2-1

Chapter 2

Answers to Review Problems

Finance For Executives – 4th Edition

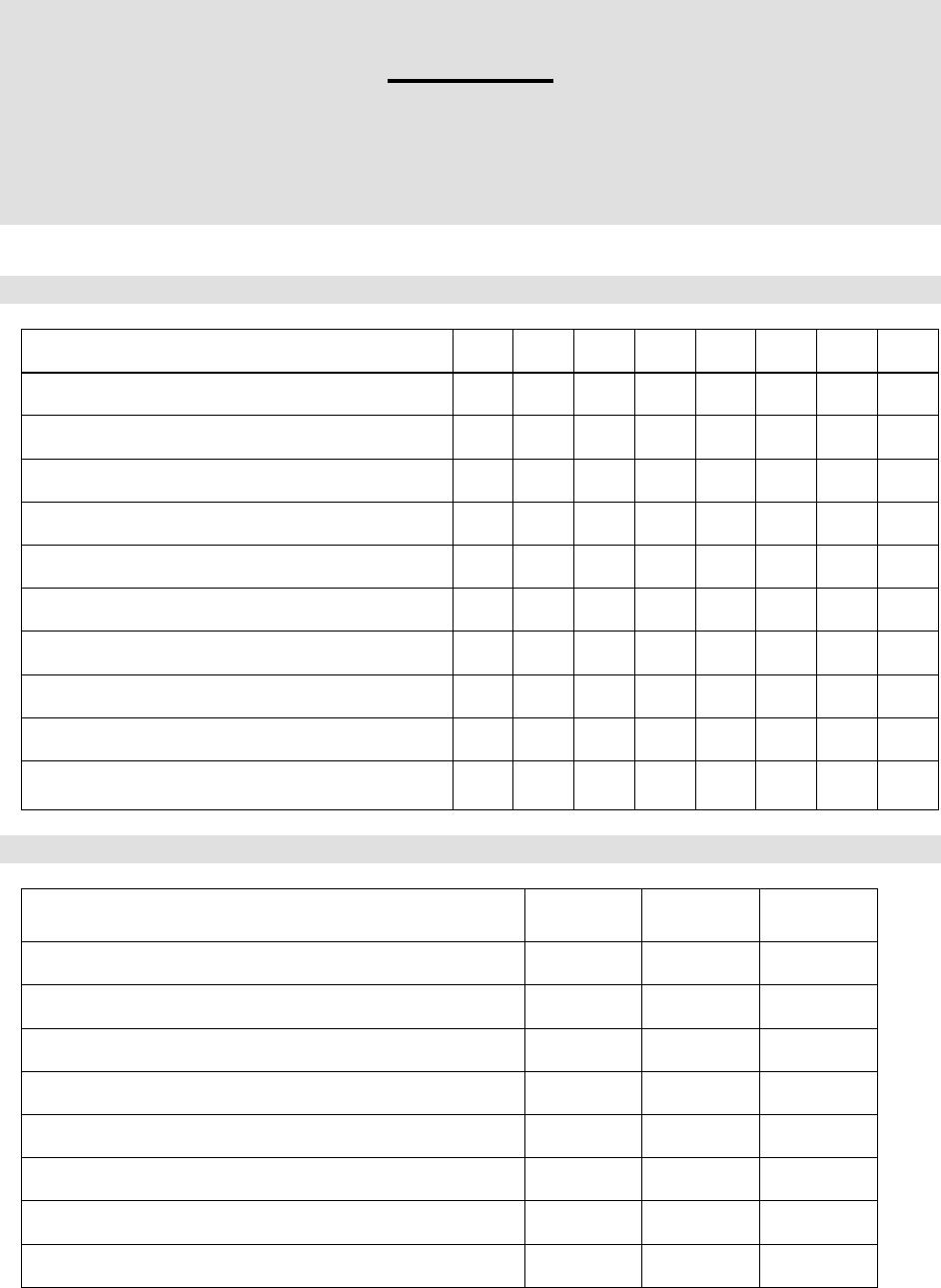

1. Accounting allocation of transactions.

CA

NCA

CL

NCL

OE

REV

EXP

RE

1. Factory equipment purchased for cash

✓

✓

2. Goodwill impairment loss

✓

✓

✓

✓

3. Interest income received

✓

✓

✓

✓

4. Dividend declared

✓

✓

✓

5. Shares repurchased

✓

✓

6. Sell merchandise on account

✓

✓

✓

✓

✓

7. Pay two months’ rent in advance

8. Purchase raw material on account

✓

✓

9. Receive cash advance from customer

✓

✓

10. Recognize salaries earned by employees

✓

✓

✓

✓

2. Missing accounts.

Firm 1

Firm 2

Firm 3

Assets, beginning of period

$1,000

$400

$1,500

Assets, end of period

1,100

500

1,500

Owner’s equity, beginning of period

500

200

900

Owners’ equity, end of period

600

260

1,000

Liabilities, beginning of period

500

200

600

Liabilities, end of period

500

240

500

Revenues of the period

2,000

200

600

Expenses of the period

1,800

180

500

2-2

Earnings after tax of the period

200

20

100

Dividends (from earnings of the period)

100

10

0

Shares issued ($ amount) during the period

0

50

0

Firm 1

Liabilities beginning of period = Assets beginning of period – Owners’ equity beginning of period

= $1,000 – $500 = $500

Firm 2

Assets beginning of period = Liabilities beginning of period + Owners’ equity beginning of period

= $200 + $200 = $400

Firm 3

Owners’ equity beginning of period = Owners’ equity end of period – Earnings after tax of the period + Dividends

– $Amount of shares issued during the period

= $1,000 – $100 + $0 – $0 = $900

2-3

3. Balance sheet changes.

Figures in millions

a.

Year 1

Total assets = Total liabilities and Owners’ equity

= $40,936

Year 2

Noncurrent assets = Total assets – Current assets

= $48,050 – $18,732 = $29,318

2-4

Year 3

Total assets = Current assets + Noncurrent assets

= $19,950 + $29,920 = $49,870

Total liabilities and owners’ equity = Total assets

Year 4

Noncurrent assets = Total liabilities and owners’ equity – Current assets

= $51,070 – $19,976 = $31,094

Total assets = Total liabilities and owners’ equity

= $51,070

2-5

End-of-year for balance sheet items

Year 1

Year 2

Year 3

Year 4

Current assets

$16,870

$18,732

$19,950

$19,976

Noncurrent assets

24,066

29,318

29,920

31,094

Total assets

40,936

48,050

49,870

51,070

Current liabilities

13,466

15,284

16,574

16,080

Noncurrent liabilities

11,998

14,624

18,414

17,326

Paid-in capital

2,034

2,298

2,584

2,798

Retained earnings

13,438

15,844

12,298

14,866

Earnings (loss) after tax

2,014

4,446

(1,312)

5,048

Dividends

1,580

2.040

2,234

2,480

Owners’ equity

15,472

18,142

14,882

17,664

Total liabilities and owners’ equity

40,936

48,050

49,870

51,070

b.

A large investment (e.g., the acquisition of another firm) would explain the increase in total assets

between years 1 and 2. A mix of debt and equity financing was used to finance the investment.

4. Balance sheet changes.

Figures in millions

a.

Year 1

Total assets = Total liabilities and Owners’ equity

= $61,404

2-6

Year 2

Current assets = (Current assets – current liabilities) + Current liabilities

= $5,712 + $22,926 = $28,638

Year 3

Total assets = Current assets + Noncurrent assets

= $29,925 + $44,880 = $74,805

Total liabilities and owners’ equity = Total assets

= $74,805

2-7

Year 4

Total assets = Total liabilities and owners’ equity

= $76,605

Noncurrent assets = Total assets – Current assets

= $76,605 – $29,964 = $46,641

End-of-year for balance sheet items

Year 1

Year 2

Year 3

Year 4

Current assets

$25,305

$28,638

$29,925

$29,964

Noncurrent assets

36,099

43,437

44,880

46,641

Total assets

61,404

72,075

74,805

76,605

Current liabilities

20,199

22,926

24,861

24,120

Current assets – current liabilities

5,106

5,712

5,064

5,844

Noncurrent liabilities

17,997

21,936

27,621

25,989

Paid-in capital

3,051

3,447

3,876

4,197

2-8

Retained earnings

20,157

23,766

18,447

22,299

Earnings (loss) after tax

n. a.

n. a.

(1,968)

7,572

Dividends

n. a.

n. a.

3,351

3,720

Total liabilities and owners’ equity

61,404

72,075

74,805

76,605

b.

A large investment (e.g., the acquisition of another firm) would explain the increase in total assets

between years 1 and 2. A mix of debt and equity financing was used to finance the investment.

5. Balance sheet changes.

Figures in millions

a.

Year 1

Noncurrent assets = Total assets – Current assets

= $21,094 – $3,092 = $18,002

Year 2

Total assets = Total liabilities and owners’ equity

= $21,182

2-9

Year 3

Total assets = Current assets + Noncurrent assets

= $2,932 + $17,996 = $20,928

Year 4

Current assets = Current liabilities × (Current assets/current liabilities)

= $3,002 × 1.04 = $3,122

Total assets = Current assets + Noncurrent liabilities

End-of-year for balance sheet items

Year 1

Year 2

Year 3

Year 4

Current assets

$ 3,092

$ 3,022

$ 2,932

$ 3,122

Noncurrent assets

18,002

18,160

17,996

20,286

Total assets

21,094

21,182

20,928

23,408

Current assets/current liabilities

1.038

1.217

1.023

1.04

Current liabilities

2,978

2,484

2,866

3,002

2-10

Noncurrent liabilities

9,286

9,830

10,004

12,322

Owners’ equity

8,830

8,868

8,058

8,084

Total liabilities and owners’ equity

21,094

21,182

20,928

23,408

b.

The noncurrent assets (fixed assets)-to-current assets ratio stayed remarkably constant over the four-year

period, varying between 5.8 (Years 1, 2, and 3) and 6.5 (Year 4). The large value of this ratio indicates

that the firm belongs to a capital intensive industry.

6. Reconstructing an income statement.

Year 1

Gross profit = Sales – Cost of goods sold

= $21,184 – $16,916 = $4,268

Year 2

Sales = Earnings after tax + Income tax expense – Interest income + Research and development

expenses + Administrative and selling expenses + Cost of goods sold

= $2,124 + $864 – $132 + $504 + $3,304 + $24,372 = $31,036

2-11

Year 3

Earnings before tax (EBT) = Earnings after tax (EAT) + Income tax expense

= $3,776 + $1,696 = $5,472

Earnings before interest and tax (EBIT) = Earnings before tax (EBT) – Interest income

Year 1 Year 2 Year 3

Sales $21,184 $31,036 $49,308

Cost of goods sold 16,916 24,372 38,420

Gross profit 4,268 6,664 10,888

Administrative and selling

expenses 2,380 3,304 4,808

2-12

7. Reconstructing an income statement.

Year 1

Gross profit = Sales – Cost of goods sold

= $21,087 – $16,182 = $4,905

Year 2

Earnings before tax (EBT) = Earnings after tax (EAT) + Income tax expense

= $408 + $252 = $660

2-13

Year 3

Earnings before tax (EBT) = Earnings after tax (EAT) + Income tax expense

= $312 + $192 = $504

Earnings before interest and tax (EBIT) = Earnings before tax (EBT) + Interest expense

= $504 + $81 = $585

Year 1 Year 2 Year 3

Sales $21,087 $22,992 $26,613

Cost of goods sold 16,182 17,709 20,481

Gross profit 4,905 5,283 6,132

2-14

8. Reconstructing a balance sheet.

Beginning

of year

End

of year

Assets

Current assets

Cash

$ 450

$ 5007

Accounts receivable

250

4508

Inventories

300

4009

Noncurrent assets

Property, plant, and equipment

Gross value

$3,0001

$4,00010

Less: Accumulated depreciation

(1,200)11 2,800

Total assets

Liabilities and owners’ equity

Current liabilities

Short-term debt

$ 400

$ 15017

Owed to banks

$3003

$50

Current portion of long-term debt

1002

$15.0

1002

Accounts payable

3006

40012

Accrued expenses

100

30013

Noncurrent liabilities

Long-term debt

40014

Total liabilities

2-15

9. Constructing income statements and balance sheets.

VideoStores

Income Statement

For period ending 12/31/10

In thousands

Sales

(items

3,

18)

$ 320,000

Cost of goods sold

(260,000)

Material cost (item 5)

$224,000

Labor expenses (item 16)

36,000

Depreciation expense (item 9)

Net interest expense (items 6, 14, 25)

Dividends (item 20)

VideoStores

Balance Sheets

December 31, 2009 and 2010

In thousands

12/31/09

12/31/10

Assets

Cash (item 23)

$ 7,500

$ 11,400

Accounts receivable (items 7, 1)

32,000

38,400

Inventories (item 18)

28,000

32,000

Prepaid expenses (item 26)

1,500

2,200

2-16

10. Forecasting financing needs.

a.

Financing needs = Capital expenditures + Increase in current assets

Capital expenditures = $1 million

Increase in current assets = $9 million × Percentage increase in sales

= $9 million × ($36 million – $27 million)/$27 million

= $3 million

Financing needs = $1 million + $3 million

= $4 million