Chapter 14: Real Options

DIFFICULTY:

Difficulty: Easy

QUESTION TYPE:

True / False

True / False

1. Real options exist when managers have the opportunity, after a project has been implemented, to make operating

changes in response to changed conditions that modify the project’s cash flows.

a.

True

b.

False

ANSWER:

True

POINTS:

1

DIFFICULTY:

Difficulty: Easy

QUESTION TYPE:

True / False

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.01 – LO: 14-1

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Real options

KEYWORDS:

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

2. Real options are options to buy real assets, like stocks, rather than interest-bearing assets, like bonds.

a.

True

b.

False

ANSWER:

False

POINTS:

1

DIFFICULTY:

Difficulty: Easy

QUESTION TYPE:

True / False

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.01 – LO: 14-1

NATIONAL STANDARDS:

United States – BUSPROG: Reflective Thinking

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Real options

KEYWORDS:

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

3. The option to abandon a project is a real option, but a call option on a stock is not a real option.

a.

True

b.

False

ANSWER:

True

Chapter 14: Real Options

HAS VARIABLES:

False

IFMG.DAVE.19.14.01 – LO: 14-1

NATIONAL STANDARDS:

United States – BUSPROG: Reflective Thinking

STATE STANDARDS:

United States – ak – DISC: Capital structure

United States – OH – Default City – TBA

TOPICS:

Real options

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

1

DIFFICULTY:

Difficulty: Easy

True / False

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.02 – LO: 14-2

United States – BUSPROG: Reflective Thinking

STATE STANDARDS:

United States – ak – DISC: Capital structure

United States – OH – Default City – TBA

TOPICS:

Real options

KEYWORDS:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

4. Real options are most valuable when the underlying source of risk is very low.

a.

True

b.

False

ANSWER:

False

POINTS:

1

Difficulty: Easy

QUESTION TYPE:

True / False

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.02 – LO: 14-2

NATIONAL STANDARDS:

United States – BUSPROG: Reflective Thinking

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Real options

KEYWORDS:

DATE CREATED:

10/30/2017 8:09 PM

1/6/2018 7:14 PM

5. Real options affect the size, but not the risk, of a project’s expected cash flows.

a.

True

b.

False

ANSWER:

False

Chapter 14: Real Options

Multiple Choice

POINTS:

1

Difficulty: Easy

QUESTION TYPE:

Multiple Choice

6. Which of the following is NOT a real option?

a.

The option to buy shares of stock if its price goes up.

b.

The option to expand into a new geographic region.

c.

The option to abandon a project.

d.

The option to switch the type of fuel used in an industrial furnace.

e.

The option to expand production if the product is successful.

ANSWER:

a

1

DIFFICULTY:

Difficulty: Moderate

QUESTION TYPE:

Multiple Choice

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.01 – LO: 14-1

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Real options

KEYWORDS:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

7. Whether to invest in a project today or to postpone the decision until next year is a decision facing the CEO of the

Aaron Co. The project has a positive expected NPV, but its cash flows could be less than expected, in which case the NPV

could be negative. No competitors are likely to invest in a similar project if Aaron decides to wait. Which of the following

statements best describes the issues that Aaron faces when considering this investment timing option?

a.

The more uncertainty about the future cash flows, the more logical it is for Aaron to go ahead with this project

today.

b.

Since the project has a positive expected NPV today, this means that its expected NPV will be even higher if it

chooses to wait a year.

c.

Since the project has a positive expected NPV today, this means that it should be accepted in order to lock in

that NPV.

d.

Waiting would probably reduce the project’s risk.

e.

The investment timing option does not affect the cash flows and will therefore have no impact on the project’s

risk.

ANSWER:

d

Chapter 14: Real Options

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.02 – LO: 14-2

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Investment timing option

KEYWORDS:

OTHER:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

POINTS:

1

DIFFICULTY:

Difficulty: Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

8. Which of the following will NOT increase the value of a real option?

a.

An increase in the volatility of the underlying source of risk.

b.

An increase in the risk-free rate.

c.

An increase in the cost of obtaining the real option.

d.

A decrease in the probability that a competitor will enter the market of the project in question.

e.

Lengthening the time in which a real option must be exercised.

ANSWER:

c

POINTS:

1

DIFFICULTY:

Difficulty: Moderate

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.02 – LO: 14-2

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Real options

KEYWORDS:

OTHER:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

9. Which of the following is most CORRECT?

a.

Real options change the risk, but not the size, of projects’ expected cash flows.

b.

Real options are likely to reduce the cost of capital that should be used to discount a project’s expected cash

flows.

c.

Very few projects actually have real options.

d.

Real options are less valuable when there is a lot of uncertainty about the true values future sales and costs.

e.

Real options change the size, but not the risk, of projects’ expected cash flows.

ANSWER:

b

Chapter 14: Real Options

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.02 – LO: 14-2

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Real options

KEYWORDS:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

Copyright Cengage Learning. Powered by Cognero.

Page 5

10. Which one of the following is an example of a “flexibility” option?

a.

A company has an option to close down an operation if it turns out to be unprofitable.

b.

A company agrees to pay more to build a plant in order to be able to change the plant’s inputs and/or outputs at

a later date if conditions change.

c.

A company invests in a project today to gain knowledge that may enable it to expand into different markets at

a later date.

d.

A company invests in a jet aircraft so that its CEO, who must travel frequently, can arrive for distant meetings

feeling less tired than if he had to fly commercial.

e.

A company has an option to invest in a project today or to wait a year.

ANSWER:

b

DIFFICULTY:

Difficulty: Easy

QUESTION TYPE:

Multiple Choice

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.04 – LO: 14-4

United States – BUSPROG: Analytic

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Real options

KEYWORDS:

TYPE: Multiple Choice: Conceptual

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

11. Ashgate Enterprises uses the NPV method for selecting projects, and it does a reasonably good job of estimating

projects’ sales and costs. However, it never considers real options that might be associated with projects. Which of the

following statements is most likely to describe its situation?

a.

Its estimated capital budget is probably too large due to its failure to consider abandonment and growth

options.

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 6

b.

Failing to consider abandonment and flexibility options probably makes the optimal capital budget too large,

but failing to consider growth and timing options probably makes the optimal capital budget too small, so it is

unclear what impact not considering real options has on the overall capital budget.

c.

Failing to consider abandonment and flexibility options probably makes the optimal capital budget too small,

but failing to consider growth and timing options probably makes the optimal capital budget too large, so it is

unclear what impact not considering real options has on the overall capital budget.

d.

Real options should not have any effect on the size of the optimal capital budget.

e.

Its estimated capital budget is probably too small, because projects’ NPVs are often larger when real options

are taken into account.

Difficulty: Moderate

Multiple Choice

False

IFMG.DAVE.19.14.04 – LO: 14-4

United States – BUSPROG: Analytic

United States – ak – DISC: Capital structure

United States – OH – Default City – TBA

Real options

TYPE: Multiple Choice: Conceptual

10/30/2017 8:09 PM

1/6/2018 7:14 PM

Drilling Experts, Inc.

Drilling Experts, Inc. (DEI) finds and develops oil properties and then sells the successful ones to major oil refining

companies. DEI is now considering a new potential field, and its geologists have developed the following data, in

thousands of dollars.

t = 0.

A $400 feasibility study would be conducted at t = 0. The results of this study would

determine if the company should commence drilling operations or make no further

investment and abandon the project.

t = 1.

If the feasibility study indicates good potential, the firm would spend $1,000 at t = 1

to drill exploratory wells. The best estimate is that there is an 80% probability that the

exploratory wells would indicate good potential and thus that further work would be

done, and a 20% probability that the outlook would look bad and the project would be

abandoned.

t = 2.

If the exploratory wells test positive, DEI would go ahead and spend $10,000 to

obtain an accurate estimate of the amount of oil in the field at t = 2. The best estimate

now is that there is a 60% probability that the results would be very good and a 40%

probability that results would be poor and the field would be abandoned.

t = 3.

If the full drilling program is carried out, there is a 50% probability of finding a lot of

oil and receiving a $25,000 cash inflow at t = 3, and a 50% probability of finding less

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 7

oil and then only receiving a $10,000 inflow.

12. Refer to the data for Drilling Experts, Incorporated. Since the project is considered to be quite risky, a 20% cost of

capital is used. What is the project’s expected NPV, in thousands of dollars?

a.

$336.15

b.

$373.50

c.

$415.00

d.

$461.11

e.

$507.22

ANSWER:

d

NPV-1 =

NPV-2 =

NPV-3 =

NPV-4 =

= 0.2.

POINTS:

1

Difficulty: Moderate

QUESTION TYPE:

Multiple Choice

False

PREFACE NAME:

Drilling Experts, Inc.

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Decision tree: expected NPV

KEYWORDS:

TYPE: Multiple Choice: Problem

NOTES:

The problems referring to Drilling Experts, Inc., MUST be kept together.

1/6/2018 7:14 PM

13. Refer to the data for Drilling Experts. Calculate the project’s coefficient of variation. (Hint: Use the expected NPV.)

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 8

a.

5.87

b.

6.52

c.

7.25

d.

7.97

e.

8.77

Prob.

0.24

0.24

0.32

0.20

1.00

1

Difficulty: Moderate

Multiple Choice

False

Drilling Experts, Inc.

IFMG.DAVE.19.14.03 – LO: 14-3

United States – BUSPROG: Analytic

United States – ak – DISC: Capital structure

United States – OH – Default City – TBA

Decision tree: SD and CV

TYPE: Multiple Choice: Problem

The problems referring to the preface for Drilling Experts MUST be kept together.

10/30/2017 8:09 PM

1/6/2018 7:14 PM

Nationwide Pharmaceutical Corporation

A project with an up-front cost at t = 0 of $1500 is being considered by Nationwide Pharmaceutical Corporation (NPC).

(All dollars in this problem are in thousands.) The project’s subsequent cash flows are critically dependent on whether a

competitor’s product is approved by the Food and Drug Administration. If the FDA rejects the competitive product, NPC’s

product will have high sales and cash flows, but if the competitive product is approved, that will negatively impact NPC.

There is a 75% chance that the competitive product will be rejected, in which case NPC’s expected cash flows will be

$500 at the end of each of the next seven years (t = 1 to 7). There is a 25% chance that the competitor’s product will be

approved, in which case the expected cash flows will be only $25 at the end of each of the next seven years (t = 1 to 7).

NPC will know for sure one year from today whether the competitor’s product has been approved.

NPC is considering whether to make the investment today or to wait a year to find out about the FDA’s decision. If it

waits a year, the project’s up-front cost at t = 1 will remain at $1,500, the subsequent cash flows will remain at $500 per

year if the competitor’s product is rejected and $25 per year if the alternative product is approved. However, if NPC

decides to wait, the subsequent cash flows will be received only for six years (t = 2 … 7).

14. Refer to the data for Nationwide Pharmaceutical Corporation (NPC). Assuming that all cash flows are discounted at

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 9

10%, if NPC chooses to wait a year before proceeding, how much will this increase or decrease the project’s expected

NPV in today’s dollars (i.e., at t = 0), relative to the NPV if it proceeds today?

a.

$77.23

b.

$85.81

c.

$95.34

d.

$105.94

e.

$116.53

ANSWER:

d

POINTS:

1

QUESTION TYPE:

Multiple Choice

HAS VARIABLES:

False

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.03 – LO: 14-3

STATE STANDARDS:

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

KEYWORDS:

kept together.

DATE MODIFIED:

1/6/2018 7:14 PM

15. Refer to the data for Nationwide Pharmaceutical Corporation (NPC). Calculate the effect of waiting on the project’s

risk, using the same data. By how much will delaying reduce the project’s coefficient of variation? (Hint: Use the expected

NPV.)

a.

2.23

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 10

b.

2.46

c.

2.70

d.

2.97

e.

3.27

Prob.

0.75

0.25

1.00

Prob.

0.75

0.25

1.00

1

Difficulty: Moderate

False

IFMG.DAVE.19.14.03 – LO: 14-3

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

kept together.

1/6/2018 7:14 PM

Garner-Wagner Incorporated

The executives of Garner-Wagner Inc. are considering a project that has an up-front cost of $3 million and is expected to

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 11

produce a cash flow of $500,000 at the end of each of the next 5 years. The project‘s cost of capital is 10%.

16. Refer to the data for Garner-Wagner Incorporated. Based on the above data, what is the project’s net present value?

a.

−$1,312,456

b.

−$1,104,607

c.

−$875,203

d.

$105,999

e.

$321,788

ANSWER:

b

POINTS:

1

Difficulty: Easy

Multiple Choice

HAS VARIABLES:

False

Garner-Wagner Incorporated

LEARNING OBJECTIVES:

IFMG.DAVE.19.14.03 – LO: 14-3

United States – BUSPROG: Analytic

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

Project NPV–nonalgorithmic

KEYWORDS:

TYPE: Multiple Choice: Multi-part

together.

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

17. Refer to the data for Garner-Wagner Incorporated. If Garner-Wagner goes ahead with this project today, it will obtain

knowledge that will give rise to additional opportunities 5 years from now (at t = 5). The company can decide at t = 5

whether or not it wants to pursue these additional opportunities. Based on the best information available today, there is a

35% probability that the outlook will be favorable, in which case the future investment opportunity will have a net present

value of $6 million at t = 5. There is a 65% probability that the outlook will be unfavorable, in which case the future

investment opportunity will have a net present value of −$6 million at t = 5. Garner-Wagner does not have to decide today

whether it wants to pursue the additional opportunity. Instead, it can wait to see what the outlook is. However, the

company cannot pursue the future opportunity unless it makes the $3 million investment today. What is the estimated net

present value of the project, after consideration of the potential future opportunity?

a.

−$1,104,607

b.

−$875,203

c.

$199,328

d.

$561,947

e.

$898,205

ANSWER:

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 12

Enter the following data inputs in the financial calculator:

N = 5; I/YR = 10; PMT = 0; FV = 2,100,000; and then solve for PV = $1,303,935.

Difficulty: Moderate

Multiple Choice

Garner-Wagner Incorporated

United States – BUSPROG: Analytic

United States – ak – DISC: Capital structure

Growth option–nonalgorithmic

TYPE: Multiple Choice: Multi-part

10/30/2017 8:09 PM

Steppingstone Incorporated

The Z−90 project being considered by Steppingstone Incorporated (SI) has an up-front cost of $250,000. The project’s

subsequent cash flows are critically dependent on whether another of its products, Z−45, becomes an industry standard.

There is a 50% chance that the Z−45 will become the industry standard, in which case the Z−90’s expected cash flows will

be $110,000 at the end of each of the next 5 years. There is a 50% chance that the Z−45 will not become the industry

standard, in which case the Z−90’s expected cash flows will be $25,000 at the end of each of the next 5 years. Assume that

the cost of capital is 12%.

18. Refer to data for Steppingstone Incorporated. Based on the above information, what is the Z−90’s expected net present

value?

Chapter 14: Real Options

a.

−$6,678

b.

−$3,251

c.

$15,303

d.

$20,004

e.

$45,965

ANSWER:

a

Step 1:

Find the project’s expected cash flows in Years 1 through 5:

(0.5)($110,000) + (0.5)($25,000) = $67,500.

calculator:

1

DIFFICULTY:

Difficulty: Easy

Multiple Choice

HAS VARIABLES:

False

PREFACE NAME:

Steppingstone Incorporated

IFMG.DAVE.19.14.03 – LO: 14-3

NATIONAL STANDARDS:

United States – BUSPROG: Analytic

United States – ak – DISC: Capital structure

LOCAL STANDARDS:

United States – OH – Default City – TBA

TOPICS:

Project NPV–nonalgorithmic

OTHER:

TYPE: Multiple Choice: Multi-part

The problems referring to Preface for Steppingstone Incorporated MUST be kept together.

DATE CREATED:

10/30/2017 8:09 PM

DATE MODIFIED:

1/6/2018 7:14 PM

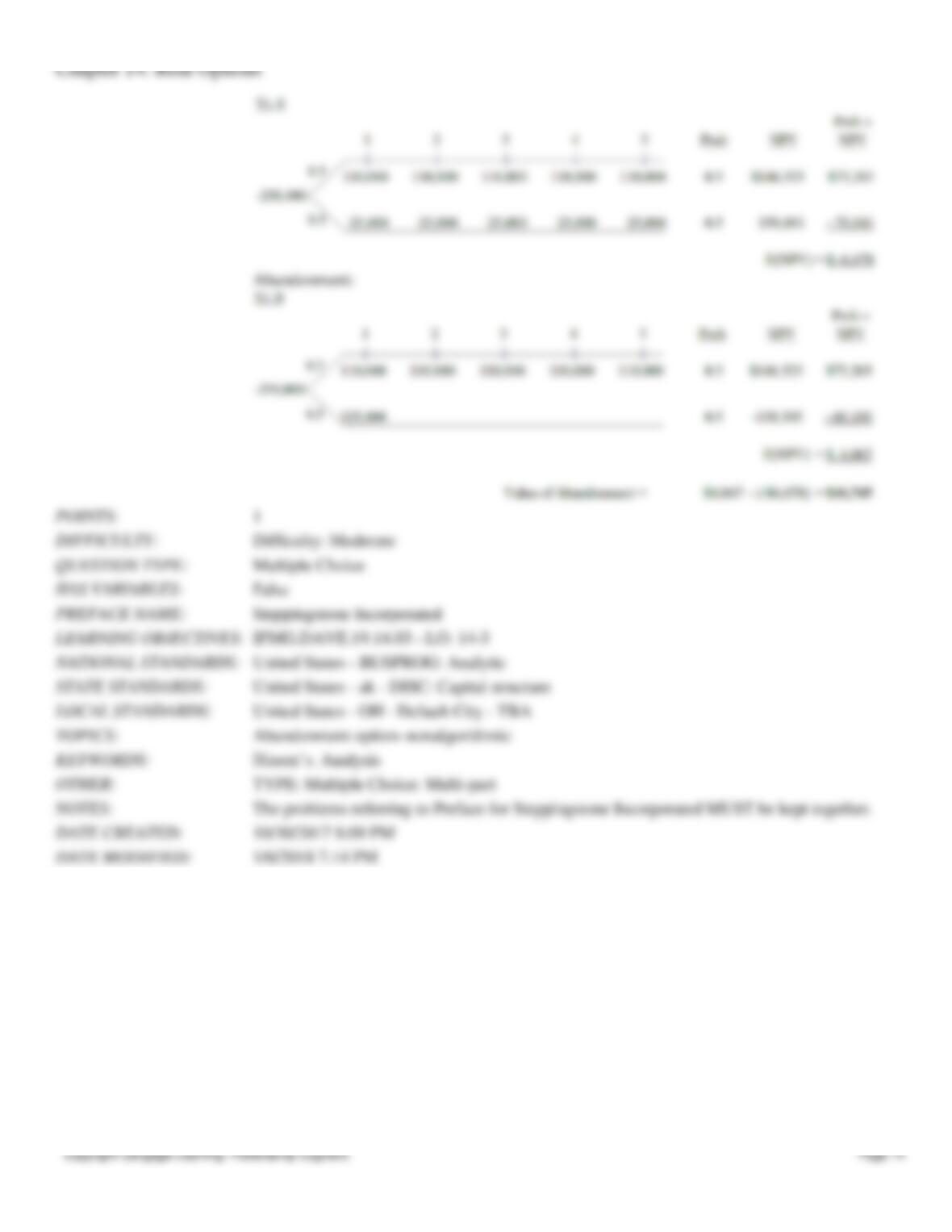

19. Refer to data for Steppingstone Incorporated (SI). Now assume that one year from now SI will know if the Z−45 has

become the industry standard. Also assume that after receiving the cash flows at t = 1, SI has the option to abandon the

project, in which case it will receive an additional $100,000 at t = 1 but no cash flows after t = 1. Assuming that the cost

of capital remains at 12%, what is the estimated value of the abandonment option?

a.

$0

b.

$2,075

c.

$4,067

d.

$8,945

e.

$10,745

ANSWER:

e

Chapter 14: Real Options

Copyright Cengage Learning. Powered by Cognero.

Page 14