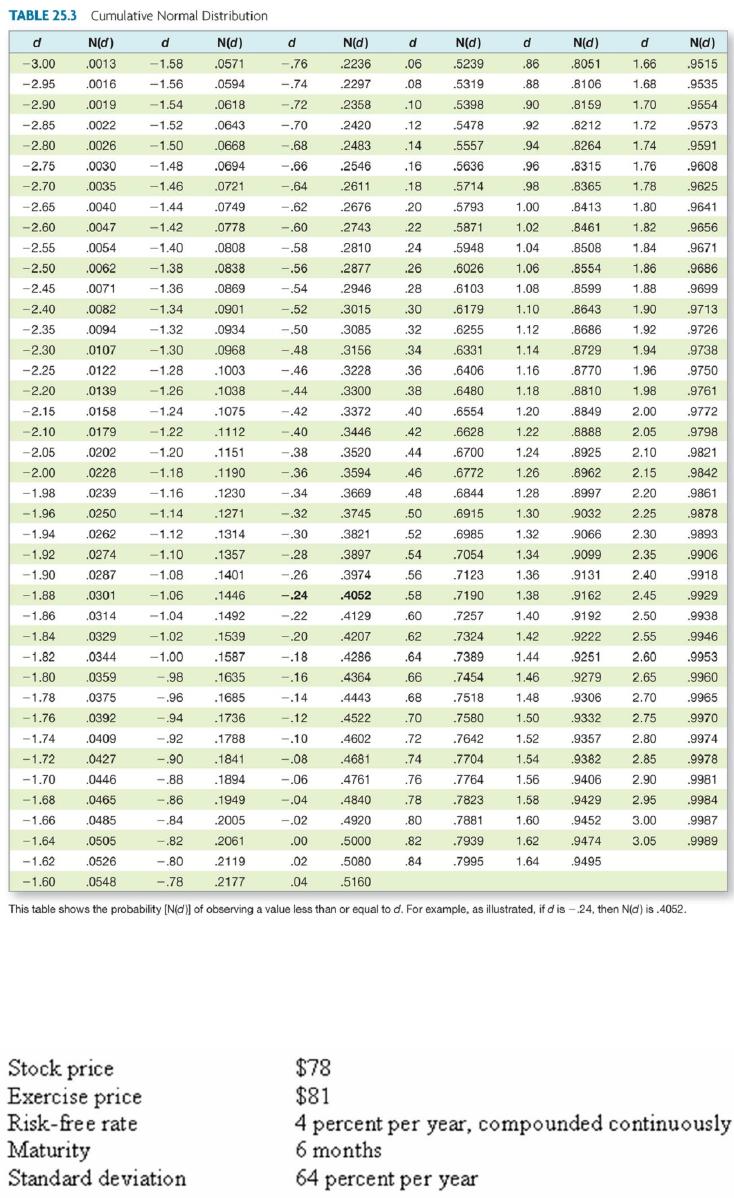

61.

What is the value of a 6-month call with a strike price of $25 given the

Black-Scholes option pricing model and the following information?

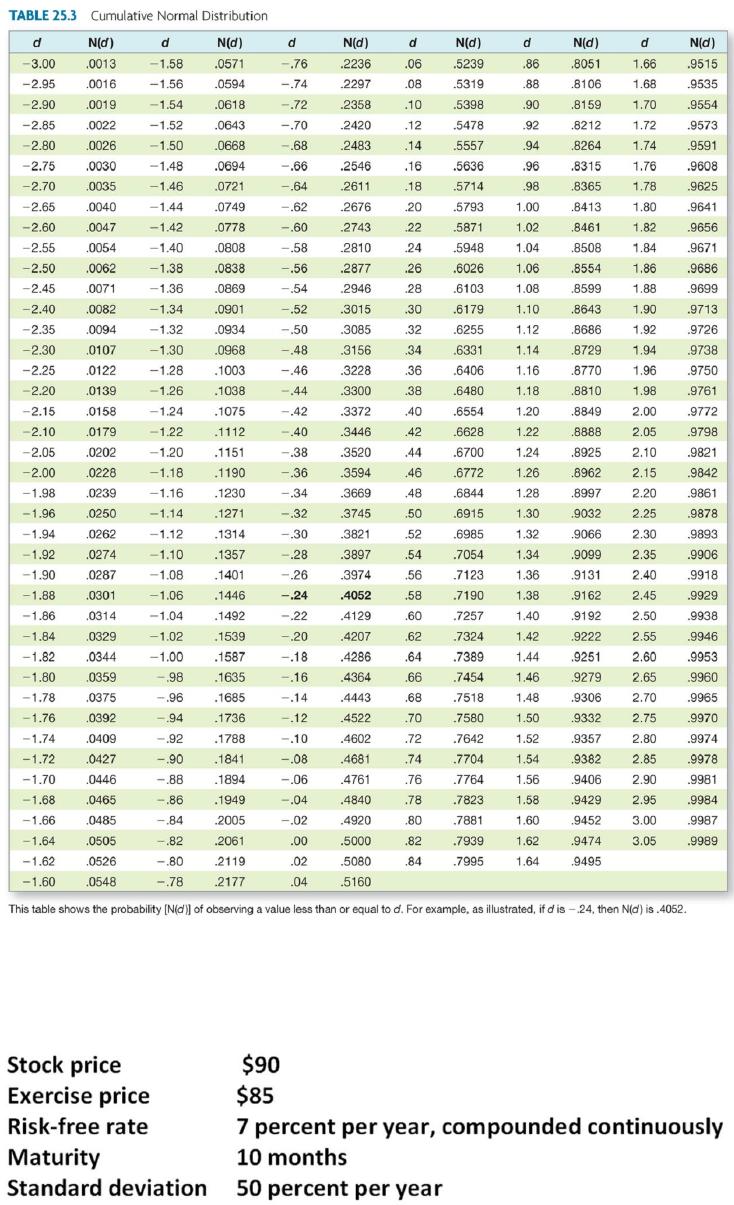

62.

What is the value of a 6-month put with a strike price of $27.25 given the

Black-Scholes option pricing model and the following information?

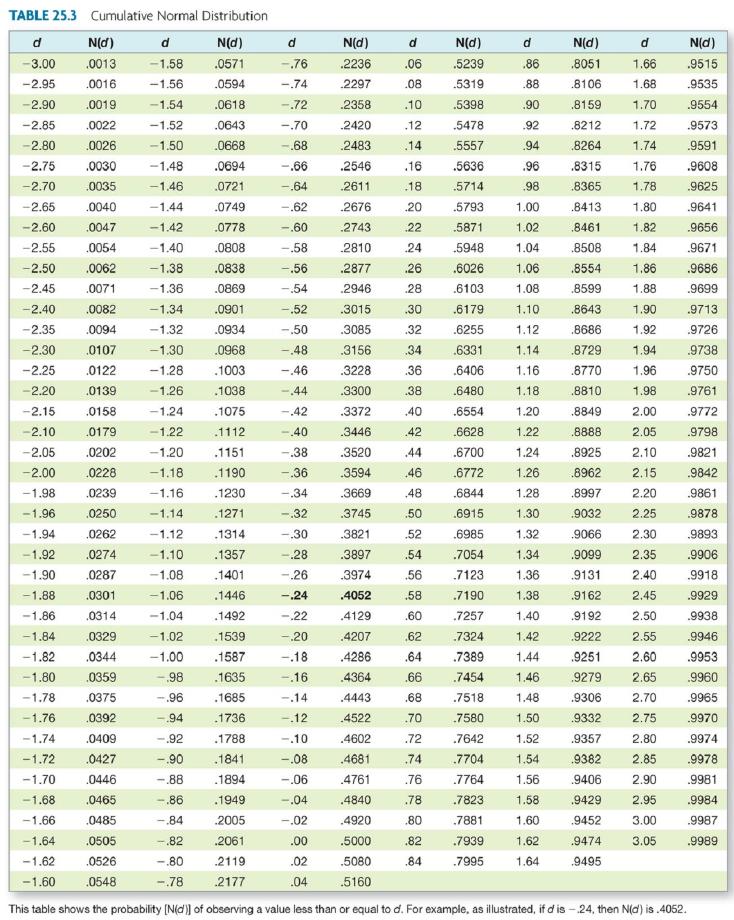

63.

What is the value of a 3-month put with a strike price of $45 given the

Black-Scholes option pricing model and the following information?

64.

A stock is currently selling for $56 a share. The risk-free rate is 3 percent

and the standard deviation is 18 percent. What is the value of d1 of a 9-

month call option with a strike price of $57.50?

65.

A stock is currently selling for $36 a share. The risk-free rate is 3.8 percent

and the standard deviation is 27 percent. What is the value of d1 of a 9-

month call option with a strike price of $40?

66.

The delta of a call option on a firm’s assets is 0.767. This means that a

$75,000 project will increase the value of equity by:

67.

The delta of a call option on a firm’s assets is 0.727. This means that a

$195,000 project will increase the value of equity by:

68.

The current market value of the assets of Smethwell, Inc. is $54 million,

with a standard deviation of 16 percent per year. The firm has zero-coupon

bonds outstanding with a total face value of $40 million. These bonds

mature in 2 years. The risk-free rate is 4 percent per year compounded

continuously. What is the value of d1?

69.

The current market value of the assets of Cristopherson Supply is $46.5

million. The market value of the equity is $28.7 million. The risk-free rate is

4.75 percent and the outstanding debt matures in 4 years. What is the

market value of the firm’s debt?

70.

The current market value of the assets of Nano Tek is $19.5 million. The

market value of the equity is $7.5 million. The risk-free rate is 4.5 percent

and the outstanding debt matures in 5 years. What is the market value of

the firm’s debt?

71.

You need $12,000 in 6 years. How much will you need to deposit today if

you can earn 11 percent per year, compounded continuously? Assume this

is the only deposit you make.

72.

A stock is selling for $60 per share. A call option with an exercise price of

$65 sells for $3.31 and expires in 4 months. The risk-free rate of interest is

2.8 percent per year, compounded continuously. What is the price of a put

option with the same exercise price and expiration date?

73.

A put option that expires in eight months with an exercise price of $57 sells

for $3.85. The stock is currently priced at $59, and the risk-free rate is 3.1

percent per year, compounded continuously. What is the price of a call

option with the same exercise price and expiration date?

74.

What is the price of a put option given the following information?

75.

What is the delta of a put option given the following information?

76.

You own a lot in Key West, Florida, that is currently unused. Similar lots

have recently sold for $1.2 million. Over the past five years, the price of land

in the area has increased 10 percent per year, with an annual standard

deviation of 19 percent. A buyer has recently approached you and wants an

option to buy the land in the next 9 months for $1,310,000. The risk-free

rate of interest is 7 percent per year, compounded continuously. How much

should you charge for the option?

(Round your answer to the nearest