Job Order Costing

15 – 41

Ex. 165 (Cont.)

Instructions

Calculate the balances of the work in process and finished goods inventory accounts at the end

of May.

Ex. 166

The gross earnings of factory workers for Dinkel Company during the month of January are

$400,000. The employer’s payroll taxes for the factory payroll are $48,000. Of the total

accumulated cost of factory labor, 75% is related to direct labor and 25% is attributable to indirect

labor.

Instructions

(a) Prepare the entry to record the factory labor costs for the month of January.

(b) Prepare the entry to assign factory labor to production.

(c) Prepare the entry to assign manufacturing overhead to production, assuming the

predetermined overhead rate is 125% of direct labor cost.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 42

Ex. 167

Foster Manufacturing uses a job order cost accounting system. On April 1, the company has

Work in Process Inventory of $7,600 and two jobs in process: Job No. 221, $3,600, and Job No.

222, $4,000. During April, a summary of source documents reveals the following:

For Materials Requisition Slips Labor Time Tickets

Job No. 221 $1,200 $1,600

222 1,700 2,200

223 2,400 2,900

224 2,600 2,800

General use 600 400

Totals $8,500 $9,900

Foster applies manufacturing overhead to jobs at an overhead rate of 60% of direct labor cost.

Job No. 221 is completed during the month.

Instructions

(a) Prepare summary journal entries to record the raw materials requisitioned, factory labor

used, the assignment of manufacturing overhead to jobs, and the completion of Job No. 221.

(b) Calculate the balance of the Work in Process Inventory account at April 30.

Job Order Costing

15 – 43

Ex. 168

Manufacturing cost data for Dolan Company, which uses a job order cost system, are presented

below:

Case A Case B

Direct Materials Used (a) $103,000

Direct Labor $ 70,000 160,000

Manufacturing Overhead Applied 63,000 (d)

Total Manufacturing Costs 220,000 (e)

Work in Process, 1/1/13 (b) 45,000

Total Cost of Work in Process 300,000 (f)

Work in Process, 12/31/13 (c) 40,000

Cost of Goods Manufactured 205,000 (g)

Instructions

Indicate the missing amount for each letter. Assume that overhead is applied on the basis of

direct labor cost and that the rate is the same for both cases.

Ex. 169

Fort Corporation had the following transactions during its first month of operations:

1. Purchased raw materials on account, $85,000.

2. Raw Materials of $30,000 were requisitioned to the factory. An analysis of the materials

requisition slips indicated that $6,000 was classified as indirect materials.

3. Factory labor costs incurred were $150,000 of which $120,000 pertained to factory wages

payable and $30,000 pertained to employer payroll taxes payable.

4. Time tickets indicated that $126,000 was direct labor and $24,000 was indirect labor.

5. Overhead costs incurred on account were $168,000.

6. Manufacturing overhead was applied at the rate of 150% of direct labor cost.

7. Goods costing $115,000 are still incomplete at the end of the month; the other goods were

completed and transferred to finished goods.

8. Finished goods costing $100,000 to manufacture were sold on account for $130,000.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 44

Ex. 169 (Cont.)

Instructions

Journalize the above transactions for Fort Corporation.

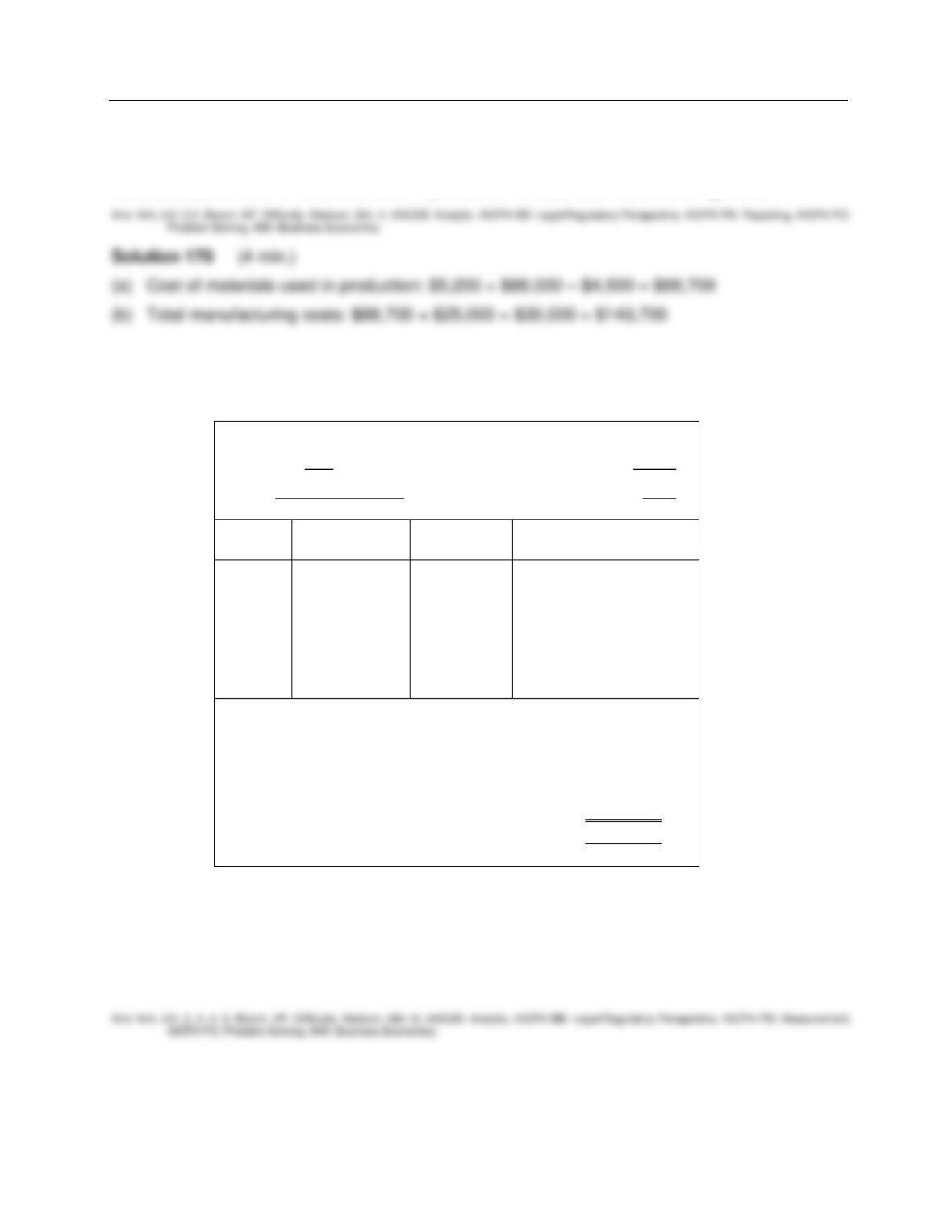

Ex. 170

Lando Company reported the following amounts for 2013:

Raw materials purchased $88,000

Beginning raw materials inventory 5,200

Ending raw materials inventory 4,500

Beginning finished goods inventory 7,600

Ending finished goods inventory 8,000

Direct labor used 25,000

Manufacturing overhead costs applied 30,000

Beginning work in process inventory 6,100

Ending work in process inventory 6,300

Job Order Costing

15 – 45

Ex. 170 (Cont.)

Instructions

Calculate (a) the cost of materials used in production and (b) total manufacturing costs.

Ex. 171

A job cost sheet of Fugate Company is given below.

Job Cost Sheet

JOB NO. 172 Quantity 1,500

FOR James Company Date Completed 5/31

Date

Direct

Materials

Direct

Labor

Manufacturing

Overhead

5/10

12

15

22

24

27

31

1,030

1,120

1,000

1,870

550

480

670

825

720

1,005

Cost of completed job:

Direct materials ________

Direct labor ________

Manufacturing Overhead ________

Total cost ________

Unit cost ________

Instructions

(a) Answer the following questions.

(1) What is the predetermined manufacturing overhead rate?

(2) What are the total cost and the unit cost of the completed job?

(b) Prepare the entry to record the completion of the job.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 46

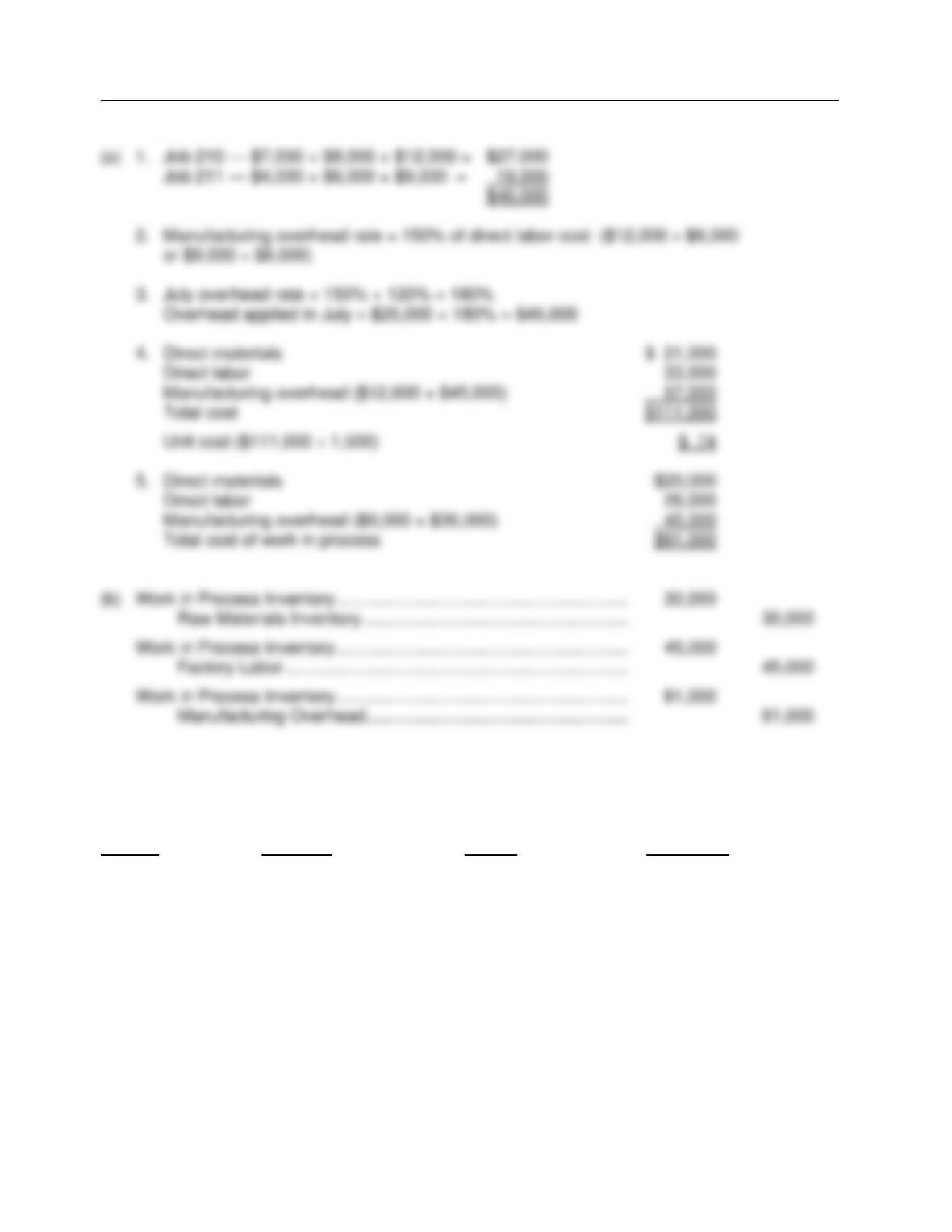

Solution 171 (8 min.)

Ex. 172

At May 31, 2013, the accounts of Kuhlmann Manufacturing Company show the following.

1. May 1 inventories—finished goods $12,600, work in process $14,700, and raw materials

$8,200.

2. May 31 inventories—finished goods $8,500, work in process $22,900, and raw materials

$7,100.

3. Debit postings to work in process were: direct materials $67,400, direct labor $50,000, and

manufacturing overhead applied $45,000.

4. Sales totaled $220,000.

Instructions

(a) Prepare a condensed cost of goods manufactured schedule.

(b) Prepare an income statement for May through gross profit.

Job Order Costing

15 – 47

Solution 172 (Cont.)

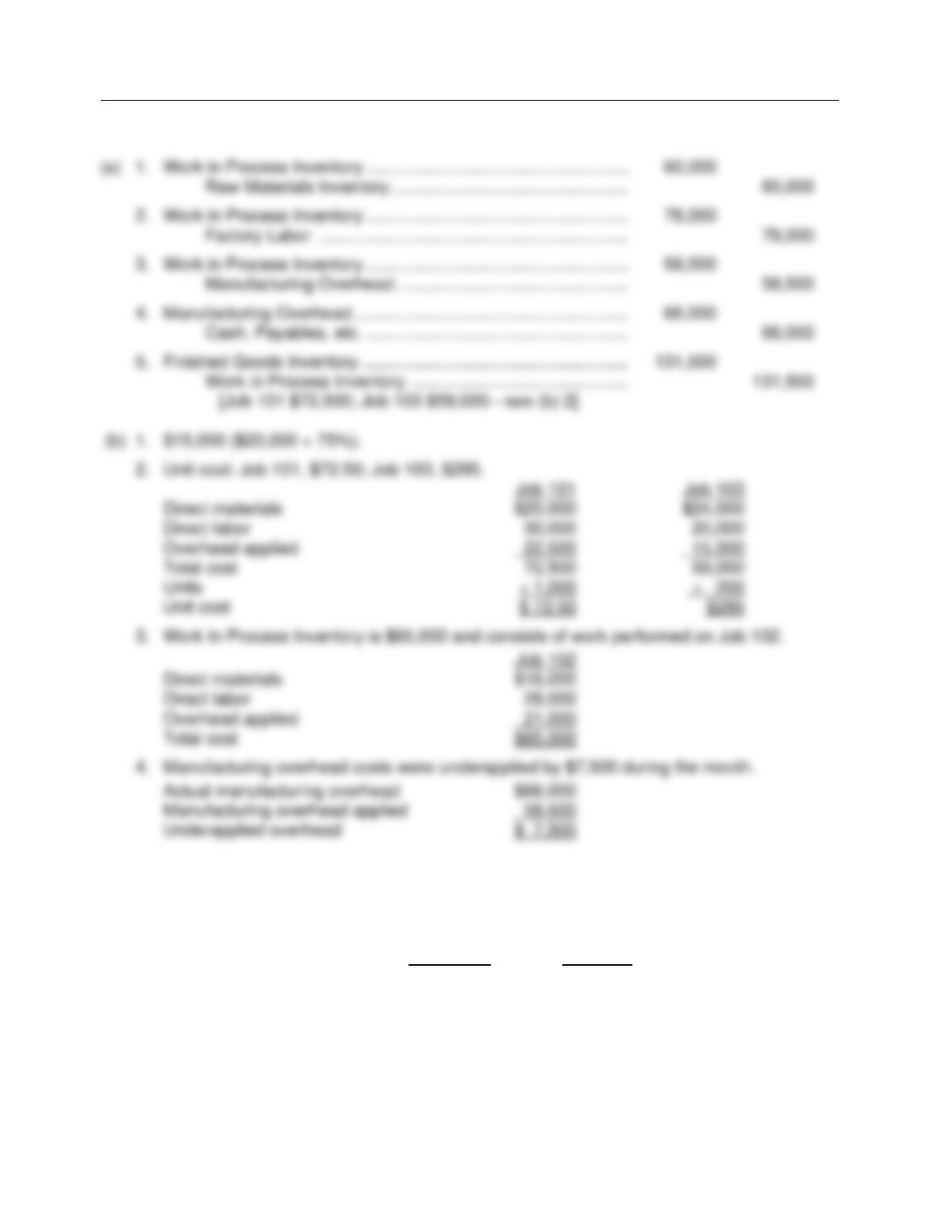

Ex. 173

Watson Manufacturing Company employs a job order cost accounting system and keeps

perpetual inventory records. The following transactions occurred in the first month of operations:

1. Direct materials requisitioned during the month:

Job 101 $20,000

Job 102 16,000

Job 103 24,000

$60,000

2. Direct labor incurred and charged to jobs during the month was:

Job 101 $30,000

Job 102 28,000

Job 103 20,000

$78,000

3. Manufacturing overhead was applied to jobs worked on using a predetermined overhead rate

based on 75% of direct labor costs.

4. Actual manufacturing overhead costs incurred during the month amounted to $66,000.

5. Job 101 consisting of 1,000 units and Job 103 consisting of 200 units were completed during

the month.

Instructions

(a) Prepare journal entries to record the above transactions.

(b) Answer the following questions:

1. How much manufacturing overhead was applied to Job 103 during the month?

2. Compute the unit cost of Jobs 101 and 103.

3. What is the balance in Work In Process Inventory at the end of the month?

4. Determine if manufacturing overhead was under- or overapplied during the month. How

much?

Ans: N/A, LO: 2, 3, 4, 5, 6, Bloom: AP, Difficulty: Medium, Min: 15, AACSB: Analytic, AICPA BB: Legal/Regulatory Perspective, AICPA FN: Measurement,

AICPA PC: Problem Solving, IMA: FSA

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 48

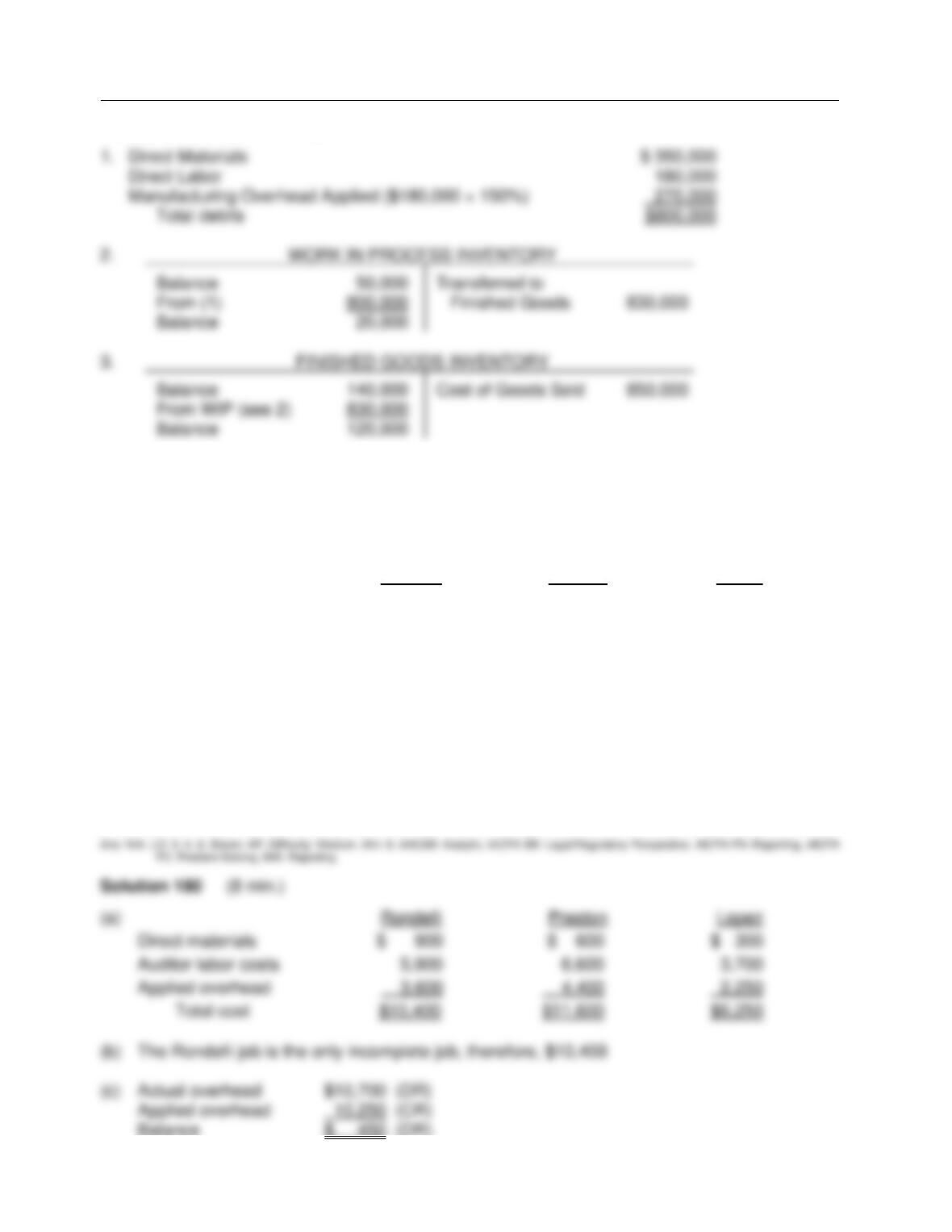

Solution 173 (15–20 min.)

Ex. 174

Graham Manufacturing is a small manufacturer that uses machine-hours as its activity base for

assigned overhead costs to jobs. The company estimated the following amounts for 2013 for the

company and for Job 62:

Company Job 62

Direct materials $60,000 $4,500

Direct labor $25,000 $2,500

Manufacturing overhead costs $72,000

Machine hours 80,000 1,350

During 2013, the actual machine-hours totaled 84,000, and actual overhead costs were $71,000.

Job Order Costing

15 – 49

Ex. 174 (Cont.)

Instructions

(a) Compute the predetermined overhead rate.

(b) Compute the total manufacturing costs for Job 62.

(c) How much overhead is over or underapplied for the year for the company? State amount and

whether it is over- or underapplied.

(d) If Graham Manufacturing sells Job 62 for $14,000, compute the gross profit.

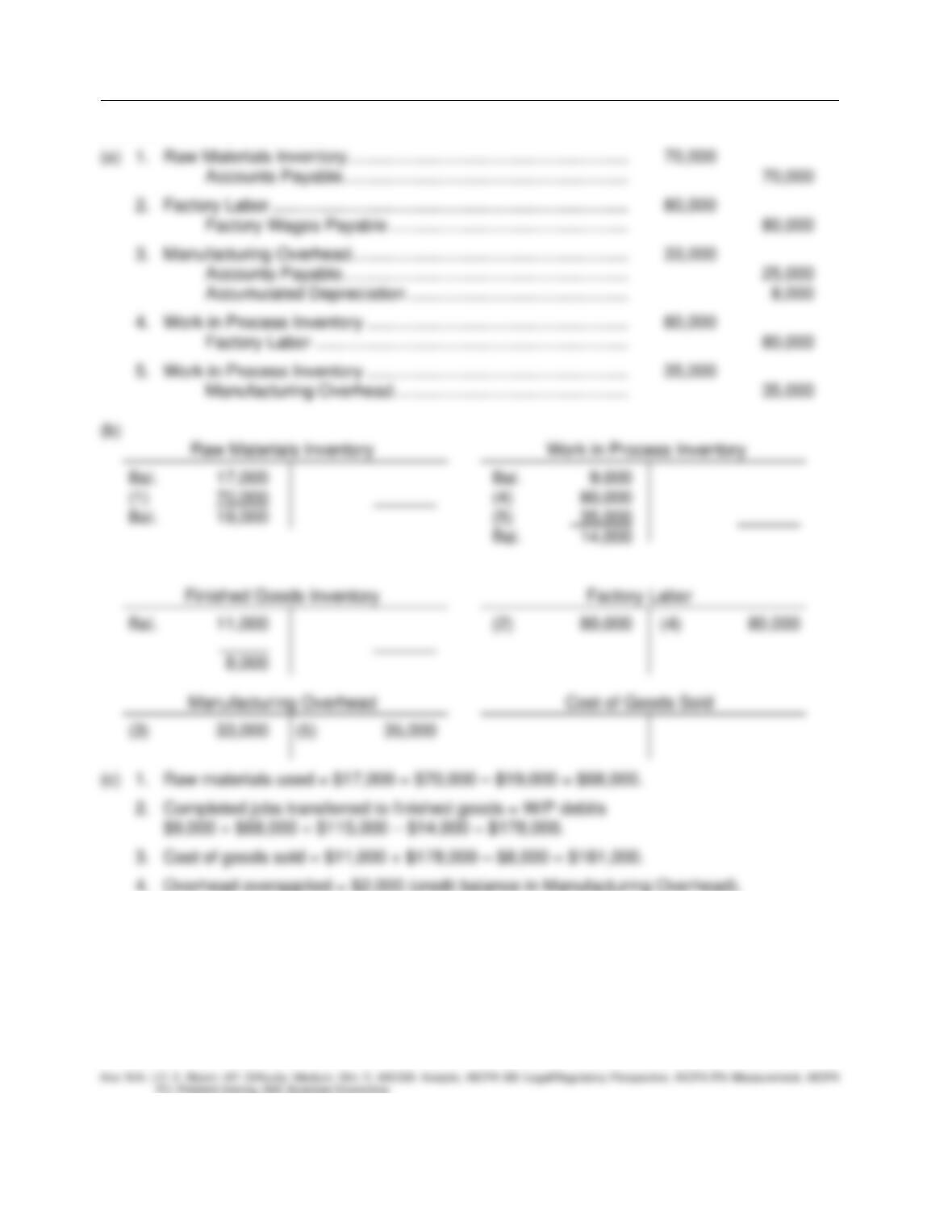

Ex. 175

The following inventory information is available for Ricci Manufacturing Corporation for the year

ended December 31, 2013:

Beginning Ending

Inventories:

Raw materials $17,000 $19,000

Work in process 9,000 14,000

Finished goods 11,000 8,000

Total $37,000 $41,000

In addition, the following transactions occurred in 2013:

1. Raw materials purchased on account, $70,000.

2. Incurred factory labor, $80,000, all is direct labor. (Credit Factory Wages Payable).

3. Incurred the following overhead costs during the year: Utilities $6,800, Depreciation on

manufacturing machinery $8,000, Manufacturing machinery repairs $9,200, Factory insurance

$9,000 (Credit Accounts Payable and Accumulated Depreciation).

4. Assigned $80,000 of factory labor to jobs.

5. Applied $35,000 of overhead to jobs.

Instructions

(a) Journalize the above transactions.

(b) Reproduce the manufacturing cost and inventory accounts. Use T-accounts.

(c) From an analysis of the accounts, compute the following:

1. Raw materials used.

2. Completed jobs transferred to finished goods.

3. Cost of goods sold.

4. Under- or overapplied overhead.

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 50

Solution 175 (16–22 min.)

4. Overhead overapplied = $2,000 (credit balance in Manufacturing Overhead).

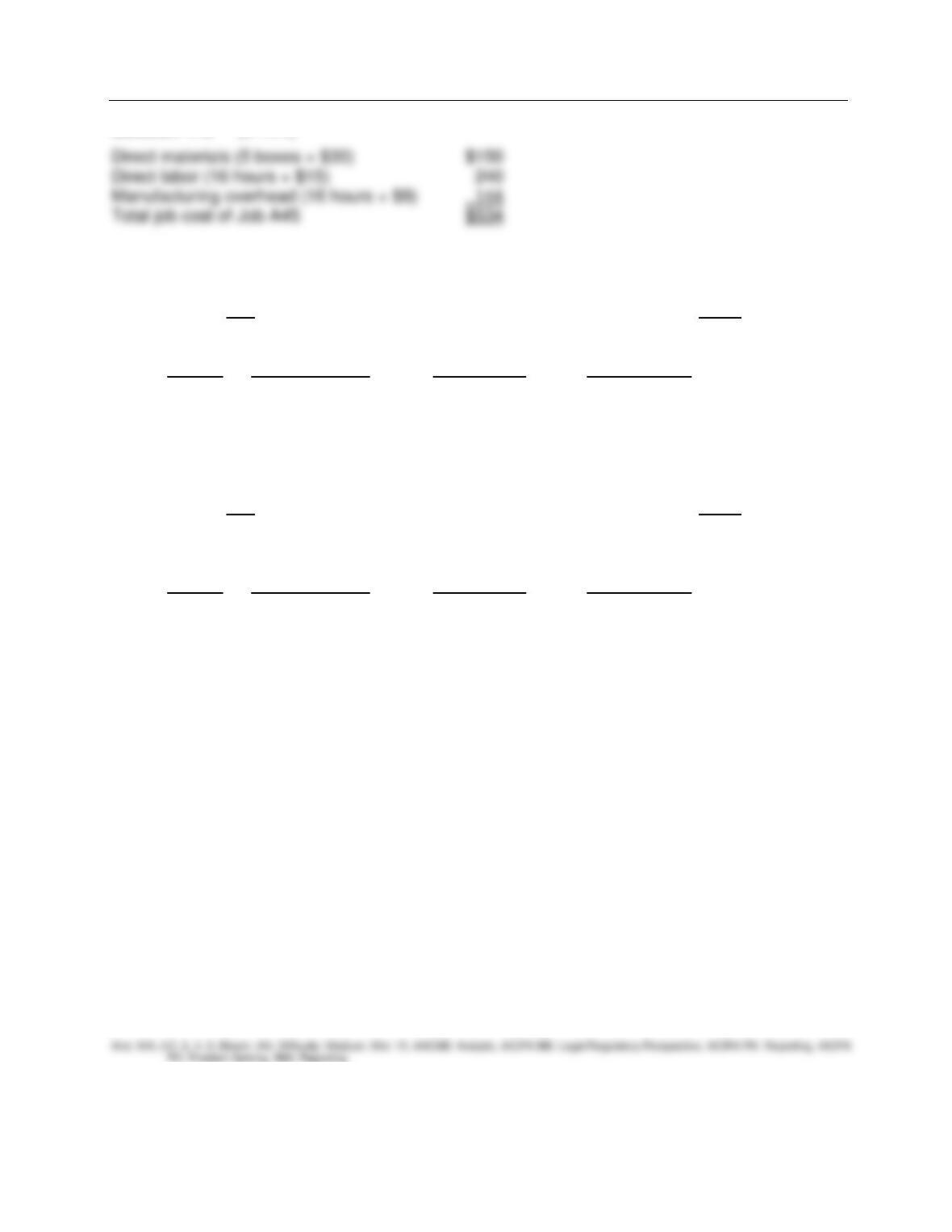

Ex. 176

Builder Bug Company allocates manufacturing overhead at $9 per direct labor hour. Job A45

required 5 boxes of direct materials at a cost of $30 per box and took employees 16 hours to

complete. Employees earn $15 per hour.

Instructions

Compute the total cost of Job A45.

Job Order Costing

15 – 51

Solution 176 (5 min.)

Ex. 177

Job cost sheets for Howard Manufacturing are as follows:

Job No 210 Quantity 1,500

Manufacturing

Date Direct Materials Direct Labor Overhead

July 1 7,000 8,000 12,000

8 8,500

10 10,000

15 5,500

25 15,000

Job No 211 Quantity 1,200

Manufacturing

Date Direct Materials Direct Labor Overhead

July 1 4,000 6,000 9,000

10 9,000

15 8,000

20 7,000

27 12,000

Instructions

(a) Answer the following questions.

1. What was the balance in Work in Process Inventory on July 1 if these were the only

unfinished jobs?

2. What was the predetermined overhead rate in June if overhead was applied on the basis

of direct labor cost?

3. If July is the start of a new fiscal year and the overhead rate is 20% higher than in the

preceding year, how much overhead should be applied to Job 210 in July?

4. Assuming Job 210 is complete, what is the total and unit cost of the job?

5. Assuming Job 211 is the only unfinished job at July 31, what is the balance in Work in

Process Inventory on this date?

(b) Journalize the summary entries to record the assignment of costs to the jobs in July.

(Note: Make one entry in total for each manufacturing cost element.)

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 52

Solution 177 (15–20 min.)

Ex. 178

Garner Company begins operations on July 1, 2013. Information from job cost sheets shows the

following:

Manufacturing Costs Assigned

Job No. July August September

100 $12,000 $8,800

101 8,800 9,700 $12,000

102 5,000

103 11,800 6,000

104 5,800 7,000

Job 102 was completed in July. Job 100 was completed in August, and Jobs 101 and 103 were

completed in September. Each job was sold for 80% above its cost in the month following

completion.

Job Order Costing

15 – 53

Ex. 178 (Cont.)

Instructions

(a) Compute the balance in Work in Process Inventory at the end of July.

(b) Compute the balance in Finished Goods Inventory at the end of September.

(c) Compute the gross profit for August.

Ex. 179

The accounting records of Roland Manufacturing Company include the following information:

Dec. 31 Jan. 1

Work in process inventory $ 20,000 $ 50,000

Finished goods inventory 120,000 140,000

Direct materials used 350,000

Direct labor 180,000

Selling expenses 125,000

Manufacturing overhead is applied at a rate of 150% of direct labor cost.

Instructions

Answer the following questions:

1. What is the total of the debits to Work in Process Inventory during the year?

2. What is the amount transferred to Finished Goods Inventory during the year?

3. What is the cost of goods sold?

Test Bank for Accounting, Tools for Business Decision Making Fifth Edition

15 – 54

Solution 179 (10–14 min.)

Ex. 180

Grant Marwick and Associates, a CPA firm, uses job order costing to capture the costs of its audit

jobs. There were no audit jobs in process at the beginning of November. Listed below are data

concerning the three audit jobs conducted during November.

Rondelli Preston Lopez

Direct materials $900 $600 $300

Auditor labor costs $5,900 $6,600 $3,700

Auditor hours 72 88 45

Overhead costs are applied to jobs on the basis of auditor hours, and the predetermined

overhead rate is $50 per auditor hour. The Rondelli job is the only incomplete job at the end of

November. Actual overhead for the month was $10,700.

Instructions

(a) Determine the cost of each job.

(b) Indicate the balance of the Work in Process account at the end of November.

(c) Calculate the ending balance of the Manufacturing Overhead account for November.