1

Corporate Finance, 4e (Berk / DeMarzo)

Chapter 19 Valuation and Financial Modeling: A Case Study

19.1 Valuation Using Comparables

Use the tables for the question(s) below.

Estimated 2005 Income Statement and Balance Sheet Data for Ideko Corporation

Year

2005

Year

2005

Income Statement

($ 000)

Balance Sheet ($ 000)

1 Sales

75,000

Assets

2 Cost of Goods Sold

1 Cash and Equivalents

12,664

3 Raw Materials

(16,000)

2 Accounts Receivable

18,493

4 Direct Labor Costs

(18,000)

3 Inventories

6165

5 Gross Profit

1000

4 Total Current Assets

37,322

6 Sales and Marketing

(11,250)

5 Property, Plant, and Equipment

49,500

7 Administrative

(13,500)

6 Goodwill

—

8 EBITDA

16,250

7 Total Assets

86,822

9 Depreciation

(5500)

Liabilities and Stockholder’s Equity

10 EBIT

10,750

8 Accounts Payable

4654

11 Interest Expense (net)

(75)

9 Debt

4500

12 Pre-tax Income

10,675

10 Total Liabilities

9154

13 Income Tax

(3736)

11 Stockholder’s Equity

77,668

14 Net Income

6939

12 Total Liabilities and Equity

86,822

The following are financial ratios for three comparable companies:

Ratio

Oakley, Inc.

Luxottica

Group

Nike, Inc.

P/E

24.8x

28x

18.2x

EV/Sales

2x

2.7x

1.5x

EV/EBITDA

11.6x

14.4x

9.3x

EBITDA/Sales

17.0%

18.5%

15.9

1) Based upon the average P/E ratio of the comparable firms, Ideko’s target market value of equity is

closest to:

A) $157 million

B) $155 million

C) $193 million

D) $165 million

2) Based upon the average EV/Sales ratio of the comparable firms, Ideko’s target economic value is

closest to:

A) $191 million

B) $155 million

C) $165 million

D) $157 million

3) Based upon the average EV/Sales ratio of the comparable firms, if Ideko holds $6.5 million of cash in

excess of its working capital needs, then Ideko’s target market value of equity is closest to:

A) $165 million

B) $157 million

C) $193 million

D) $191 million

4) Based upon the average EV/EBITDA ratio of the comparable firms, Ideko’s target economic value is

closest to:

A) $191 million

B) $155 million

C) $157 million

D) $193 million

5) Based upon the average EV/EBITDA ratio of the comparable firms, if Ideko holds $6.5 million of cash

in excess of its working capital needs, then Ideko’s target market value of equity is closest to:

A) $155 million

B) $157 million

C) $165 million

D) $193 million

6) What range for the market value of equity for Ideko is implied by the range of P/E multiples for the

comparable firms?

7) What range for the market value of equity for Ideko is implied by the range of EV/Sales multiples for

the comparable firms if Ideko holds $6.5 million of cash in excess of its working capital needs?

8) What range for the market value of equity for Ideko is implied by the range of EV/EBITDA multiples

for the comparable firms if Ideko holds $6.5 million of cash in excess of its working capital needs?

19.2 The Business Plan

Use the following information to answer the question(s) below:

Ideko’s Planned Debt

Year

2005

2006

2007

2008

2009

2010

Outstanding Debt

100,000

100,000

100,000

115,000

120,000

120,000

1) If Ideko’s loans will have an interest rate of 6.8%, then the interest expense paid in 2008 is closest to:

A) $6800

B) $7310

C) $7820

D) $7990

2) If Ideko’s loans will have an interest rate of 6.8%, then the interest expense paid in 2009 is closest to:

A) $6800

B) $7310

C) $7820

D) $7990

Use the table for the question(s) below.

Ideko Sales and Operating Cost Assumptions

Year

2005

2006

2007

2008

2009

2010

Sales Data

Growth/Year

1 Market Size (000 units)

5.0%

10,000

10,500

11,025

11,576

12,155

12,763

2 Market Share

1.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

3 Average Sales Price

($/unit)

2.0%

75.00

76.50

78.03

79.59

81.18

82.81

Cost of Goods Data

4 Raw Materials ($/unit)

1.0%

16.00

16.16

16.32

16.48

16.65

16.82

5 Direct Labor Costs

($/unit)

4.0%

18.00

18.72

19.47

20.25

21.06

21.90

Operating Expense

and Tax Data

6 Sales and Marketing

(% sales)

15.0%

16.5%

18.0%

19.5%

20.0%

20.0%

7 Administrative (% sales)

18.0%

15.0%

15.0%

14.0%

13.0%

13.0%

8 Tax Rate

35.0%

35.0%

35.0%

35.0%

35.0%

35.0%

3) Based upon Ideko’s Sales and Operating Cost Assumptions, what production capacity will Ideko

require in 2007?

A) 1505 units

B) 1323 units

C) 1914 units

D) 1115 units

1 Market Size

2 Market Share

4) Based upon Ideko’s Sales and Operating Cost Assumptions, what production capacity will Ideko

require in 2008?

A) 1702 units

B) 1323 units

C) 1505 units

D) 1914 units

5) Based upon Ideko’s Sales and Operating Cost Assumptions, what production capacity will Ideko

require in 2009?

A) 1505 units

B) 1115 units

C) 1323 units

D) 1702 units

Use the tables for the question(s) below.

Estimated 2005 Income Statement and Balance Sheet Data for Ideko Corporation

Year

2005

Year

2005

Income Statement

($ 000)

Balance Sheet ($ 000)

1 Sales

75,000

Assets

2 Cost of Goods Sold

1 Cash and Equivalents

12,664

3 Raw Materials

(16,000)

2 Accounts Receivable

18,493

4 Direct Labor Costs

(18,000)

3 Inventories

6165

5 Gross Profit

1000

4 Total Current Assets

37,322

6 Sales and Marketing

(11,250)

5 Property, Plant, and Equipment

49,500

7 Administrative

(13,500)

6 Goodwill

—

8 EBITDA

16,250

7 Total Assets

86,822

9 Depreciation

(5500)

Liabilities and Stockholder’s Equity

10 EBIT

10,750

8 Accounts Payable

4654

11 Interest Expense (net)

(75)

9 Debt

4500

12 Pre-tax Income

10,675

10 Total Liabilities

9154

13 Income Tax

(3736)

11 Stockholder’s Equity

77,668

14 Net Income

6939

12 Total Liabilities and Equity

86,822

6) Ideko’s Accounts Receivable Days is closest to:

A) 84 days

B) 95 days

C) 90 days

D) 75 days

19.3 Building the Financial Model

Use the following information to answer the question(s) below:

1) The after tax interest expense in 2008 is closest to:

A) 2380

B) 4420

C) 6800

D) 7820

2) The free cash flow to the firm in 2008 is closest to:

A) -5005

B) -1755

C) 5575

D) 14,995

3) The free cash flow to equity in 2008 is closest to:

A) -5005

B) -1755

C) 5575

D) 9995

4) The after tax interest expense in 2010 is closest to:

A) 0

B) 2856

C) 5304

D) 8160

5) The free cash flow to the firm in 2010 is closest to:

A) 10,684

B) 11,559

C) 23,698

D) 26,394

6) The free cash flow to equity in 2010 is closest to:

A) 6255

B) 10,684

C) 11,559

D) 18,394

12

Use the table for the question(s) below.

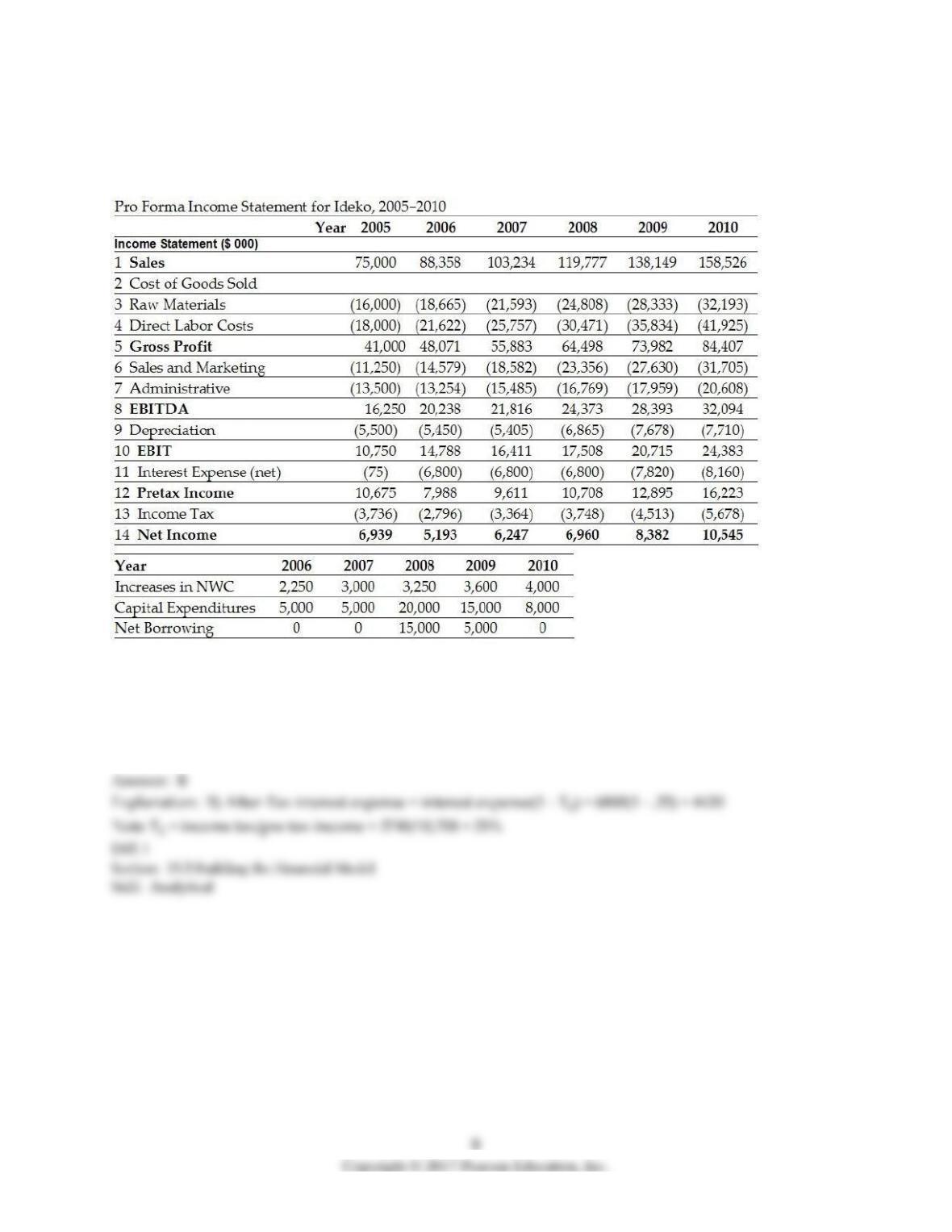

Pro Forma Income Statement for Ideko, 2005-2010

Year

2005

2006

2007

2008

2009

2010

Income Statement ($ 000)

1 Sales

75,000

88,358

103,234

119,777

138,149

158,526

2 Cost of Goods Sold

3 Raw Materials

(16,000)

(18,665)

(21,593)

(24,808)

(28,333)

(32,193)

4 Direct Labor Costs

(18,000)

(21,622)

(25,757)

(30,471)

(35,834)

(41,925)

5 Gross Profit

41,000

48,071

55,883

64,498

73,982

84,407

6 Sales and Marketing

(11,250)

(14,579)

(18,582)

(23,356)

(27,630)

(31,705)

7 Administrative

(13,500)

(13,254)

(15,485)

(16,769)

(17,959)

(20,608)

8 EBITDA

16,250

20,238

21,816

24,373

28,393

32,094

9 Depreciation

(5500)

(5450)

(5405)

(6865)

(7678)

(7710)

10 EBIT

10,750

14,788

16,411

17,508

20,715

24,383

11 Interest Expense (net)

(75)

(6800)

(6800)

(6800)

(7820)

(8160)

12 Pre-tax Income

10,675

7988

9611

10,708

12,895

16,223

13 Income Tax

(3736)

(2796)

(3364)

(3748)

(4513)

(5678)

14 Net Income

6939

5193

6247

6960

8382

10,545

7) With the proper changes it is believed that Ideko’s credit policies will allow for an account receivables

days of 60. The forecasted accounts receivable for Ideko in 2006 is closest to:

A) $19,690

B) $16,970

C) $22,710

D) $14,525

8) With the proper changes it is believed that Ideko’s credit policies will allow for an account receivables

days of 60. The forecasted accounts receivable for Ideko in 2007 is closest to:

A) $14,525

B) $16,970

C) $22,710

D) $19,690

9) With the proper changes it is believed that Ideko’s credit policies will allow for an account receivables

days of 60. The forecasted accounts receivable for Ideko in 2008 is closest to:

A) $14,525

B) $19,690

C) $22,710

D) $16,970

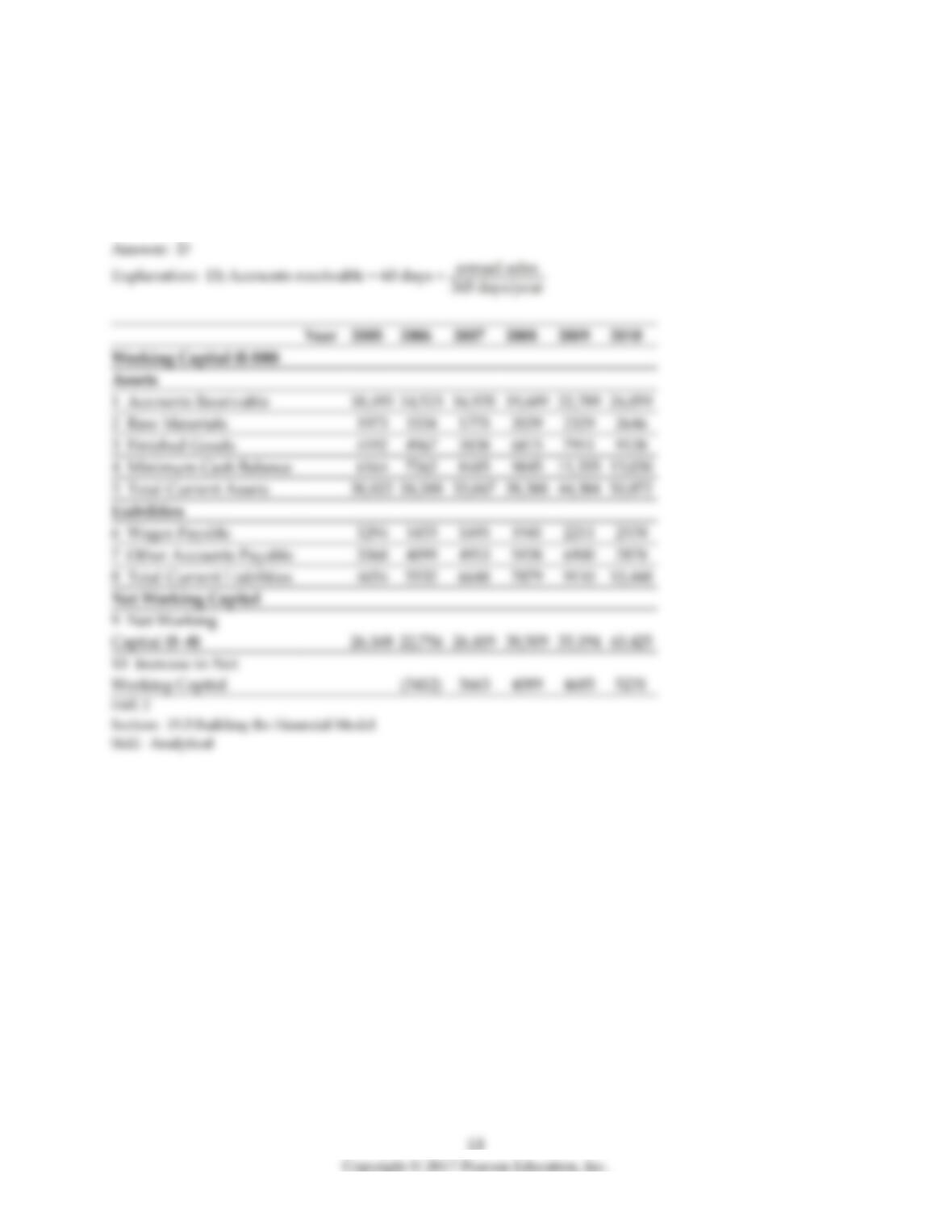

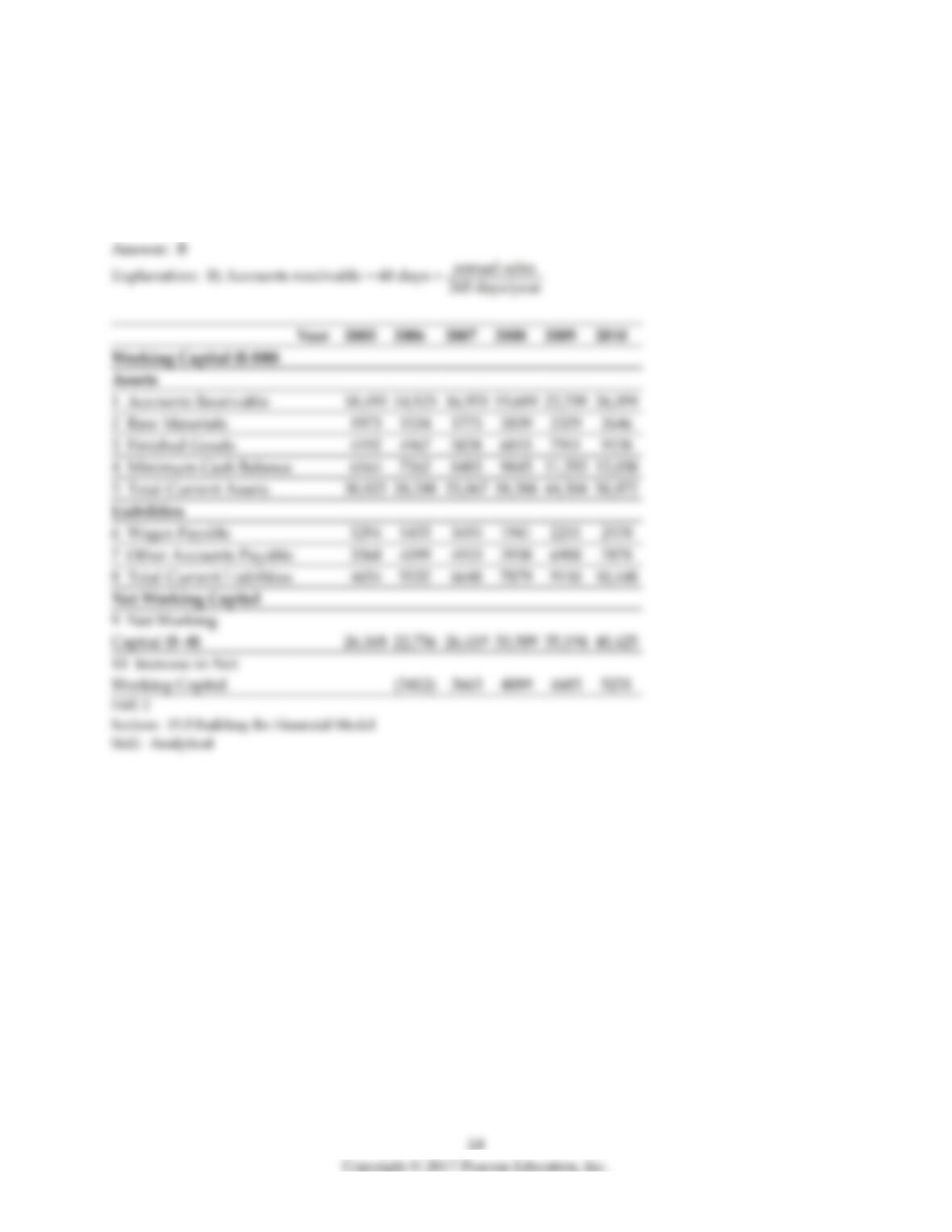

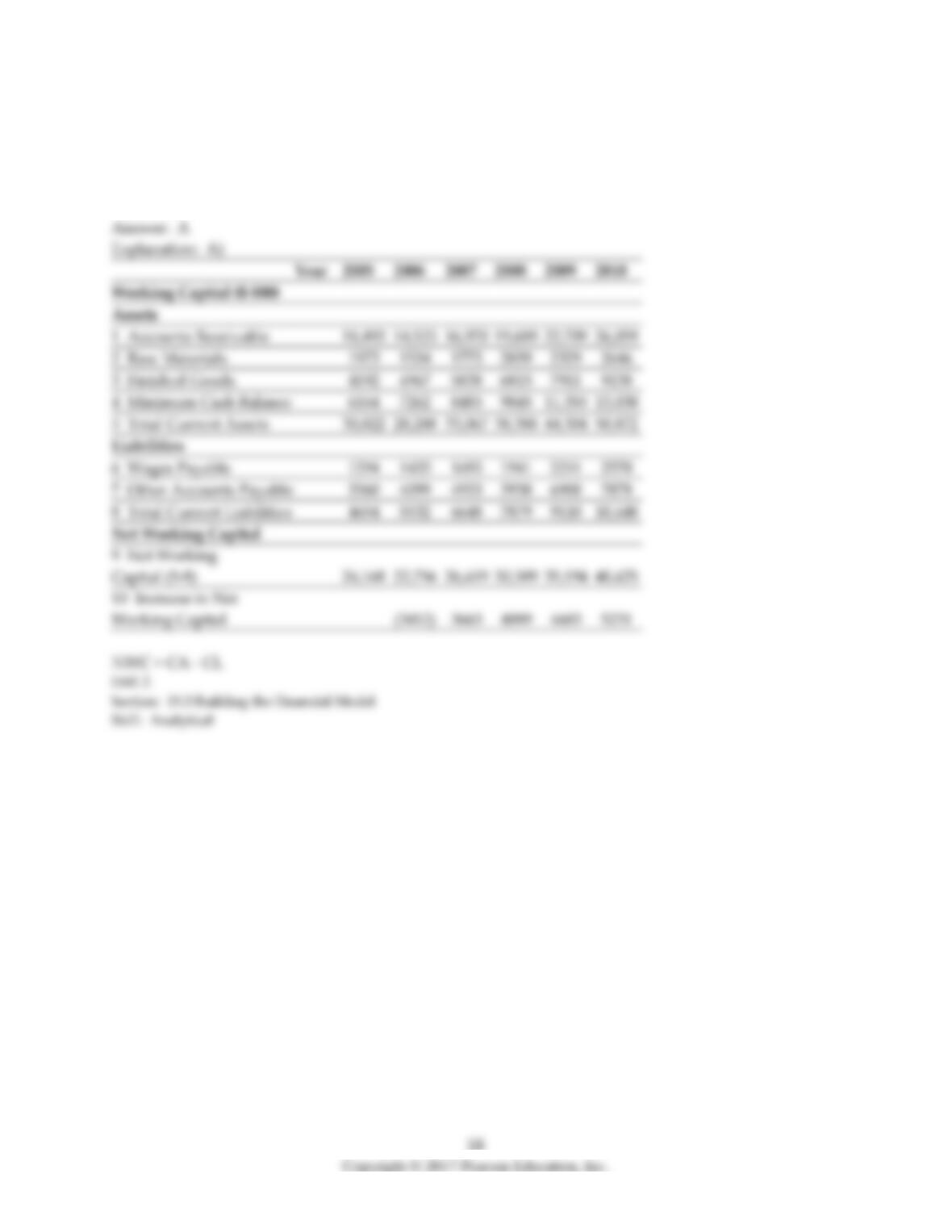

10) The amount of net working capital for Ideko in 2006 is closest to:

A) $22,750

B) $35,195

C) $30,510

D) $26,420