Process Costing

16 – 41

EXERCISES

Ex. 159

Lutz Company produces a product in two departments: (1) Mixing and (2) Finishing. The

company uses a process cost accounting system.

(a) Purchased raw materials for $50,000 on account.

(b) Raw materials requisitioned for production were:

Direct materials

Mixing department $20,000

Finishing department 14,000

(c) Incurred labor costs of $69,000.

(d) Factory labor used:

Mixing department $44,000

Finishing department 25,000

(e) Manufacturing overhead is applied to the product based on machine hours used in each

department:

Mixing department—300 machine hours at $30 per machine hour.

Finishing department—500 machine hours at $20 per machine hour.

(f) Units costing $56,000 were completed in the Mixing Department and were transferred to the

Finishing Department.

(g) Units costing $60,000 were completed in the Finishing Department and were transferred to

finished goods.

(h) Finished goods costing $40,000 were sold on account for $55,000.

Instructions

Prepare the journal entries to record the preceding transactions for Lutz Company.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 42

Solution 159 (Cont.)

Ex. 160

Sanders Company has two production departments: Fabricating and Finishing. Beginning

inventories are: Work in Process—Fabricating, $6,030; Work in Process—Finishing, $4,100; and

Finished Goods, $5,600. During the month the following transactions occurred:

1. Purchased $40,000 of raw materials on account.

2. Incurred $65,000 of factory labor. Wages are unpaid.

3. Incurred $50,000 of manufacturing overhead; $40,000 was paid and the remainder is unpaid.

4. Requisitioned materials for Fabricating, $10,000 and Finishing, $8,000.

5. Used factory labor for Finishing, $52,000 and Fabricating, $13,000.

6. Applied $45,000 of overhead based on machine hours used in each department. The

Finishing Department used twice as many machine hours as did Fabricating.

Instructions

Journalize the transactions for the month.

Process Costing

16 – 43

Solution 160 (12–16 min.)

Ex. 161

The Pasta Factory manufactures spaghetti sauce through two production departments: Cooking

and Packaging. For the month of February, the work in process accounts show the following

debits:

Cooking Packaging

Beginning work in process $ -0- $ 6,000

Materials 40,000 26,000

Labor 16,000 9,000

Overhead 30,000 19,000

Costs transferred in 65,000

Instructions

Journalize the February transactions that involved the work in process accounts.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 44

Solution 161 (Cont.)

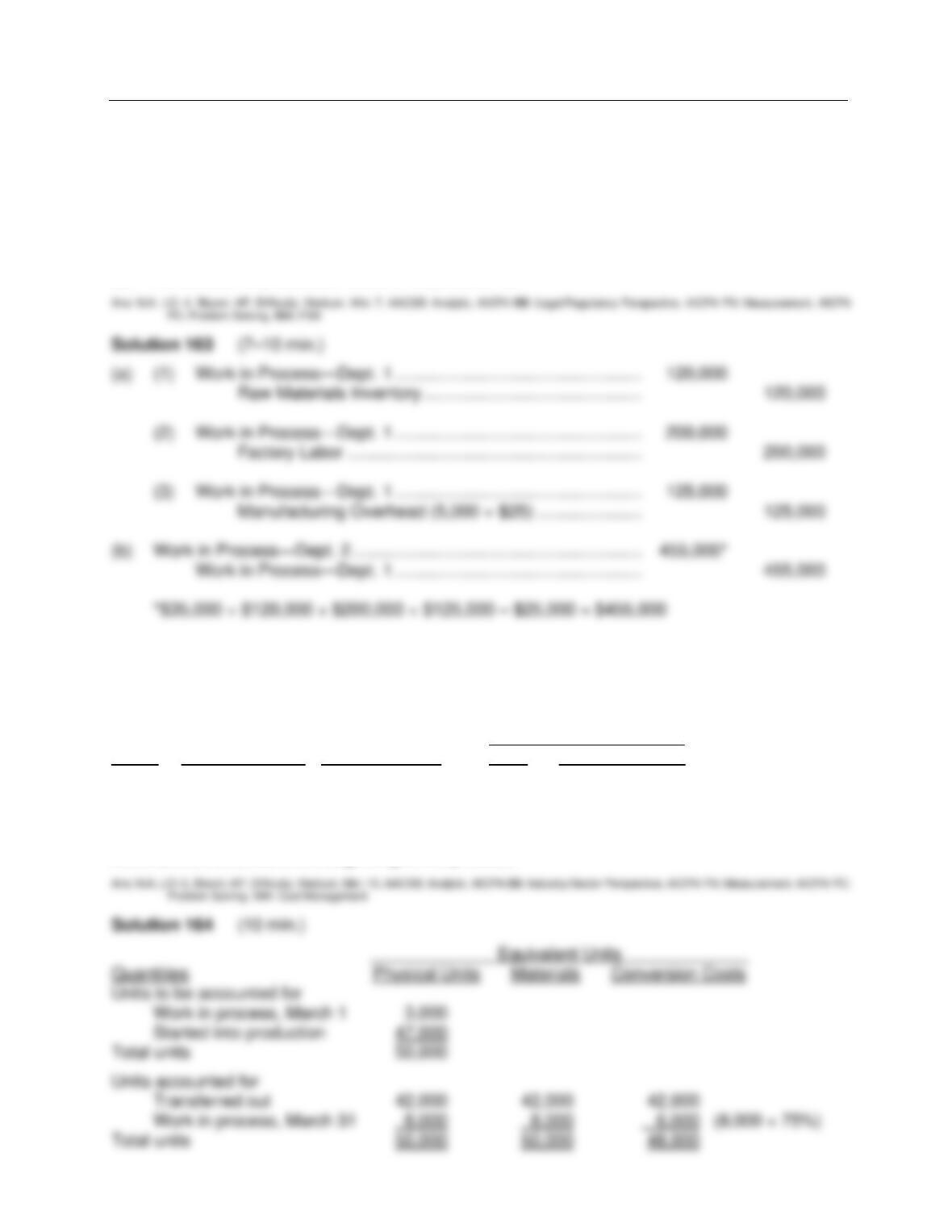

Ex. 162

Benson Industries uses a process cost system. Products are processed first by Department A,

second by Department B, and then they are transferred to the finished goods warehouse. Shown

below is the cost information for Department B during the month of October:

Costs of units transferred in $120,000

Manufacturing costs added in Department B:

Direct materials $50,000

Direct labor 6,000

Manufacturing overhead 19,000 75,000

Total costs charged to Department B in October $195,000

The cost of work in process in Department B at October 1 is $25,000, and the cost of work in

process at October 31 has been determined to be $30,000.

Instructions

Prepare journal entries to record for the month of October:

(a) The transfer of production from Department A to B.

(b) The manufacturing costs incurred by Department B.

(c) The transfer of completed units from Department B to the finished goods warehouse.

Ex. 163

Hardy Company manufactures a single product by a continuous process, involving two production

departments. The records indicate that $120,000 of direct materials were issued to and $200,000

of direct labor was incurred by Department 1 in the manufacture of the product. The factory

overhead rate is $25 per machine hour; machine hours were 5,000 in Department 1. Work in

process in the department at the beginning of the period totaled $35,000; and work in process at

the end of the period was $25,000.

Process Costing

16 – 45

Ex. 163 (Cont.)

Instructions

Prepare entries to record

(a) The flow of costs into Department 1 for

(1) direct materials

(2) direct labor

(3) overhead

(b) The transfer of production costs to Department 2.

Ex. 164

Muffy Painting Company has the following production data for March.

Ending Work in Process

Beginning Units % Complete as to

Month Work in Process Transferred Out Units Conversion Cost

March 3,000 42,000 8,000 75%

Instructions

Compute equivalent units of production for March for both materials and conversion costs.

Materials are entered at the beginning of the process.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 46

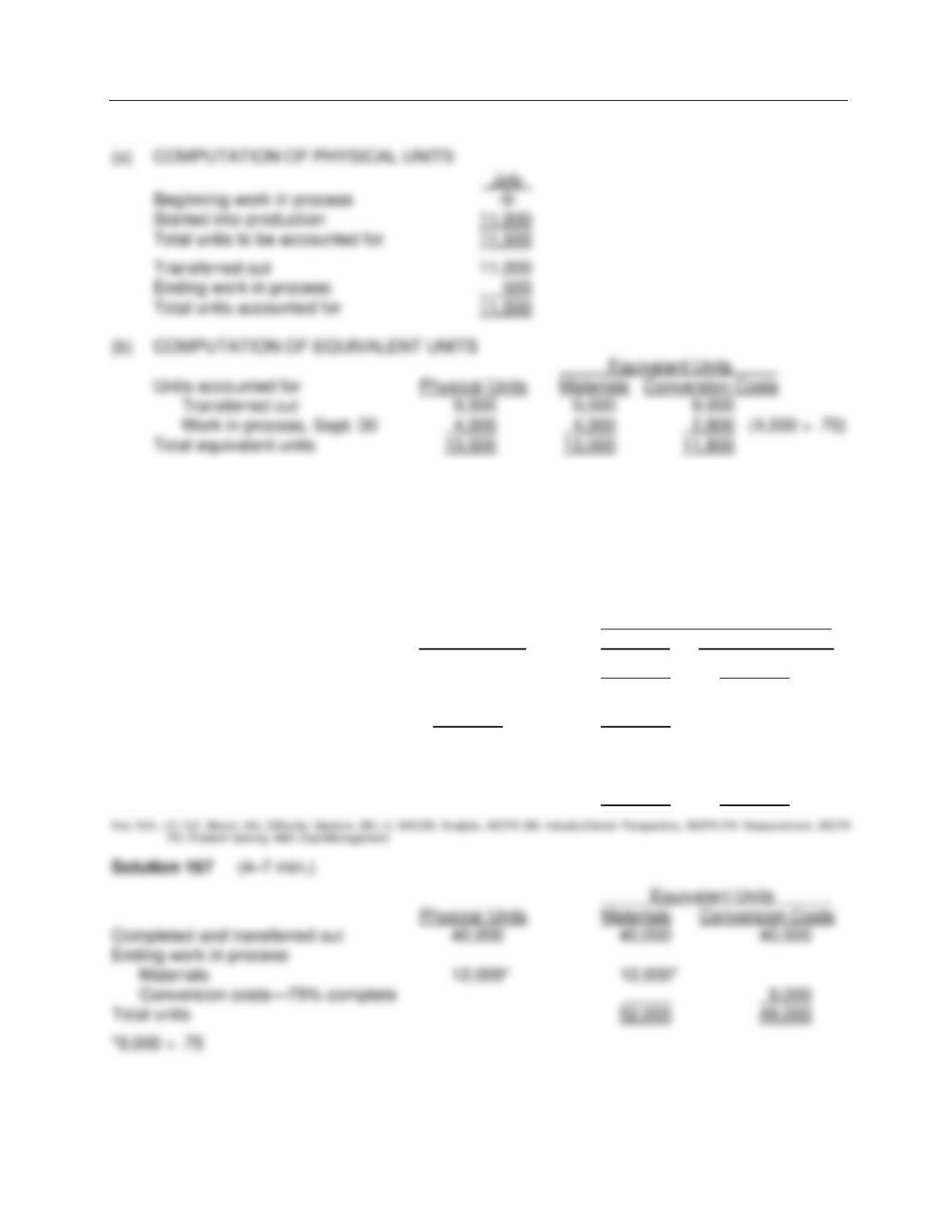

Ex. 165

The Nitrogen Fixation Department of Tomco Company began the month of December with

beginning work in process of 4,000 units that are 100% complete as to materials and 30%

complete as to conversion costs. Units transferred out are 12,000 units. Ending work in process

contains 5,000 units that are 100% complete as to materials and 40% complete as to conversion

costs.

Instructions

Compute the equivalent units of production for materials and conversion costs for the month of

December.

Ex. 166

At Crenshaw Company, materials are entered at the beginning of each process. Work in process

inventories, with the percentage of work done on conversion, and production data for its Painting

Department in selected months are as follows:

Beginning Work In Process Ending Work In Process

Percentage Units Completed Percentage

Month Units Completed and Transferred Out Units Completed

July -0- — 11,000 500 90%

Sept. 2,500 20% 9,000 4,000 70%

Instructions

(a) Compute the physical units for July.

(b) Compute the equivalent units of production for materials and conversion costs for

September.

Process Costing

16 – 47

Solution 166 (10–14 min.)

Ex. 167

Watts Company adds materials at the beginning of the process and conversion costs are incurred

uniformly throughout the process.

Instructions

Complete the following calculation of equivalent units for materials and conversion costs.

Equivalent Units

Physical Units Materials Conversion Costs

Completed and transferred out 40,000

Ending work in process

Materials

Conversion costs, 75% complete 9,000

Total units

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 48

Ex. 168

The general ledger of Oates Company has the following work in process account.

WORK IN PROCESS—FINISHING

6/1 Balance 8,000 6/30 Transferred out ?

6/30 Materials 1,800

6/30 Labor 3,800

6/30 Overhead 2,800

6/30 Balance ?

Production records show that there were 2,000 units in beginning inventory, 50% complete; 6,000

units started, and 4,500 units transferred out. The beginning work in process had conversion

costs of $3,300. The units in ending inventory were 60% complete. Materials are added at the

beginning of the process.

Instructions

Answer the following questions.

(a) How many units are in process at June 30?

(b) What is the unit conversion cost for June?

(c) What is the conversion cost in the June 30 inventory?

Ex. 169

The Assembly Department uses a process cost accounting system and a weighted-average cost

flow assumption. The department adds materials at the beginning of the process and incurs

conversion costs uniformly throughout the process. During July, $190,000 of materials costs and

$135,500 in conversion costs were charged to the department. The beginning work in process

inventory was $93,000 on July 1, comprised of $80,000 of materials costs and $13,000 of

conversion costs.

Other data for the month of July are as follows:

Beginning work in process inventory, 7/1 25,000 units (40% complete)

Units completed and transferred out 90,000 units

Ending work in process inventory, 7/31 30,000 units (30% complete)

Process Costing

16 – 49

Ex. 169 (Cont.)

Instructions

Answer the following questions and show computations to support your answers.

1. How many physical units have to be accounted for in July?

2. What are the equivalent units of production for materials and for conversion costs for the

month of July?

3. What is the total cost assigned to the 90,000 units that were transferred out of the process in

July?

4. What is the total cost of the July 31 inventory?

Ex. 170

The Finishing Department of Edwards Company has the following production and cost data for

July:

1. Transferred out, 4,000 units.

2. Started 2,000 units that are 40% completed at July 31.

3. Materials added, $30,000; conversion costs incurred, $19,200.

Materials are entered at the beginning of the process. Conversion costs are incurred uniformly

during the process.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 50

Ex. 170 (Cont.)

Instructions

(a) Compute the equivalent units of production for materials and conversion costs for the month

of July.

(b) Compute unit costs and prepare a cost reconciliation schedule.

Ex. 171

Massey Corporation uses a process cost system and the weighted-average cost flow assumption.

Production begins in the Fabricating Department where materials are added at the beginning of

the process and conversion costs are incurred uniformly throughout the process. On March 1, the

beginning work in process inventory consisted of 20,000 units which were 60% complete and had

a cost of $175,000, $145,000 of which were materials costs. During March, the following

occurred:

Materials added $305,000

Conversion costs incurred $120,000

Units completed and transferred out in March 65,000

Units in ending work in process March 31 (40% complete) 25,000

Instructions

Answer the following questions and show the computations that support your answers.

1. What are the equivalent units of production for materials and conversion costs in the

Fabricating Department for the month of March?

2. What are the costs assigned to the ending work in process inventory on March 31?

3. What are the costs assigned to units completed and transferred out during March?

Process Costing

16 – 51

Solution 171 (15–20 min.)

Ex. 172

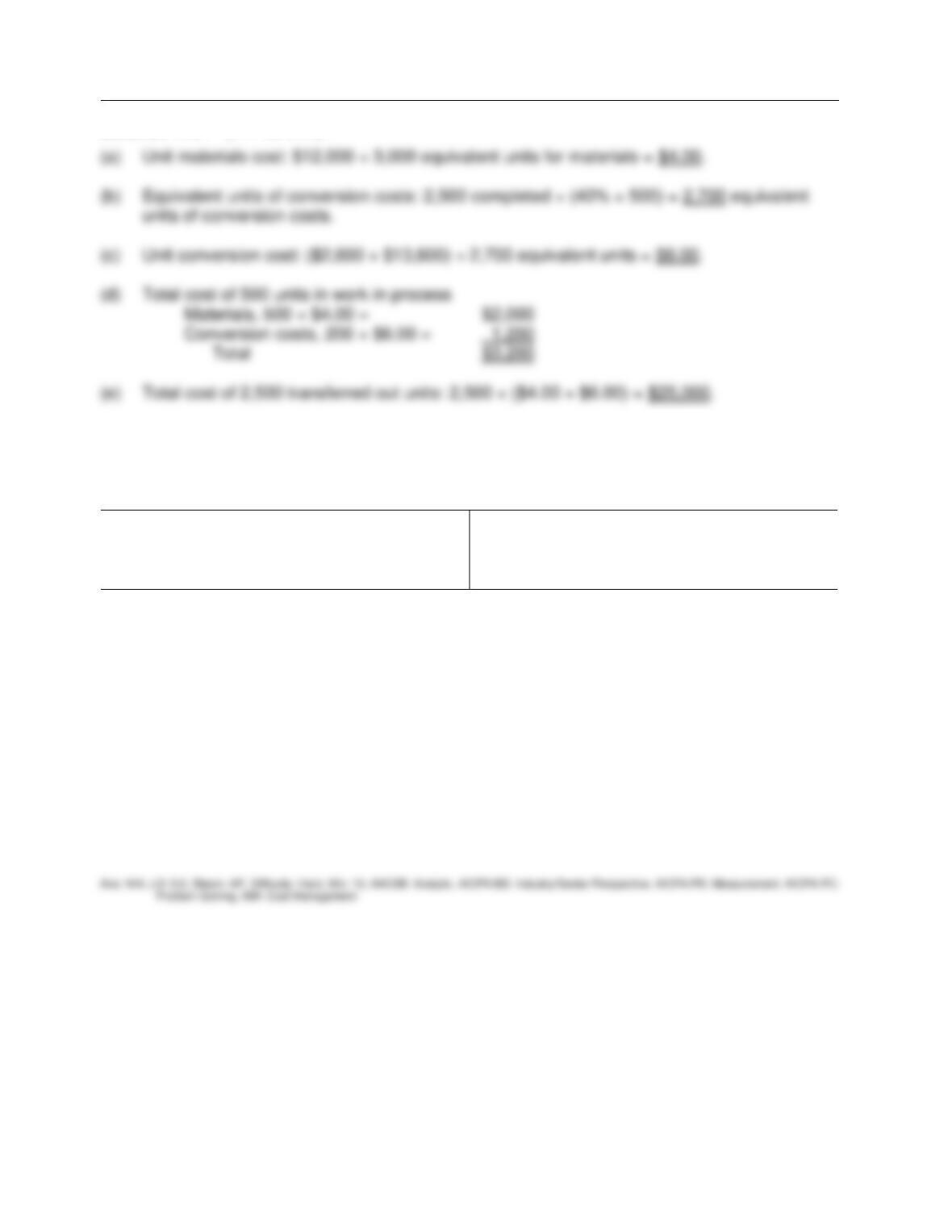

Given below are the production data for Department No. 1 for the first month of operation:

Costs charged to Department 1:

Materials $12,000

Labor 2,600

Overhead 13,600

During this first month of operations, 3,000 units were started into production; 2,500 units were

transferred out; and the remaining 500 units are 100% completed with respect to materials and

40% complete with respect to conversion costs.

Instructions

Compute the following:

(a) Unit materials cost.

(b) Equivalent units of conversion costs.

(c) Unit conversion cost.

(d) Total cost of 500 units in process at end of month.

(e) Total cost of 2,500 units transferred out.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 52

Solution 172 (14–18 min.)

Ex. 173

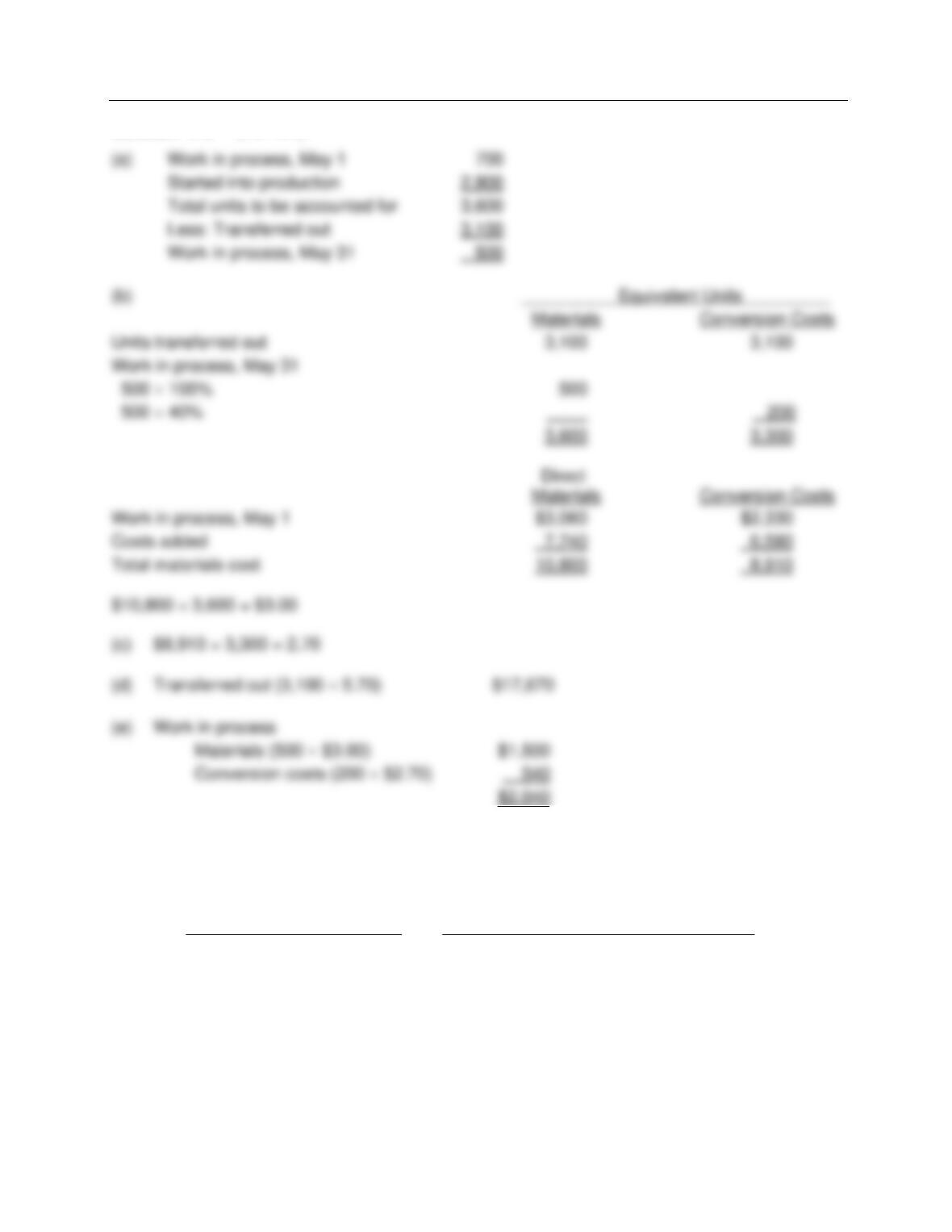

The ledger of Kinsler Company has the following work in process account.

Work in Process—Painting

5/1

5/31

5/31

5/31

Balance

Materials

Labor

Overhead

5,390

7,740

4,110

2,470

5/31

Transferred out

?

5/31

Balance

?

Production records show that there were 700 units in the beginning inventory, 30% complete,

2,900 units started, and 3,100 units transferred. The beginning work in process had materials

cost of $3,060 and conversion costs of $2,330. The units in ending inventory were 40% complete.

Materials are entered at the beginning of the painting process.

Instructions

(a) How many units are in process at May 31?

(b) What is the unit materials cost for May?

(c) What is the unit conversion cost for May?

(d) What is the total cost of units transferred out in May?

(e) What is the cost of the May 31 inventory?

Process Costing

16 – 53

Solution 173 (10 min.)

Ex. 174

The Cutting Department of Sanderson Company has the following production and cost data for

July.

Production

Costs

1. Transferred out 10,000

units

2. Started 5,000 units that

are 60% complete as

to conversion costs

and 100% complete as

to materials at July 31.

Beginning work in process

Materials

Labor

Manufacturing overhead

$ -0-

60,000

21,600

25,200

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

16 – 54

Ex. 174 (Cont.)

Materials are entered at the beginning of the process. Conversion costs are incurred uniformly

during the process.

Instructions

(a) Determine the equivalent units of production for (1) materials and (2) conversion costs.

(b) Compute unit costs and prepare a cost reconciliation schedule.

Ex. 175

Wilkinson Company has gathered the following information.

Units in beginning work in process -0-

Units started into production 60,000

Units in ending work in process 10,000

Percent complete for conversion costs in

ending work in process 40%

Costs incurred:

Direct materials $ 81,000

Direct labor $ 99,000

Overhead $130,500

Instructions

(a) Compute equivalent units of production for materials and for conversion costs.

(b) Determine the unit costs of production.

(c) Show the assignment of costs to units transferred out and in process.

Process Costing

16 – 55

Solution 175 (8 min.)

Ex. 176

Carlton Company has gathered the following information

Units in beginning work in process 25,000

Units started into production 115,000

Units in ending work in process 30,000

Percent complete for conversion costs in

ending work in process 60%

Costs incurred:

Direct materials $161,000

Direct labor $235,400

Overhead $180,600

Instructions

(a) Compute equivalent units of production for materials and for conversion costs.

(b) Determine the unit costs of production.

(c) Show the assignment of costs to units transferred out and in process.