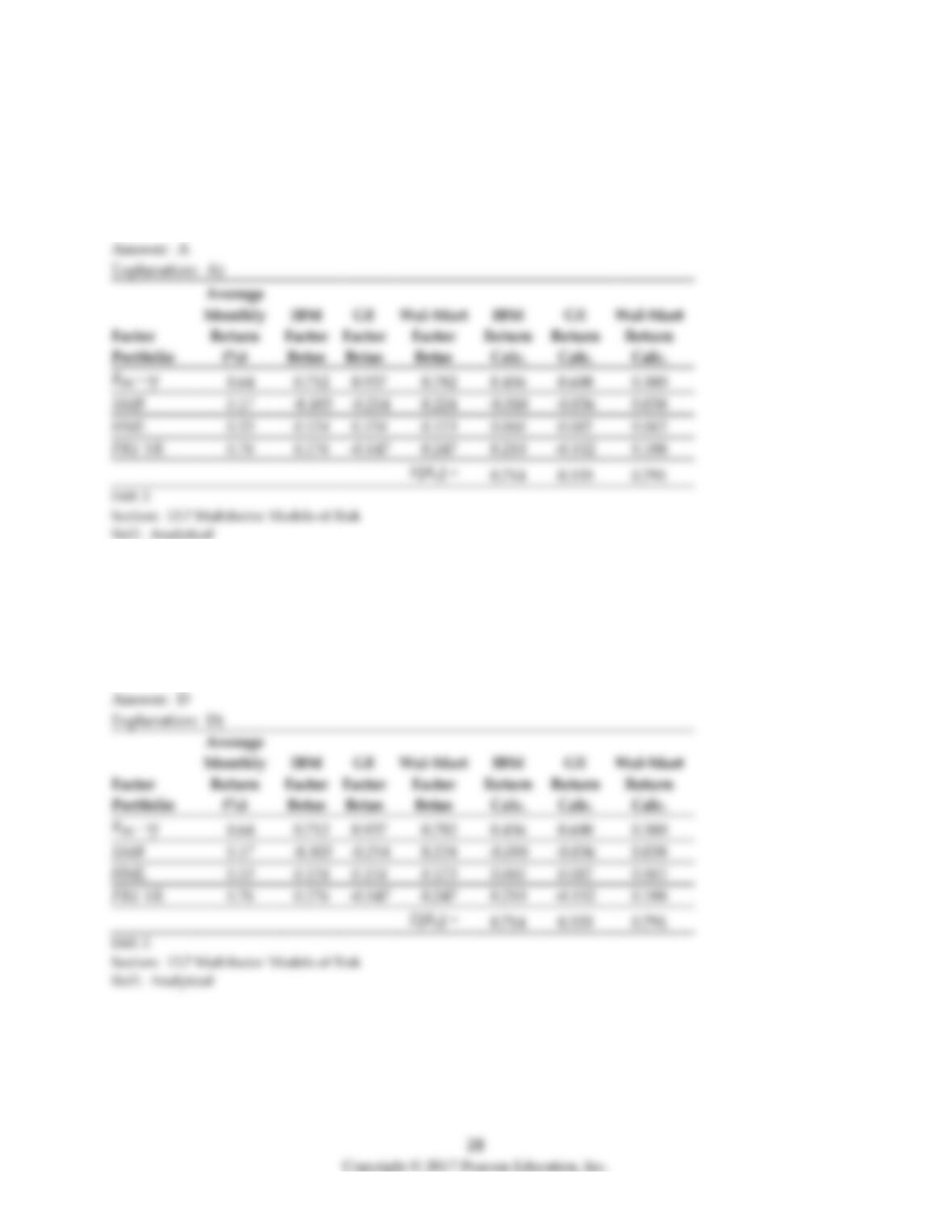

10) Portfolio “C”:

A) is less risky than the market portfolio.

B) has a relatively lower expected return than predicted.

C) is underpriced.

D) has a negative alpha.

11) Portfolio “D”:

A) falls below the SML.

B) has a negative alpha.

C) is overpriced.

D) offers an expected return equal to the risk-free rate.

12) The market portfolio:

A) is underpriced.

B) has a positive alpha.

C) is overpriced.

D) falls on the SML.

13) Which of the following statements regarding portfolio “A” is/are correct?

1. Portfolio “A” has a positive alpha.

2. Portfolio “A” is overpriced.

3. Portfolio “A” is less risky than the market portfolio.

4. Portfolio “A” should not exist if the market portfolio is efficient.

A) 1 and 2

B) 1, 3, and 4

C) 1 and 3

D) 1, 2, 3, and 4

14) Which of the following statements regarding portfolio “B” is/are correct?

1. Portfolio “B” has a positive alpha.

2. Portfolio “B” is overpriced.

3. Portfolio “B” is less risky than the market portfolio.

4. Portfolio “B” should not exist if the market portfolio is efficient.

A) 2 and 4

B) 4 only

C) 1, 3, and 4

D) 1 and 4

15) Which of the following statements regarding portfolio “C” is/are correct?

1. Portfolio “C” has a negative alpha.

2. Portfolio “C” is overpriced.

3. Portfolio “C” is less risky than the market portfolio.

4. Portfolio “C” should not exist if the market portfolio is efficient.

A) 1 and 3

B) 2 and 4

C) 1, 3, and 4

D) 3 only

Use the information for the question(s) below.

Consider two firms, Chihuahua Corporation and Bernard Industries that are each expected to pay the

same $1.5 million dollar dividend every year in perpetuity. Chihuahua Corporation is riskier and has

an equity cost of capital of 15%. Bernard Industries is not as shaky as Chihuahua, so Bernard has an

equity cost of capital of only 10%. Assume that the market portfolio is not efficient. Both stocks have

the same beta and an expected return of 12%.

16) The market value for Chihuahua is closest to:

A) $10.0 million

B) $12.5 million

C) $12.0 million

D) $15 million

17) The market value for Bernard is closest to:

A) $12.0 million

B) $10 million

C) $15.0 million

D) $12.5 million

18) The alpha for Chihuahua is closest to:

A) +2%

B) –5%

C) –3%

D) +3%

19) The alpha for Bernard is closest to:

A) +5%

B) –2%

C) –3%

D) +2%

20) Various trading strategies appear to offer non-zero alphas when we examine real world data. If

indeed these alphas are positive, it could be explained by any of the following EXCEPT:

A) Investors are systematically ignoring positive-NPV investment opportunities.

B) The market portfolio is inefficient, but the market portfolio proxy used to calculate the alphas is

efficient.

C) A stock’s beta with the market portfolio does not adequately measure a stock’s systematic risk.

D) The positive alpha trading strategies contain risk that investors are unwilling to bear but the CAPM

does not capture.

21) Which of the following is NOT an investment likely to be found in any proxy for the market

portfolio?

A) Human capital

B) Stocks

C) Bonds

D) Precious metals

22) Which of the following statements is FALSE?

A) If the CAPM correctly computes the risk premium, investors would stop investing only when they

expected the alpha of an investment strategy to be negative.

B) If the CAPM correctly computes the risk premium, an investment opportunity with a positive alpha

is a positive NPV investment opportunity.

C) If the CAPM correctly computes the risk premium, investors should flock to invest in positive alpha

stocks.

D) Anyone can implement a momentum trading strategy and therefore generate a positive investment

opportunity.

23) Which of the following statements is FALSE?

A) If indeed alphas are positive, it is possible that the positive alpha trading strategies contain risk that

investors are unwilling to bear but the CAPM does not capture.

B) If indeed alphas are positive, it is possible that the costs of implementing investment strategies are

larger than the NPVs of undertaking them.

C) If indeed alphas are positive, then investors have to be systematically ignoring negative-NPV

investment opportunities.

D) The only way a positive NPV investment opportunity can exist in a market is if some barrier to entry

restricts competition.

24) Which of the following statements is FALSE?

A) The existence of the momentum trading strategies has been widely known for at least ten years.

B) The information required to implement a momentum strategy is not readily available to investors.

C) If the market portfolio is not efficient, then a stock’s beta with the market is not an adequate measure

of its systematic risk.

D) If the market portfolio is not efficient, then the so-called profits from a positive alpha trading strategy

are really returns for bearing risk that investors are averse to and the CAPM doesn’t capture.

25) Which of the following statements is FALSE?

A) A significant fraction of investors might care about aspects of their portfolios other than expected

return and volatility, and so would be unwilling to hold inefficient investment portfolios.

B) Although the true market portfolio of all invested wealth might be efficient, the proxy portfolio

might not track the actual market very well.

C) We might be using the wrong proxy portfolio when we calculate alphas.

D) The true market portfolio consists of all traded investment wealth in the economy.

26) Which of the following statements is FALSE?

A) Nonzero alphas may merely indicate that the wrong market proxy is beings used; they do not

necessarily indicate forgone positive NPV investment opportunities.

B) The true market portfolio contains much more than just stocks, it includes bonds, real estate, art,

precious metals, and any other investment vehicles available.

C) If the true market portfolio is efficient, but the proxy portfolio is not highly correlated with the true

market portfolio, then the true market portfolio will not be efficient and stocks will have nonzero

alphas.

D) Much of the investment wealth cannot be included in the proxy for the market portfolio since it does

not trade in competitive markets.

27) Which of the following statements is FALSE?

A) The most important example of non-tradeable wealth is human capital.

B) If investors have a significant amount of non-tradeable wealth, this wealth will be an important part

of their portfolios, but will not be part of the market portfolio of tradeable securities.

C) If the entire portfolio of investments is efficient, then just the tradeable part of the portfolio should be

efficient also.

D) Researchers have found evidence that the presence of human capital can explain at least part of the

reason for the inefficiency of the most commonly used market proxies.

28) What does the existence of a positive alpha investment strategy imply?

29) Explain why the market portfolio proxy may not be efficient.

13.7 Multifactor Models of Risk

1) A group of portfolios from which we can form an efficient portfolio are called:

A) factor portfolios.

B) semi-efficient portfolios.

C) partially efficient portfolios.

D) characteristic portfolios.

Use the equation for the question(s) below.

Consider the following regression model:

Rs – rf = as + (RF1 – rf) + (RF2 – rf) + e

2) The term as is a(n):

A) error term that has an expectation of zero and is uncorrelated with either factor.

B) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the first factor portfolio.

C) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the second factor portfolio.

D) constant term.

3) The term is a(n):

A) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the second factor portfolio.

B) error term that has an expectation of zero and is uncorrelated with either factor.

C) constant term.

D) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the first factor portfolio.

4) The term is a(n):

A) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the second factor portfolio.

B) constant term.

C) error term that has an expectation of zero and is uncorrelated with either factor.

D) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the first factor portfolio.

5) The term ε is a(n):

A) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the first factor portfolio.

B) error term that has an expectation of zero and is uncorrelated with either factor.

C) measure of the expected percent change in the excess return of a security for a 1% change in the

excess return of the second factor portfolio.

D) constant term.

6) Which of the following statements is FALSE?

A) The risk premium of any marketable security can be written as the sum of the risk premium of each

factor multiplied by the sensitivity of the stock with that factor.

B) The factor betas measure the sensitivity of the stock to a particular factor.

C) If we use more than one portfolio as factors, then together these factors will capture systematic risk,

but each factor captures different components of the systematic risk.

D) When we use more than one portfolio to capture risk, the model is known as a single factor model.

7) Which of the following statements is FALSE?

A) It is not actually necessary to identify the efficient portfolio itself. All that is required is to identify a

collection of portfolios from which the efficient portfolio can be constructed.

B) Although we might not be able to identify the efficient portfolio itself, we know some characteristics

of the efficient portfolio.

C) An efficient portfolio can be constructed from other diversified portfolios.

D) An efficient portfolio need not be well diversified.

8) Which of the following statements is FALSE?

A) A portfolio costs nothing to construct is called a self–financing portfolio.

B) The most obvious portfolio to use in a multifactor model is the market portfolio itself.

C) In general, a self-financing portfolio is any portfolio with portfolio weights that sum to one rather

than zero.

D) We can construct a self-financing portfolio by going long some stocks, and going short other stocks

with equal market value.

9) Which of the following statements is FALSE?

A) Rather than relying on the efficiency of a single portfolio (such as the market), multifactor models

rely on the weaker condition that an efficient portfolio can be constructed from a collection of well-

diversified portfolios or factors.

B) A positive alpha in a single factor model means that the portfolios that implement the trading

strategy capture risk that is not captured by the market portfolio.

C) Multifactor models have a distinct advantage over single-factor models in that it is much easier to

identify a collection of portfolios that captures systematic risk than just a single portfolio.

D) Trading strategies based on market capitalization, book–to-market ratios, and momentum have been

developed that appear to have zero alphas.

25

10) Which of the following statements is FALSE?

A) Because expected returns are not easy to estimate, each portfolio that is added to a multifactor model

increases the difficulty of implementing the model.

B) The self-financing portfolio made from high minus low book-to-market stocks is called the high-

minus-low (HML) portfolio.

C) The FFC factor specification was identified a little more than ten years ago. Although it is widely

used in academic literature to measure risk, much debate persists about whether it really is a significant

improvement over the CAPM.

D) A trading strategy that each year short sells portfolio S (small stocks) and uses this position to buy

portfolio B (big stocks) has produced positive risk adjusted returns historically. This self-financing

portfolio is widely known as the small minus big (SMB) portfolio.

11) Which of the following statements is FALSE?

A) As a practical matter, it is extremely difficult to identify portfolios that are efficient because we

cannot measure the expected return and the standard deviation of a portfolio with great accuracy.

B) The portfolios in a multifactor model can be thought of as either risk factors themselves or portfolios

of stocks correlated with unobservable risk factors.

C) Each factor beta is the expected percent change in the excess return of a security for a 1% change in

the excess return of the factor portfolio.

D) Even if the market portfolio is not efficient, it still must capture all components of systematic risk.

Use the equation for the question(s) below.

Consider the following factor model:

E[Rs] – rf = (E[RMkt] – rf) + E[RSMB] + E[RHML] + E[RPR1 YR]

12) The term measures the sensitivity of the securities returns to:

A) size.

B) book-to-market.

C) momentum.

D) the overall market.

13) The term measures the sensitivity of the securities returns to:

A) momentum.

B) the overall market.

C) book-to-market.

D) size.

14) The term measures the sensitivity of the securities returns to:

A) book-to-market.

B) momentum.

C) size.

D) the overall market.

15) The term measures the sensitivity of the securities returns to:

A) the overall market.

B) book-to-market.

C) size.

D) momentum.

Use the table for the question(s) below.

Consider the following information regarding the Fama French Carhart four factor model:

Factor

Portfolio

Average

Monthly

Return (%)

IBM

Factor

Betas

GE Factor

Betas

Wal-Mart

Factor

Betas

Rm – rf

0.64

0.712

0.937

0.782

SMB

0.17

-0.103

-0.214

0.224

HML

0.53

0.124

0.154

0.123

PR1 YR

0.76

0.276

-0.147

0.247

16) Using the FFC four factor model and the historical average monthly returns, the expected monthly

return for IBM is closest to:

A) 0.79%

B) 0.53%

C) 0.71%

D) 1.01%

Portfolio

GE

Calc.

Rm – rf

SMB

0.038

HML

PR1 YR

17) Using the FFC four factor model and the historical average monthly returns, the expected monthly

return for GE is closest to:

A) 0.53%

B) 0.73%

C) 0.79%

D) 0.71%

18) Using the FFC four factor model and the historical average monthly returns, the expected monthly

return for Wal-Mart is closest to:

A) 0.71%

B) 0.53%

C) 1.38%

D) 0.79%

13.8 Methods Used in Practice

1) According to a survey of 392 CFOs conducted by John Graham and Campbell Harvey, the most

common method used in corporate America to estimate the cost of capital is:

A) the CAPM.

B) multifactor models.

C) characteristic models.

D) the dividend discount model.

2) According to study by Berk and van Binsbergen, which risk model determines mutual fund flows?

A) The CAPM risk-adjusted return

B) The absolute return

C) The excess return over T–Bills

D) Alpha-Beta factors