Principles of Managerial Finance, 15e (Zutter)

Chapter 19 International Managerial Finance

19.1 The multinational company and its environment

1) NAFTA is a treaty establishing free trade and open markets among Europe and the United States.

2) The World Trade Organization is an international body established to police world trading practices

and to mediate disputes among member countries.

3) Offshore Centers are cities or states that have achieved prominence as major centers for Euromarket

business.

4) NAFTA is an international financial market that provides for borrowing and lending currencies

outside their country of origin.

5) Fluctuations in foreign exchange markets can affect foreign revenues and profits of a multinational

company, but they have no impact on its overall value.

6) The Euromarket is the international financial market that provides for borrowing and lending

currencies outside their country of origin.

7) The Euromarket provides multinational companies with an external opportunity to borrow or lend

funds with the additional feature of less government regulation.

8) The existence of specific regulations and controls on dollar deposits in the United States, including

interest rate ceiling imposed by the government, has contributed to the growth of the Euromarket.

9) A joint venture is a partnership under which the participants have contractually agreed to contribute

specified amounts of money and expertise in exchange for stated proportions of ownership and profit.

10) The official melding of the national currencies of the European Union into one currency, the euro,

created the European monetary union in 2002.

11) Mercosur is a major South American trading bloc that includes countries that account for more than

half of the total of Latin America’s GDP.

12) The Mercosur is a major European trading bloc that includes former Soviet bloc countries in Eastern

Europe.

13) Multinational companies are firms that have international assets but operations in domestic markets

only and draw part of their total revenue and profits from such markets.

14) In 2003-2004, the United States signed a regional trade pact with the Dominican Republic, Costa Rica,

El Salvador, Guatemala, Honduras, and Nicaragua called the Central American Free Trade Agreement or

CAFTA.

15) As a result of the Maastricht Treaty of 1991, 12 EU nations adopted a single currency, the euro, as a

continent-wide medium of exchange.

16) In the grossing up procedure, MNCs add the before-tax subsidiary income to their total taxable

income, calculate the U.S. tax liability on the grossed -up income, and the related taxes are paid in the

foreign country are applied as a credit against the additional U.S. tax liability.

17) A partnership between a multinational company and a foreign investor in which contractually

specified amounts of money and expertise are contributed by the participants for stated proportions of

ownership and profit is a ________.

A) multinational corporation

B) floating relationship

C) joint venture

D) consolidation

18) The ________ is the taxation technique that increases the U.S. income of an MNC by the amount of

foreign income (before foreign taxes). The U.S. tax calculation is then based on that higher level.

A) unitary tax law

B) grossing up procedure

C) GmbH

D) nationalization procedure

19) Which of the following is considered as a major offshore center for Euromarket business?

A) Cuba

B) North Korea

C) Iran

D) Hong Kong

20) A partnership under which the participants have contractually agreed to contribute specified amounts

of money and expertise in exchange for stated proportions of ownership and profit is called a(n)

________.

A) S corporation

B) GmbH

C) S.A.R.L.

D) joint venture

21) Which of the following factors can influence the operations of an MNC?

A) foreign ownership of portions of equity

B) debt and equity structures based on home country’s capital market

C) dividend payout policy

D) consolidation of financial statements based on only one currency

22) Which of the following is a reason for growth of the Euromarket?

A) The sudden decline of U.S dollars after the introduction of Euro.

B) The functional-currency-denominated financial statements of the foreign subsidiary were translated

into the parent’s currency without authorization.

C) The existence of offshore centers caused massive financial losses and problems for MNCs.

D) The consistently large U.S. balance-of-payments deficits helped scatter dollars around the world.

23) The negative implications for the operation of a foreign-based subsidiary due to joint venture laws

and restrictions can result in ________.

A) high degree of leverage

B) deficit in balance-of-payment position for the home country

C) difficulties obtaining the remission of profits

D) manipulation of tax rules

24) The ________ is a significant economic force currently made up of 28 nations with a population of

more than 500 million that permits free trade within the countries that make up this group.

A) North American Free Trade Agreement (NAFTA)

B) Mercosur Group

C) Asian Economic Area Network (ASEAN)

D) European Union (EU)

25) ________ is a major South American trading bloc that includes countries that account for more than

half of total Latin American GDP.

A) The group of five

B) Mercosur

C) Latin and South American Free Trade Area (LASTA)

D) The group of seven

26) CAFTA is ________.

A) a treaty establishing free trade and open markets between Europe and five Central American

Countries

B) a major South American trading bloc that includes countries that account for more than half of total

Latin American GDP

C) a significant economic force currently made up of 28 nations with a population of more than 500

million that permits free trade within the countries that make up this group

D) a trade agreement signed in 2003—2004 by the United States, the Dominican Republic, and five

Central American countries

27) ________ is an international body that polices world commercial trading practices and mediates

disputes among two or more member countries.

A) NAFTA

B) GATT

C) WTO

D) CAFTA

28) ________ is a treaty that has governed world trade throughout most of the post World War II era.

A) NAFTA

B) GATT

C) WTO

D) CAFTA

19.2 Financial statements

1) FASB No. 52 requires U.S. multinationals to first convert the financial statement accounts of foreign

subsidiaries into their functional currency and then to translate the accounts into the parent firm’s

currency using the all-current-rate method.

2) The all-current-rate method is the method by which the functional currency-denominated financial

statements of an MNC’s subsidiary are translated into the parent company’s currency.

3) Self-sustaining foreign entity operates independent of the parent multinational and the current-rate

method is the primary approach for translation of individual accounts.

4) The temporal method requires specific assets and liabilities to be translated at so-called historic

exchange rates and that foreign-exchange translation gains or losses be reflected in the current year‘s

income.

5) Current U.S. tax laws require the separation of financial statements of subsidiaries and the operating

results for some subsidiaries are excluded from the parent entirely for some countries such as China and

India.

6) A functional currency is the currency of the parent company’s country.

7) A functional currency is the currency of the host country in which a subsidiary primarily generates and

expends cash and in which its accounts are maintained.

8) FASB No. 52 is a statement issued by the Financial Accounting Standards Board requiring American

MNCs to first convert the financial statement accounts of foreign subsidiaries into the country’s

functional currency and then translate the accounts into the parent firm’s currency using the ________

method.

A) historical rate

B) all-current-rate

C) average rate

D) weighted average

9) The all-current-rate method dictated by the FASB No. 52 statement requires the translation of all

balance sheet accounts at the ________ rate and all income statement items at the ________ rates.

A) closing; average

B) average; closing

C) historical; current

D) average; historical

10) Harry Mining, a U.S.-based MNC has a foreign subsidiary that earns $1,050,000 before local taxes,

with all the after tax funds to be available to the parent in the form of dividends. The foreign income tax

rate is 30 percent, the foreign dividend withholding tax rate is 15 percent, and the firm’s U.S. tax rate is 35

percent. What are the funds available to the parent MNC if foreign taxes can be applied as a credit against

the MNC’s U.S. tax liability?

A) $624,750

B) $425,250

C) $257,250

D) $735,000

11) Harry Mining, a U.S.-based MNC has a foreign subsidiary that earns $1,050,000 before local taxes,

with all the after tax funds to be available to the parent in the form of dividends. The foreign income tax

rate is 30 percent, the foreign dividend withholding tax rate is 15 percent, and the firm’s U.S. tax rate is 35

percent. What are the funds available to the parent MNC if no tax credits are allowed?

A) $624,752

B) $425,250

C) $406,088

D) $735,000

12) A U.S.-based MNC has three subsidiaries: S1 (40 percent owned by the MNC); S2 (33 percent owned

by S1), and S3 (20 percent owned by S2). The taxable income for each firm is $100 million. The local taxes

for each firm are $15 million, $20 million, and $10 million, respectively. The MNC’s tax rate is 40 percent.

(a) Can the MNC apply all of its local taxes as a credit against its U.S. taxes?

(b) Based on the “grossing up” concept, calculate all tax credits applicable to the MNC.

11

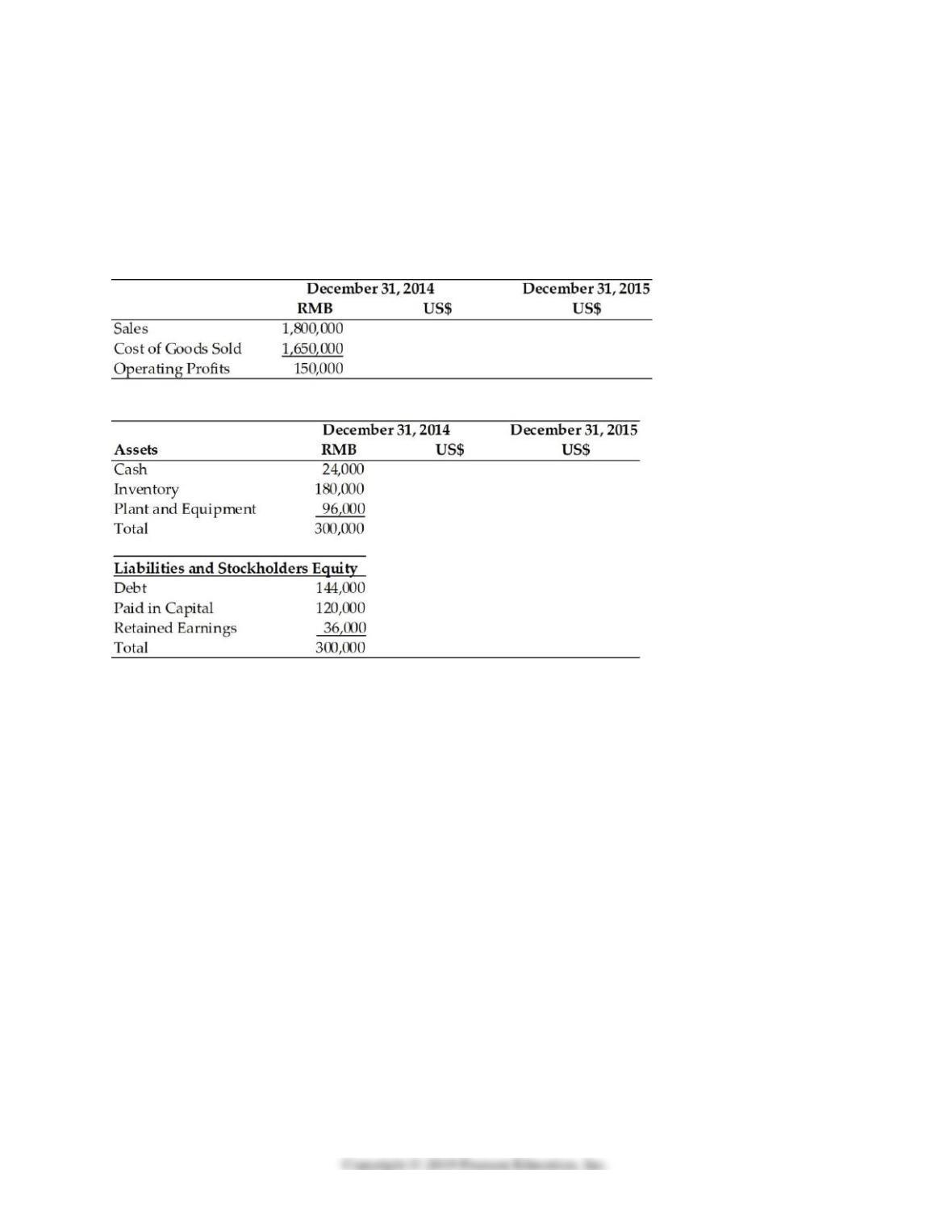

13) A U.S-based MNC has a subsidiary in China where the local currency is the Renminbi (RMB). The

balance sheets and income statements of the subsidiary are presented in the table below. On December

31, 2014, the exchange rate was 8.27 RMB/US$. Assume the local currency figures in the statement below

remain the same on December 31, 2015. Calculate the U.S. dollar translated figures for the two ending

time periods assuming that between December 31, 2014 and December 31, 2015, the Chinese government

revalues (appreciates) the RMB by 20 percent.

Translation of Income Statement

Translation of Balance Sheet

19.3 Risk

1) The spot exchange rate is the rate of exchange between two currencies at some specified future date.

2) The forward exchange rate is the rate of exchange between two currencies on any given day.

3) The functional currency is the currency in which a business entity primarily generates and expends

cash and in which its accounts are maintained.

4) Accounting exposure is the risk resulting from the effects of changes in foreign exchange rates on the

translated value of a firm’s financial statement accounts denominated in a given foreign currency.

5) Economic exposure is the risk resulting from the effects of changes in foreign exchange rates on a firm’s

value.

6) The three basic types of risks associated with international cash flows are business and financial risks,

inflation and exchange rate risks, and political risks.

7) Countries that experience high inflation rates will see their currencies decline in value relative to the

currencies of countries with lower inflation rates.

8) When more units of a foreign currency are required to buy one dollar, the currency is said to have

appreciated with respect to the dollar.

9) Although several economic and political factors can influence foreign exchange rate movements, by far

the most important explanation for long-term changes in exchange rates is a differing inflation rate

between two countries.

10) Although several economic and political factors can influence foreign exchange rate movements, by

far the most important explanation for long-term changes in exchange rates is fiscal policy that a country

adopts.

11) Macro political risk is the risk faced by all foreign firms in a host country related to political change,

revolution, or the adoption of new policies by the government of host country.

12) Micro political risk is the risk faced by all foreign firms in a host country related to political change,

revolution, and the adoption of new policies by the government of host country.

13) Recent years have seen the emergence of a third path to political risk that encompasses “global” events

such as terrorism, antiglobalization movements and protests, Internet-based risks, and concerns over

poverty, AIDS, and the environment all affect various MNCs’ operations worldwide.

14) National entry control systems are comprehensive rules, regulations, and incentives introduced by

host governments to regulate inflows of foreign direct investment from MNCs and at the same time

extract more benefits from their presence.

15) National entry control systems are comprehensive rules, regulations, and immigration policies

introduced by xenophobic host governments to regulate inflows of foreign workers.

16) Both theory and empirical evidence indicate that the capital structures of MNCs differ from those of

purely domestic firms.

17) Both theory and empirical evidence indicate that the capital structures of MNCs are not different from

those of purely domestic firms.