Corporate Finance, 4e (Berk / DeMarzo)

Chapter 18 Capital Budgeting and Valuation with Leverage

18.1 Overview of Key Concepts

1) Which of the following is NOT one of the simplifying assumptions made for the three main methods

of capital budgeting?

A) The firm pays out all earnings as dividends.

B) The project has average risk.

C) Corporate taxes are the only market imperfection.

D) The firm’s debt-equity ratio is constant.

2) Which of the following methods are used in capital budgeting decisions?

A) WACC method

B) APV method

C) FTE method

D) All of the above are used in capital budgeting decisions.

3) The assumption that the firm’s debt-equity ratio is constant means:

A) the firm’s cost of capital will not fluctuate when it accepts a new project.

B) corporate taxes are the only imperfection.

C) the risk of its debt and equity will change when it accepts a new project.

D) the firm adjusts its leverage to maintain a constant debt-equity ratio in terms of book value.

18.2 The Weighted Average Cost of Capital Method

1) Which of the following statements is FALSE?

A) Because the WACC incorporates the tax savings from debt, we can compute the levered value of an

investment, which is its value including the benefit of interest tax shields given the firm’s leverage

policy, by discounting its future free cash flow using the WACC.

B) The WACC incorporates the benefit of the interest tax shield by using the firm’s before–tax cost of

capital for debt.

C) When the market risk of the project is similar to the average market risk of the firm’s investments,

then its cost of capital is equivalent to the cost of capital for a portfolio of all of the firm’s securities; that

is, the project’s cost of capital is equal to the firm’s weighted average cost of capital (WACC).

D) A project’s cost of capital depends on its risk.

2) Which of the following statements is FALSE?

A) The WACC can be used throughout the firm as the company wide cost of capital for new

investments that are of comparable risk to the rest of the firm and that will not alter the firm’s debt–

equity ratio.

B) A disadvantage of the WACC method is that you need to know how the firm’s leverage policy is

implemented to make the capital budgeting decision.

C) The intuition for the WACC method is that the firm’s weighted average cost of capital represents the

average return the firm must pay to its investors (both debt and equity holders) on an after-tax basis.

D) To be profitable, a project should generate an expected return of at least the firm’s weighted average

cost of capital.

3) Which of the following is NOT a step in the WACC valuation method?

A) Compute the value of the investment, including the tax benefit of leverage, by discounting the free

cash flow of the investment using the WACC.

B) Compute the weighted average cost of capital.

C) Determine the free cash flow of the investment.

D) Adjust the WACC for the firm’s current debt/equity ratio.

4) Consider the following equation:

rwacc = rE + rD(1 – τc)

the term E in this equation is:

A) the dollar amount of equity.

B) the dollar amount of debt.

C) the required rate of return on debt.

D) the required rate of return on equity.

5) Consider the following equation:

rwacc = rE + rD(1 – τc)

the term D in this equation is:

A) the dollar amount of debt.

B) the required rate of return on equity.

C) the required rate of return on debt.

D) the dollar amount of equity.

6) Consider the following equation:

rwacc = rE + rD(1 – τc)

the term rE in this equation is:

A) the after tax required rate of return on debt.

B) the required rate of return on debt.

C) the required rate of return on equity.

D) the dollar amount of equity.

7) Consider the following equation:

rwacc = rE + rD(1 – τc)

the term rD(1 – τc) in this equation is:

A) the required rate of return on debt.

B) the dollar amount of equity.

C) the after tax required rate of return on debt.

D) the required rate of return on equity.

8) Consider the following equation:

Dt = d ×

the term Dt in this equation is:

A) the firms target debt to value ratio.

B) the firms target debt to equity ratio.

C) the investment’s debt capacity.

D) the dollar amount of debt outstanding at time t.

9) Consider the following equation:

Dt = d ×

the term d in this equation is:

A) the firms target debt to value ratio.

B) the dollar amount of debt outstanding at time t.

C) the firms target debt to equity ratio.

D) the investment’s debt capacity.

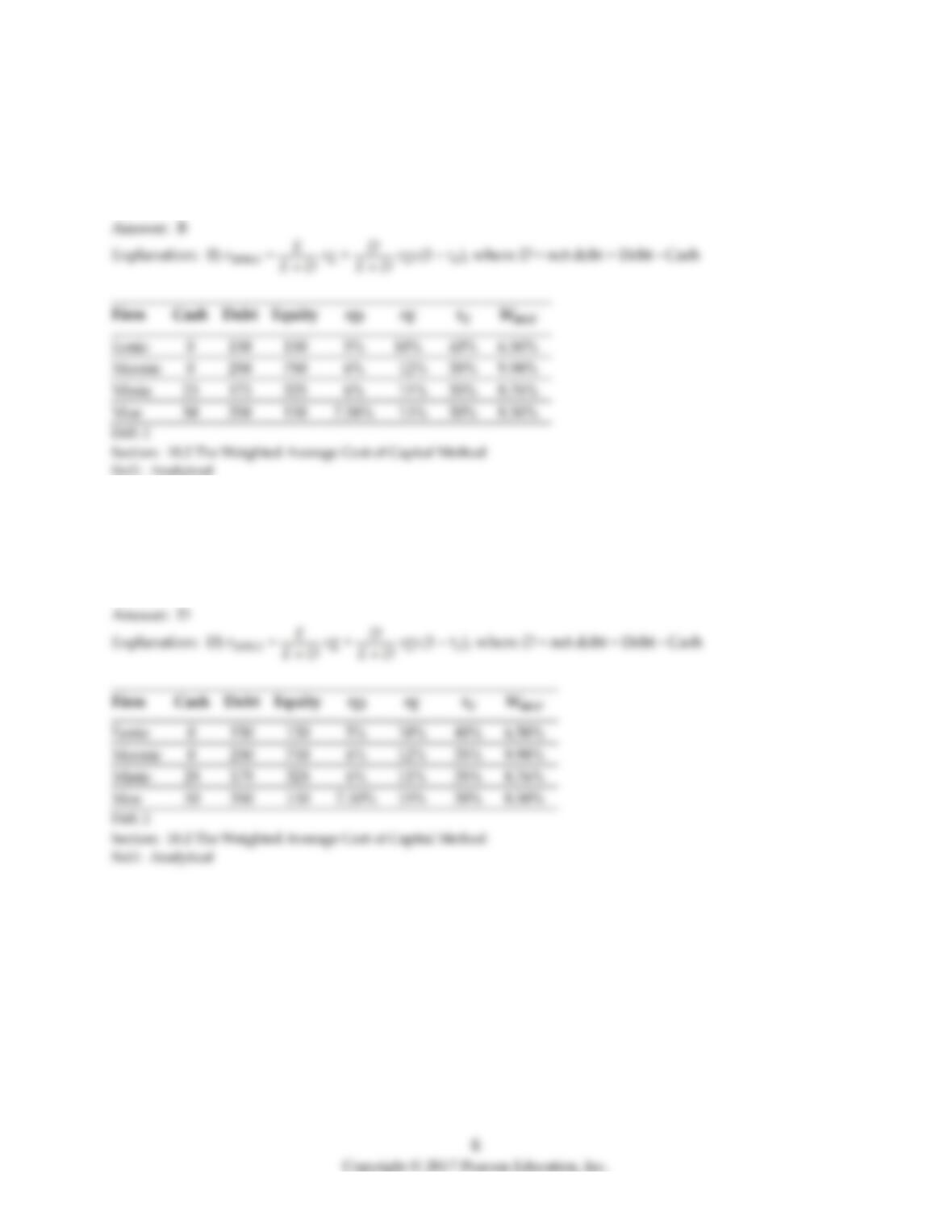

Use the table for the question(s) below.

Consider the information for the following four firms:

Firm

Cash

Debt

Equity

rD

rE

τc

Eenie

0

150

150

5%

10%

40%

Meenie

0

250

750

6%

12%

35%

Minie

25

175

325

6%

11%

35%

Moe

50

350

150

7.50%

15%

30%

10) The weighted average cost of capital for “Eenie” is closest to:

A) 6.0%

B) 6.5%

C) 7.5%

D) 5.5%

Eenie

150

150

5%

10%

40%

Meenie

250

750

6%

12%

35%

Minie

25

175

325

6%

11%

35%

11) The weighted average cost of capital for “Meenie” is closest to:

A) 10.5%

B) 7.4%

C) 10.0%

D) 8.8%

Eenie

150

150

5%

10%

40%

Meenie

250

750

6%

12%

35%

Minie

25

175

325

6%

11%

35%

Moe

50

350

150

15%

30%

12) The weighted average cost of capital for “Minie” is closest to:

A) 9.50%

B) 8.75%

C) 6.75%

D) 8.25%

13) The weighted average cost of capital for “Moe” is closest to:

A) 10.00%

B) 7.75%

C) 8.25%

D) 8.50%

Use the information for the question(s) below.

Omicron Industries’ Market Value Balance Sheet ($ Millions)

and Cost of Capital

Assets

Liabilities

Cost of Capital

Cash

0

Debt

200

Debt

6%

Other Assets

500

Equity

300

Equity

12%

τc

35%

Omicron Industries New Project Free Cash Flows

Year

0

1

2

3

Free Cash Flows

($100)

$40

$50

$60

Assume that this new project is of average risk for Omicron and that the firm wants to hold constant its

debt to equity ratio.

14) Omicron’s weighted average cost of capital is closest to:

A) 7.10%

B) 7.50%

C) 9.60%

D) 8.75%

15) The NPV for Omicron’s new project is closest to:

A) $23.75

B) $27.50

C) $28.75

D) $25.75

16) The Debt Capacity for Omicron’s new project in year 0 is closest to:

A) $38.75

B) $75.50

C) $50.25

D) $10.25

17) The Debt Capacity for Omicron’s new project in year 1 is closest to:

A) $38.75

B) $48.25

C) $50.25

D) $58.00

18) The Debt Capacity for Omicron’s new project in year 2 is closest to:

A) $55.25

B) $38.75

C) $22.00

D) $33.00

Use the information for the question(s) below.

Iota Industries Market Value Balance Sheet ($ Millions) and Cost of Capital

Assets

Liabilities

Cost of Capital

Cash

250

Debt

650

Debt

7%

Other Assets

1200

Equity

800

Equity

14%

τc

35%

Iota Industries New Project Free Cash Flows

Year

0

1

2

3

Free Cash Flows

($250)

$75

$150

$100

Assume that this new project is of average risk for Iota and that the firm wants to hold constant its debt

to equity ratio.

19) Iota’s weighted average cost of capital is closest to:

A) 8.40%

B) 9.75%

C) 10.85%

D) 11.70%

20) The NPV for Iota‘s new project is closest to:

A) $25.25

B) $13.25

C) $9.00

D) $18.50

21) The Debt Capacity for Iota’s new project in year 0 is closest to:

A) $263.25

B) $87.75

C) $50.25

D) $118.00

22) Calculate the NPV for Iota’s new project.

12

Use the information for the question(s) below.

Omicron Industries’ Market Value Balance Sheet ($ Millions)

and Cost of Capital

Assets

Liabilities

Cost of Capital

Cash

0

Debt

200

Debt

6%

Other Assets

500

Equity

300

Equity

12%

τc

35%

Omicron Industries New Project Free Cash Flows

Year

0

1

2

3

Free Cash Flows

($100)

$40

$50

$60

Assume that this new project is of average risk for Omicron and that the firm wants to hold constant its

debt to equity ratio.

23) Calculate the debt capacity of Omicron’s new project for years 0, 1, and 2.

13

24) Suppose Luther Industries is considering divesting one of its product lines. The product line is

expected to generate free cash flows of $2 million per year, growing at a rate of 3% per year. Luther has

an equity cost of capital of 10%, a debt cost of capital of 7%, a marginal tax rate of 35%, and a debt–

equity ratio of 2. If this product line is of average risk and Luther plans to maintain a constant debt–

equity ratio, what after- tax amount must it receive for the product line in order for the divestiture to be

profitable?

18.3 The Adjusted Present Value Method

1) Which of the following is NOT a step in the adjusted present value method?

A) Deducting costs arising from market imperfections

B) Calculating the unlevered value of the project

C) Calculating the after-tax WACC

D) Calculating the value of the interest tax shield

2) Which of the following statements is FALSE?

A) The firm’s unlevered cost of capital is equal to its pre–tax weighted average cost of capital – that is,

using the pre-tax cost of debt, rd, rather than its after-tax cost, rd (1 – τc ).

B) A firm’s levered cost of capital is a weighted average of its equity and debt costs of capital.

C) When the firm maintains a target leverage ratio, its future interest tax shields have similar risk to the

project’s cash flows, so they should be discounted at the project’s unlevered cost of capital.

D) The first step in the APV method is to calculate the value of free cash flows using the project‘s cost of

capital if it were financed without leverage.

3) Which of the following statements is FALSE?

A) To determine the project’s debt capacity for the interest tax shield calculation, we need to know the

value of the project.

B) To compute the present value of the interest tax shield, we need to determine the appropriate cost of

capital.

C) Because we don’t value the tax shield separately, with the APV method we need to include the

benefit of the tax shield in the discount rate as we do in the WACC method.

D) A target leverage ratio means that the firm adjusts its debt proportionally to the project’s value or its

cash flows.

4) Which of the following statements is FALSE?

A) The APV approach explicitly values the market imperfections and therefore allows managers to

measure their contribution to value.

B) We need to know the debt level to compute the APV, but with a constant debt–equity ratio we need

to know the project’s value to compute the debt level.

C) The WACC method is more complicated than the APV method because we must compute two

separate valuations: the unlevered project and the interest tax shield.

D) Implementing the APV approach with a constant debt-equity ratio requires solving for the project’s

debt and value simultaneously.

Use the table for the question(s) below.

Consider the information for the following four firms:

Firm

Cash

Debt

Equity

rD

rE

τc

Eenie

0

150

150

5%

10%

40%

Meenie

0

250

750

6%

12%

35%

Minie

25

175

325

6%

11%

35%

Moe

50

350

150

7.50%

15%

30%

5) The unlevered cost of capital for “Eenie” is closest to:

A) 6.0%

B) 5.5%

C) 7.5%

D) 6.5%

Eenie

150

150

Meenie

250

750

Minie

25

175

325

11%

35%

Moe

50

350

150

6) The unlevered cost of capital for “Moe” is closest to:

A) 8.25%

B) 7.75%

C) 8.50%

D) 10.00%

Eenie

0

150

150

Meenie

0

250

750

12%

35%

Minie

25

175

325

11%

35%

Moe

50

350

150

15%

30%

Use the information for the question(s) below.

Suppose Luther Industries is considering divesting one of its product lines. The product line is

expected to generate free cash flows of $2 million per year, growing at a rate of 3% per year. Luther has

an equity cost of capital of 10%, a debt cost of capital of 7%, a marginal tax rate of 35%, and a debt–

equity ratio of 2. This product line is of average risk and Luther plans to maintain a constant debt–

equity ratio.

7) Luther’s Unlevered cost of capital is closest to:

A) 8.0%

B) 8.5%

C) 9.0%

D) 6.4%

8) The unlevered value of Luther’s Product Line is closest to:

A) $25 million

B) $60 million

C) $45 million

D) $40 million

Use the information for the question(s) below.

Omicron Industries’ Market Value Balance Sheet ($ Millions)

and Cost of Capital

Assets

Liabilities

Cost of Capital

Cash

0

Debt

200

Debt

6%

Other Assets

500

Equity

300

Equity

12%

τc

35%

Omicron Industries New Project Free Cash Flows

Year

0

1

2

3

Free Cash Flows

($100)

$40

$50

$60

Assume that this new project is of average risk for Omicron and that the firm wants to hold constant its

debt to equity ratio.

9) Omicron’s Unlevered cost of capital is closest to:

A) 8.75%

B) 7.10%

C) 9.60%

D) 7.50%

10) The unlevered value of Omicron’s new project is closest to:

A) $96

B) $124

C) $126

D) $25

11) The interest tax shield provided by Omicron’s new project in year 1 is closest to:

A) $3.00

B) $1.05

C) $50.25

D) $17.60

Use the information for the question(s) below.

Suppose that Rose Industries is considering the acquisition of another firm in its industry for $100

million. The acquisition is expected to increase Rose’s free cash flow by $5 million the first year, and

this contribution is expected to grow at a rate of 3% every year there after. Rose currently maintains a

debt to equity ratio of 1, its marginal tax rate is 40%, its cost of debt rD is 6%, and its cost of equity rE is

10%. Rose Industries will maintain a constant debt-equity ratio for the acquisition.

12) Rose’s unlevered cost of capital is closest to:

A) 8.0%

B) 7.5%

C) 7.0%

D) 9.0%

13) The unlevered value of Rose’s acquisition is closest to:

A) $63 million

B) $50 million

C) $167 million

D) $100 million

14) Given that Rose issues new debt of $50 million initially to fund the acquisition, the present value of

the interest tax shield for this acquisition is closest to:

A) $24 million

B) $50 million

C) $20 million

D) $15 million