Chapter 21: Mergers True/False Page 679

(Difficulty Levels: Easy, Easy/Medium, Medium, Medium/Hard, and Hard)

Please see the preface for information on the AACSB letter indicators (F, M, etc.) on the subject

lines.

Multiple Choice: True/False

1

. In a merger with true synergies, the post-merger value exceeds the sum

of the separate companies’ pre-merger values.

a. True

b. False

2

. Synergistic benefits can arise from a number of different sources,

including operating economies of scale, financial economies, and

increased managerial efficiency.

a. True

b. False

3

. Most defensive mergers occur as a result of managers’ actions to

maximize shareholders’ wealth.

a. True

b. False

4

. A conglomerate merger occurs when two firms with either a horizontal or

a vertical business relationship combine.

a. True

b. False

5

. Merger activity is likely to heat up when interest rates are high

because target firms can expect to receive an especially high premium

over the pre-announcement stock price.

a. True

b. False

CHAPTER 21

MERGERS AND ACQUISITIONS

Page 680 True/False Chapter 21: Mergers

6

. A company seeking to fight off a hostile takeover might employ the

services of an investment banking firm to develop a defensive strategy.

a. True

b. False

7

. Post-merger control and the negotiated price paid by the acquirer are

two of the most important issues in the terms to merger agreements.

a. True

b. False

8

. Since the primary rationale for any operating merger is synergy, in

planning such mergers the development of accurate pro forma cash flows

is the single most important task.

a. True

b. False

9

. Borrowing funds on terms that would require immediate repayment of all

loans if the firm is acquired, selling off at bargain prices the assets

that originally made the firm a desirable target, and granting huge

“golden parachutes” that open if the firm is acquired are 3 procedures

used to defend against hostile takeovers. These strategies are known

as “poison pills.”

a. True

b. False

10

. A joint venture is one in which two, or sometimes more, independent

companies agree to combine resources in order to achieve a specific

objective, usually limited in scope.

a. True

b. False

11

. Leveraged buyouts (LBOs) occur when a firm’s managers, generally backed

by private equity groups, try to gain control of a publicly owned

company by buying shares in the company using large amounts of borrowed

money.

a. True

b. False

12

. A spin-off is a type of divestiture in which the assets of a division

are sold to another firm.

Chapter 21: Mergers True/False Page 681

a. True

b. False

Page 682 True/False Chapter 21: Mergers

13

. The purchase of assets at below their replacement cost and tax

considerations are two factors that motivate mergers.

a. True

b. False

14

. The primary reason given by managers for most mergers is the

acquisition of more assets so as to increase sales and market share.

a. True

b. False

15

. Since managers’ central goal is to maximize stock price, managers’

personal incentives do not interfere with mergers that would benefit

the target firm’s stockholders.

a. True

b. False

16

. If a petrochemical firm that used oil as feedstock merged with an oil

producer that had large oil reserves and a drilling subsidiary, this

would be a vertical merger.

a. True

b. False

17

. A congeneric merger is one where the merging firms operate in related

businesses but do not necessarily produce the same products or have a

producer-supplier relationship.

a. True

b. False

18

. One of the main reasons why foreign firms are interested in buying U.S.

companies is to gain entrance to the U.S. market. A decline in the

value of the dollar relative to most foreign currencies makes this

competitive strategy especially attractive.

a. True

b. False

19

. Since a manager’s central goal is to maximize the firm’s stock price,

any merger offer that provides stockholders with significant gains over

the current stock price will be approved by the current management

team.

a. True

Chapter 21: Mergers True/False Page 683

b. False

Page 684 True/False Chapter 21: Mergers

20

. Only if a target firm’s value is greater to the acquiring firm than its

market value as a separate entity will a merger be financially

justified.

a. True

b. False

21

. Discounted cash flow methods are not appropriate for evaluating mergers

because the cash flows are uncertain and the discount rate can only be

determined after the merger is consummated.

a. True

b. False

22

. In a financial merger, the relevant post-merger cash flows are simply

the sum of the expected cash flows of the two companies, measured as if

they were operated independently.

a. True

b. False

23

. The rate used to discount projected merger cash flows should be the

overall cost of capital of the new consolidated firm because it

incorporates the actual capital structure of the new firm.

a. True

b. False

24

. The distribution of synergistic gains between the stockholders of two

merged firms is almost always based strictly on their respective market

values before the announcement of the merger.

a. True

b. False

25

. The value of the target firm is calculated by discounting residual cash

flows that belong to the acquiring firm’s shareholders at the target’s

cost of equity reflecting any changes to its capital structure as a

result of the merger.

a. True

b. False

Chapter 21: Mergers Conceptual M/C Page 685

Multiple Choice: Conceptual

26

. The text gives a number of valid, acceptable reasons for companies to

merge. Which of the following is NOT acceptable?

a. Synergistic benefits arising from mergers.

b. Reduction in competition resulting from mergers.

c. Acquisition of assets at below replacement value.

d. Attempts to minimize taxes by acquiring a firm with large

accumulated losses that can be used immediately.

e. Using surplus cash to acquire another firm and prevent unfavorable

tax consequences for shareholders.

27

. Firms use defensive tactics to fight off undesired mergers. These

tactics do NOT include

a. raising antitrust issues.

b. developing poison pills.

c. getting white knights to bid for the firm.

d. repurchasing their own stock.

e. engaging in risk arbitrage.

28

. Which of the following actions does NOT help managers defend against a

hostile takeover?

a. Establishing a poison pill provision.

b. Granting lucrative golden parachutes to senior managers.

c. Establishing a super-majority provision in the company’s bylaws to

raise the percentage of the board of directors that must approve an

acquisition from 50% to 75%.

d. Retiring long-term debt early to reduce total debt on the balance

sheet which will increase the firm’s financial position.

e. Finding a “white squire” that will buy enough of the target firm’s

shares to block the hostile takeover.

29

. Which of the following statements is most CORRECT?

a. A conglomerate merger is one where a firm combines with another firm

in the same industry.

b. Regulations in the United States prohibit acquiring firms from using

common stock to purchase another firm.

c. Defensive mergers are designed to make a company less vulnerable to

a takeover.

d. The equity residual method values a target firm by discounting

residual cash flows at the acquiring firm’s overall cost of capital

reflecting the combined firm’s post-merger capital structure.

e. A financial merger occurs when the operations of the firms involved

are integrated in the hope of achieving synergistic benefits.

Page 686 Conceptual M/C Chapter 21: Mergers

30

. Which of the following statements is most CORRECT?

a. Tax considerations often play a part in mergers. If one firm has

excess cash, purchasing another firm exposes the purchasing firm to

additional taxes. Thus, firms with excess cash rarely undertake

mergers.

b. The smaller the synergistic benefits of a particular merger, the

greater the scope for striking a bargain in negotiations, and the

higher the probability that the merger will be completed.

c. Since mergers are frequently financed by debt rather than equity, a

lower cost of debt or a greater debt capacity are rarely relevant

considerations when considering a merger.

d. Managers who purchase other firms often assert that the new combined

firm will enjoy benefits from diversification, including more stable

earnings. However, since shareholders are free to diversify their

own holdings, and at what’s probably a lower cost, research of U.S.

firms suggests that in most cases, diversification through mergers

does not increase the firm’s value.

e. Research of U.S. firms suggests that managers’ personal motivations

have had little, if any, impact on firms’ decisions to merge.

31

. Which of the following statements is most CORRECT?

a. The high value of the U.S. dollar relative to Japanese and European

currencies in the 1980s, made U.S. companies comparatively

inexpensive to foreign buyers, spurring many mergers.

b. During the 1980s, the Reagan and Bush administrations tried to

foster greater competition and they were adamant about preventing

the loss of competition; thus, most large mergers were disallowed.

c. The expansion of the junk bond market made debt more freely

available for large acquisitions and LBOs in the 1980s, and thus, it

resulted in an increased level of merger activity.

d. Increased nationalization of business and a desire to scale down and

focus on producing in one’s home country has virtually halted cross–

border mergers today.

e. Because strategic alliances and joint ventures are easy to form and

enable firms to compete better in the global economy than would

mergers, merger activity has virtually come to a halt in the 21st

century.

32

. Which of the following statements is most CORRECT?

a. The acquiring firm’s required rate of return in most horizontal

mergers will not be affected, because the two firms will have

similar betas.

b. The goal of merger valuation is to value the target firm’s total

capital at the target firm’s weighted average cost of capital

because a firm is acquired from all of its investors–both

shareholders and creditors.

c. The basic rationale for any financial merger is synergy and, thus,

the estimation of pro forma cash flows is the single most important

part of the analysis.

Chapter 21: Mergers Conceptual M/C Page 687

d. In most mergers, the benefits of synergy and the premium the

acquirer pays over the market price are summed and then divided

equally between the shareholders of the acquiring and target firms.

e. The primary rationale for most operating mergers is synergy.

33

. Which of the following statements is most CORRECT?

a. Leveraged buyouts (LBOs) occur when a firm issues equity and uses

the proceeds to take a firm public.

b. In a typical LBO, bondholders do well but shareholders see their

value decline.

c. Firms are forbidden by law to sell any assets during the first five

years following a leverage buyout.

d. Not all target firms are acquired by publicly traded corporations.

In recent years, an increasing number of firms have been acquired by

private equity firms. Private equity firms raise capital from

wealthy individuals and look for opportunities to make profitable

investments.

e. In an LBO sometimes the acquiring group plans to run the acquired

company for a number of years, boost its sales and profits, and then

take it public again as a stronger company. In other instances, the

LBO firm plans to sell off divisions to other firms that can gain

synergies. In either case, the acquiring group expects to make a

substantial profit from the LBO, but the inherent risks are small

due to the heavy use of venture capital and very little debt.

34

. Which of the following statements is most CORRECT?

a. If a company that produces military equipment merges with a company

that manages a chain of motels, this is an example of a horizontal

merger.

b. A defensive merger is one where the firm’s managers decide to merge

with another firm to avoid or lessen the possibility of being

acquired through a hostile takeover.

c. Acquiring firms send a signal that their stock is undervalued if

they choose to use stock to pay for the acquisition.

d. In a liquidation, the firm’s existing stockholders are given new

stock representing separate ownership rights in the division that

was divested. The division establishes its own board of directors

and officers, and it becomes a separate company.

e. If there are no synergistic benefits to be gained from a merger, the

acquiring company will stop its plans for the merger. However, if

synergistic gains are large, plans for the merger will continue. In

fact, the greater the synergistic gains, the smaller the gap between

the target’s current price and the maximum the acquiring company

could pay because of the acquiring company’s upper hand in the

merger.

Page 688 M/C Problems Chapter 21: Mergers

Multiple Choice: Problems

35

. Simpson Inc. is considering a vertical merger with The Lachey Company.

Simpson currently has a required return of 11%, while Lachey’s required

return is 15%. The market risk premium is 5% and the risk-free rate is

5%. Assume the market is in equilibrium. If Simpson is going to make

up 67% of the new firm (and Lachey will comprise the remaining 33%),

what will be the beta of the new merged firm? There will be no

additional infusion of debt in the merger.

a. 1.46

b. 1.54

c. 1.61

d. 1.69

e. 1.78

36

. In early 2011 Ham Inc.’s management was considering making an offer to

buy Egg Corporation. Egg’s projected operating income (EBIT) for 2011

was $30 million, but Ham believes that if the two firms were merged, it

could consolidate some operations, reduce Egg’s expenses, and raise its

EBIT to $40 million. Neither company uses any debt, and they both pay

income taxes at a 40% rate. Ham has a better reputation among

investors, who regard it as better managed and also less risky, so

Ham’s stock has a P/E ratio of 15 versus a P/E of 12 for Egg. Since

Ham’s management will be running the entire enterprise after a merger,

investors will value the resulting corporation based on Ham’s P/E.

Based on expected market values, how much synergy should the merger

create?

a. $129.96

b. $136.80

c. $144.00

d. $151.20

e. $158.76

37

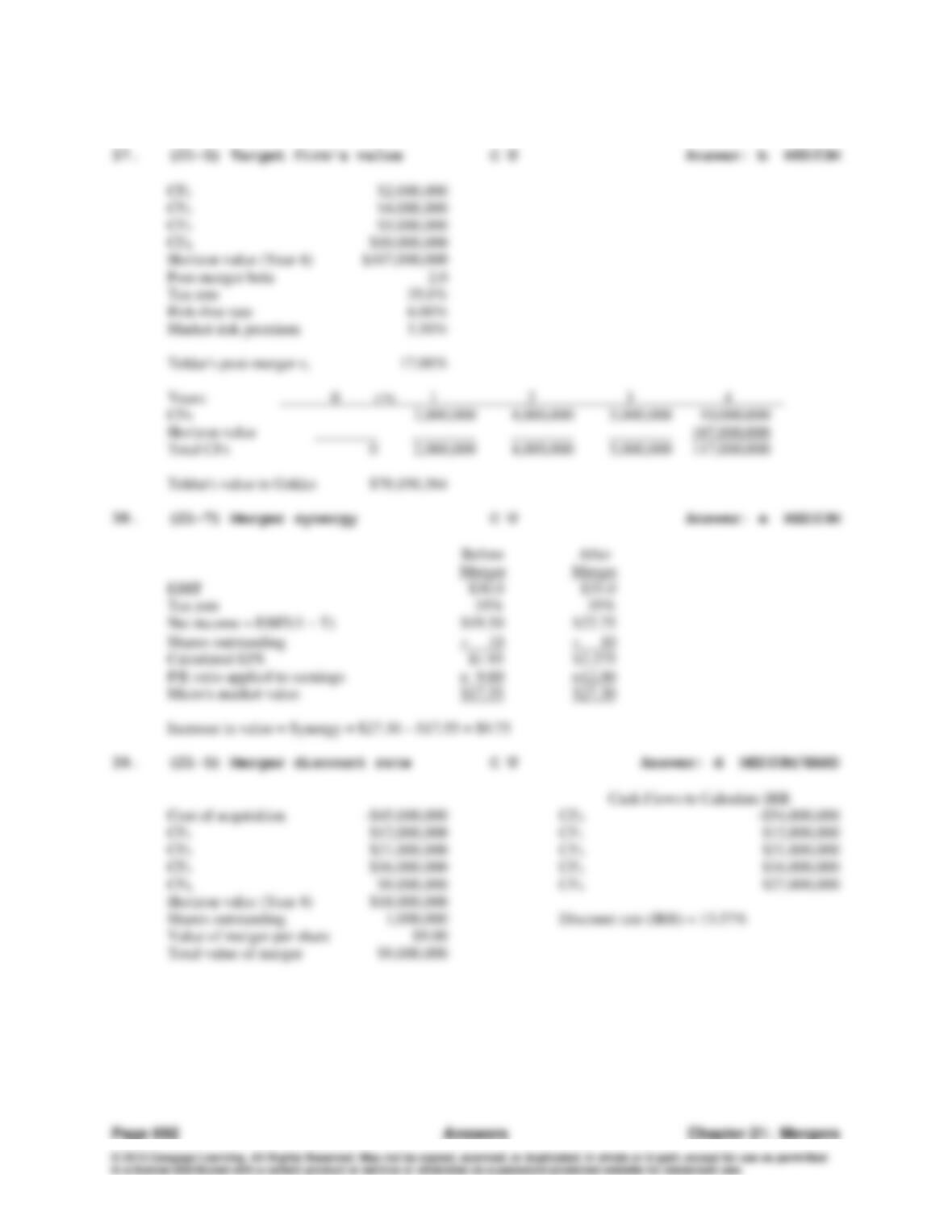

. Gekko Properties is considering purchasing Teldar Properties. Gekko’s

analysts project that the merger will result in incremental after-tax

cash flows of $2 million, $4 million, $5 million, and $10 million over

the next four years. The horizon value of the firm’s operations, as of

Year 4, is expected to be $107 million. Assume all cash flows occur at

the end of the year. The acquisition would be made immediately, if it

is undertaken. Teldar’s post-merger beta is estimated to be 2.0, and

its post-merger tax rate would be 35%. The risk-free rate is 6%, and

the market risk premium is 5.5%. What is the value of Teldar to Gekko

Properties?

a. $66,680,846

b. $70,190,364

c. $73,699,883

d. $77,384,877

e. $81,254,121

Chapter 21: Mergers M/C Problems Page 689

38

. In early 2011 Giant Inc.’s management was considering making an offer

to buy Micro Corporation. Micro’s projected operating income (EBIT)

for 2011 was $30 million, but Giant believes that if the two firms were

merged, it could consolidate some operations, reduce Micro’s expenses,

and raise its EBIT to $35 million. Neither company uses any debt, and

they both pay income taxes at a 35% rate. Giant has a better

reputation among investors, who regard it as very well managed and not

very risky, so its stock has a P/E ratio of 12 versus a P/E of 9 for

Micro. Since Giant’s management would be running the entire enterprise

after a merger, investors would value the resulting corporation based

on Giant’s P/E. If Micro has 10 million shares outstanding, by how

much should the merger increase its share price, assuming all of the

synergy will go to its stockholders?

a. $7.94

b. $8.36

c. $8.80

d. $9.26

e. $9.75

39

. Anacott Steel is acquiring Terafly Incorporated. Terafly is expected

to provide Anacott with operating cash flows of $12, $21, $16, and $9

million over the next four years, respectively. In addition, the

horizon value of all remaining cash flows at the end of Year 4 is

estimated at $18 million. The merger will cost Anacott $45.0 million

today. If the value of the merger is estimated at $9.00 per share and

Anacott has 1,000,000 shares outstanding, what equity discount rate

must the firm be using to value this acquisition?

a. 11.63%

b. 12.25%

c. 12.89%

d. 13.57%

e. 14.25%

Page 690 Answers Chapter 21: Mergers

CHAPTER 21

ANSWERS AND SOLUTIONS