31. Your company doesn’t face any taxes and has $500 million in assets, currently financed

entirely with equity. Equity is worth $40 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities as shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the

standard deviation in EPS if they switch to the proposed capital structure?

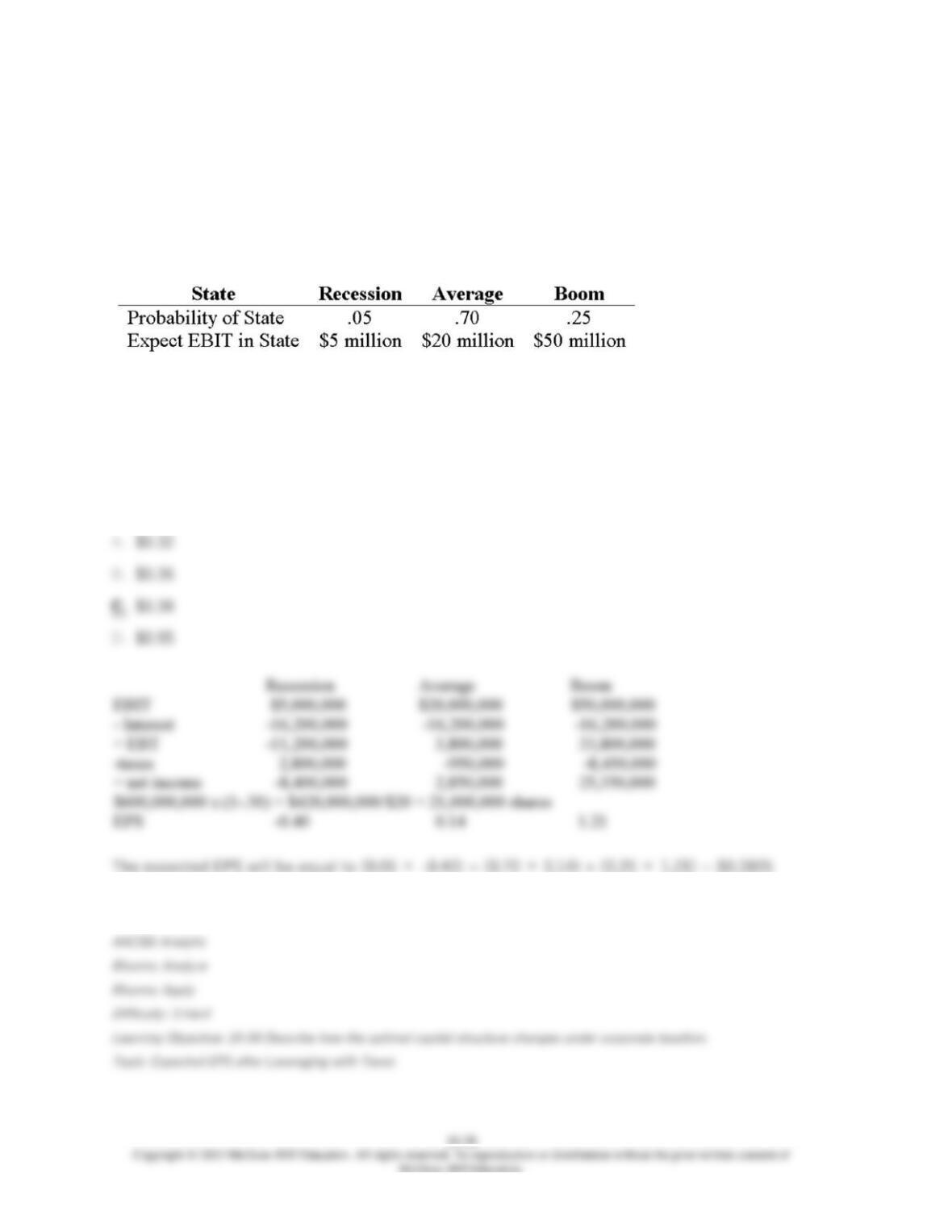

32. Your company doesn’t face any taxes and has $200 million in assets, currently financed

entirely with equity. Equity is worth $25 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 40 percent debt capital structure, and has determined that

they would have to pay a 7 percent yield on perpetual debt in either event. What will be the

standard deviation in EPS if they switch to the proposed capital structure?

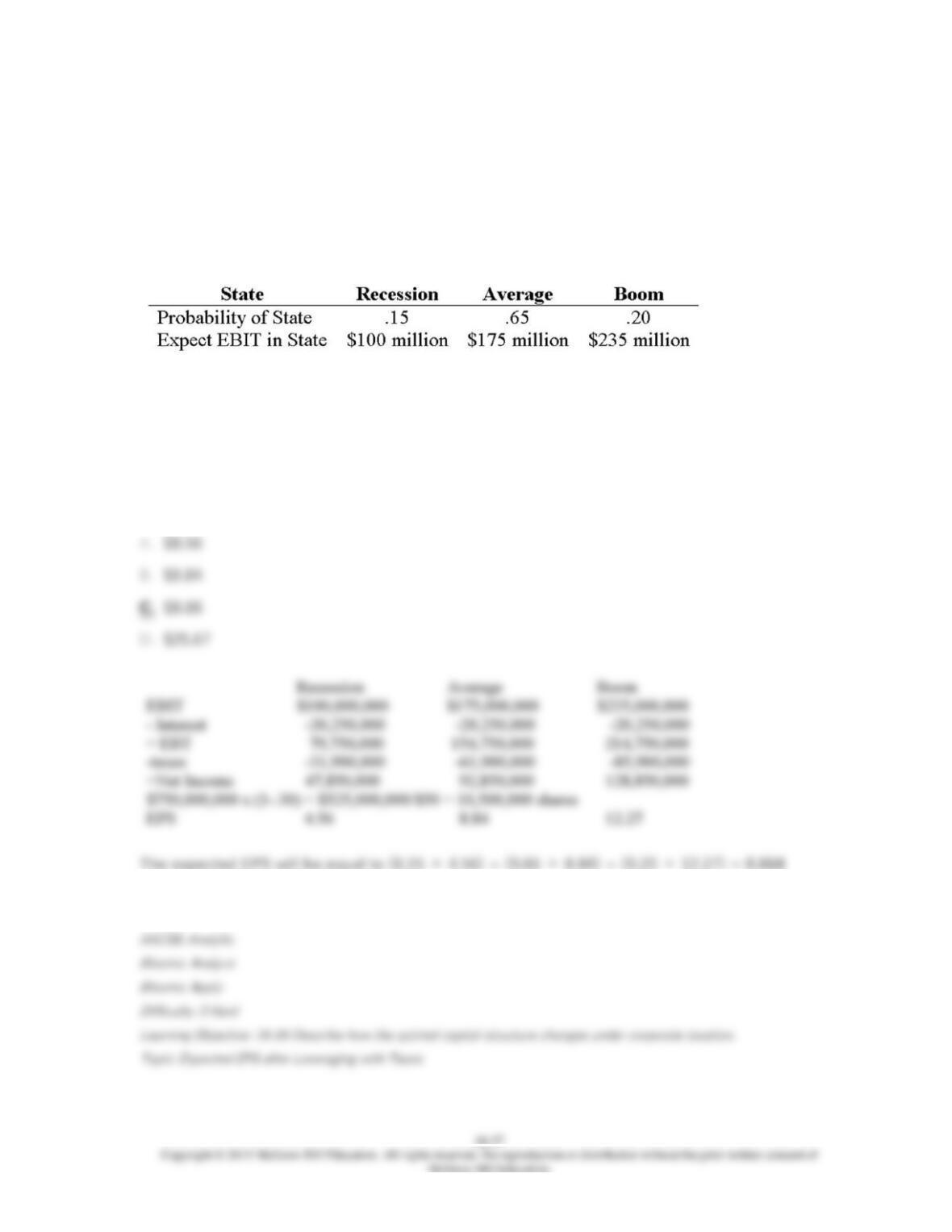

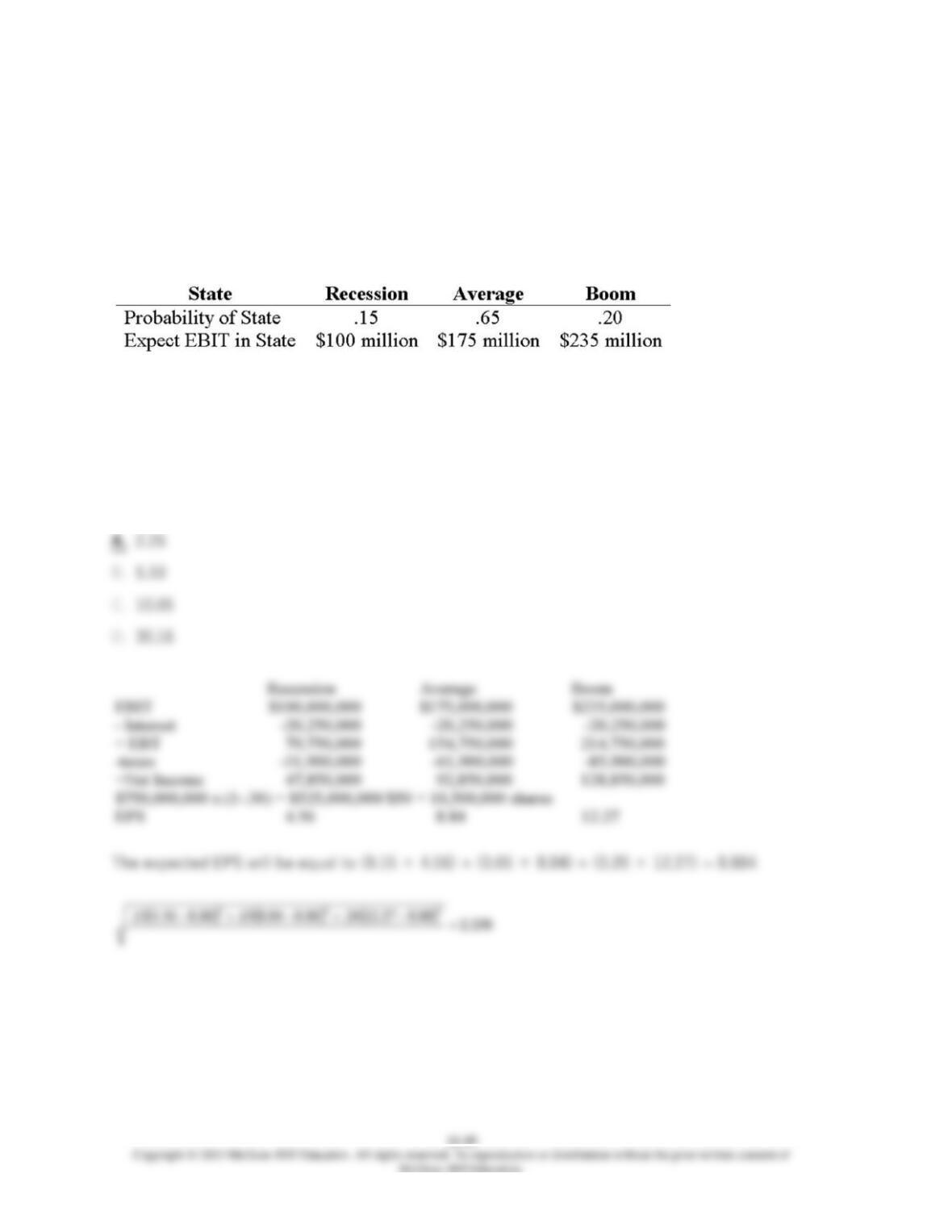

33. Your company doesn’t face any taxes and has $750 million in assets, currently financed

entirely with equity. Equity is worth $50 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the

standard deviation in EPS if they switch to the proposed capital structure?

34. Your company doesn’t face any taxes and has $800 million in assets, currently financed

entirely with equity. Equity is worth $60 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 20 percent debt capital structure, and has determined that

they would have to pay a 10 percent yield on perpetual debt in either event. What will be the

standard deviation in EPS if they switch to the proposed capital structure?

35. Your company doesn’t face any taxes and has $250 million in assets, currently financed

entirely with equity. Equity is worth $8 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 20 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

36. Your company doesn’t face any taxes and has $300 million in assets, currently financed

entirely with equity. Equity is worth $15 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 10 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

37. Your company doesn’t face any taxes and has $750 million in assets, currently financed

entirely with equity. Equity is worth $25 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 25 percent debt capital structure, and has determined that

they would have to pay a 10 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

38. Your company doesn’t face any taxes and has $200 million in assets, currently financed

entirely with equity. Equity is worth $10 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities as shown below:

The firm is considering switching to a 40 percent debt capital structure, and has determined that

they would have to pay an 8 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

39. Your company doesn’t face any taxes and has $750 million in assets, currently financed

entirely with equity. Equity is worth $25 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 25 percent debt capital structure, and has determined that

they would have to pay a 10 percent yield on perpetual debt in either event. What will be the

break-even level of EBIT?

40. Your company doesn’t face any taxes and has $300 million in assets, currently financed

entirely with equity. Equity is worth $10 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the

break-even EBIT?

41. Your company doesn’t face any taxes and has $200 million in assets, currently financed

entirely with equity. Equity is worth $10 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 40 percent debt capital structure, and has determined that

they would have to pay an 8 percent yield on perpetual debt in either event. What will be the

break-even EBIT?

42. Your company doesn’t face any taxes and has $150 million in assets, currently financed

entirely with equity. Equity is worth $8 per share, and book value of equity is equal to market

value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon which

state of the economy occurs this year, with the possible values of EBIT and their associated

probabilities shown as follows:

The firm is considering switching to a 25 percent debt capital structure, and has determined that

they would have to pay a 12 percent yield on perpetual debt in either event. What will be the

break-even EBIT?

43. Your company has a 40 percent tax rate and has $750 million in assets, currently

financed entirely with equity. Equity is worth $50 per share, and book value of equity is equal to

market value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon

which state of the economy occurs this year, with the possible values of EBIT and their

associated probabilities shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

44. Your company has a 25 percent tax rate and has $600 million in assets, currently

financed entirely with equity. Equity is worth $20 per share, and book value of equity is equal to

market value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon

which state of the economy occurs this year, with the possible values of EBIT and their

associated probabilities shown as follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

45. Your company has a 38 percent tax rate and has $800 million in assets, currently

financed entirely with equity. Equity is worth $60 per share, and book value of equity is equal to

market value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon

which state of the economy occurs this year, with the possible values of EBIT and their

associated probabilities shown as follows:

The firm is considering switching to a 20 percent debt capital structure, and has determined that

they would have to pay a 10 percent yield on perpetual debt in either event. What will be the level

of expected EPS if they switch to the proposed capital structure?

46. Your company has a 40 percent tax rate and has $750 million in assets, currently

financed entirely with equity. Equity is worth $50 per share, and book value of equity is equal to

market value of equity. Also, let’s assume that the firm’s expected values for EBIT depend upon

which state of the economy occurs this year, with the possible values of EBIT and their

associated probabilities shown follows:

The firm is considering switching to a 30 percent debt capital structure, and has determined that

they would have to pay a 9 percent yield on perpetual debt in either event. What will be the

standard deviation in EPS if they switch to the proposed capital structure?