Fundamentals of Multinational Finance, 5e (Moffett et al.)

Chapter 14 Multinational Tax Management

Multiple Choice and True/False Questions

14.1 Tax Principles

1) The primary objective of multinational tax planning is to minimize the firm’s worldwide tax

burden.

2) The issue of ethics in the reporting of income and the payment of taxes is a considerable one.

The authors state that most MNEs operating in foreign countries tend to follow the general

principle of

A) “when in Rome, do as the Romans do.”

B) full disclosure to the tax authorities.

C) maintain a competitive playing field by cheating as much as the local competition, no more,

no less.

D) none of the above.

3) Which of the following is an unlikely objective of U.S. government policy for the taxation of

foreign MNEs?

A) to raise revenues

B) to provide an incentive for U.S. private investment in developing countries

C) to improve the U.S. balance of payments

D) All of the above are objectives.

2

4) A ________ tax policy is one that has no impact on private decision-making, while a

________ policy is designed to encourage specific behavior.

A) flat; tax incentive

B) neutral; flat

C) neutral; tax incentive

D) none of the above

5) Which of the following is NOT an example of a tax incentive policy?

A) The federal government gives a tax credit to MNEs that make domestic capital improvements

but not foreign capital improvements.

B) Corporations are allowed to take a direct tax credit for each dollar of matching donations they

make to institutions of higher education.

C) A tax law is passed that makes interest on property non tax-deductible, but interest payments

on durable goods are.

D) All are examples of a tax incentive policy.

6) General Motors operates in many different countries and pays taxes at many different rates.

However, they always pay the same rate as their local competitors. General Motors is operating

in an environment of ________ tax policy.

A) domestic neutrality

B) foreign neutrality

C) territorial approach

D) none of the above

7) The United States taxes the domestic and remitted foreign earnings of U.S. based MNEs no

matter where the earnings occurred. This is an example of a ________ approach to levying taxes.

A) worldwide

B) territorial

C) neutral

D) equitable

8) The United States taxes all earnings on U.S. soil by both domestic and foreign firms. This is

3

an example of a ________ approach to levying taxes.

A) worldwide

B) neutral

C) territorial

D) none of the above

9) A country CANNOT have both a territorial and a worldwide approach as a national tax policy.

10) Jensen Optimetrics Inc. is based in a country with a territorial approach to taxation but

generates 100% of its income in a country with a worldwide approach to taxation. The tax rate in

the country of incorporation is 25%, and the tax rate in the country where they earn their income

is 50%. In theory, and barring any special provisions in the tax codes of either country, Jensen

should pay taxes at a rate of

A) 75%.

B) 62.5%.

C) 0%.

D) 50%.

11) The territorial approach to taxation policy is also termed the ________ approach.

A) source

B) ethical

C) greedy

D) location

12) Tax treaties generally have the effect of increasing the withholding taxes between the

countries that are negotiating the treaties.

13) Typical result of a tax treaty between two countries is

A) decreased level of business relationships.

B) reduced withholding tax on dividend repatriation.

C) stipulation that both countries will use worldwide approach in determining taxable income.

D) eliminating any tax on imported goods.

14) Corporate income tax rates

A) have been in constant decline over the last decade.

B) are becoming competitiveness argument to attract inward direct and portfolio investments.

C) tend to be higher in the highly industrialized countries.

D) all of the above

15) ________ taxes are applied to income and ________ taxes are applied to some other

measurable performance characteristic of the firm.

A) Income; direct

B) Indirect; income

C) Indirect; direct

D) Direct; indirect

16) Depending on the host country, corporate income taxes worldwide may be as low as

A) 0%.

B) 5%.

C) 10%.

D) 15%.

17) The basic idea behind withholding taxes for foreign investors is

A) to receive taxes on passively earned income.

B) a recognition that most foreign investors are unlikely to file taxes in the host country.

C) to ensure that income earned is taxed by the host country.

D) all of the above.

18) A value-added tax has gained widespread use in Western Europe, Canada, and parts of Latin

America.

19) A tax that is effectively a sales tax at each stage of production is defined as a/an ________

tax.

A) flat

B) equitable

C) value-added tax

D) none of the above

20) What is the total value of taxes paid in the following example if the value added tax is 10%?

A farmer raises wheat that he sells for $1.50 to the grain company. The grain company sells to

the processor for $2.00 per bushel. The processor turns the wheat into a breakfast cereal and

wholesales it for $3.00 per bushel. The retailer sells the cereal for $4.00 per bushel.

A) $0.15

B) $0.20

C) $0.30

D) $0.40

21) A tax that is a form of social redistribution of income is defined as a/an ________ tax.

A) un-American

B) transfer

C) flat

D) none of the above

22) A ________ is a direct reduction of taxes whereas a ________ reduces the taxable income

before taxes.

A) foreign tax credit; domestic tax credit

B) tax deduction; tax credit

C) tax credit; tax deduction

D) none of the above

23) Tax credits are less valuable on a dollar-for-dollar basis than are tax-deductible expenses.

Instruction 14.1:

Use the information to answer the following question(s).

Rogue River Exporters USA has $100,000 of before-tax foreign income. The host country has a

corporate income tax rate of 25% and the U.S. has a corporate income tax rate of 35%.

24) Refer to Instruction 14.1. If the U.S. has no bilateral trade agreement with the host country,

what is the total amount of income taxes Rogue River Exporters will pay?

A) $25,000

B) $35,000

C) $51,250

D) $60,000

25) Refer to Instruction 14.1. If the U.S. has a bilateral trade agreement with the host country

that calls for the total tax paid to be equal to the maximum amount that could be paid in the

highest taxing country, what is the total amount of income taxes Rogue River Exporters will pay

to the host country, and how much will they pay in U.S income taxes on the foreign earned

income?

A) $25,000; $10,000

B) $25,000; $26,250

C) $35,000; $0

D) None of the above

26) Refer to Instruction 14.1. If the U.S. treated the taxes paid on income earned in the host

country as a tax-deductible expense, then Rogue River’s total U.S. corporate tax on the foreign

earnings would be

A) $10,000.

B) $26,250.

C) $35,000.

D) $51,250.

27) Refer to Instruction 14.1. If the U.S. treated the taxes paid on income earned in the host

country as a tax-credit, then Rogue River’s total U.S. corporate tax on the foreign earnings would

be

A) $51,250.

B) $35,000.

C) $26,250.

D) $10,000.

28) Which of the following factors is NOT important for U.S. corporations for determining the

amount of foreign tax credit allowed for direct taxes paid on income in a foreign country?

A) the Foreign corporate income tax rate

B) the U.S. corporate income tax rate

C) the foreign corporate dividend withholding tax rate

D) All of the above are important factors.

29) Tax treaties typically result in ________ between the two countries in question.

A) lower property taxes for U.S. citizens overseas

B) elimination of differential tax rates

C) increased double taxation

D) reduced withholding tax rates

30) The value-added tax is

A) similar to an ad valorem tax on imports.

B) a form of direct taxation on corporate income.

C) a form of national sales tax.

D) none of the above.

31) Domestic tax neutrality means that

A) a dollar earned anywhere in the world by a U.S. corporation is taxed the same as if earned in

the U.S.

B) tax rates are neither regressive nor progressive.

C) foreign affiliates must neutralize their income by subtraction of foreign investment credits.

D) all of the above.

32) Some countries assess extremely low corporate income tax rates on foreign source income in

order to

A) attract tax haven affiliates of foreign multinationals.

B) boost the value of their domestic currency.

C) support higher taxes of their domestic companies.

D) none of the above.

33) Developing foreign markets can create shareholder value. Manipulating global tax payments

does not create shareholder value.

34) Poland has a corporate income tax rate that is higher than that in the United States by the

amount of 40% in Poland and 35% in the U.S. This differential mean that a U.S. parent operating

with a subsidiary in Poland can realize an

A) excess profit on their Polish investment.

B) excess foreign tax deficit.

C) excess foreign tax credit.

D) none of the above.

35) Which of the following is NOT a disadvantage of the value-added tax?

A) The tax may have an inflationary impact.

B) It is a regressive tax.

C) It increases the total tax burden.

D) All are disadvantages.

36) The purpose of a withholding tax on dividend income is to

A) raise the effective as rate of the local host country.

B) provide an incentive for MNEs to pay higher dividends to their parent companies.

C) obtain a minimum tax payment on the incomes of dividend income receipts.

D) encourage MNEs to reposition profits outside of their countries.

37) The two basic approaches to national tax systems are

A) domestic and foreign.

B) worldwide and territorial.

C) high and low rates.

D) continental and global.

38) All indications are that the value-added tax will soon be the dominant form of taxation in the

U.S.

14.2 Transfer Pricing

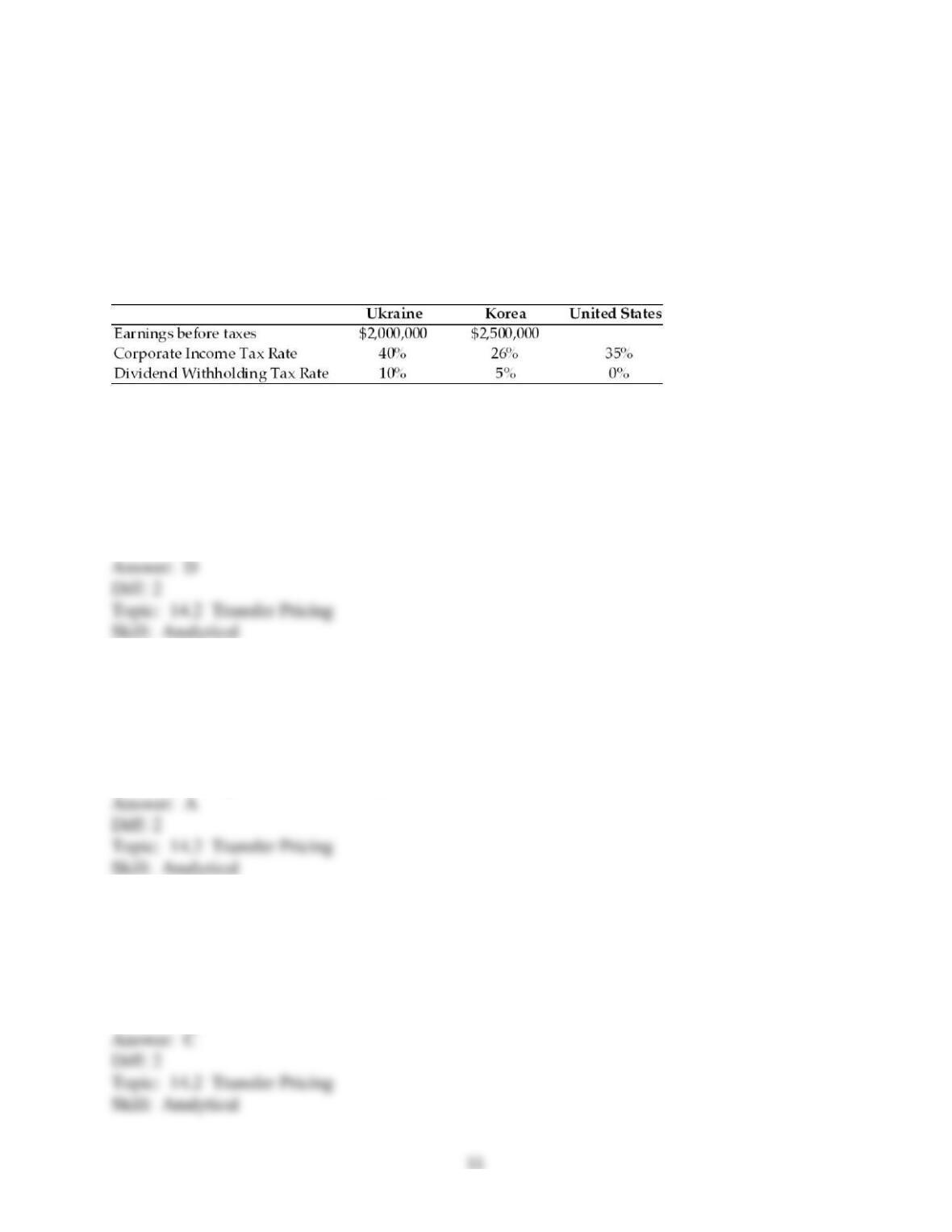

TABLE 14.1

Uses the information to answer the following question(s).

MetroCity Designs Inc., located in Northern California, has two international subsidiaries, one

located in the Ukraine, the other in Korea. Consider the information below to answer the next

several questions.

1) Refer to Table 14.1. If MetroCity pays out 50% of its earnings from each subsidiary, what are

the additional U.S. taxes due on the foreign sourced income from the Ukraine and Korea

respectively.

A) Ukraine = $0; Korea = ($30,000)

B) Ukraine = $100,000; Korea = $0

C) Ukraine = $0; Korea = $66,250

D) None of the above

2) Refer to Table 14.1. The additional U.S. taxes due on the repatriation of income from the

Ukraine to the United States, alone, assuming a 50% payout rate, is

A) excess foreign tax credits of $110,000.

B) additional U.S. taxes due of $97,000.

C) additional U.S. taxes due of $36,500.

D) excess foreign tax credits of $18,500.

3) Refer to Table 14.1. How much in additional U.S. taxes would be due if MetroCity averaged

the tax credits and liabilities of the two foreign units, assuming a 50% payout rate from each?

A) $3,750

B) $13,750

C) $2,500

D) $0

4) Refer to Table 14.1. If MetroCity set the payout rate from the Ukraine subsidiary at 25%, how

should MetroCity set the payout rate of the Korean subsidiary (approximately) to more

efficiently manage its total foreign tax bill?

A) 28.5%

B) 24.5%

C) 42.6%

D) 82.3%

5) Refer to Table 14.1. What is the minimum effective tax rate that MetroCity can achieve on its

foreign-sourced income?

A) 26%

B) 35%

C) 40%

D) 0%

6) Transfer pricing is a strategy that may be used by MNEs to

A) reduce consolidated corporate income taxes.

B) partially finance a subsidiary in another country.

C) transfer funds from a subsidiary to the parent corporation.

D) all of the above.

7) The U.S. Internal Revenue Service can reallocate revenues and expenses between parent

corporations and their subsidiaries to more clearly reflect a proper allocation of income. In such

instances it is the responsibility of the corporation to prove that the IRS has been arbitrary in its

decision-making, thus establishing a “guilty until proven innocent” tax approach.

8) A parent firm wishing to transfer funds out of its subsidiary country

A) can charge lower prices on goods and services sold to its subsidiary in the country.

B) can petition the Government for 0% withholding tax on interest earned worldwide.

C) can loan zero interest intra-company funds from the HQ for purchase of new assets.

D) can issue a cross border letter of credit guaranteeing for its subsidiary line of credit.

9) ________ is NOT an “arm’s length price” method of determining transfer prices among parent

and affiliated firms.

A) Comparable uncontrolled price method

B) Resale price method

C) Cost-plus method

D) All of the above are acceptable methods.

10) Johnson Worldwide Aeronautics Inc., headquartered in the United States, is attempting to

reduce the firm’s consolidated total income taxes. The firm has just made a sale of parts to their

affiliate in Lithuania, a country that has a corporate income tax rate of 15%. If the United States

has a corporate income tax rate of 35%, which of the following transfer pricing strategies should

Johnson attempt to follow?

A) Comparable parts were sold to a subsidiary in the United States for $1,000,000, therefore,

Johnson should price the parts for $1,000,000.

B) If Johnson made an individual stand-alone sale of these parts on the open market the

estimated price is $1,250,000. Therefore, this should be Johnson’s price.

C) If Johnson were to allocate full costs including overhead and a reasonable profit on the sale,

they could charge a total of $1,500,000. Therefore this should be Johnson’s price.

D) Johnson’s price to its affiliate makes no difference; the consolidated income taxes will be the

same regardless of the transfer pricing technique used by the firm.

11) A foreign subsidiary has $2,000,000 of taxable income, a (foreign) corporate tax rate of 25%,

and a foreign dividend withholding rate of 10%. The U.S. (domestic) parent has a corporate tax

rate of 30%. What are the total taxes paid by the foreign subsidiary? Assume that the foreign

subsidiary is 100% owned by the U.S. parent and that all after-tax income is paid to the U.S.

parent.

A) $0.00

B) $650,000

C) $500,000

D) $1,350,000

12) A foreign subsidiary has $2,000,000 of taxable income, a (foreign) corporate tax rate of 25%,

and a foreign dividend withholding rate of 10%. The U.S. (domestic) parent has a corporate tax

rate of 30%. What are the additional taxes paid by the U.S. domestic parent after the foreign

subsidiary pays corporate and withholding taxes? Assume that the foreign subsidiary is 100%

owned by the U.S. parent and that all after-tax income is paid to the U.S. parent.

A) $0.00

B) $600,000

C) $405,000

D) $250,000

13) Among the G7 nations, the U.S. has a below average corporate income tax rate that makes it

attractive for other countries to invest in the U.S.

14) In the mid 1980s the U.S. led the way to higher corporate income tax rates worldwide.

Today, most of the G7 nations have surpassed the U.S. and have higher corporate income tax

rates than the U.S.

15

15) ________ is the pricing of goods, services, and technology between related companies.

A) Among pricing

B) Retail pricing

C) Transfer pricing

D) Wholesale pricing

14.3 Tax Management at Trident

1) Trident Germany paid 28% corporate income tax and declared dividend to its US parent. The

corporate tax rate in US is 35%.

A) Dividends remitted to US parent result in excess foreign tax credit

B) Dividends remitted to US parent result in deficit foreign tax credit.

C) Dividends remitted to US parent are not subject to withholding tax because US tax rate is

higher.

D) US parent does not pay taxes on income earned outside of US.

14.4 Tax-Haven Subsidiaries and International Offshore Financial Centers

1) Tax-haven subsidiaries, categorically referred to as International Offshore Financial Centers,

have the following characteristics EXCEPT

A) a low tax on foreign investment or sales income earned by resident corporations and a low

dividend withholding tax on dividends paid to the parent firm.

B) a stable currency to permit easy conversion of funds into and out of the local currency. This

requirement can be met by permitting and facilitating the use of Eurocurrencies.

C) a stable government that encourages the establishment of foreign-owned financial and service

facilities within its borders.

D) All of the above are tax-haven subsidiary characteristics.

2) The typical tax-haven subsidiary owns the common stock of its related operating foreign

subsidiaries.

3) For U.S. MNEs, the tax-deferral privilege operating through a foreign subsidiary was not

originally a tax loophole. On the contrary, it was granted by the U.S. government to allow U.S.

firms to expand overseas and place them on a par with foreign competitors, that also enjoy

similar types of tax deferral and export subsidies of one type or another.

Essay Questions

14.1 Tax Principles

1) Explain the worldwide and territorial approaches of national taxation. The authors state that

the United States uses both approaches. How can this be? Give an example of each taxation

approach.

2) What is a value-added tax? Where is this type of tax in wide usage? Why do you suppose this

form of taxation has not been widely accepted in the United States?

14.2 Transfer Pricing

1) The pricing of goods, services, and technology transferred to a foreign subsidiary from an

affiliated company, transfer pricing, is the first and foremost method of transferring funds out of

a foreign subsidiary. When engaged in transfer pricing managers must consider at least two basic

factors; Fund Positioning Effect and the Income Tax Effect. Explain each of these effects.

14.3 Tax Management at Trident

1) There are no questions in this section.

14.4 Tax-Haven Subsidiaries and International Offshore Financial Centers

1) Many MNEs have foreign subsidiaries that act as tax havens for corporate funds awaiting

reinvestment or repatriation. Tax-haven subsidiaries, categorically referred to as International

Offshore Financial Centers, are partially a result of tax-deferral features on earned foreign

income allowed by some of the parent countries. Tax-haven subsidiaries are typically established

in a country that can meet four basic requirements: List and define these requirements.