Principles of Managerial Finance, 15e (Zutter)

Chapter 17 Hybrid and Derivative Securities

17.1 Overview of hybrids and derivatives

1) Derivatives are used by corporations as a useful tool for managing certain aspects of a firm’s risk.

2) An option derives its value from an underlying asset that is often another security.

3) Preferred stock is considered a hybrid security because it blends the characteristics of both debt and

equity.

4) A hybrid security is neither debt nor equity but instead derives its value from an underlying asset.

5) A hybrid security is a form of debt or equity financing that possesses characteristics of both debt and

equity.

6) A derivative security is neither debt nor equity but instead derives its value from an underlying asset.

7) Which of the following securities is a popular hybrid security?

A) preferred stock

B) common stock

C) options

D) futures

8) A form of debt or equity that possesses characteristics of both debt and equity financing is called

________.

A) hybrid security

B) convertible security

C) derivative security

D) cumulative security

9) In their simplest form, bonds are pure ________.

A) debt

B) equity

C) hybrid security

D) current assets

10) A(n) ________ is neither debt nor equity but derives its value from an underlying asset.

A) derivative security

B) hybrid security

C) financing lease

D) operating lease

17.2 Leasing

1) A lessee is the receiver of the services of the assets under a lease whereas a lessor is the owner of the

assets that are being leased.

2) A lessor is the receiver of the services of the assets under a lease whereas a lessee is the owner of the

assets that are being leased.

3) Leasing is considered a source of financing provided by the lessee to the lessor.

4) An operating lease is often referred as a capital lease.

5) A financial lease is often referred as a capital lease.

6) If a lessee leases (under a financial lease) an asset that subsequently becomes obsolete, it can require the

lessor to replace it with an equally productive asset in real term over the remaining term of the lease.

7) An operating lease is noncancellable and obligates the lessee to make payments for the use of an asset

over a predefined period of time.

8) A financial lease is a cancelable contractual arrangement whereby the lessee agrees to make periodic

payments to the lessor, often for five or fewer years, for an asset’s services.

9) In a financial lease, the lessor must receive more than the asset‘s purchase price in order to earn its

required return on the investment.

10) A direct lease is a lease under which the lessee sells an asset for cash to a prospective lessor and then

leases back the same asset, making fixed periodic payments for its use.

11) Maintenance clauses are provisions normally included in an operating lease that require the lessor to

maintain the assets and to make insurance and tax payments.

12) Renewal options normally require the lessor to maintain the assets and to make insurance and tax

payments.

13) Renewal options are provisions normally included in an operating lease that grant the lessee the right

to re-lease assets at the expiration of the lease.

14) Purchase options are provisions frequently included in both operating and financial leases that allow

the lessee to purchase the leased asset at maturity.

15) Renewal options are provisions frequently included in both operating and financial leases that allow

the lessee to purchase the leased asset at maturity.

16) A leveraged lease is a lease under which the lessee sells an asset for cash to a prospective lessor and

then leases back the same asset, making fixed periodic payments for its use.

17) An operating lease is when the present value of all its payments included as an asset and

corresponding liability on a firm’s balance sheet.

18) If a lease meets any of the FASB Standards No. 13 criteria, it should be shown as a capitalized lease,

meaning the present value of all its payments should be included as an asset and corresponding liability

on a firm’s balance sheet.

19) An operating lease need not be capitalized, but its basic features must be disclosed in a footnote to the

financial statements.

20) Since operating leases result in the receipt of services from an asset without increasing the assets or

liabilities on a firm’s balance sheet, leasing may result in misleading financial ratios.

21) At the end of the term of the lease agreement, the terminal value of an asset, if any, is realized by the

lessee.

22) When a firm becomes bankrupt or is reorganized, the maximum claim of lessors against the

corporation is three years of lease payments.

23) Leasing allows the lessee, in effect, to depreciate land, which is prohibited if the land were purchased.

24) A lease arrangement has many more restrictive covenants than those that are normally included as

part of a long-term loan.

25) One advantage of leasing is that in many cases, the return to the lessor is quite low so the firm in need

of an asset might be better off borrowing to purchase it.

26) One disadvantage of leasing is that in many cases, the return to the lessor is quite high so the firm in

need of an asset might be better off borrowing to purchase it.

27) A(n) ________ lease is a contractual arrangement whereby the lessee agrees to make periodic

payments to the lessor for five or fewer years for an asset’s services. This type of lease may also be

canceled at the option of the lessee.

A) financial

B) operating

C) capital

D) direct

28) Assets leased under ________ leases generally have a usable life longer than the term of the lease.

A) financial

B) operating

C) capital

D) direct

29) ________ leases are noncancellable and are generally used for leasing land, buildings, and large pieces

of fixed equipment.

A) Financial

B) Operating

C) Leveraged

D) Direct

30) The total payments of ________ lease over the lease period are greater than the initial cost of the

leased asset to the lessor.

A) a financial

B) an operating

C) a leveraged

D) a direct

31) Under FASB Standard No. 13, which of the following element should be present to qualify as a capital

lease?

A) The lease does not transfer ownership of the property to the lessee by the end of the lease.

B) The lease contains an option to purchase the property at a “bargain” price.

C) The lease term is less than 50 percent of the economic life of the property.

D) At the beginning of the lease, the present value of the lease payment is equal to 50 percent or more of

the fair market value of the leased property less any investment tax credit received by the lessor.

32) FASB Standard No. 13 requires explicit disclosure of ________ obligation on the firm’s balance sheet.

A) an operating lease

B) a leveraged lease

C) a sale-leaseback

D) a capital lease

33) A(n) ________ is a cancelable contractual arrangement whereby the lessee agrees to make periodic

payments to the lessor, often for 5 or fewer years, to obtain an asset’s services.

A) operating lease

B) financial lease

C) capital lease

D) direct lease

34) A(n) ________ is a noncancellable arrangement that requires the lessee to make payments for the use

of an asset over a relatively long period of time.

A) operating lease

B) financial lease

C) sale-leaseback arrangement

D) direct lease

35) A capital or capitalized lease is also known as ________.

A) an operating lease

B) a financial lease

C) a direct lease

D) a leveraged lease

36) A ________ is normally initiated by a firm that needs funds for operations. Here, lessors acquire

leased assets by purchasing assets already owned by the lessee and leasing them back.

A) direct lease

B) leveraged lease

C) sale-leaseback

D) mortgage

37) In a(n) ________ a lessor owns or acquires the assets that are leased to a given lessee.

A) operating lease

B) financial lease

C) sale-leaseback arrangement

D) direct lease

38) A lease under which a lessee sells an asset for cash to a prospective lessor and then leases back the

same asset is called a(n) ________.

A) operating lease

B) leveraged lease

C) sale-leaseback arrangement

D) direct lease

39) A lease under which a lessor acts as an equity participant, supplying only about 20 percent of the cost

of the asset, while a lender supplies the balance is called a(n)________.

A) operating lease

B) leveraged lease

C) sale-leaseback arrangement

D) direct lease

40) In a ________, the lessor acts as an equity participant supplying part of the necessary capital while a

lender supplies the remaining balance.

A) direct lease

B) leveraged lease

C) sale-leaseback

D) mortgage

41) A type of lease in which the lessor acquires or purchases the asset in order to lease to a given lessee is

known as ________.

A) a mortgage

B) a direct lease

C) a sale-leaseback arrangement

D) a leveraged lease

42) Which of the following must be considered when making a lease-versus-purchase decision?

A) the before-tax cash outflows for each year under the lease alternative

B) the before-tax cash outflows for each year under the purchase alternative

C) the after-tax cash outflows for each year under the lease alternative

D) the depreciation expense under the lease

43) The consequences of missing a financial lease payment are ________ those of missing an interest or

principal payment on debt.

A) less severe than

B) the same as

C) more severe than

D) unrelated to

44) Which of the following is a disadvantage of leasing from a lessee’s perspective?

A) capability of effectively depreciating land

B) ability to avoid restrictive covenants that are normally part of a long-term loan

C) benefit of the salvage value at the end of the term of the lease reverts to the lessor

D) 100 percent debt financing

45) Which of the following is an advantage of leasing from a lessee’s perspective?

A) The return to the lessor is quite high.

B) prohibition on leasehold improvements

C) Maximum claim of the lessor in the event of bankruptcy is ten years of lease payments.

D) Maximum claim of the lessor in the event of bankruptcy is three years of lease payments.

46) Lisa’s Riding Equipment Company has entered into two lease arrangements. One lease is an operating

lease on an office copier requiring annual lease payments of $2,000 for the next three years. The other

lease is a 15-year financial lease on a building requiring annual lease payments of $150,000. If the firm’s

discount rate is 10 percent, how should each lease be presented on the firm’s balance sheet?

47) Dwyer Corporation is determining whether to lease or purchase new equipment. The firm is in the

38% tax bracket, and its after-tax cost of debt is currently 7%. The terms of the lease and the purchase are:

Lease: Annual end–of-year lease payments of $31,500 are required over the 3-year life of the lease. All

maintenance costs will be paid by the lessor; insurance and other costs will be borne by the lessee. The

lessee will exercise its option to purchase the equipment for $6,000 at the termination of the lease.

Purchase: The equipment, costing $77,000, can be financed entirely with a 12% loan requiring annual end–

of-year payments of $32,059 for 3 years. The firm will depreciate the equipment under MACRS using a 3–

year recovery period (33% in year 1, 45% in year 2, 15% in year 3 and 7% in year 4). The firm will pay

$2,000 per year for a service contract that covers maintenance costs; insurance and other costs will be

borne by the firm. The firm plans to keep the equipment and use it beyond its 3-year recovery period.

Calculate the present value of the cash outflow for both the lease and purchasing and recommend one

alternative.

A) The present value of the cash outflow for the lease is $56,151 and for purchasing is $56,775, therefore

Dwyer should choose the lease.

B) The present value of the cash outflow for the lease is $56,151 and for purchasing is $56,775, therefore

Dwyer should choose purchase.

C) The present value of the cash outflow for the lease is $64,590 and for purchasing is $65,398, therefore

Dwyer should choose the lease.

D) The present value of the cash outflow for the lease is $51,178 and for purchasing is $51,703, therefore

Dwyer should choose the lease.

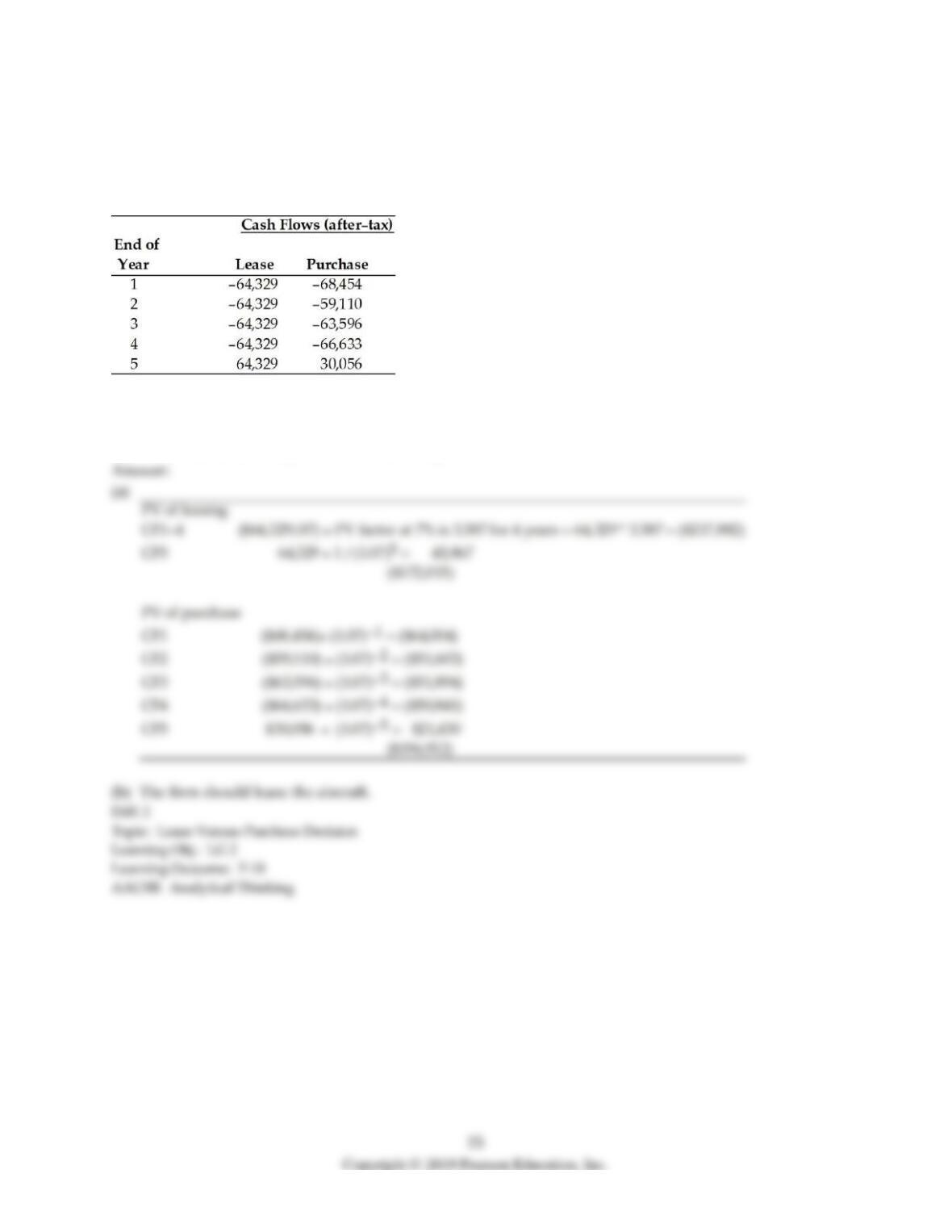

48) Bessey Aviation is considering leasing or purchasing a small aircraft to transport executives between

manufacturing facilities and the main administrative headquarters. The firm is in the 40 percent tax

bracket and its after-tax cost of debt is 7 percent. The estimated after-tax cash flows for the lease and

purchase alternatives are given below:

(a) Given the above cash outflows for each alternative, calculate the present value of the after-tax cash

flows using the after-tax cost of debt for each alternative.

(b) Which alternative do you recommend? Why?

17.3 Convertible securities

1) A conversion feature is an option that is included as part of a common stock issue that allows its holder

to change the stock into a stated number of shares of preferred stock.

2) The conversion ratio is the ratio at which a convertible security can be exchanged for a nonconvertible

security.

3) Diluted earnings per share (EPS) are found by adjusting basic EPS for the impact of converting all

convertibles and exercising all warrants and options that would have diluting effects on a firm’s earnings.

4) The presence of contingent securities such as warrants and stock options affects the reporting of a

firm’s earnings per share.

5) The conversion ratio can be obtained by dividing the par value of the convertible by the conversion

price.

6) The conversion value is the value of a convertible security as measured by the market price of the

common stock into which it can be converted.

7) Contingent securities such as convertibles, warrants, and stock options affect the reporting of a firm’s

earnings per share (EPS).

8) Common stock equivalents are all contingent securities that derive a major portion of their value from

their conversion privileges or common stock characteristics.

9) Contingent securities such as common stocks and bonds affect the reporting of a firm’s earnings per

share (EPS).

10) Convertibles can normally be sold with lower interest rates than nonconvertibles.

11) The conversion feature permits a firm’s capital structure to be changed without increasing the total

financing.

12) By using convertible bonds, an issuing firm can temporarily raise debt, which is typically less

expensive than common stock, to finance projects.

13) Because a security is first sold with a conversion price above the current market price of a firm’s stock,

conversion is initially not attractive.

14) Convertibles can be used as a form of deferred common stock financing.

15) Since the conversion feature provides the purchaser of a convertible bond with the possibility of

becoming a stockholder, convertible bonds are a less expensive form of financing than similar-risk

nonconvertible or straight bonds.

16) Since the purchaser of a convertible security is given an opportunity to become a common

stockholder, convertibles can normally be sold with higher interest rates than nonconvertibles.

17) In case of an overhanging issue, if a firm were to call the issue, the bondholders would accept the call

price rather than converting their bonds.

18) One motive for issuing convertibles is that convertible securities can be issued with far fewer

restrictive covenants than nonconvertibles.

19) An overhanging issue is a convertible security that cannot be forced into conversion by using the call

feature.

20) The conversion feature, which can be part of either a bond or preferred stock, permits a firm to raise

additional funds at some point in the future by selling common stock, thereby shifting the company’s

capital structure to a less highly levered position.

21) Converting a convertible security is beneficial when the market price of the common stock into which

it can be converted is greater than its conversion price.

22) When the market price of the common stock exceeds the conversion price, the conversion (or stock)

value exceeds the par value of the convertible security.

23) Convertible preferred stock is converted into ________.

A) secured bonds

B) debentures

C) shares of common stock

D) warrants

24) A ________ is an option included as part of a bond or preferred stock that permits the holder to

convert the security into a specified number of shares of common stock.

A) put option

B) call option

C) conversion feature

D) repurchase agreement

25) Which of the following is a characteristic of convertible bonds?

A) Conversion increases a firm’s debt ratio.

B) It is a more expensive form of financing than straight bonds.

C) It enhances marketability of a firm’s bonds.

D) It is nothing but a put option.