Financial Markets and Institutions, 8e (Mishkin)

Chapter 23 Risk Management in Financial Institutions

23.1 Multiple Choice

1) Banks face the problem of ________ in loan markets because bad credit risks are the ones

most likely to seek bank loans.

A) adverse selection

B) moral hazard

C) moral suasion

D) intentional fraud

2) If borrowers with the most risky investment projects are more likely to seek bank loans than

borrowers with the safest investment projects, banks face the problem of ________.

A) adverse credit risk

B) adverse selection

C) moral hazard

D) conflict of interest

3) Because borrowers, once they have a loan, are more likely to invest in high-risk investment

projects, banks face the

A) adverse selection problem.

B) lemon problem.

C) adverse credit risk problem.

D) moral hazard problem.

4) Banks’ attempts to solve adverse selection and moral hazard problems help explain loan

management principles such as

A) screening and monitoring of loan applicants.

B) collateral and compensating balances.

C) credit rationing.

D) all of the above.

E) only A and B of the above.

5) To be profitable, financial institutions must overcome the adverse selection and moral hazard

problems that make loan defaults ________.

A) more likely

B) certain

C) unlikely

D) impossible

6) In one sense, ________ appears surprising since it means that the bank is not ________ its

portfolio of loans and thus is exposing itself to more risk.

A) specialization in lending; diversifying

B) specialization in lending; rationing

C) credit rationing; diversifying

D) screening; rationing

7) From the standpoint of ________, specialization in lending is surprising but makes perfect

sense when one considers the ________ problem.

A) moral hazard; diversification

B) diversification; moral hazard

C) adverse selection; diversification

D) diversification; adverse selection

8) Provisions in loan contracts that proscribe borrowers from engaging in specified risky

activities are called ________.

A) proscription bonds

B) collateral clauses

C) restrictive covenants

D) liens

9) Banks attempt to screen good credit risks from bad to reduce the incidence of loan defaults.

To do this, banks

A) specialize in lending to certain industries or regions.

B) write restrictive covenants into loan contracts.

C) expend resources to acquire accurate credit histories of their potential loan customers.

D) do all of the above.

10) A bank’s commitment (for a specified future period of time) to provide a firm with loans up

to a given amount at an interest rate that is tied to a market interest rate is called

A) credit rationing.

B) a line of credit.

C) continuous dealings.

D) none of the above.

11) Lines of credit and long-term relationships between banks and their customers

A) reduce the costs of information collection.

B) make it easier for banks to screen good risks from bad.

C) enable banks to deal with moral hazard contingencies that are neither anticipated nor specified

in restrictive covenants.

D) do all of the above.

E) do only A and B of the above.

12) Compensating balances

A) are a particular form of collateral commonly required on commercial loans.

B) are a required minimum amount of funds that a borrower (i.e., a firm receiving a loan) must

keep in a checking account at the bank.

C) allow banks to monitor firms’ check payment practices, which can yield information about

their borrowers’ financial conditions.

D) are all of the above.

13) A bank that wants to monitor the check payment practices of its commercial borrowers, so

that moral hazard can be prevented, will require borrowers to

A) place a bank officer on their board of directors.

B) place a corporate officer on the bank’s board of directors.

C) keep compensating balances in a checking account at the bank.

D) do all of the above.

E) do only A and B of the above.

14) Of the following methods that banks might use to reduce moral hazard problems, the one not

legally permitted in the United States is the requirement that

A) firms keep compensating balances at the banks from which they obtain their loans.

B) firms place on their board of directors an officer from the bank.

C) loan contracts include restrictive covenants.

D) individuals provide detailed credit histories to bank loan officers.

15) When a lender refuses to make a loan, although borrowers are willing to pay the stated

interest rate or even a higher rate, it is said to engage in ________.

A) constrained lending

B) strategic refusal

C) credit rationing

D) collusive behavior

16) When a lender refuses to make a loan, even though borrowers are willing to pay the stated

interest rate or even a higher rate, it is said to engage in ________.

A) specialized lending

B) strategic refusal

C) diversified lending

D) coercive behavior

E) none of the above

17) Credit rationing occurs when a bank

A) refuses to make a loan of any amount to a borrower, even when she is willing to pay a higher

interest rate.

B) restricts the amount of a loan to less than the borrower would like.

C) does either A or B of the above.

D) does neither A nor B of the above.

18) Because larger loans create greater incentives for borrowers to engage in undesirable

activities that make it less likely they will repay the loans, banks

A) ration credit, granting borrowers smaller loans than they have requested.

B) ration credit, charging higher interest rates to borrowers who want large loans than to those

who want small loans.

C) ration credit, charging higher fees as a percentage of the loan to borrowers who want large

loans than to those who want small loans.

D) do none of the above.

19) When banks offer borrowers smaller loans than they have requested, banks are said to

________.

A) shave credit

B) discount the loan

C) raze credit

D) ration credit

20) Which of the following are not generally rate-sensitive assets?

A) Securities with a maturity of less than one year

B) Variable-rate mortgages

C) Fixed-rate mortgages

D) All of the above are rate-sensitive assets

E) None of the above are rate-sensitive assets

21) Liabilities that are partially, but not fully, rate-sensitive include ________.

A) checkable deposits

B) federal funds

C) non-negotiable CDs

D) fixed-rate mortgages

E) money market deposit accounts

22) If a bank has more rate-sensitive liabilities than rate-sensitive assets, then a(n) ________ in

interest rates will ________ bank profits.

A) increase; increase

B) increase; reduce

C) decline; reduce

D) decline; not affect

23) If a bank has more rate-sensitive assets than rate-sensitive liabilities, then a(n) ________ in

interest rates will ________ bank profits.

A) increase; increase

B) increase; reduce

C) decline; increase

D) decline; not affect

24) If a bank has ________ rate-sensitive assets than rate-sensitive liabilities, then a(n) ________

in interest rates will increase bank profits.

A) more; decline

B) more; increase

C) less; increase

D) both A and C

25) The difference between rate-sensitive liabilities and rate-sensitive assets is known as the

________.

A) duration

B) interest-sensitivity index

C) interest-rate risk index

D) gap

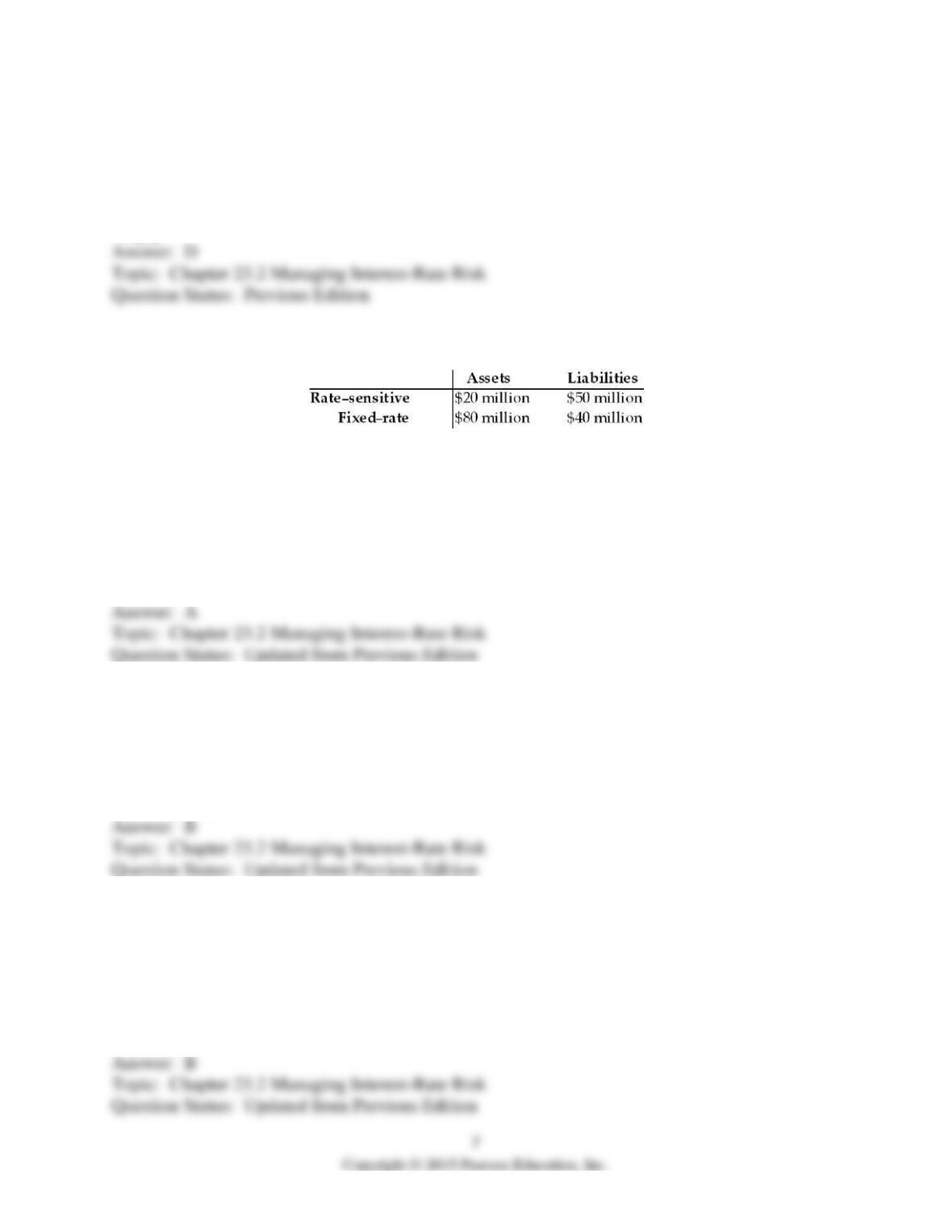

First National Bank

Table 23.1

26) Referring to Table 23.1, First National Bank has a gap of ________.

A) -30

B) +30

C) 60

D) 0

27) Referring to Table 23.1, if interest rates rise by 5 percentage points, then bank profits

(measured using gap analysis) will

A) decline by $0.5 million.

B) decline by $1.5 million.

C) decline by $2.5 million.

D) increase by $1.5 million.

28) Refer to Table 23.1. Assuming that the average duration of its assets is five years, while the

average duration of its liabilities is three years, a rise in interest rates from 5% to 10% will cause

the net worth of First National to ________ by ________ of the total original asset value.

A) increase; 11%

B) decline; 11%

C) increase; 10%

D) decline; 5%

First National Bank

Table 23.2

29) Referring to Table 23.2, First National Bank has a gap of ________.

A) -10

B) 10

C) 20

D) 0

30) Referring to Table 23.2, if interest rates rise by 5 percentage points, then bank profits

(measured using gap analysis) will

A) decline by $0.5 million.

B) decline by $1.5 million.

C) decline by $2.5 million.

D) increase by $2.0 million.

31) Refer to Table 23.2. Assuming that the average duration of the bank’s assets is four years,

while the average duration of its liabilities is three years, a rise in interest rates from 5 percent to

10 percent will cause the net worth of First National to ________ by ________ of the total

original asset value.

A) decline; 5%

B) decline; 1.3%

C) decline; 6.2%

D) increase; 5%

32) If First State Bank has a gap equal to a positive $20 million, then a 5 percentage point drop

in interest rates will cause profits to

A) increase by $10 million.

B) increase by $1.0 million.

C) decline by $10 million.

D) decline by $1.0 million.

33) If First National Bank has a gap equal to a negative $30 million, then a 5 percentage point

increase in interest rates will cause profits to

A) increase by $15 million.

B) increase by $1.5 million.

C) decline by $15 million.

D) decline by $1.5 million.

34) Measuring the sensitivity of bank profits to changes in interest rates by multiplying the gap

times the change in the interest rate is called ________.

A) basic duration analysis

B) basic gap analysis

C) interest-exposure analysis

D) gap-exposure analysis

35) Measuring the sensitivity of bank profits to changes in interest rates by multiplying the gap

for several maturity subintervals by the change in the interest rate is called

A) basic gap analysis.

B) the segmented maturity approach to gap analysis.

C) the maturity bucket approach to gap analysis.

D) the segmented maturity approach to interest-exposure analysis.

E) none of the above.

36) Duration gap analysis

A) is a refinement of basic gap analysis that accounts for interest-rate changes over a multiyear

period.

B) is a refinement of basic gap analysis that accounts for how long a gap will last.

C) is a complement to basic gap analysis that accounts for the effect of interest rate changes on

market value.

D) is a complement to basic gap analysis that accounts for the influence of partially rate-sensitive

assets.

37) Duration analysis involves comparing the average duration of the bank’s ________ to the

average duration of its ________.

A) securities portfolio; nondeposit liabilities

B) loan portfolio; nondeposit liabilities

C) loan portfolio; rate-sensitive liabilities

D) rate-sensitive assets; rate-sensitive liabilities

E) assets; liabilities

38) To use the concept of duration to analyze the effect of changes in interest rates on the market

value of an asset, a bank manager would multiply

A) the negative of the duration of the asset by the change in the interest rate, Δi.

B) the negative of the duration of the asset by Δi /(1 + i).

C) the duration of the asset by the change in the interest rate, Δi.

D) the duration of the asset by Δi /(1 + i).

39) If a bank has a duration gap of 2 years, then a rise in interest rates from 6 percent to 9 percent

will lead to

A) a rise in the market value of its net worth of 5.66 percent.

B) a rise in net interest income of 5.66 percent.

C) a fall in the market value of its net worth of 5.66 percent.

D) a fall in net interest income of 5.66 percent.

E) an unknown change.

40) If a bank has a duration gap of 2 years, then a fall in interest rates from 6 percent to 3 percent

will lead to

A) a rise in the market value of its net worth of 5.66 percent.

B) a fall in the market value of its net worth of 5.66 percent.

C) a rise in net interest income of 5.66 percent.

D) a fall in net interest income of 5.66 percent.

E) an unknown change.

41) If a decline in interest rates causes the market value of a bank’s net worth to rise, then the

bank must have a ________.

A) negative duration gap

B) positive duration gap

C) negative gap

D) positive gap

42) If a rise in interest rates causes the market value of a bank’s net worth to rise, then the bank

must have a ________.

A) negative duration gap

B) positive duration gap

C) negative gap

D) positive gap

43) One problem with duration gap analysis is that it

A) is calculated assuming that the yield curve is flat.

B) is calculated assuming that the yield curve does not change.

C) does not measure the sensitivity of net worth to interest rate changes.

D) does not measure the sensitivity of income to interest rate changes.

E) applies only to financial institutions.

44) One problem with basic gap analysis is that it

A) is calculated assuming interest rates on all maturities are equal.

B) is calculated assuming interest rates on all maturities change by equal amounts.

C) measures the sensitivity of net worth to interest rate changes.

D) does not measure the sensitivity of income to interest rate changes.

E) applies only to financial institutions.

45) A bank manager concerned about interest income who expects interest rates to rise and who

knows the bank currently has a positive gap should ________ rate-sensitive assets and ________

rate-sensitive liabilities.

A) increase; increase

B) decrease; increase

C) decrease; decrease

D) increase; decrease

46) A bank manager concerned about interest income who expects interest rates to fall and who

knows the bank currently has a positive gap should ________ rate-sensitive assets and ________

rate-sensitive liabilities.

A) increase; increase

B) decrease; increase

C) decrease; decrease

D) increase; decrease

23.2 True/False

1) If a bank has more rate-sensitive liabilities than assets, then an increase in interest rates will

reduce bank profits.

2) The difference between rate-sensitive liabilities and rate-sensitive assets is known as the

duration gap.

3) If a bank has a negative gap, then a decrease in interest rates will increase income.

4) Banks face the problem of adverse selection in loan markets because bad credit risks are the

ones most likely to seek bank loans.

5) Effective screening and information collection together form an important principle of credit

risk management.

6) Deciding on how good a risk you is entirely scientific, based on your credit score.

7) Credit rationing reduces adverse selection problems.

8) Credit rationing occurs when lenders charge higher interest rates on the loans they make to

riskier borrowers.

9) Developing and maintaining long-term customer relationships help to reduce banks’ costs of

screening and monitoring borrowers.

10) Measuring the sensitivity of bank profits to changes in interest rates by multiplying the gap

for several maturity subintervals by the change in the interest rate is called duration analysis.

11) If interest rates rise by 5 percentage points, then bank profits (measured using gap analysis)

will increase regardless of the income gap.

12) Income gap analysis and duration gap analysis are basically the same thing, so hedging

against one gap automatically hedges against the other.

23.3 Essay

1) What is the difference between credit risk and interest-rate risk?

2) How is credit risk related to the concepts of adverse selection and moral hazard?

3) What steps do banks take to reduce their exposure to credit risk?

4) How do the concepts of adverse selection and moral hazard explain the credit risk

management principles that banks adopt?

5) What is gap analysis and why is it important to a bank?

6) What is duration gap analysis and why is it important to a bank?

7) Explain how banks benefit from long-term customer relationships.

8) Explain how banks benefit from specialization in lending.

9) What special assumptions do income and duration gap analyses make about interest rate

changes and the yield curve?

10) What is the difference between income gap analysis and duration gap analysis?

11) Discuss some of the problems in using income gap and duration gap analysis to manage

interest rate risk in a financial institution.