted, i.e., before the account balance would become negative? (Hint: Round down to the

nearest whole number.)

a.

18

b.

19

c.

20

d.

21

e.

22

Chapter 28: Time Value of Money

POINTS:

1

126. Your aunt has $500,000 invested at 5.5%, and she now wants to retire. She wants to withdraw $45,000 at the

beginning of each year, beginning immediately. When she makes her last withdrawal (at the beginning of a year), she also

wants to have enough left in the account so that you can make a final withdrawal of $50,000 at the end of that year (her

last withdrawal is at the beginning of the year, your withdrawal is at the end of that same year). What is the maximum

number of $45,000 withdrawals that she can make and still have enough in the account so that you can make a $50,000

withdrawal at the end of the year of her last withdrawal? (Hint: If your solution for N is not an integer, round down to the

nearest whole number.)

a.

13

b.

14

c.

15

d.

16

e.

17

POINTS:

1

127. Suppose you just won the state lottery, and you have a choice between receiving $2,550,000 today or a 20-year

annuity of $250,000, with the first payment coming one year from today. What rate of return is built into the annuity?

Disregard taxes.

a.

7.12%

b.

7.49%

c.

7.87%

d.

8.26%

e.

8.67%

ANSWER:

b

128. Your girlfriend just won the Florida lottery. She has the choice of $15,000,000 today or a 20-year annuity of

$1,050,000, with the first payment coming one year from today. What rate of return is built into the annuity?

a.

3.44%

b.

3.79%

c.

4.17%

d.

4.58%

e.

5.04%

ANSWER:

a

129. Assume that you own an annuity that will pay you $15,000 per year for 12 years, with the first payment being made

today. You need money today to open a new restaurant, and your uncle offers to give you $120,000 for the annuity. If you

sell it, what rate of return would your uncle earn on his investment?

a.

6.85%

b.

7.21%

c.

7.59%

d.

7.99%

e.

8.41%

ANSWER:

e

Copyright Cengage Learning. Powered by Cognero.

Page 80

130. Your Green Investment Tips subscription is about to expire. You plan to subscribe to the magazine for the rest of

your life, and you can renew it by paying $85 annually, beginning immediately, or you can get a lifetime subscription for

$850, also payable immediately. Assuming that you can earn 6.0% on your funds and that the annual renewal rate will

remain constant, how many years must you live to make the lifetime subscription the better buy?

a.

7.48

b.

8.80

c.

10.35

d.

12.18

e.

14.33

ANSWER:

e

131. You agree to make 24 deposits of $500 at the beginning of each month into a bank account. At the end of the 24th

month, you will have $13,000 in your account. If the bank compounds interest monthly, what nominal annual interest rate

will you be earning?

a.

7.62%

b.

8.00%

c.

8.40%

d.

8.82%

e.

9.26%

ANSWER:

a