Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-60

Solution 220 (25 min.)

Ex. 221

These items are taken from the financial statements of Drew Corporation for 2014.

Retained earnings (beginning of year) $33,000

Utilities expense 2,000

Equipment 56,000

Accounts payable 15,300

Cash 15,900

Salaries and wages payable 3,000

Common stock 13,000

Dividends 14,000

Service revenue 78,000

Prepaid insurance 3,500

Maintenance and repairs expense 1,800

Depreciation expense 3,300

Accounts receivable 14,200

Insurance expense 2,200

Salaries and wages expense 47,000

Accumulated depreciation—equipment 17,600

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-61

Ex. 221 (Cont.)

Instructions

Prepare an income statement and a retained earnings statement for the year ended December 31,

2014 and a classified balance sheet as of December 31, 2014.

Ans: N/A, LO: 1, 3, Bloom: AP, Difficulty: Medium, Min: 25, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Problem Solving, IMA: Reporting

Solution 221 (25 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-62

Solution 221 (Cont.)

Ex. 222

The Dobson Company gathered the following condensed data for the year ended December 31,

2014:

Cost of goods sold $ 720,000

Net sales 1,249,000

Administrative expenses 289,000

Interest expense 68,000

Dividends paid 38,000

Selling expenses 45,000

Instructions

Prepare an income statement for the year ended December 31, 2014.

Ans: N/A, LO: 2, Bloom: AP, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Solution 222 (10 min.)

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-63

Ex. 223

The following data are taken from the financial statements of Rosen, Inc. as of the end of the year

2014. The data are in alphabetical order.

Accounts payable $ 28,000 Net income $ 48,000

Accounts receivable 66,000 Other current liabilities 17,000

Cash 24,000 Salaries and wages payable 5,000

Gross profit 160,000 Total assets 250,000

Income before income taxes 54,000 Total liabilities 175,000

Additional information: The average common shares outstanding during the year was 40,000.

Instructions

Compute the following:

(a) Current ratio. (c) Earnings per share.

(b) Working capital. (d) Debts to assets ratio.

Ex. 224

Use the following data to calculate the liquidity and profitability ratios listed below.

Average common shares outstanding 10,000 Current liabilities $100,000

Capital expenditures $20,000 Net income 21,000

Cash provided by operating activities 32,000 Net sales 150,000

Dividends paid 5,000 Total liabilities 126,000

Current assets 190,000 Total assets 210,000

Instructions

Compute the following:

(a) Current ratio. (d) Debt to assets ratio.

(b) Working capital. (e) Free cash flow.

(c) Earnings per share.

Ans: N/A, LO: 2, 4, 5 Bloom: AP, Difficulty: Medium, Min: 15, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Problem Solving, IMA: Business Economics

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-64

Solution 224 (15 min.)

Ex. 225

The following data are taken from the financial statements of Edington Company. The data

are in alphabetical order.

Accounts payable $ 28,000 Net sales 500,000

Accounts receivable 65,000 Other current liabilities 20,000

Average common shares out. 20,000 Salaries and wages payable 7,000

Cash 56,000 Stockholders’ equity 135,000

Gross profit 190,000 Total assets 300,000

Net income 50,000

Instructions

Compute the following:

(a) Current ratio. (c) Earnings per share.

(b) Working capital. (d) Debt to assets ratio.

Ans: N/A, LO: 2, 4, Bloom: AP, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Problem Solving, IMA: Business Economics

Solution 225 (10 min.)

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-65

Ex. 226

Comparative financial statement data for Arthur Corporation and Lancelot Corporation, two

competitors, appear below. All balance sheet data are as of December 31, 2014.

Arthur Corporation Lancelot Corporation

2014 2014

Net sales $1,850,000 $620,000

Cost of goods sold 1,225,000 365,000

Operating expenses 303,000 98,000

Interest expense 9,000 3,800

Income tax expense 85,000 36,800

Current assets 427,200 130,336

Plant assets (net) 532,000 139,728

Current liabilities 66,325 35,348

Long-term liabilities 148,500 29,620

Additional Information:

Cash from operating activities $153,000 $44,000

Capital expenditures $90,000 $20,000

Dividends paid $36,000 $15,000

Average number of shares outstanding 100,000 50,000

Instructions

(a) Comment on the relative profitability of the companies by computing the net income and

earnings per share for each company for 2014.

(b) Comment on the relative solvency of the companies by computing the debt to assets ratio

and the free cash flow for each company for 2014.

Ans: N/A, LO: 2, 4, 5, Bloom: AN, Difficulty: Medium, Min: 15, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Problem Solving, IMA: Business Economics

Solution 226 (15 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-66

Solution 226 (Cont.)

Ex. 227

For each of the ratios listed below, indicate by the appropriate code letter, whether it is a liquidity

ratio, a profitability ratio, or a solvency ratio.

Code:

L = Liquidity ratio

P = Profitability ratio

S = Solvency ratio

____ 1. Price-earnings ratio

____ 2. Free cash flow

____ 3. Debt to assets ratio

____ 4. Earnings per share

____ 5. Current ratio

Ans: N/A, LO: 2, 4, 5, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Business Economics

Solution 227 (5 min.)

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-67

Ex. 228

The following information is available from the annual reports of Marin Company and Nance

Company.

(amounts in millions)

Marin Nance

Sales $26,510 $34,512

Gross profit 6,610 8,887

Net income 565 1,221

Current assets 13,712 28,447

Beginning total assets 17,102 33,130

Ending total assets 22,088 36,167

Current liabilities 7,966 13,950

Total liabilities 16,136 29,222

Average common shares outstanding 250 480

Preferred stock dividends paid -0- -0-

Instructions

(a) For each company, compute the following ratios:

1. Current ratio

2. Debt to assets ratio

3. Earnings per share

(b) Based on your calculations, discuss the relative liquidity, solvency, and profitability of the two

companies.

Ans: N/A, LO: 2, 4, Bloom: AP, Difficulty: Medium, Min: 12, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Problem Solving, IMA: Business Economics

Solution 228 (12 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

2-68

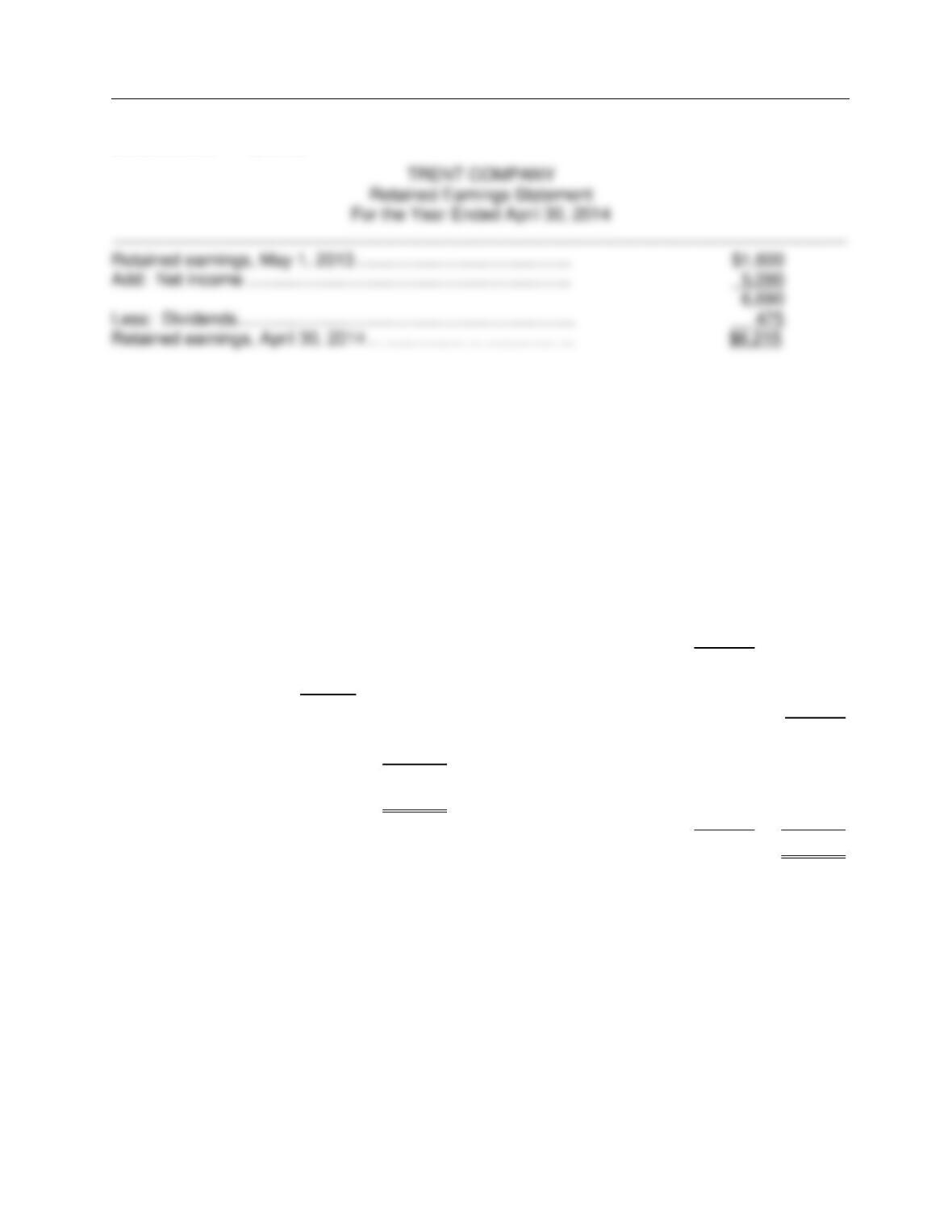

Ex. 229

You are provide with the following information for Trent Company, effective as of its April 30,

2014, year-end.

Accounts payable $ 834

Accounts receivable 810

Buildings, net of accumulated depreciation 3,537

Cash 770

Common stock 900

Cost of goods sold 2,500

Current portion of long-term debt 450

Depreciation expense 335

Dividends paid during the year 475

Equipment, net of accumulated depreciation 1,220

Income tax expense 265

Income taxes payable 265

Interest expense 400

Inventory 967

Land 1,600

Long-term debt 3,500

Prepaid expenses 12

Retained earnings, beginning 1,600

Service revenue 9,600

Selling expenses 310

Debt investments 1,200

Salaries and wages expense 700

Salaries and wages payable 222

Instructions

Prepare an income statement and a retained earnings statement for Trent Company for the year

ended April 30, 2014.

Ans: N/A, LO: 3, Bloom: AP, Difficulty: Medium, Min: 15, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Reporting

Solution 229 (15 min.)

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-69

Solution 229 (Cont.)

Ex. 230

The chief financial officer (CFO) of SuperClean Corporation requested that the accounting

department prepare a preliminary balance sheet on December 30, 2014, so that the CFO could

get an idea of how the company stood. He knows that certain debt agreements with its creditors

require the company to maintain a current ration of at least 2:1. The preliminary balance sheet is

as follows.

SUPERCLEAN CORPORATION

Balance Sheet

December 30, 2014

Current assets

Current liabilities

Cash

$25,000

Accounts payable

$ 20,000

Accounts receivable

20,000

Salaries and wages

payable

10,000

$ 40,000

Prepaid insurance

15,000

$ 60,000

Long-term liabilities

Notes payable

90,000

Total liabilities

130,000

Property, plant, and equipment

(net)

210,000

Stockholders' equity

Total assets

$270,000

Common stock

100,000

Retained earnings

40,000

140,000

Total liabilities and

stockholders equity

$270,000

Instructions

(a) Calculate the current ratio and working capital based on the preliminary balance sheet.

(b) Based in the results in (a), the CFO requested that $20,000 of cash be used to pay off the

balance of the accounts payable account on December 31, 2014. Calculate the new current

ratio and working capital after the company takes these actions.

Ans: N/A, LO: 4, Bloom: AN, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA PC:

Problem Solving, IMA: Business Economics

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

2-70

COMPLETION STATEMENTS

231. The rules and practices that are recognized as general guides for financial reporting are

called ______________ _____________ _______________.

232. In accounting, ____________ results when different companies use the same accounting

principles.

233. _______________ is a company-specific aspect of relevance where size is likely to

influence the decision of an investor or creditor.

234. The _______________ constraint relates to the fact that providing information is costly.

235. The earnings per share value is calculated by dividing net income – preferred stock

dividends by _______________ ______________ ______________.

236. Assets that are expected to be converted to cash or used in the business within a relatively

short period of time are called ______________.

237. The ________________ is current assets divided by current liabilities.

A Further Look at Financial Statements

2-71

238. A measurement to provide additional insight regarding a company’s cash-generating ability

is _____________.

Answers to Completion Statements

MATCHING

239. Match the items below by entering the appropriate code letter in the space provided.

A. Relevance G. Working capital

B. Liquidity ratios H. Current ratio

C. Comparability I. Earnings per share

D. Consistency J. Solvency ratios

E. Intangible assets K. Economic entity assumption

F. Free cash flow L. Materiality

____ 1. Measures of the ability of the company to survive over a long period of time.

____ 2. Current assets divided by current liabilities.

____ 3. Information that has a bearing on a decision.

____ 4. Economic events can be identified with a particular unit of accountability.

____ 5. An item important enough to influence the decision of an investor or creditor.

____ 6. Same accounting principles and methods used from year to year within a company.

____ 7. Cash from operating activities less capital expenditures and cash dividends.

____ 8. Noncurrent assets that do not have physical substance.

____ 9. (Net income – preferred stock dividends) divided by average common shares

outstanding.

____ 10. Different companies using the same accounting principles.

____ 11. Measures of the short-term ability of the enterprise to pay its maturing obligations.

____ 12. The excess of current assets over current liabilities.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-72

Answers to Matching

SHORT-ANSWER ESSAY QUESTIONS

S-A E 240

Identify the two parts of stockholders' equity in a corporation and indicate the purpose of each.

Ans: N/A, LO: 1, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 240

S-A E 241

What do these classes of ratios measure?

(a) Liquidity ratios.

(b) Profitability ratios.

(c) Solvency ratios.

Ans: N/A, LO: 2,4, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting,

AICPA PC: Communication, IMA: Business Economics

Solution 241

S-A E 242

Give the definition of current assets, current liabilities and the current ratio.

Ans: N/A, LO: 1, 4, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting,

AICPA PC: Communication, IMA: Business Economics

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-73

Solution 242

S-A E 243

Are short-term creditors, long-term creditors, and stockholders primarily interested in the same

characteristics of a company? Explain.

Ans: N/A, LO: 2, 4, Bloom: C, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting,

AICPA PC: Communication, IMA: Business Economics

Solution 243

S-A E 244

Relevance and faithful representation are the fundamental qualities of useful information.

(a) Briefly define each term.

(b) Why are these characteristics important to users of financial statements?

Ans: N/A, LO: 7, Bloom: C, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 244

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-74

S-A E 245

You and the CEO of your company are waiting on an elevator. You are going to the 25th floor and

the CEO is going to the 35th floor. The CEO says “What is the difference between consistency

and comparability?” You have two minutes to respond. What will you say?

Ans: N/A, LO: 7, Bloom: C, Difficulty: Medium, Min: 2, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 245

S-A E 246

Comparability and consistency are enhancing qualities that make accounting information useful

for decision-making purposes. Briefly explain the difference between these two qualities and

explain how they are related to each other.

Ans: N/A, LO: 7, Bloom: C, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 246

S-A E 247

Identify and briefly explain the two fundamental qualities of useful information.

Ans: N/A, LO: 7, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 247

A Further Look at Financial Statements

FOR INSTRUCTOR USE ONLY

2-75

S-A E 248

What are three of the five enhancing qualities of useful information.

Ans: N/A, LO: 7, Bloom: K, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 248

S-A E 249 (Ethics)

Many bonus plans are based upon the attainment of some specified short-term goal. For

example, sales personnel at Metal Crafters are given a bonus of 5% of the amount by which their

sales exceed $100,000. Sometimes the attainment of these goals is achieved by methods

detrimental to the long-term needs of the company. Sales representative Sara Crown, for

example, finds herself tempted to court certain customers that place large orders, even though

she knows they may not be able to pay. She complains that the bonus system itself is unethical.

Required:

Is a bonus system like the one at Metal Crafters unethical? Explain.

Ans: N/A, LO: 4, Bloom: E, Difficulty: Medium, Min: 5, AACSB: Ethics, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Decision Modeling, AICPA

PC: Communication, IMA: Performance Measurement

Solution 249

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-76

S-A E 250 (Communication)

Sunshine Sugar grows sugar cane in Florida, California, and Hawaii. Its investment in land to

grow sugar exceeds $2 million. Currently, land whose original cost was more than $300,000 in

Florida is threatened by plans to flood the Everglades to reclaim the wetlands. Sunshine plans to

fight vigorously to keep its land in production, particularly because most of the rest of its land is in

California, which is threatened by water shortages. The land in Florida is also significantly more

productive than that in California, and the wages paid to workers to process the sugar cane are

substantially less. Current plans include litigation to prevent government seizure of the land, an

extensive public education campaign, and intense lobbying efforts.

Required:

Sunshine has determined that a footnote disclosure should be made in the financial statements to

alert the investors of the threat to the land. Carefully consider how much of the above information

is appropriate for inclusion in the footnote. Write the footnote.

Ans: N/A, LO: 7, Bloom: E, Difficulty: Medium, Min: 5, AACSB: Communication, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Reporting, AICPA

PC: Communication, IMA: Reporting

Solution 250

A Further Look at Financial Statements

2-77

IFRS Questions

1. The classified balance sheet is

a. required under GAAP but not under IFRS.

b. required under IFRS in the same format as under GAAP.

c. required under IFRS but not under GAAP.

d. required under IFRS with certain variations in format as compared to GAAP.

2. IFRS requires the use of

a. the term balance sheet.

b. the term statement of financial position.

c. neither balance sheet nor statement of financial position, but recommends use of the

term balance sheet.

d. neither balance sheet nor statement of financial position, but recommends use of the

term statement of financial position.

3. IFRS

a. requires a specific format for the balance sheet (statement of financial position) that is

identical to U.S. GAAP.

b. requires a specific format for the balance sheet (statement of financial position) that is

different from U.S. GAAP.

c. requires no specific format for the balance sheet (statement of financial position) but

most companies that follow IFRS prepare the statement identical to U.S. GAAP .

d. requires no specific format for the balance sheet (statement of financial position) but

most companies that follow IFRS prepare the statement in a different format from U.S.

GAAP.

4. Most companies that follow IFRS present balance sheet (statement of financial position)

information in this order.

a. current assets; investments; property; plant and equipment; intangible assets; current

liabilities; long term liabilities; owners' equity.

b. intangible assets; property; plant and equipment; investments; current assets; current

liabilities; owners' equity; long term liabilities.

c. current assets; noncurrent assets; current liabilities; noncurrent liabilities; equity.

d. noncurrent assets; current assets; equity; noncurrent liabilities; current liabilities.

5. Under IFRS and under GAAP, current assets are listed in

IFRS GAAP

a. order of liquidity order of liquidity

b. reverse order of liquidity order of liquidity

c. order of liquidity reverse order of liquidity

d. reverse order of liquidity reverse order of liquidity

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

FOR INSTRUCTOR USE ONLY

2-78

6. The subtotal net assets is used in

a. both GAAP and IFRS.

b. GAAP but not IFRS.

c. IFRS but not GAAP.

d. neither IFRS nor GAAP.

7. Both IFRS and GAAP require disclosure about

a. accounting policies followed.

b. judgements that management has made in the process of applying the entity's

accounting policies.

c. the key assumptions and estimation uncertainty.

d. all of the above.

8. Under IFRS

a. comparative prior-period information must be presented, but financial statements need

not be provided annually.

b. comparative prior-period information must be presented, and financial statements

must be provided annually.

c. comparative prior-period information is not required, but financial statements need not

be provided annually.

d. comparative prior-period information is not required, but financial statements must be

provided annually.

9. The use of fair value to report assets

a. is not allowed under GAAP or IFRS.

b. is required by GAAP and IFRS.

c. is increasing under GAAP and IFRS, but GAAP has adopted it more broadly.

d. is increasing under GAAP and IFRS, but IFRS has adopted it more broadly.

10 Under IFRS

a. companies can apply fair value to property, plant, and equipment and natural

resources.

b. companies can apply fair value to property, plant, and equipment but not to natural

resources.

c. companies can apply fair value to neither property, plant, and equipment nor natural

resources.

d. companies can apply fair value to natural resources but not to property, plant, and

equipment.