Corporate Finance, 4e (Berk / DeMarzo)

Chapter 13 Investor Behavior and Capital Market Efficiency

13.1 Competition and Capital Markets

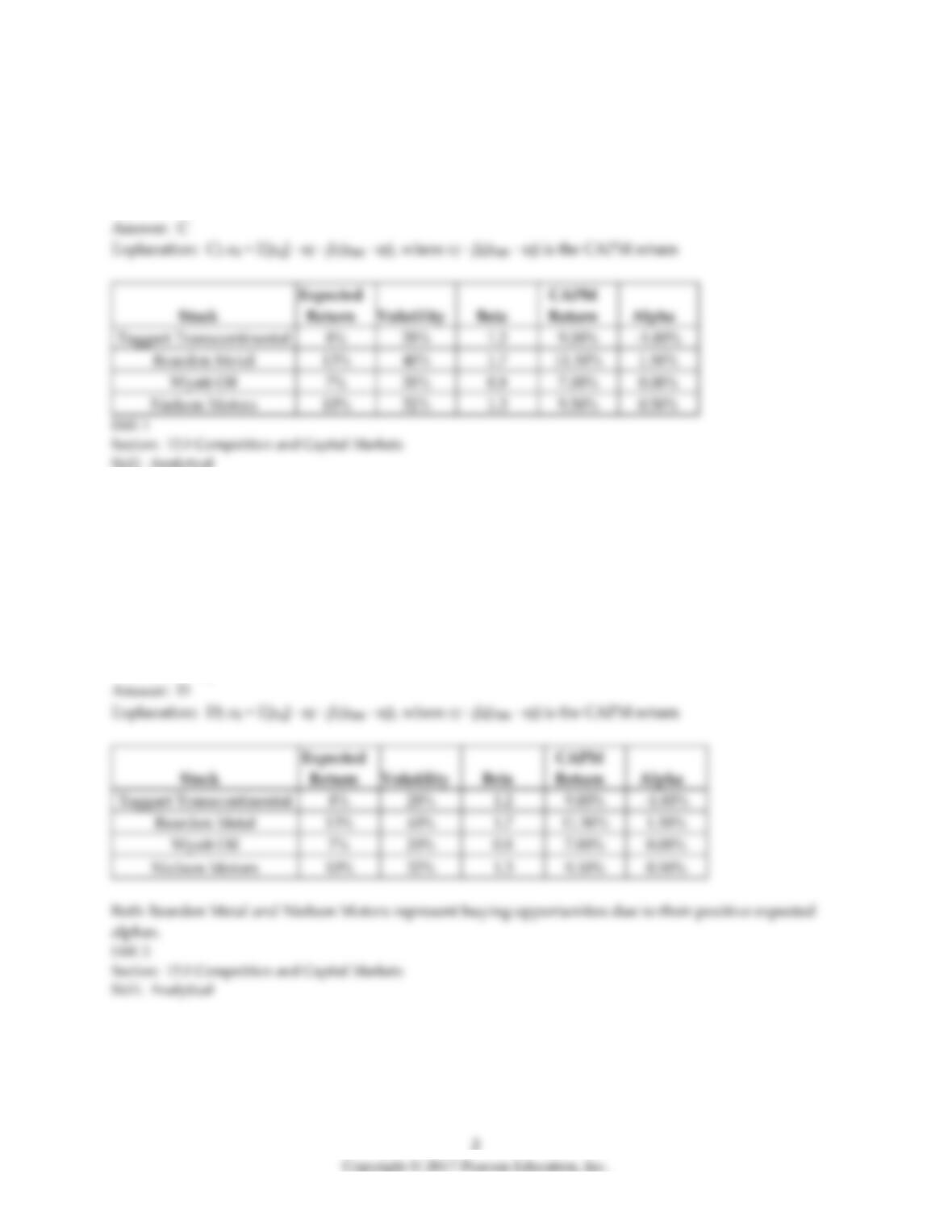

Use the following information to answer the question(s) below.

Assume that the CAPM is a good description of stock price returns. The market expected return is 8%

with 12% volatility and the risk-free rate is 3%. New news arrives that does not change any of these

numbers, but it does change the expected returns of the following stocks:

Stock

Expected

Return

Volatility

Beta

Taggart Transcontinental

8%

28%

1.2

Rearden Metal

13%

40%

1.7

Wyatt Oil

7%

20%

0.8

Nielson Motors

10%

32%

1.3

1) The expected alpha for Taggart Transcontinental is closest to:

A) -3.00%

B) -1.00%

C) 1.00%

D) 3.00%

2) The expected alpha for Wyatt Oil is closest to:

A) -3.00%

B) -1.00%

C) 0.00%

D) 3.00%

3) Which of the following stocks represent buying opportunities?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 1 and 2 only

C) 2 and 3 only

D) 2 and 4 only

4) Which of the following stocks represent selling opportunities?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 1 and 2 only

C) 2 and 3 only

D) 2 and 4 only

5) A stock’s alpha is defined as the stock‘s:

A) expected return minus its required return.

B) expected return minus its actual return.

C) nominal return minus its required return.

D) required return minus its actual return.

13.2 Information and Rational Expectations

1) When all investors correctly interpret and use their own information, as well as information that can

be inferred from market prices or the trades of others, they are said to have:

A) sensation seeking expectations.

B) positive expectations.

C) rational expectations.

D) confident expectations.

2) The CAPM does not require investors have homogeneous expectations, but rather that they have:

A) rational biases.

B) no biases.

C) heterogenous expectations.

D) rational expectations.

3) Which of the following statements is FALSE?

A) A conclusion of the CAPM that investors should hold the market portfolio only if they have high

quality information.

B) A conclusion of the CAPM that investors should hold the market portfolio even if they do not have

high trading skills.

C) Even naive investors with no information should hold the market portfolio.

D) The CAPM assumption of homogeneous expectations is not necessarily a good description of the real

world.

13.3 The Behavior of Individual Investors

1) Investors that suffer from a familiarity bias:

A) prefer not to invest in companies they are familiar with.

B) favor investments in companies they are familiar with.

C) invest in the same stocks that their friends or family recommend.

D) tend to overestimate the precision of their knowledge.

2) The tendency of uninformed individuals to overestimate the precision of their knowledge is known

as:

A) overconfidence bias.

B) herd behavior.

C) familiarity bias.

D) disposition bias.

3) If investors have relative wealth concerns, they care most about:

A) the return on their portfolio relative to their overall current wealth.

B) the performance of their portfolio relative to that of their peers.

C) their current portfolio performance relative to their past portfolio performance.

D) the performance of their current wealth relative to their past wealth.

4) An individual’s desire for intense risk-taking experiences is known as:

A) phenomenon seeking.

B) herd seeking.

C) sensation seeking.

D) rational expectations seeking.

5) Which of the following is NOT true regarding individual investor behavior?

A) Individual investors fail to diversify their portfolios adequately.

B) A vast majority of individual investors hold fewer than 10 stocks in their portfolio.

C) Employees tend to overinvest in their company’s own stock.

D) Individual investors’ portfolios consistently outperform the market averages.

13.4 Systematic Trading Biases

Use the following information to answer the question(s) below.

Consider the price paths of the following stocks over a six-month period:

Stock

January

February

March

April

May

June

Taggart Transcontinental

$15

$18

$21

$18

$20

$24

Rearden Metal

$30

$22

$16

$24

$30

$36

Wyatt Oil

$20

$21

$23

$24

$26

$26

Nielson Motors

$20

$17

$14

$12

$14

$12

None of these stocks pay dividends.

1) Assume that you are an investor with the disposition effect and you bought each of these stocks in

January. Suppose that it is currently the end of March, which stocks are you most inclined to sell?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 1 and 3 only

C) 2 only

D) 2 and 4 only

2) Assume that you are an investor with the disposition effect and you bought each of these stocks in

January. Suppose that it is currently the end of March, which stocks are you most inclined to hold?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 1 and 3 only

C) 2 only

D) 2 and 4 only

3) Assume that you are an investor with the disposition effect and you bought each of these stocks in

January. Suppose that it is currently the end of June, which stocks are you most inclined to sell?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 1 and 3 only

C) 2 only

D) 1, 2, and 3 only

4) Assume that you are an investor with the disposition effect and you bought each of these stocks in

January. Suppose that it is currently the end of June, which stocks are you most inclined to hold?

1. Taggart Transcontinental

2. Rearden Metal

3. Wyatt Oil

4. Nielson Motors

A) 1 only

B) 4 only

C) 1 and 3 only

D) 2 and 4 only

5) If investors believe that others have superior information which they can take advantage of by

copying their trades, this can lead to:

A) an informational cascade effect.

B) a disposition effect.

C) a sensation seeking effect.

D) an overconfidence bias.

6) The tendency to hang on to losers and sell winners is known as the:

A) cascade effect.

B) disposition effect.

C) overconfidence bias.

D) systematic behavior bias.

7) When investors imitate each other’s actions, this is known as ________ behavior.

A) pack

B) flock

C) herd

D) shepherd

13.5 The Efficiency of the Market Portfolio

Use the following information to answer the question(s) below.

Assume that the economy has three types of people. 20% are fad followers, 75% are passive investors,

and 5% are informed traders. The portfolio consisting of all informed traders has a beta of 1.4 and an

expected return of 16%. The market has an expected return of 10% and the risk-free rate is 4%.

1) The alpha for the informed investors is closest to:

A) -2.4%

B) -0.9%

C) 0.0%

D) 3.6%

2) The alpha for the passive investors is closest to:

A) -2.4%

B) -0.9%

C) 0.0%

D) 3.6%

3) The expected return for the fad follower’s portfolio is closest to:

A) 11.5%

B) 12.4%

C) 13.6%

D) 16.0%

4) The alpha for the fad follower’s portfolio is closest to:

A) -0.9%

B) 0.0%

C) 3.6%

D) 6.0%

Use the following information to answer the question(s) below.

John Galt is a mutual fund manager at Atlas Asset Management. He can generate an alpha of 2% a year

up to $500 million of invested capital. After that amount, his skills are spread too thin, so he cannot add

value and his alpha is zero for all investments over $500 million. Atlas Asset Management charges a fee

of 0.80% on the total amount of money under management. Assume that there are always investors

looking for positive alpha investments and no investor would invest in a fund with a negative alpha.

Assume that the fund is in equilibrium, meaning that no investor either takes out money or wishes to

invest new money into the fund.

5) The alpha that investors in Galt’s fund expect to receive is closest to:

A) -.80%

B) 0.0%

C) 0.80%

D) 1.8%

6) The amount of money that Galt’s fund will have under management is closest to:

A) $500 million

B) $600 million

C) $1000 million

D) $1250 million

7) The amount of fee income that Galt’s fund will generate is closest to:

A) $3.75 million

B) $8.00 million

C) $10.00 million

D) $25.00 million

8) A stock’s ________ measures the stock’s return relative to that predicted based on its beta, at the time

of some event.

A) excessive abnormal return

B) cumulative average return

C) excessive predicted return

D) cumulative abnormal return

13.6 Style-Based Techniques and the Market Efficiency Debate

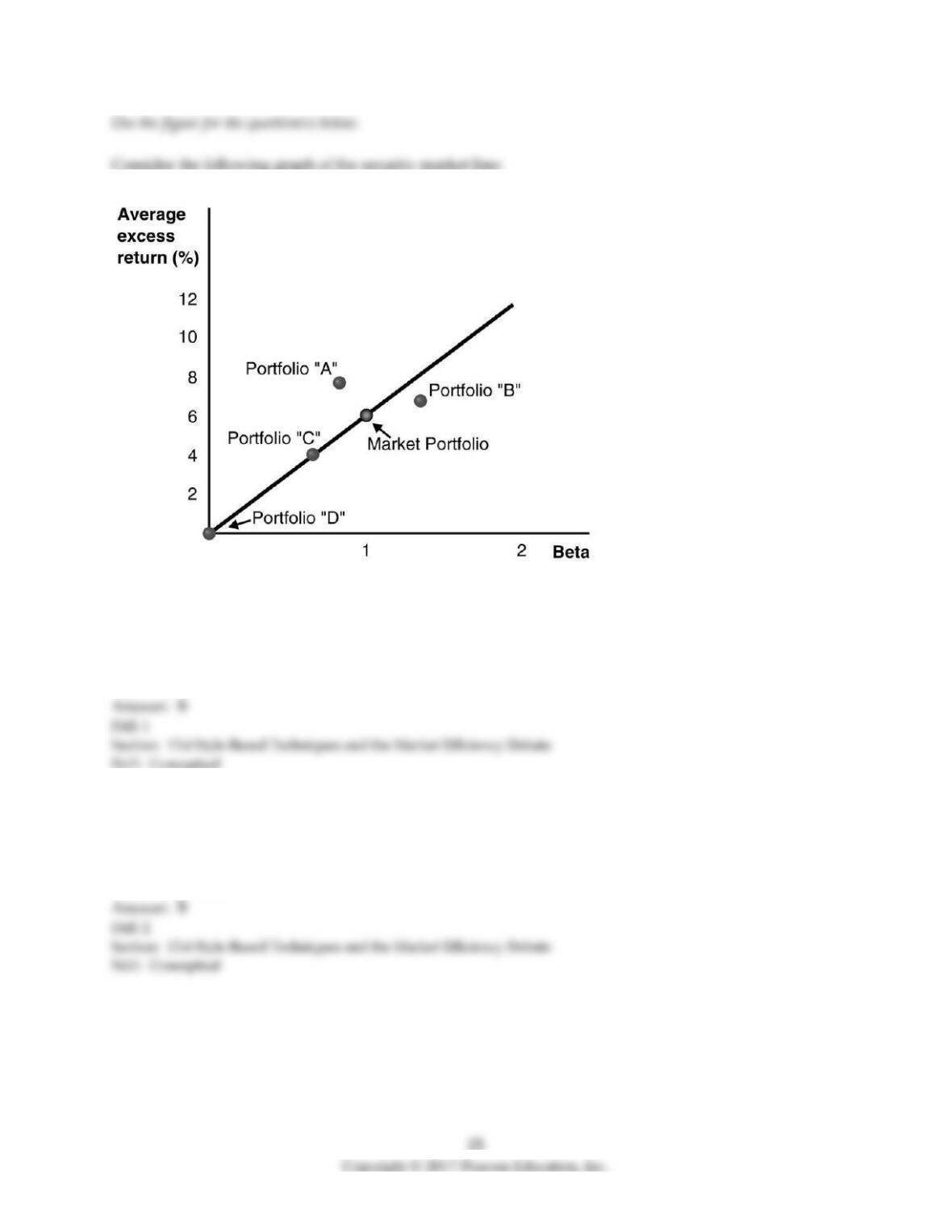

Use the following information to answer the question(s) below.

Stock

Market

Capitalization

Expected

Liquidating

Dividend

Beta

Taggart Transcontinental

$800

$920

1.10

Rearden Metal

$600

$720

1.20

Wyatt Oil

$1000

$1100

0.80

Nielson Motors

$400

$500

1.40

All amounts are in millions.

1) The correlation between the expected return and the market capitalization of these stocks is:

A) negative.

B) positive.

C) zero.

D) Unable to determine with the information given

2) If the risk-free rate is 3% and the market risk premium is 5%, then the CAPM’s predicted expected

return for Wyatt Oil is closest to:

A) 7.0%

B) 8.5%

C) 9.0%

D) 9.5%

3) If the risk-free rate is 3% and the market risk premium is 5%, then the CAPM’s predicted expected

return for Nielson Motors is closest to:

A) 8.5%

B) 9.0%

C) 9.5%

D) 10.0%

4) Which of the following statements is FALSE?

A) If the market portfolio is efficient, then all securities and portfolios must plot on the SML, not just

individual stocks.

B) For most stocks the standard errors of the alpha estimates are large, so it is impossible to conclude

that the alphas are statistically different from zero.

C) It is not difficult to find individual stocks that, in the past have not plotted on the SML.

D) Small stocks (those with lower market capitalization) have lower average returns.

5) Which of the following statements is FALSE?

A) The size effect is the observation that small stocks have positive alphas.

B) When considering portfolios formed based on the book–to-market ratio, most of the portfolios plot

below the security market line.

C) The largest alphas occur in the smallest size deciles.

D) When considering portfolios formed based on size, although the portfolios with the higher betas

yield higher returns, most size portfolios plot above the security market line.

6) Which of the following statements is FALSE?

A) Portfolios with high market capitalizations must have positive alphas if the market portfolio is not

efficient.

B) The book-to-market is the observation that firms with high book–to-market ratios have positive

alphas.

C) If the market portfolio is not efficient, then a portfolio of high book–to-market stocks will likely have

positive alphas.

D) Portfolios with low book-to-market ratios must have zero alphas if the market portfolio is efficient.

7) Which of the following statements is FALSE?

A) A momentum strategy is one where you buy stocks that have had low past returns and (short) sell

stocks that have had high past returns.

B) Over the years since the discovery of the CAPM, it has become increasing clear to researchers and

practitioners alike that forming portfolios based on market capitalization, book–to-market ratios, and

past returns, one can construct trading strategies that have a positive alpha.

C) Portfolios containing firms with the highest realized returns over the previous six months have

positive alphas over the next six months.

D) If the market portfolio is not efficient, then a portfolio of small stocks will likely have positive alphas.

8) Portfolio “B”:

A) is less risky than the market portfolio.

B) is overpriced.

C) has a positive alpha.

D) falls above the SML.

9) Portfolio “A”:

A) has a relatively lower expected return than predicted.

B) has a positive alpha.

C) falls below the SML.

D) is overpriced.