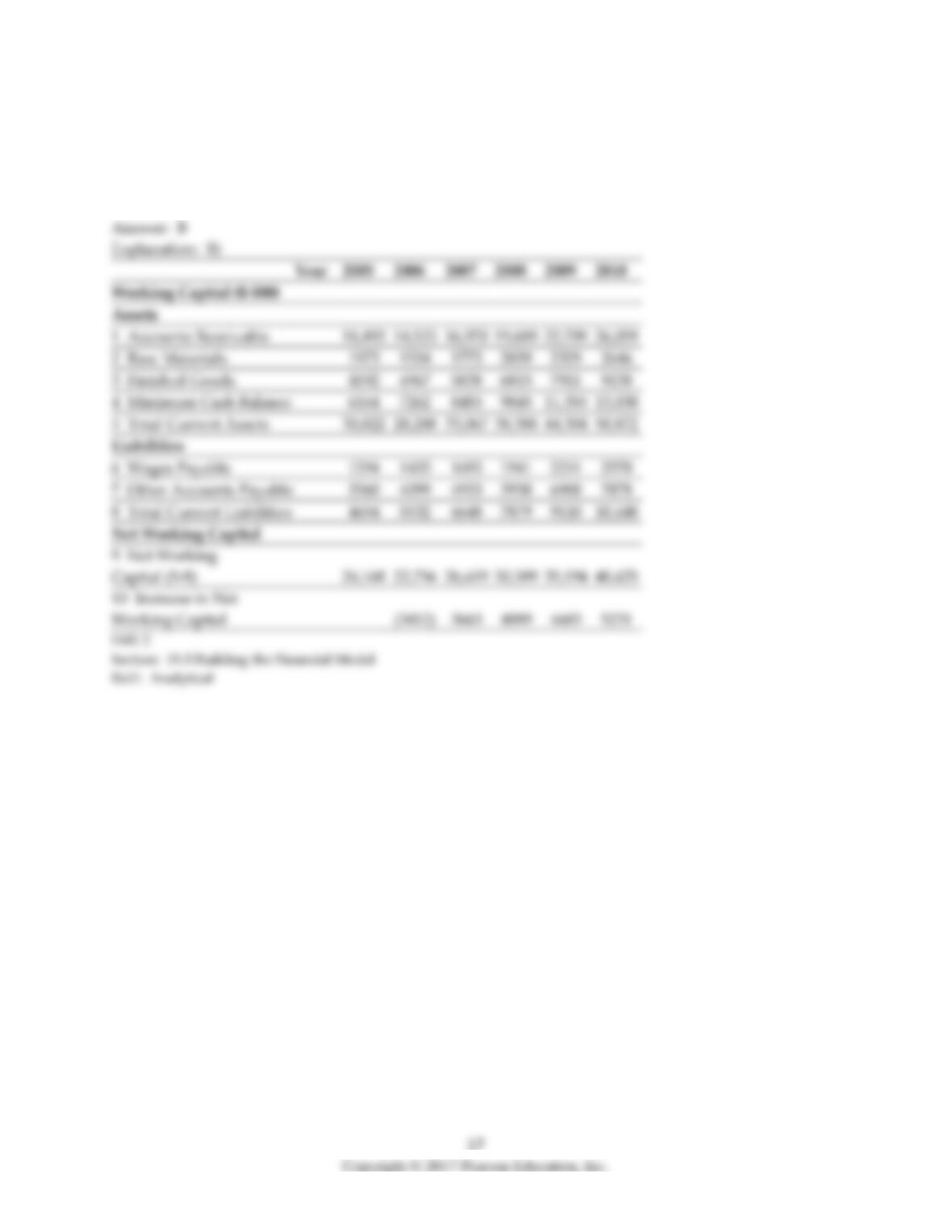

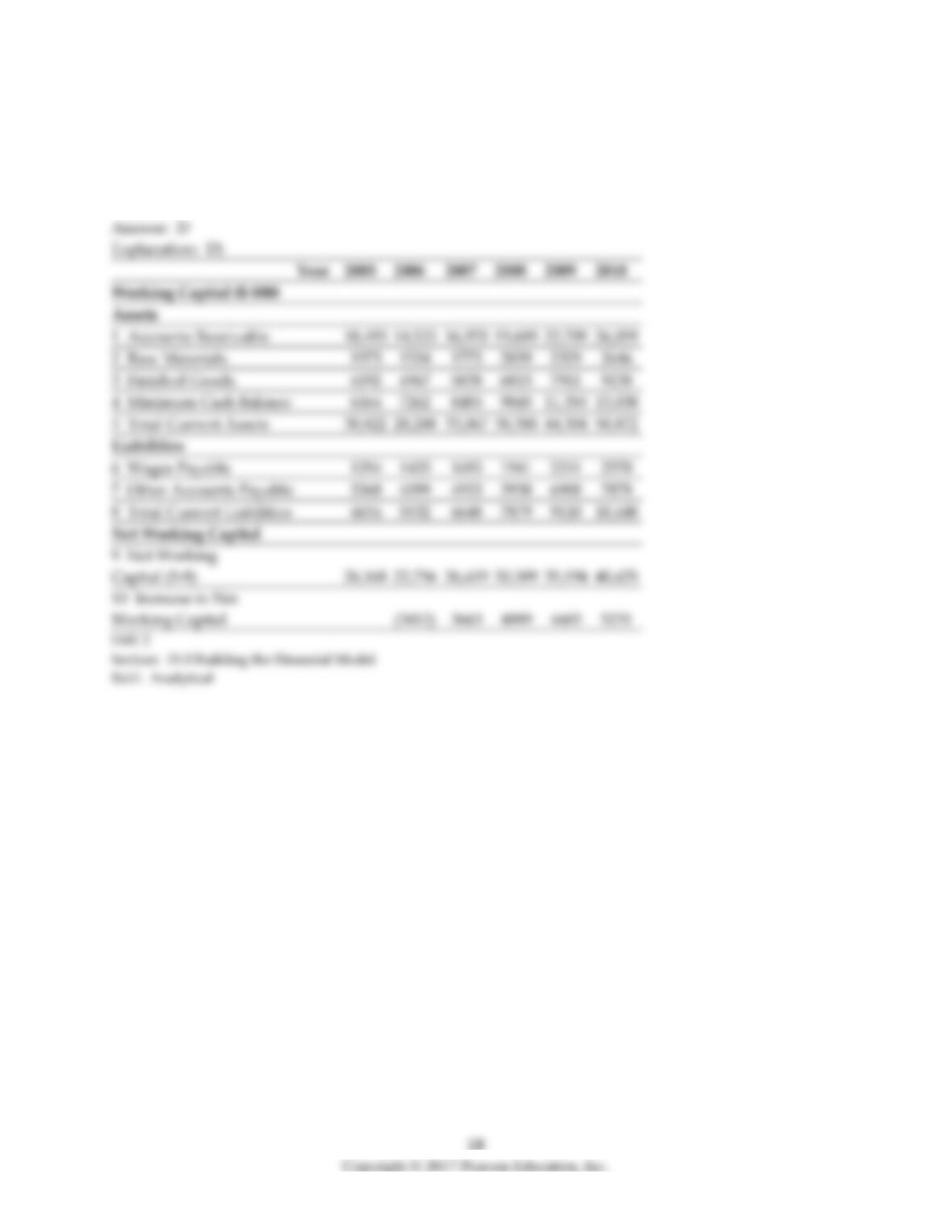

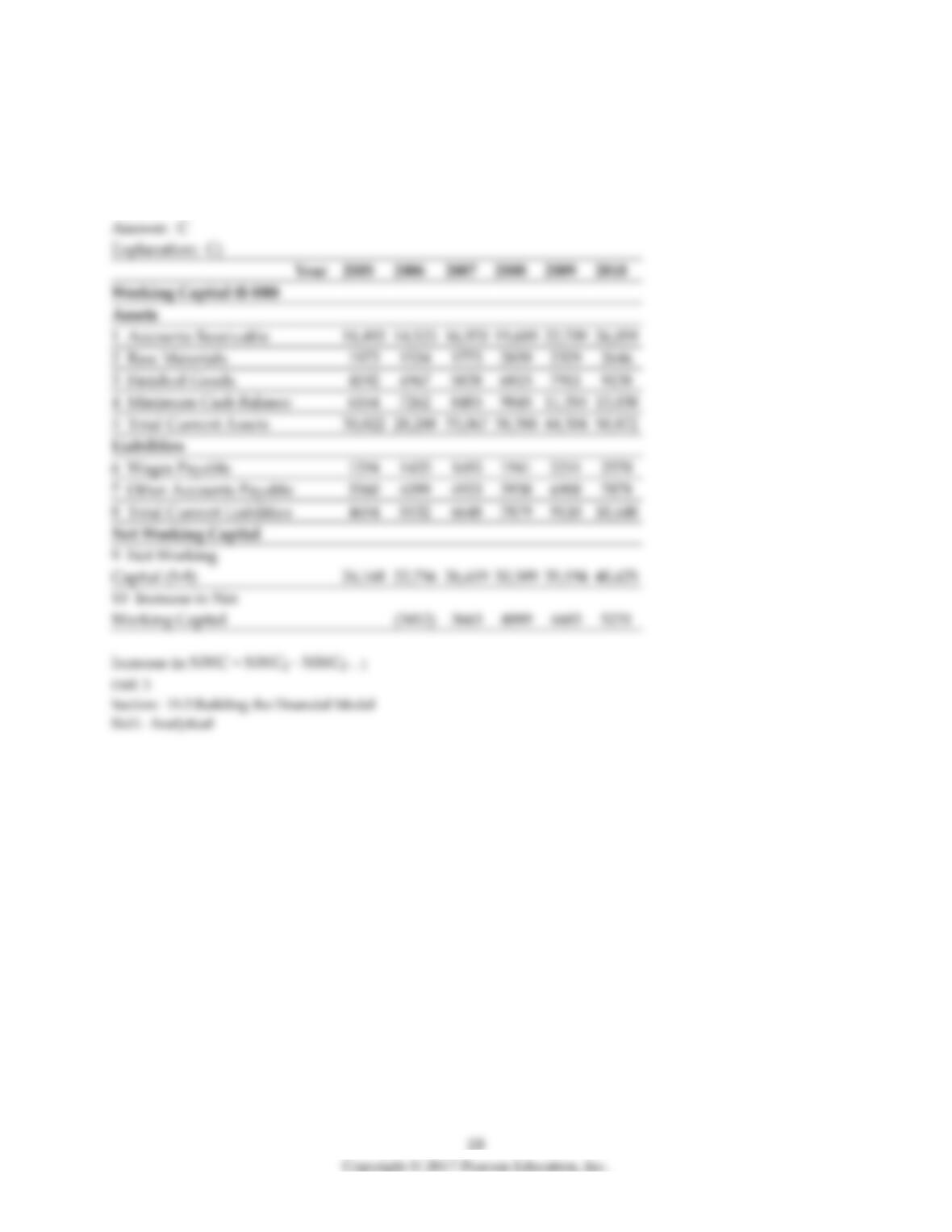

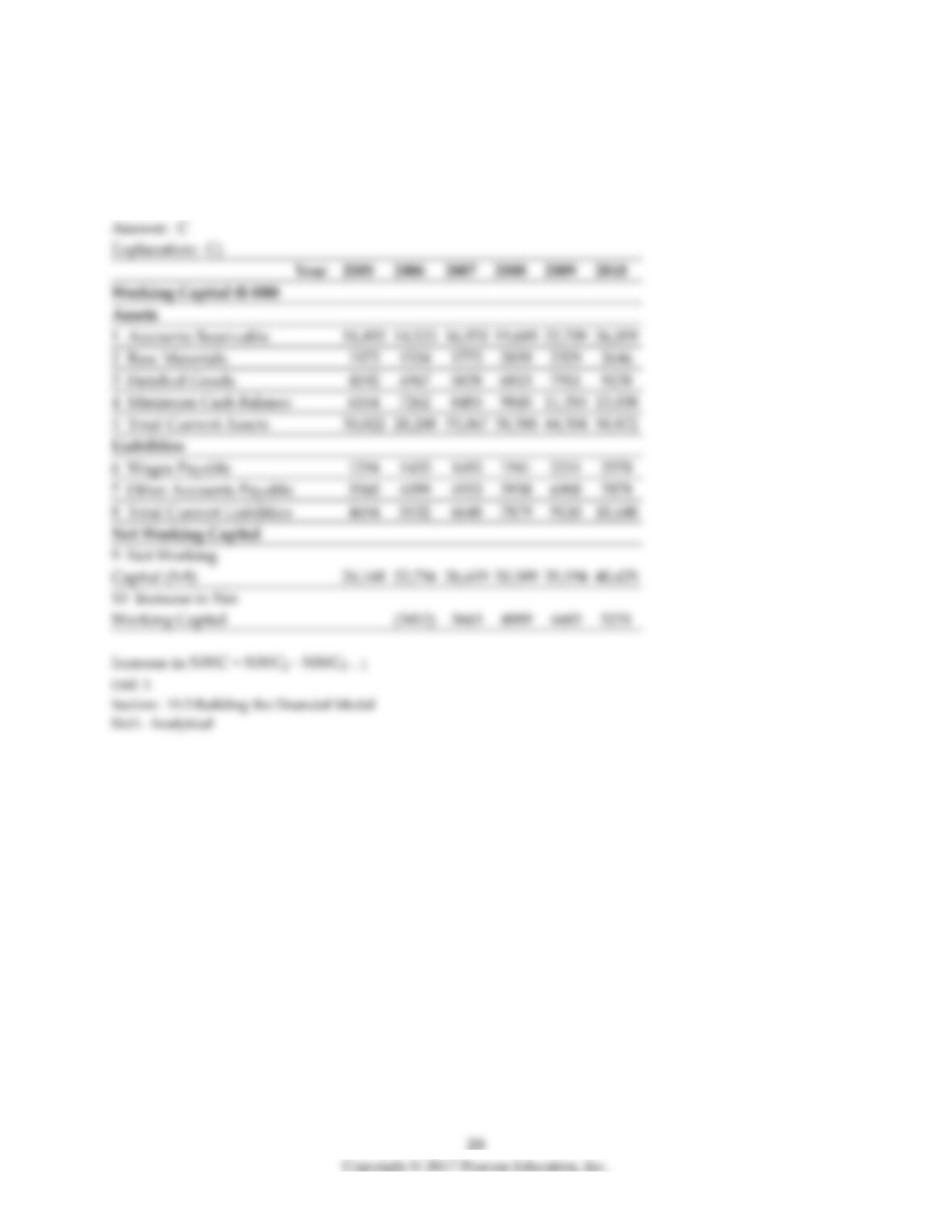

11) The amount of net working capital for Ideko in 2007 is closest to:

A) $30,510

B) $26,420

C) $22,170

D) $35,195

12) The amount of net working capital for Ideko in 2008 is closest to:

A) $35,195

B) $26,420

C) $22,170

D) $30,510

13) The amount of the increase in net working capital for Ideko in 2007 is closest to:

A) $4090

B) $4685

C) $3665

D) $5230

14) The amount of the increase in net working capital for Ideko in 2008 is closest to:

A) $4685

B) $3665

C) $4090

D) $5230

15) Using the income statement above and the following information:

Year

2006

2007

2008

2009

2010

Increases in NWC

2250

3000

3250

3600

4000

Capital Expenditures

5000

5000

20,000

15,000

8000

Net Borrowing

0

0

15,000

5000

0

Calculate Ideko’s Free Cash Flow to the Firm and Free Cash Flow to Equity in 2007.

Year

Net Income

Expense

Unlevered Net Income

Plus: Depreciation

Less: Increases in NWC

(3250)

(3600)

Less: Capital Expenditures

Free Cash Flow of Firm

(5005)

Plus: Net Borrowing

Expense

(4420)

(5083)

Free Cash Flow to Equity

16) Using the income statement above and the following information:

Year

2006

2007

2008

2009

2010

Increases in NWC

2250

3000

3250

3600

4000

Capital Expenditures

5000

5000

20,000

15,000

8000

Net Borrowing

0

0

15,000

5000

0

Calculate Ideko’s Free Cash Flow to the Firm and Free Cash Flow to Equity in 2009.

Year

Net Income

Expense

Unlevered Net Income

Plus: Depreciation

Less: Increases in NWC

(3600)

Less: Capital Expenditures

Free Cash Flow of Firm

(5005)

Plus: Net Borrowing

Expense

(4420)

(5083)

Free Cash Flow to Equity

19.4 Estimating the Cost of Capital

Use the table for the question(s) below.

Capital Structure and Unlevered Beta Estimates for Comparable Firms

Firm

βE

βD

βU

Oakley

1.00

0.00

1.50

—

1.50

Luxottica

0.83

0.17

0.75

0

0.62

Nike

1.05

-0.05

0.60

0

0.63

1) The unlevered beta for Oakley is closest to:

A) 0.70

B) 1.50

C) 1.00

D) 0.60

2) If the risk-free rate of interest is 6% and the market risk premium has historically averaged 5%, then

the cost of capital for Oakley is closest to:

A) 13.5%

B) 10.2%

C) 9.1%

D) 14.7%

3) The unlevered beta for Luxottica is closest to:

A) 1.00

B) 0.60

C) 0.70

D) 1.50

4) If the risk-free rate of interest is 6% and the market risk premium has historically averaged 5%, then

the cost of capital for Luxottica is closest to:

A) 10.2%

B) 13.5%

C) 9.1%

D) 14.7%

5) The unlevered beta for Nike is closest to:

A) 0.70

B) 1.00

C) 1.50

D) 0.60

6) If the risk-free rate of interest is 6% and the market risk premium has historically averaged 5%, then

the cost of capital for Nike is closest to:

A) 14.7%

B) 10.2%

C) 9.1%

D) 13.5%

26

19.5 Valuing the Investment

Use the following information to answer the question(s) below:

1) If Ideko’s future expected growth rate is 5%, then the estimated free cash flow for 2011 is closest to:

A) 6568

B) 11,151

C) 11,218

D) 12,137

2) If Ideko’s future expected growth rate is 5% and its WACC is 9%, then the continuation value in 2010

is closest to:

A) 164,200

B) 278,775

C) 280,450

D) 303,425

28

Use the tables for the question(s) below.

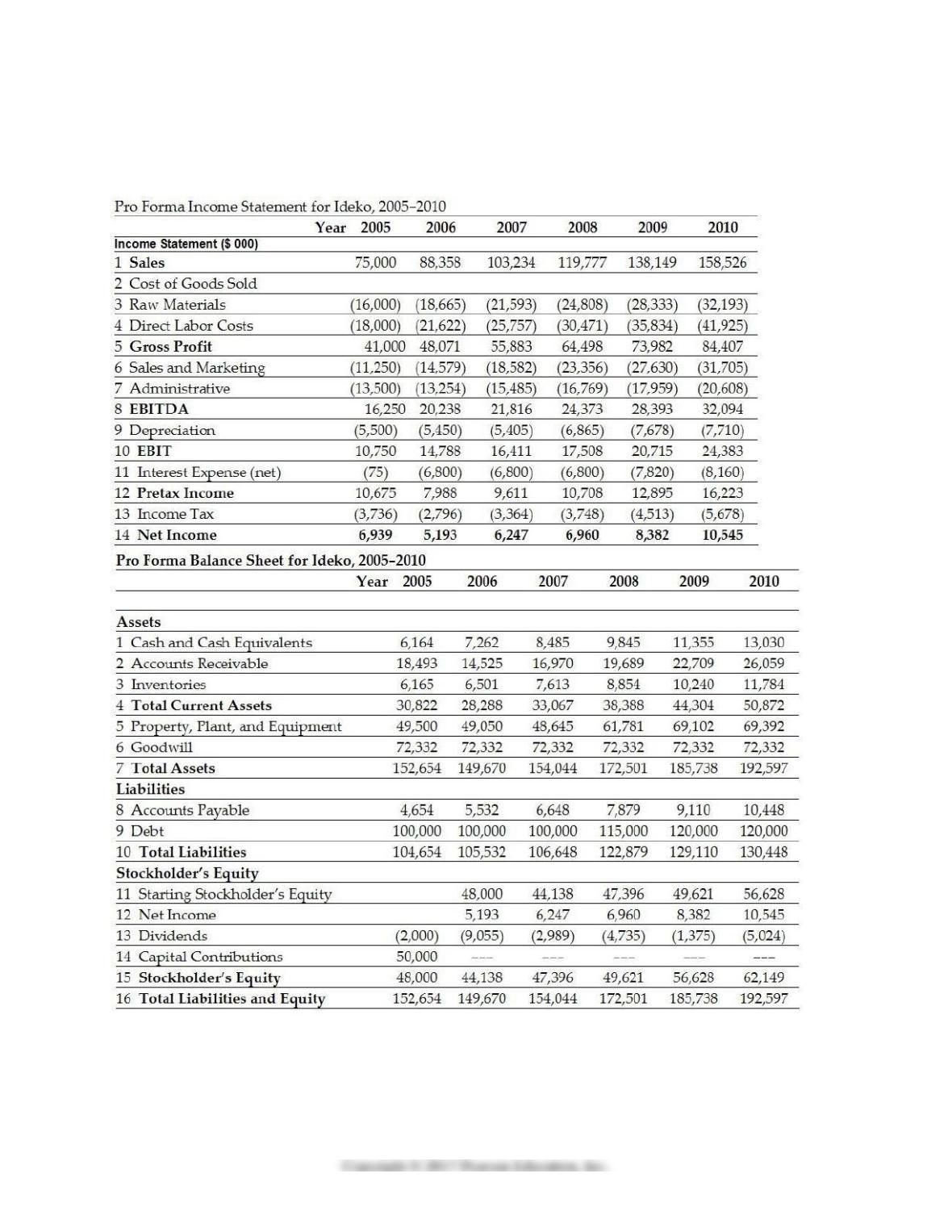

Pro Forma Income Statement for Ideko, 2005-2010

Year

2005

2006

2007

2008

2009

2010

Income Statement ($ 000)

1 Sales

75,000

88,358

103,234

119,777

138,149

158,526

2 Cost of Goods Sold

3 Raw Materials

(16,000)

(18,665)

(21,593)

(24,808)

(28,333)

(32,193)

4 Direct Labor Costs

(18,000)

(21,622)

(25,757)

(30,471)

(35,834)

(41,925)

5 Gross Profit

41,000

48,071

55,883

64,498

73,982

84,407

6 Sales and Marketing

(11,250)

(14,579)

(18,582)

(23,356)

(27,630)

(31,705)

7 Administrative

(13,500)

(13,254)

(15,485)

(16,769)

(17,959)

(20,608)

8 EBITDA

16,250

20,238

21,816

24,373

28,393

32,094

9 Depreciation

(5500)

(5450)

(5405)

(6865)

(7678)

(7710)

10 EBIT

10,750

14,788

16,411

17,508

20,715

24,383

11 Interest Expense (net)

(75)

(6800)

(6800)

(6800)

(7820)

(8160)

12 Pre-tax Income

10,675

7988

9611

10,708

12,895

16,223

13 Income Tax

(3736)

(2796)

(3364)

(3748)

(4513)

(5678)

14 Net Income

6939

5193

6247

6960

8382

10,545

Pro Forma Balance Sheet for Ideko, 2005-2010

Year

2005

2006

2007

2008

2009

2010

Balance Sheet ($ 000)

Assets

1 Cash and Cash Equivalents

6164

7262

8485

9845

11,355

13,030

2 Accounts Receivable

18,493

14,525

16,970

19,689

22,709

26,059

3 Inventories

6165

6501

7613

8854

10,240

11,784

4 Total Current Assets

30,822

28,288

33,067

38,388

44,304

50,872

5 Property, Plant, and Equipment

49,500

49,050

48,645

61,781

69,102

69,392

6 Goodwill

72,332

72,332

72,332

72,332

72,332

72,332

7 Total Assets

152,654

149,670

154,044

172,501

185,738

192,597

Liabilities

8 Accounts Payable

4654

5532

6648

7879

9110

10,448

9 Debt

100,000

100,000

100,000

115,000

120,000

120,000

10 Total Liabilities

104,654

105,532

106,648

122,879

129,110

130,448

Stockholder’s Equity

11 Starting Stockholder’s Equity

48,000

44,138

47,396

49,621

56,628

12 Net Income

5193

6247

6960

8382

10,545

13 Dividends

(2000)

(9055)

(2989)

(4735)

(1375)

(5024)

14 Capital Contributions

50,000

—

—

—

—

—

15 Stockholder’s Equity

48,000

44,138

47,396

49,621

56,628

62,149

16 Total Liabilities and Equity

152,654

149,670

154,044

172,501

185,738

192,597

3) Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation enterprise value of Ideko in

2010 is closest to:

A) $152.8 million

B) $272.8 million

C) $301.7 million

D) $181.7 million

4) Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation equity value of Ideko in

2010 is closest to:

A) $181.7 million

B) $272.8 million

C) $152.8 million

D) $301.7 million

5) Assuming that Ideko has a EBITDA multiple of 9.4, then the continuation enterprise value of Ideko in

2010 is closest to:

A) $181.7 million

B) $152.8 million

C) $272.8 million

D) $301.7 million

6) Assuming that Ideko has a EBITDA multiple of 9.4, then the continuation equity value of Ideko in

2010 is closest to:

A) $152.8 million

B) $181.7 million

C) $301.7 million

D) $272.8 million

7) Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation EV/Sales ratio of Ideko in

2010 is closest to:

A) 1.7

B) 1.9

C) 1.6

D) 1.8

8) Assuming that Ideko has a EBITDA multiple of 9.4, then the continuation EV/Sales ratio of Ideko in

2010 is closest to:

A) 1.9

B) 1.7

C) 1.6

D) 1.8

9) Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation unlevered P/E ratio of

Ideko in 2010 is closest to:

A) 17.6

B) 16.4

C) 14.5

D) 19.0

10) Assuming that Ideko has a EBITDA multiple of 9.4, then the continuation unlevered P/E ratio of

Ideko in 2010 is closest to:

A) 17.2

B) 16.4

C) 14.5

D) 19.4

11) Assuming that Ideko has a EBITDA multiple of 8.5, then the continuation levered P/E ratio of Ideko

in 2010 is closest to:

A) 19.0

B) 17.2

C) 16.4

D) 14.5

12) Assuming that Ideko has a EBITDA multiple of 9.4, then the continuation levered P/E ratio of Ideko

in 2010 is closest to:

A) 17.2

B) 14.5

C) 19.0

D) 16.4

19.6 Sensitivity Analysis

1) What is the purpose of the sensitivity analysis?