Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 36

Solution 138 (cont.)

Sales Mix

Green 25% × 60,000 = 15,000 bikes

Brown 45% × 60,000 = 27,000 bikes

Blue 30% × 60,000 = 18,000 bikes

Ex. 139

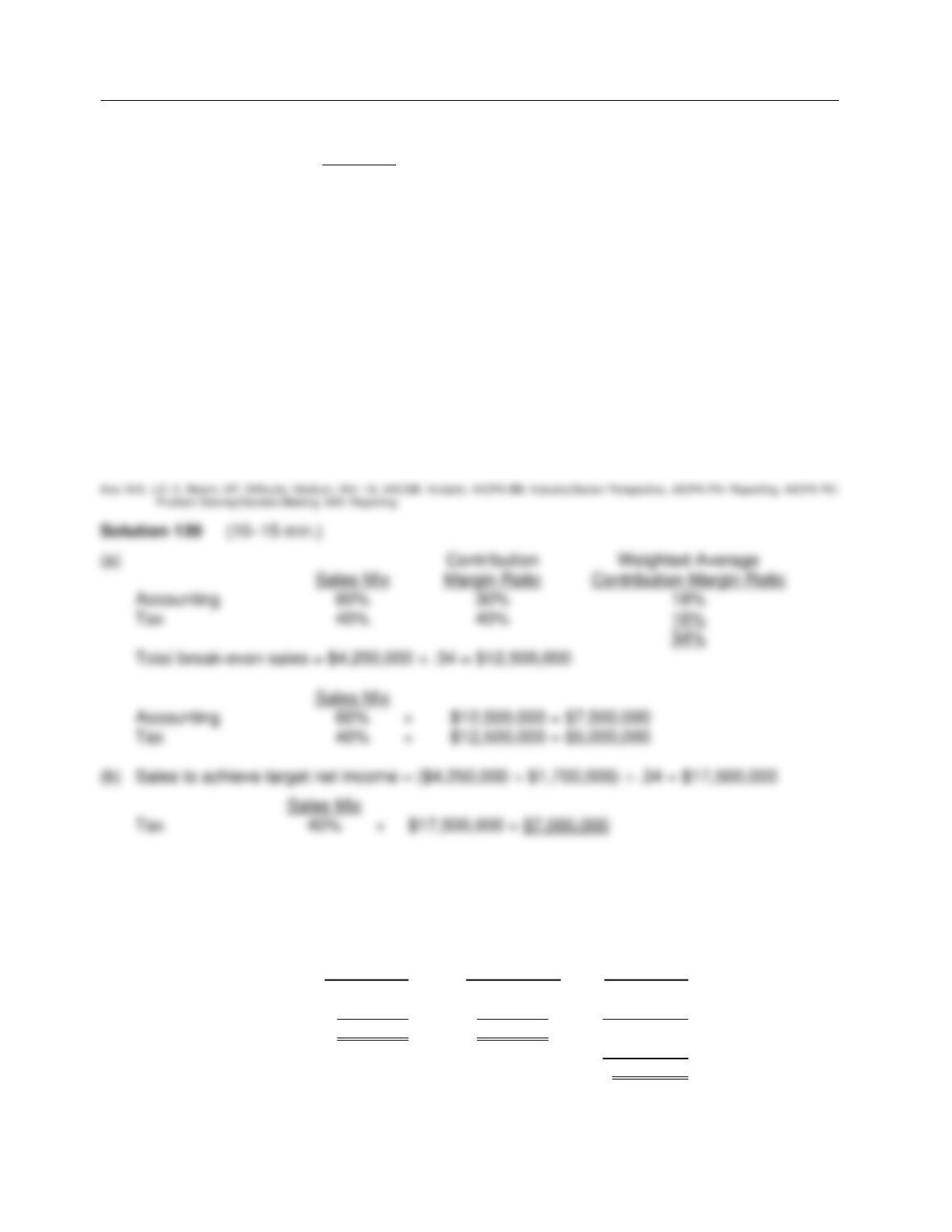

DeMont Tax Services provides primarily two lines of service: accounting and tax. Accounting–

related services represent 60% of its revenue and provide a contribution margin ratio of 30%. Tax

services represent 40% of its revenue and provide a 40% contribution margin ratio. The

company’s fixed costs are $4,250,000.

Instructions

(a) Calculate the revenue from each type of service that the company must achieve to break

even.

(b) The company has a desired net income of $1,700,000. What amount of revenue would

DeMont earn from tax services if it achieves this goal with the current sales mix?

Ex. 140

Blue Chance Co. sells computers and video game systems. The business is divided into two

divisions along product lines. Variable costing income statements for the current year are

presented below:

Computers VG Systems Total

Sales $700,000 $300,000 $1,000,000

Variable costs 420,000 210,000 630,000

Contribution margin $280,000 $ 90,000 370,000

Fixed costs 296,000

Net income $ 74,000

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 37

Ex 140 (cont.)

Instructions

(a) Determine the sales mix and contribution margin ratio for each division.

(b) Calculate the company’s weighted-average contribution margin ratio.

(c) Calculate the company’s break-even point in dollars.

(d) Determine the sales level, in dollars, for each division at the break-even point.

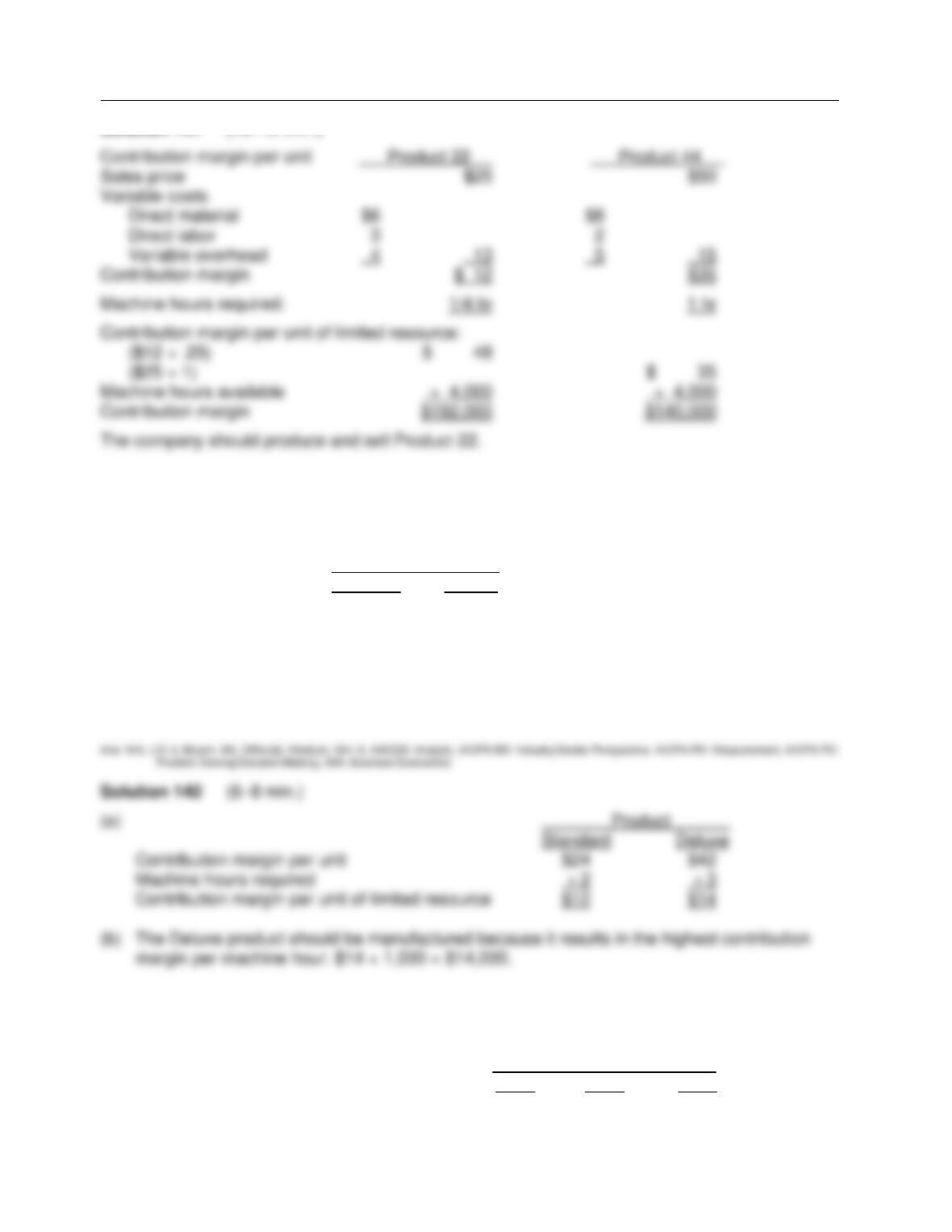

Ex. 141

Hewitt Co. has 4,000 machine hours available to produce either Product 22 or Product 44. The

cost accounting department developed the following unit information for each product:

Product 22 Product 44

Sales price $25 $50

Direct materials 6 8

Direct labor 3 2

Variable manufacturing overhead 4 5

Fixed manufacturing overhead 3 5

Machine time required 15 minutes 60 minutes

Instructions

Management wants to know which product to produce in order to maximize the company’s

income. Taking into consideration the constraints under which the company operates, prepare a

report to show which product should be produced and sold.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 38

Solution 141 (10–12 min.)

Ex. 142

Reynolds, Inc. manufactures and sells two products. Relevant per unit data concerning each

product are given below:

Product

Standard Deluxe

Selling price $50 $75

Variable costs $26 $33

Machine hours 2 3

Instructions

(a) Compute the contribution margin per unit of limited resource for each product.

(b) If 1,000 additional machine hours are available, which product should be manufactured?

Ex. 143

Oscar Corporation produces and sells three products. Unit data concerning each product is

shown below.

Product

X Y Z

Selling price $200 $300 $250

Direct labor costs 45 75 60

Other variable costs 110 130 106

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 39

Ex 143 (cont.)

The company has 2,000 hours of labor available to build inventory in anticipation of the

company’s peak season. Management is trying to decide which product should be produced. The

direct labor hourly rate is $15.

Instructions

(a) Determine the number of direct labor hours per unit.

(b) Determine the contribution margin per direct labor hour.

(c) Determine which product should be produced and the total contribution margin for that

product.

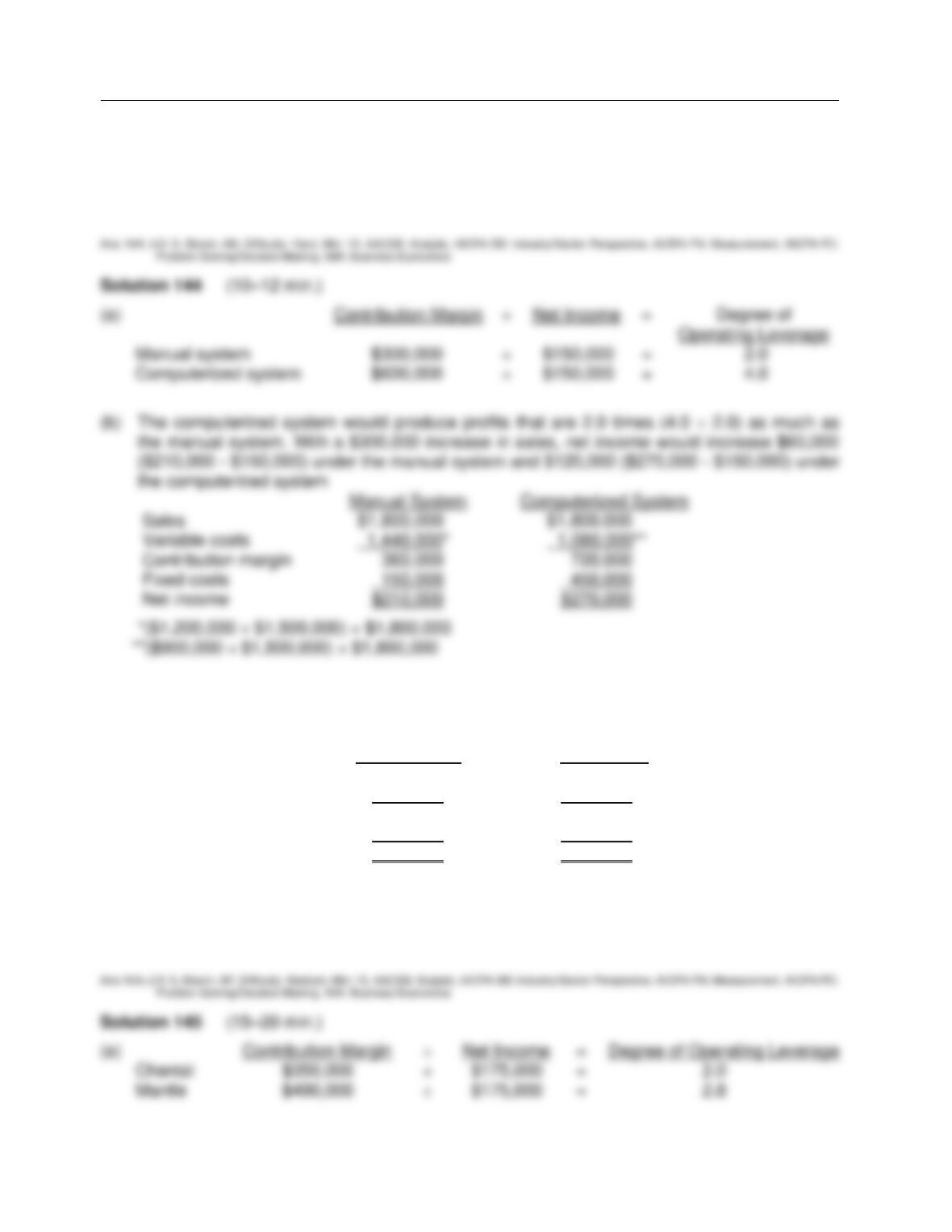

Ex. 144

Shanahan Co. of Dublin, Ireland is contemplating a major change in its cost structure. Currently,

all of its drafting work is performed by skilled draftsmen. Mike Shanahan the owner, is considering

replacing the draftsmen with a computerized drafting system.

However, before making the change, Mike would like to know the consequences of the change,

since the volume of business varies significantly from year to year. Shown below are CVP income

statements for each alternative.

Manual System Computerized System

Sales $1,500,000 $1,500,000

Variable costs 1,200,000 900,000

Contribution margin 300,000 600,000

Fixed costs 150,000 450,000

Net income $150,000 $150,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 40

Ex. 144 (cont.)

Instructions

(a) Determine the degree of operating leverage for each alternative.

(b) Which alternative would produce the higher net income if sales increased by $300,000?

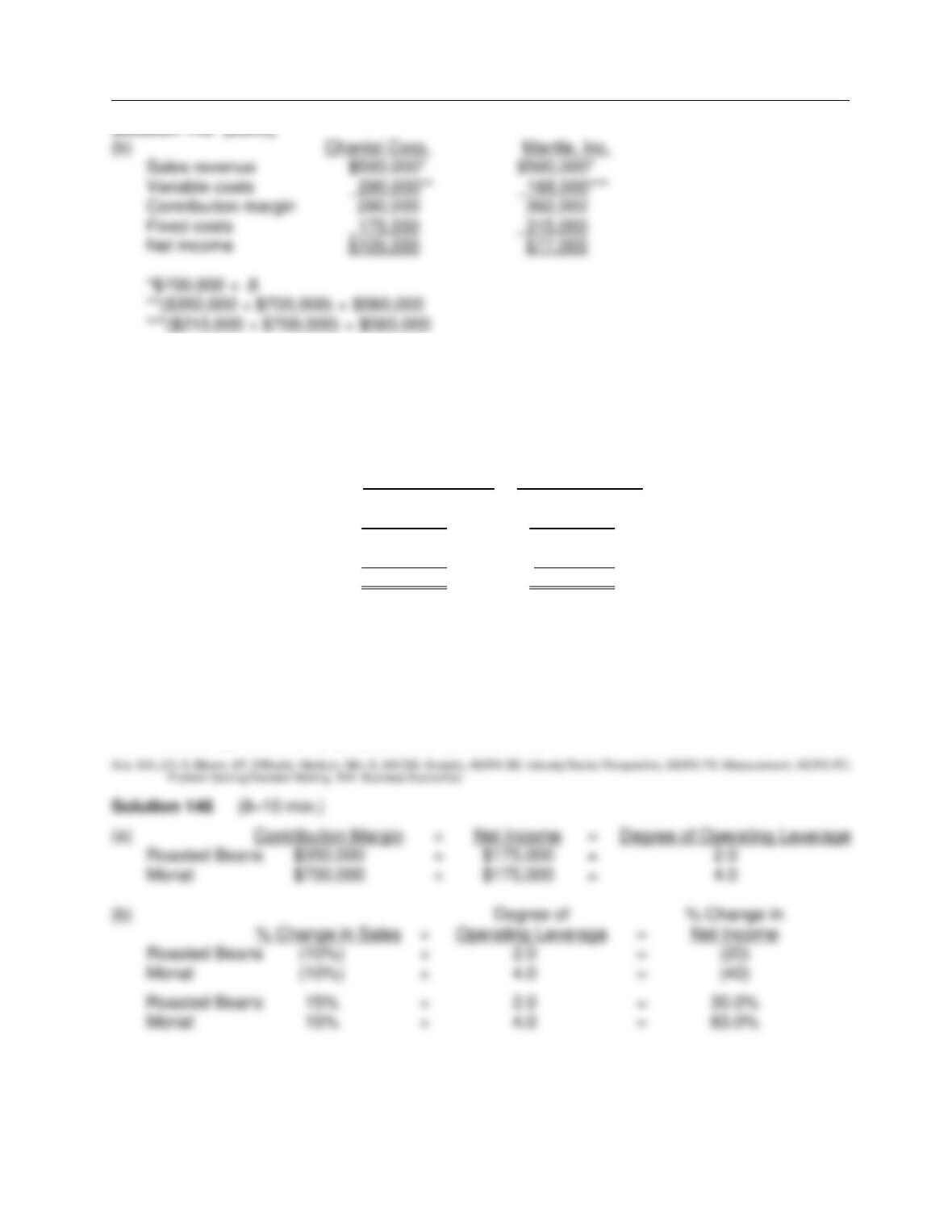

Ex. 145

The following CVP income statements are available for Chantal Corp. and Mantle, Inc.

Chantal Corp. Mantle, Inc.

Sales revenue $700,000 $700,000

Variable costs 350,000 210,000

Contribution margin 350,000 490,000

Fixed costs 175,000 315,000

Net income $175,000 $175,000

Instructions

(a) Compute the degree of operating leverage for each company.

(b) Assume that sales revenue decreases by 20%. Prepare a CVP income statement for each

company.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 41

Solution 145 (cont.)

Ex. 146

An investment banker is analyzing two companies that specialize in the production and sale of

gourmet cappuccino and chai mixes. Roasted Beans Co. uses a labor-intensive approach and

Monat Industries uses a mechanized system. Variable costing income statements for the two

companies are shown below:

Roasted Beans Monat Industries

Sales $1,000,000 $1,000,000

Variable costs 650,000 300,000

Contribution margin 350,000 700,000

Fixed costs 175,000 525,000

Net Income $ 175,000 $ 175,000

The investment banker is interested in acquiring one of these companies. However, she is

concerned about the impact that each company’s cost structure might have on its profitability.

Instructions

(a) Calculate each company’s degree of operating leverage.

(b) Determine the effect on each company’s net income if sales decrease by 10% and if sales

increase by 15%. Do not prepare income statements.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 42

aEx. 147

Indicate with a check mark whether each of the following would be a product cost or a period cost

under an absorption or a variable system for Sour Industries.

Absorption Variable

Product Period Product Period

a. Direct materials ________ ________ ________ _______

b. Direct labor ________ ________ ________ _______

c. Factory utilities ________ ________ ________ _______

d. Factory rent ________ ________ ________ _______

e. Indirect labor ________ ________ ________ _______

f. Factory supervisor salaries ________ ________ ________ _______

g. Factory maintenance (variable) ________ ________ ________ _______

h. Factory depreciation ________ ________ ________ _______

i. Sales salaries ________ ________ ________ _______

j. Sales commissions ________ ________ ________ _______

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 43

aEx. 148

Nimble Corp. manufactures and sells a variety of camping products. Recently the company

opened a new plant to manufacture a deluxe portable cooking unit. Cost and sales data for the

first month of operations are shown below:

Manufacturing Costs

Fixed Overhead $140,000

Variable overhead $3 per unit

Direct labor $12 per unit

Direct material $30 per unit

Beginning inventory 0 units

Units produced 10,000

Units sold 9,000

Selling and Administrative Costs

Fixed $200,000

Variable $4 per unit sold

The portable cooking unit sells for $110. Management is interested in the opening month’s results

and has asked for an income statement.

Instructions

Assume the company uses absorption costing. Calculate the production cost per unit and prepare

an income statement for the month of June, 2013.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

19 – 44

aEx. 149

On-Road Wheels, Inc. manufactures a basic road bicycle. Production and sales data for the most

recent year are as follows (no beginning inventory):

Variable production costs $90 per bike

Fixed production costs $400,000

Variable selling and administrative costs $22 per bike

Fixed selling and administrative costs $550,000

Selling price $200 per bike

Production 20,000 bikes

Sales 18,000 bikes

Instructions

(a) Prepare a brief income statement using absorption costing.

(b) Compute the amount to be reported for inventory in the year-end absorption costing balance

sheet.

aEx. 150

On-Road Wheels, Inc. manufactures a basic road bicycle. Production and sales data for the most

recent year are as follows (no beginning inventory):

Variable production costs $95 per bike

Fixed production costs $400,000

Variable selling and administrative costs $22 per bike

Fixed selling and administrative costs $550,000

Selling price $200 per bike

Production 20,000 bikes

Sales 16,000 bikes

Instructions

(a) Prepare a brief income statement using variable costing.

(b) Compute the amount to be reported for inventory in the year-end variable costing balance

sheet.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 45

aSolution 150 (8–12 min.)

aEx. 151

Cutting Edge Corp. produces sporting equipment. In 2012, the first year of operations, Cutting

Edge produced 25,000 units and sold 20,000 units. In 2013, the production and sales results

were exactly reversed. In each year, selling price was $100, variable manufacturing costs were

$40 per unit, variable selling expenses were $8 per unit, fixed manufacturing costs were

$540,000, and fixed administrative expenses were $200,000.

Instructions

(a) Compute the net income under variable costing for each year.

(b) Compute the net income under absorption costing for each year.

(c) Reconcile the differences each year in income from operations under the two costing

approaches.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 46

aEx. 152

Graham is a division of Flynn, Inc. The division manufactures and sells a pump that is used in a

wide variety of applications. During the coming year, it expects to sell 30,000 units for $25 per

unit. Steve Moss, division manager, is considering producing either 30,000 or 35,000 units during

the period. Other information is presented in the schedule below:

Division Information – 2013

Beginning inventory 0

Expected sales in units 30,000

Selling price per unit $25

Variable manufacturing cost per unit $7

Fixed manufacturing overhead costs (total) $420,000

Fixed manufacturing overhead costs per unit

Based on 30,000 units ($420,000 ÷ 30,000) $14

Based on 35,000 units ($420,000 ÷ 35,000) $12

Manufacturing cost per unit

Based on 30,000 units ($7 variable + $14 fixed) $21

Based on 35,000 units ($7 variable + $12 fixed) $19

Selling and administrative expenses (all fixed) $25,000

Instructions

(a) Prepare an absorption costing income statement with one column showing the results if

30,000 units are produced and one column showing the results if 35,000 units are produced.

(b) Why is income different for the two production levels when sales is 30,000 units either way?

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 47

aEx. 153

Graham is a division of Flynn, Inc. The division manufactures and sells a pump that is used in a

wide variety of applications. During the coming year, it expects to sell 30,000 units for $20 per

unit. Steve Moss, division manager, is considering producing either 30,000 or 40,000 units during

the period. Other information is presented in the schedule below:

Division Information – 2013

Beginning inventory 0

Expected sales in units 30,000

Selling price per unit $20

Variable manufacturing cost per unit $7

Fixed manufacturing overhead costs (total) $360,000

Fixed manufacturing overhead costs per unit

Based on 30,000 units ($360,000 ÷ 30,000) $12

Based on 40,000 units ($360,000 ÷ 40,000) $9

Manufacturing cost per unit

Based on 30,000 units ($7 variable + $12 fixed) $19

Based on 40,000 units ($7 variable + $9 fixed) $16

Selling and administrative expenses (all fixed) $25,000

Instructions

Prepare a variable costing income statement with one column showing the results if 30,000 units

are produced and one column showing the results if 40,000 units are produced.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 48

COMPLETION STATEMENTS

154. The ______________ income statement classifies cost as variable or fixed and computes

a contribution margin.

155. _________________ tells a company how far sales can drop before it will be operating at

a loss.

156. ___________________ is the relative percentage in which a company sells its multiple

products.

157. When more than one product is sold, the break-even point can be determined by dividing

fixed expenses by _______________________.

158. When a company has ________________, management must decide which products to

make and sell in order to maximize net income.

159. ___________________ refers to the relative proportion of fixed versus variable costs that

a company incurs.

160. The _________________________ provides a measure of a company’s earnings volatility

and can be used to compare companies.

a161. Under _____________________ all manufacturing costs are charged to, or absorbed by,

the product.

a162. Fixed manufacturing costs are treated as period costs under ______________________.

Cost-Volume-Profit Analysis: Additional Issues

FOR INSTRUCTOR USE ONLY

19 – 49

a163. When production exceeds sales, a portion of the _____________________ is deferred to

a future period as part of the cost of ending inventory under absorption costing, but not

under variable costing.

a164. When units produced exceed units sold, income under absorption costing is ___________

than income under variable costing.

a165. Management may be tempted to overproduce in a given period in order to increase net

income if _______________ is used for internal decision making.

Answers to Completion Statements

SHORT-ANSWER ESSAY QUESTIONS

S-A E 166

A CVP income statement is frequently prepared for internal use by management. Describe the

features of the CVP income statement that make it more useful for management decision-making

than the traditional income statement that is prepared for external users.

S-A E 167

Nancy Sound, president of Crosley Corp., has heard about operating leverage and asks you to

explain this term. What is operating leverage? How does a company increase its operating

leverage?

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

FOR INSTRUCTOR USE ONLY

19 – 50

Solution 167

aS-A E 168

Define variable costing and absorption costing. What are some of the benefits to a manager from

using variable costing instead of absorption costing for internal decision making?

saS-A E 169

How do differences in production and sales levels affect income under absorption and variable

costing?