Job Order Costing

15 – 21

101. For Wilton Company, the predetermined overhead rate is 70% of direct labor cost. During

the month, $360,000 of factory labor costs are incurred of which $100,000 is indirect

labor. Actual overhead incurred was $180,000. The amount of overhead debited to Work

in Process Inventory should be:

a. $182,000

b. $180,000

c. $252,000

d. $260,000

102. At the beginning of the year, Monroe Company estimates annual overhead costs to be

$1,600,000 and that 300,000 machine hours will be operated. Using machine hours as a

base, the amount of overhead applied during the year if actual machine hours for the year

was 315,000 hours is

a. $1,600,000.

b. $1,523,809.

c. $1,120,000.

d. $1,680,000.

103. Cost of goods sold is obtained from

a. analysis of all the control accounts in the cost system.

b. the finished goods inventory records.

c. the work in process inventory records.

d. the Raw Materials Inventory control account.

104. When determining costs of jobs, how does a company account for indirect materials?

a. It is added to work in process as used.

b. It remains part of raw materials inventory.

c. It is transferred out of raw materials into manufacturing overhead when used.

d. It is transferred out of raw materials into work in process as used.

105. In a job order cost system, a credit to Manufacturing Overhead will be accompanied by a

debit to

a. Cost of Goods Manufactured.

b. Finished Goods Inventory.

c. Work in Process Inventory.

d. Raw Materials Inventory.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 22

106. During 2013, Tanner Manufacturing expected Job No. 26 to cost $300,000 of overhead,

$500,000 of materials, and $200,000 in labor. Tanner applied overhead based on direct

labor cost. Actual production required an overhead cost of $280,000, $550,000 in

materials used, and $210,000 in labor. All of the goods were completed. What amount

was transferred to Finished Goods?

a. $1,000,000

b. $1,040,000

c. $1,060,000

d. $1,075,000

107. Debits to Work in Process Inventory are accompanied by a credit to all but which one of

the following accounts?

a. Raw Materials Inventory

b. Factory Labor

c. Manufacturing Overhead

d. Cost of Goods Sold

108. Which of the following is not viewed as part of accumulating manufacturing costs in a job

order cost system?

a. Cost of goods sold is recognized

b. Raw materials are purchased

c. Factory labor is incurred

d. Manufacturing overhead is incurred

109. Which of the following is not viewed as part of assigning manufacturing costs in a job

order cost system?

a. Manufacturing overhead is applied

b. Raw materials are used

c. Manufacturing overhead is incurred

d. Completed goods are recognized

110. In determining total manufacturing costs on the cost of goods manufactured schedule,

a. beginning work in process inventory should have a zero balance.

b. actual manufacturing overhead costs appear as a deduction.

c. manufacturing overhead applied is added to direct materials and direct labor.

d. ending work in process inventory is deducted from beginning work in process

inventory.

Job Order Costing

15 – 23

111. Gulick Company developed the following data for the current year:

Beginning work in process inventory $160,000

Direct materials used 96,000

Actual overhead 192,000

Overhead applied 144,000

Cost of goods manufactured 176,000

Total manufacturing costs 480,000

Gulick Company’s direct labor cost for the year is

a. $48,000.

b. $240,000.

c. $144,000.

d. $192,000.

112. Gulick Company developed the following data for the current year:

Beginning work in process inventory $160,000

Direct materials used 96,000

Actual overhead 192,000

Overhead applied 144,000

Cost of goods manufactured 176,000

Total manufacturing costs 480,000

Gulick Company’s ending work in process inventory is

a. $464,000.

b. $320,000.

c. $304,000.

d. $144,000.

113. Hayward Manufacturing Company developed the following data:

Beginning work in process inventory $450,000

Direct materials used 350,000

Actual overhead 550,000

Overhead applied 400,000

Cost of goods manufactured 600,000

Ending work in process 750,000

Hayward Manufacturing Company’s total manufacturing costs for the period is

a. $950,000.

b. $900,000.

c. $650,000.

d. cannot be determined from the data provided.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 24

114. Which of the following is not used in assigning manufacturing costs to work in process

inventory?

a. Actual manufacturing overhead

b. Time tickets

c. Materials requisitions

d. Predetermined overhead rate

115. On the cost of goods manufactured schedule, the cost of goods manufactured agrees with

the

a. balance of Finished Goods Inventory at the end of the period.

b. total debits to Work in Process Inventory during the period.

c. amount transferred from Work in Process Inventory to Finished Goods during the

period.

d. debits to Cost of Goods Sold during the period.

116. Gannon Company had the following information at December 31:

Finished goods inventory, January 1 $ 50,000

Finished goods inventory, December 31 150,000

If the cost of goods manufactured during the year amounted to $2,100,000 and annual

sales were $2,750,000, the amount of gross profit for the year is

a. $650,000.

b. $2,000,000.

c. $750,000.

d. $550,000.

117. Haight Company incurred direct materials costs of $1,500,000 during the year. Manu–

facturing overhead applied was $270,000 and is applied at the rate of 60% of direct labor

costs. Haight Company’s total manufacturing costs for the year was

a. $2,220,000.

b. $1,932,000.

c. $1,770,000.

d. $2,832,000.

Job Order Costing

15 – 25

118. Greer Company developed the following data for the current year:

Beginning work in process inventory $ 102,000

Direct materials used 156,000

Actual overhead 132,000

Overhead applied 138,000

Cost of goods manufactured 675,000

Total manufacturing costs 642,000

How much is Greer Company’s direct labor cost for the year?

a. $381,000

b. $450,000

c. $348,000

d. $246,000

119. Greer Company developed the following data for the current year:

Beginning work in process inventory $ 102,000

Direct materials used 156,000

Actual overhead 132,000

Overhead applied 138,000

Cost of goods manufactured 675,000

Total manufacturing costs 642,000

How much is Greer Company’s ending work in process inventory for the year?

a. $69,000

b. $363,000

c. $63,000

d. $279,000

120. Chmelar Manufacturing Company developed the following data:

Beginning work in process inventory $ 80,000

Direct materials used 480,000

Actual overhead 560,000

Overhead applied 540,000

Cost of goods manufactured 1,280,000

Ending work in process 60,000

How much are total manufacturing costs for the period?

a. $1,580,000

b. $1,260,000

c. $1,100,000

d. $1,220,000

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 26

121. Barger Company had the following information at December 31:

Finished goods inventory, January 1 $ 90,000

Finished goods inventory, December 31 126,000

If the cost of goods manufactured during the year amounted to $1,995,000 and annual

sales were $2,994,000, how much is the amount of gross profit for the year?

a. $999,000

b. $909,000

c. $1,959,000

d. $1,035,000

Solution: $2,994,000 − ($90,000 + $1,995,000 − $126,000) = $1,035,000

122. Emley Company incurred direct materials costs of $600,000 during the year.

Manufacturing overhead applied was $560,000 and is applied based on direct labor costs.

The predetermined overhead rate is 70%. How much are Emley Company’s total

manufacturing costs for the year?

a. $1,552,000

b. $1,400,000

c. $1,160,000

d. $1,960,000

123. During 2013, Durham Manufacturing expected Job No. 51 to cost $300,000 of overhead,

$500,000 of materials, and $200,000 in labor. Durham applied overhead based on direct

labor cost. Actual production required overhead cost of $290,000, $550,000 in materials

used, and $220,000 in labor. All of the goods were completed. What amount was

transferred to Finished Goods?

a. $1,070,000

b. $1,100,000

c. $1,000,000

d. $1,060,000

124. During 2013, Cotte Manufacturing expected Job No. 59 to cost $300,000 of overhead,

$500,000 of materials, and $200,000 in labor. Cotte applied overhead based on direct

labor cost. Actual production required an overhead cost of $290,000, $550,000 in

materials used, and $220,000 in labor. All of the goods were completed. How much is the

amount of over- or underapplied overhead?

a. $10,000 underapplied

b. $10,000 overapplied

c. $40,000 underapplied

d. $40,000 overapplied

Job Order Costing

15 – 27

125. Kimble Company applies overhead on the basis of machine hours. Given the following

data, compute overhead applied and the under– or overapplication of overhead for the

period:

Estimated annual overhead cost $1,600,000

Actual annual overhead cost $1,540,000

Estimated machine hours 400,000

Actual machine hours 380,000

a. $1,520,000 applied and $20,000 overapplied

b. $1,600,000 applied and $20,000 overapplied

c. $1,520,000 applied and $20,000 underapplied

d. $1,463,000 applied and neither under– nor overapplied

126. Barnes Company applies overhead on the basis of machine hours. Given the following

data, compute overhead applied and the under– or overapplication of overhead for the

period:

Estimated annual overhead cost $3,000,000

Actual annual overhead cost $2,940,000

Estimated machine hours 300,000

Actual machine hours 290,000

a. $2,900,000 applied and $40,000 overapplied

b. $3,000,000 applied and $40,000 overapplied

c. $2,900,000 applied and $40,000 underapplied

d. $2,940,000 applied and neither under– nor overapplied

127. A company assigned overhead to work in process. At year end, what does the amount of

overapplied overhead mean?

a. The overhead assigned to work in process is greater than the estimated overhead

costs.

b. The overhead assigned to work in process is less than the estimated overhead costs.

c. The overhead assigned to work in process is less than the actual overhead.

d. The overhead assigned to work in process is greater than the overhead incurred.

128. If the Manufacturing Overhead account has a debit balance at the end of a period, it

means that

a. actual overhead costs were less than overhead costs applied to jobs.

b. actual overhead costs were greater than overhead costs applied to jobs.

c. actual overhead costs were equal to overhead costs applied to jobs.

d. no jobs have been completed.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 28

129. If the manufacturing overhead costs applied to jobs worked on were greater than the

actual manufacturing costs incurred during a period, overhead is said to be

a. underapplied.

b. overapplied.

c. in error.

d. prepaid.

130. At the end of the year, any balance in the Manufacturing Overhead account is generally

eliminated by adjusting

a. Work In Process Inventory.

b. Finished Goods Inventory.

c. Cost of Goods Sold.

d. Raw Materials Inventory.

131. If Manufacturing Overhead has a credit balance at the end of the period, then

a. overhead has been underapplied.

b. the overhead assigned to Work in Process Inventory is less than the overhead incurred.

c. overhead has been overapplied.

d. management must take corrective action.

132. The Manufacturing Overhead account shows debits of $30,000, $24,000, and $28,000

and one credit for $86,000. Based on this information, manufacturing overhead

a. has been overapplied.

b. has been underapplied.

c. has not been applied.

d. shows a zero balance.

133. If Manufacturing Overhead has a debit balance at the end of the period, then

a. overhead has been underapplied.

b. the overhead assigned to Work in Process Inventory is more than the overhead

incurred.

c. overhead has been overapplied.

d. management must take corrective action.

134. If actual overhead is greater than applied manufacturing overhead, then manufacturing

overhead is:

a. underapplied.

b. overapplied.

c. a loss on the income statement under “Other Expenses and Losses.”

d. considered a miscellaneous expense.

Job Order Costing

15 – 29

135. If actual overhead is less than applied manufacturing overhead, then manufacturing

overhead is:

a. underapplied.

b. overapplied.

c. a loss on the income statement under “Other Expenses and Losses.”

d. considered a miscellaneous expense.

136. If manufacturing overhead has been underapplied during the year, the adjusting entry at

the end of the year will show a

a. debit to Manufacturing Overhead.

b. credit to Cost of Goods Sold.

c. debit to Work in Process Inventory.

d. debit to Cost of Goods Sold.

137. If manufacturing overhead has been overapplied during the year, the adjusting entry at the

end of the year will show a

a. debit to Manufacturing Overhead.

b. credit to Finished Goods Inventory

c. debit to Cost of Goods Sold.

d. credit to Work in Process Inventory.

138. The existence of under– or overapplied overhead at the end of the year:

a. requires an adjustment to Cost of Goods Sold.

b. indicates that an error has been made.

c. requires a retroactive adjustment to the cost of all jobs completed.

d. is written off as a bad estimate expense.

139. Conceptually, any under- or overapplied overhead at the end of the year should be

allocated among all of the following except

a. cost of goods sold.

b. ending work in process inventory.

c. ending raw materials inventory.

d. ending finished goods inventory.

140. If, at the end of the year, Manufacturing Overhead has been overapplied, it means that

a. actual overhead costs were greater than the overhead assigned to jobs.

b. actual overhead costs were less than the overhead assigned to jobs.

c. overhead has not been applied to jobs still in process.

d. cost of goods will have to be increased by the amount of the overapplied overhead.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 30

141. A process cost system would be used for all of the following except the

a. manufacture of cereal.

b. refining of petroleum.

c. printing of wedding invitations.

d. production of automobiles.

142. In a job order cost system, it would be correct in recording the purchase of raw materials

to debit

a. Work in Process Inventory.

b. Work in Process and Manufacturing Overhead.

c. Raw Materials Inventory.

d. Finished Goods Inventory.

143. In a manufacturing company, the cost of factory labor consists of all of the following

except

a. employer payroll taxes.

b. fringe benefits incurred by the employer.

c. net earnings of factory workers.

d. gross earnings of factory workers.

144. Which of the following is not a control account?

a. Raw Materials Inventory

b. Factory Labor

c. Manufacturing Overhead

d. All of these are control accounts.

145. When the company assigns factory labor costs to jobs, the direct labor cost is debited to

a. Direct Labor.

b. Factory Labor.

c. Manufacturing Overhead.

d. Work in Process Inventory.

146. Jinnah Company applies overhead on the basis of 200% of direct labor cost. Job No. 501

is charged with $180,000 of direct materials costs and $240,000 of manufacturing

overhead. The total manufacturing costs for Job No. 501 is

a. $420,000.

b. $660,000.

c. $540,000.

d. $600,000.

Job Order Costing

15 – 31

147. Companies assign manufacturing overhead to work in process on an estimated basis

through the use of a(n)

a. actual overhead rate.

b. estimated overhead rate.

c. assigned overhead rate.

d. predetermined overhead rate.

148. Overapplied manufacturing overhead exists when overhead assigned to work in process is

a. more than overhead incurred and there is a debit balance in Manufacturing Overhead

at the end of a period.

b. less than overhead incurred and there is a debit balance in Manufacturing Overhead

at the end of a period.

c. more than overhead incurred and there is a credit balance in Manufacturing Overhead

at the end of a period.

d. less than overhead incurred and there is a credit balance in Manufacturing Overhead

at the end of a period.

149. Usually, under- or overapplied overhead is considered to be an adjustment to

a. work in process.

b. finished goods.

c. finished goods and cost of goods sold.

d. cost of goods sold.

150. Which of the following statements about under- or overapplied manufacturing overhead is

correct?

a. After the entry to transfer over- or underapplied overhead to Cost of Goods Sold is

posted, Manufacturing Overhead will have a zero balance.

b. When Manufacturing Overhead has a credit balance, overhead is said to be under–

applied.

c. At the end of the year, under– or overapplied overhead is eliminated by a closing entry.

d. When annual financial statements are prepared, overapplied overhead is reported in

current liabilities.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 32

Answers to Multiple Choice Questions

BRIEF EXERCISES

BE 151

During the first year of operations, Shapiro Tool accumulated the following manufacturing costs:

Raw materials purchased on account $10,000

Factory labor accrued 6,000

Incurred manufacturing overhead on account 4,000

Instructions

Prepare separate journal entries for each manufacturing cost.

Job Order Costing

15 – 33

BE 152

In January, Harlan, Inc. production supervisor requisitioned raw materials for production as

follows: Job 1 $600, Job 2 $900, Job 3 $400, and general factory use, $520.

Instructions

Prepare a summary journal entry to record raw materials used.

BE 153

Lando Company reported the following amounts for 2013:

Raw materials purchased $88,000 Ending work in process inventory $ 6,300

Beginning raw materials inventory 5,200 Manufacturing overhead costs applied 36,000

Ending raw materials inventory 4,500 Beginning work in process inventory 6,100

Instructions

Calculate the cost of materials used in production

BE 154

Builder Bug Company allocates overhead at $9 per direct labor hour. Job A45 required 4 boxes of

direct materials at a cost of $30 per box and took employees 15 hours to complete. Employees

earn $15 per hour.

Instructions

Compute the total cost of Job A45.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 34

BE 155

Colby Company estimates that annual manufacturing overhead costs will be $600,000.

Estimated annual operating activity bases are: direct labor cost $460,000, direct labor hours

40,000 and machine hours 80,000. The actual manufacturing overhead cost for the year was

$601,000 and the actual direct labor cost for the year was $456,000. Actual direct labor hours

totaled 40,200 and machine hours totaled 79,000. Colby applies overhead based on direct labor

hours.

Instructions

Compute the predetermined overhead rate and determine the amount of manufacturing overhead

applied. Determine if overhead is over– or underapplied and the amount.

BE 156

Martin Company applies manufacturing overhead based on direct labor hours. Information

concerning manufacturing overhead and labor for the year follows:

Actual manufacturing overhead $150,000

Estimated manufacturing overhead $140,000

Direct labor hours incurred 4,800

Direct labor hours estimated 5,000

Instructions

Compute the predetermined overhead rate.

BE 157

The manufacturing operations of Bryant, Inc. had the following balances for the month of January:

Inventories January 1 January 31

Raw materials $12,000 $13,000

Work in process 21,000 23,000

Finished goods 14,000 16,000

Bryant transferred $270,000 of completed goods out of work in process during January.

Instructions

Compute the cost of goods sold.

Job Order Costing

15 – 35

Solution 157 (2 min.)

BE 158

The following amounts were reported by Burke Company before adjusting its immaterial

overapplied manufacturing overhead of $8,000.

Raw Materials Inventory $ 40,000

Finished Goods Inventory 60,000

Work in Process Inventory 100,000

Cost of Goods Sold 770,000

Instructions

Compute what amount Burke will report as cost of goods sold after it disposes of its overapplied

overhead.

BE 159

During 2013, Arb Company incurred the following direct labor costs: January $20,000 and

February $30,000. Arb uses a predetermined overhead rate of 120% of direct labor cost.

Estimated overhead for the 2 months, respectively, totaled $19,500 and $35,700. Actual overhead

for the 2 months, respectively, totaled $24,500 and $32,500.

Instructions

Determine if overhead is over– or underapplied for each of the two months and the respective

amounts.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 36

BE 160

At December 31, Ding Company reported the following balances in its accounts:

Cost of Goods Sold $210,000

Finished Goods Inventory 30,000

The company’s balance in its Manufacturing Overhead account at the same date was a debit of

$2,400.

Instructions

Prepare the entry to adjust the over– or underapplied overhead amount at December 31.

EXERCISES

Ex. 161

The manufacturing operations of Beatly, Inc. had the following balances for the month of January:

January 1 January 31

Raw materials $12,000 $13,000

Work in process 21,000 23,000

Finished goods 14,000 12,000

Beatly transferred $240,000 of completed goods out of work in process during January.

Instructions

Compute the cost of goods sold for January.

Ex. 162

A selected list of accounts used by Cline Manufacturing Company follows:

Code Code

A Cash F Accounts Payable

B Accounts Receivable G Factory Labor

C Raw Materials Inventory H Manufacturing Overhead

D Work In Process Inventory I Cost of Goods Sold

E Finished Goods Inventory J Sales Revenue

Cline Manufacturing Company uses a job order system and maintains perpetual inventory

records.

Job Order Costing

15 – 37

Ex. 162 (Cont.)

Instructions

Place the appropriate code letter in the columns indicating the appropriate account(s) to be

debited and credited for the transactions listed below.

———————————————————————————————————————————

Account(s) Account(s)

Transactions Debited Credited

———————————————————————————————————————————

1. Raw materials were purchased on account.

———————————————————————————————————————————

2. Issued a check to Dixon Machine Shop for

repair work on factory equipment.

———————————————————————————————————————————

3. Direct materials were requisitioned for Job 280.

———————————————————————————————————————————

4. Factory labor was paid as incurred.

———————————————————————————————————————————

5. Recognized direct labor and indirect labor used.

———————————————————————————————————————————

6. The production department requisitioned indirect

materials for use in the factory.

———————————————————————————————————————————

7. Overhead was applied to production based on a

predetermined overhead rate of $8 per labor hour.

———————————————————————————————————————————

8. Goods that were completed were transferred to

finished goods.

———————————————————————————————————————————

9. Goods costing $80,000 were sold for $105,000

on account.

———————————————————————————————————————————

10. Paid for raw materials purchased previously

on account.

———————————————————————————————————————————

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 38

Solution 162 (10–15 min.)

Ex. 163

Finn Manufacturing Company uses a job order cost accounting system and keeps perpetual

inventory records. Prepare journal entries to record the following transactions during the month of

June.

June 1 Purchased raw materials for $20,000 on account.

8 Raw materials requisitioned by production:

Direct materials $8,000

Indirect materials 1,000

15 Paid factory utilities, $2,100 and repairs for factory equipment, $8,000.

25 Incurred $96,000 of factory labor.

25 Time tickets indicated the following:

Direct Labor (6,000 hrs × $12 per hr) = $72,000

Indirect Labor (3,000 hrs × $8 per hr) = 24,000

$96,000

Job Order Costing

15 – 39

Ex. 163 (Cont.)

25 Applied manufacturing overhead to production based on a predetermined overhead

rate of $7 per direct labor hour worked.

28 Goods costing $18,000 were completed in the factory and were transferred to finished

goods.

30 Goods costing $15,000 were sold for $20,000 on account.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 40

Ex. 164

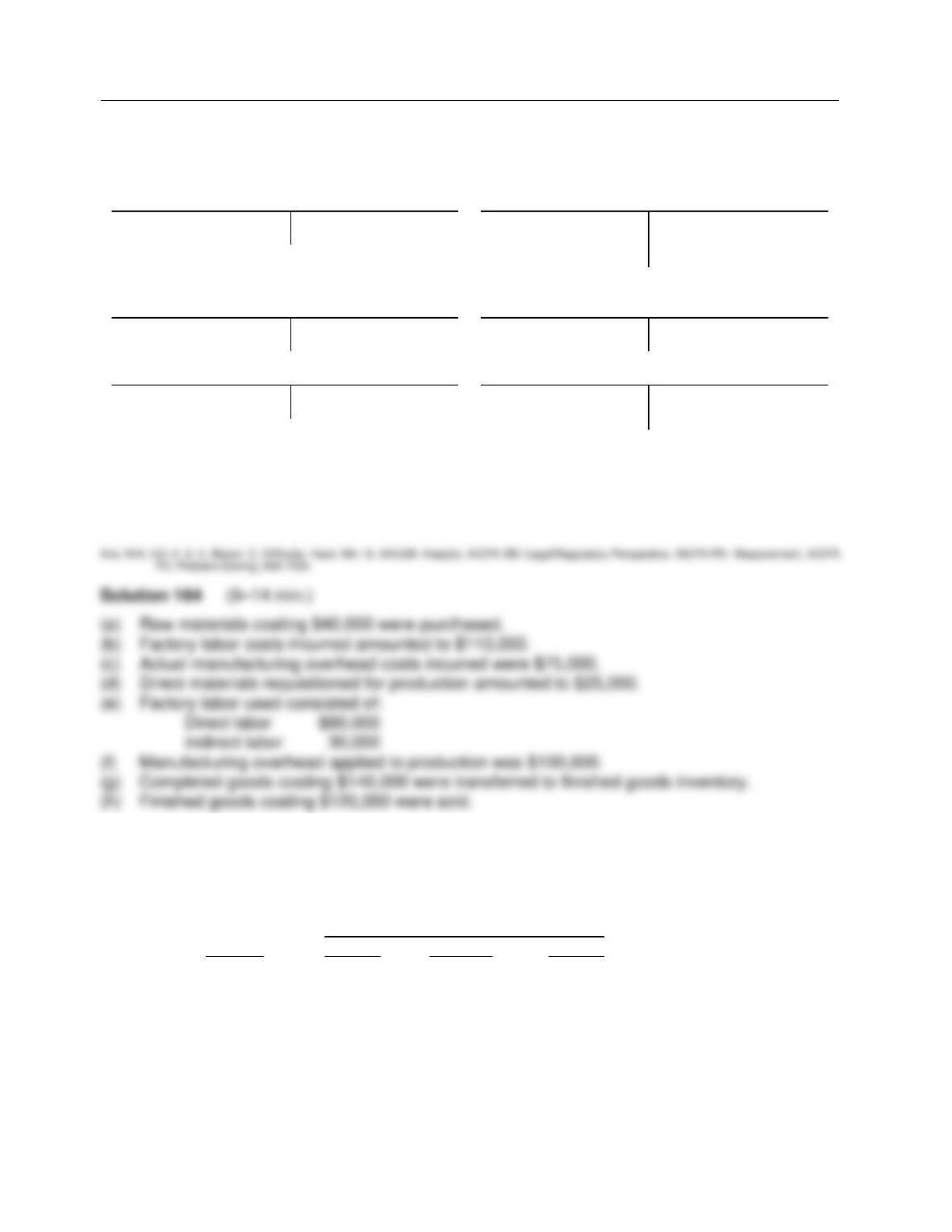

Selected accounts of Kosar Manufacturing Company at year end appear below:

RAW MATERIALS INVENTORY WORK IN PROCESS INVENTORY

(a) 40,000 (d) 25,000 (d) 25,000 (g) 140,000

(e) 80,000

(f) 100,000

FINISHED GOODS INVENTORY COST OF GOODS SOLD

(g) 140,000 (h) 120,000 (h) 120,000

FACTORY LABOR MANUFACTURING OVERHEAD

(b) 110,000 (e) 110,000 (c) 75,000 (f) 100,000

(e) 30,000

Instructions

Explain the probable transaction that took place for each of the items identified by letters in the

accounts. For example:

(a) Raw materials costing $40,000 were purchased.

Ex. 165

Sardin Company begins the month of March with $17,000 of work in process costs from Job 324.

Information from job cost sheets shows the following additional costs assigned during March,

April, and May of 2013:

Manufacturing Costs Assigned

Job No. March April May

324 $26,000

325 20,000 $28,000 $15,000

326 41,000 11,000

327 16,000 34,000

328 29,000 51,000

Job 324 was completed in March. Jobs 325 and 327 were completed in May, and Job 326 was

completed in April. Jobs are sold during the month after completion. Total revenue for jobs sold

during the 3-month period is $145,000.