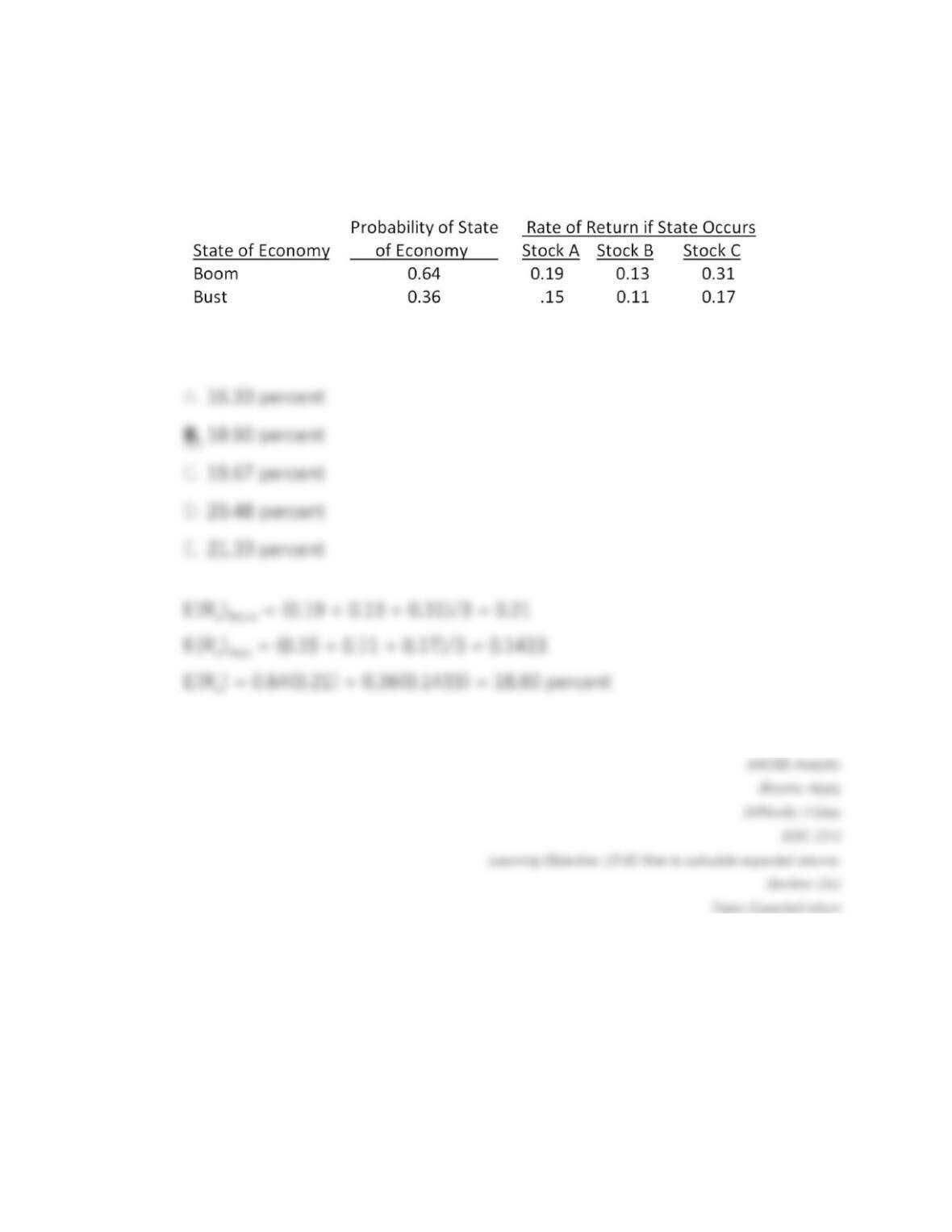

96.

What is the expected return of an equally weighted portfolio comprised of

the following three stocks?

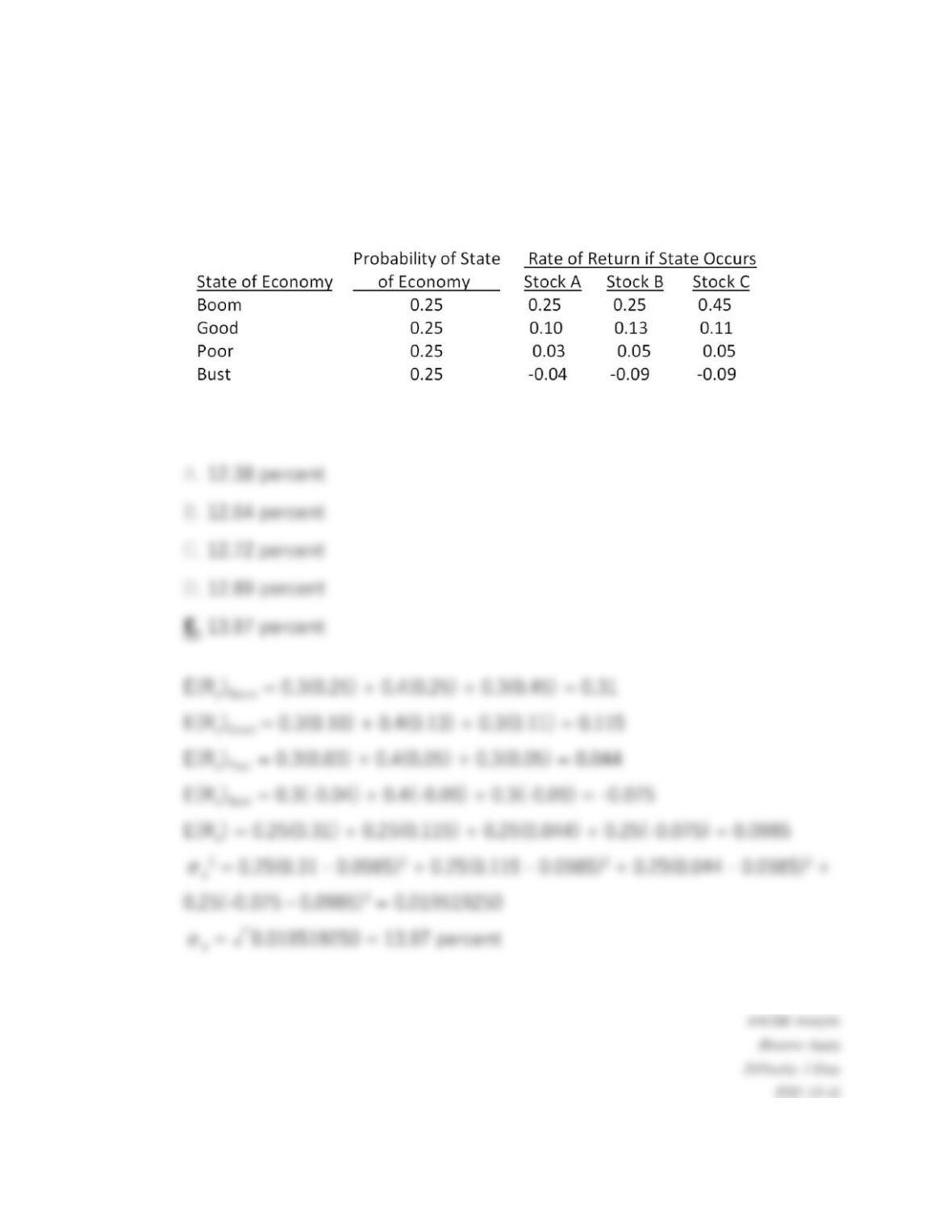

97.

Your portfolio is invested 30 percent each in Stocks A and C, and 40 percent

in Stock B. What is the standard deviation of your portfolio given the

following information?

98.

You own a portfolio equally invested in a risk-free asset and two stocks.

One of the stocks has a beta of 1.9 and the total portfolio is equally as risky

as the market. What is the beta of the second stock?

99.

A stock has an expected return of 11 percent, the risk-free rate is 5.2

percent, and the market risk premium is 5 percent. What is the stock’s

beta?

100.

A stock has a beta of 1.2 and an expected return of 17 percent. A risk-free

asset currently earns 5.1 percent. The beta of a portfolio comprised of these

two assets is 0.85. What percentage of the portfolio is invested in the

stock?

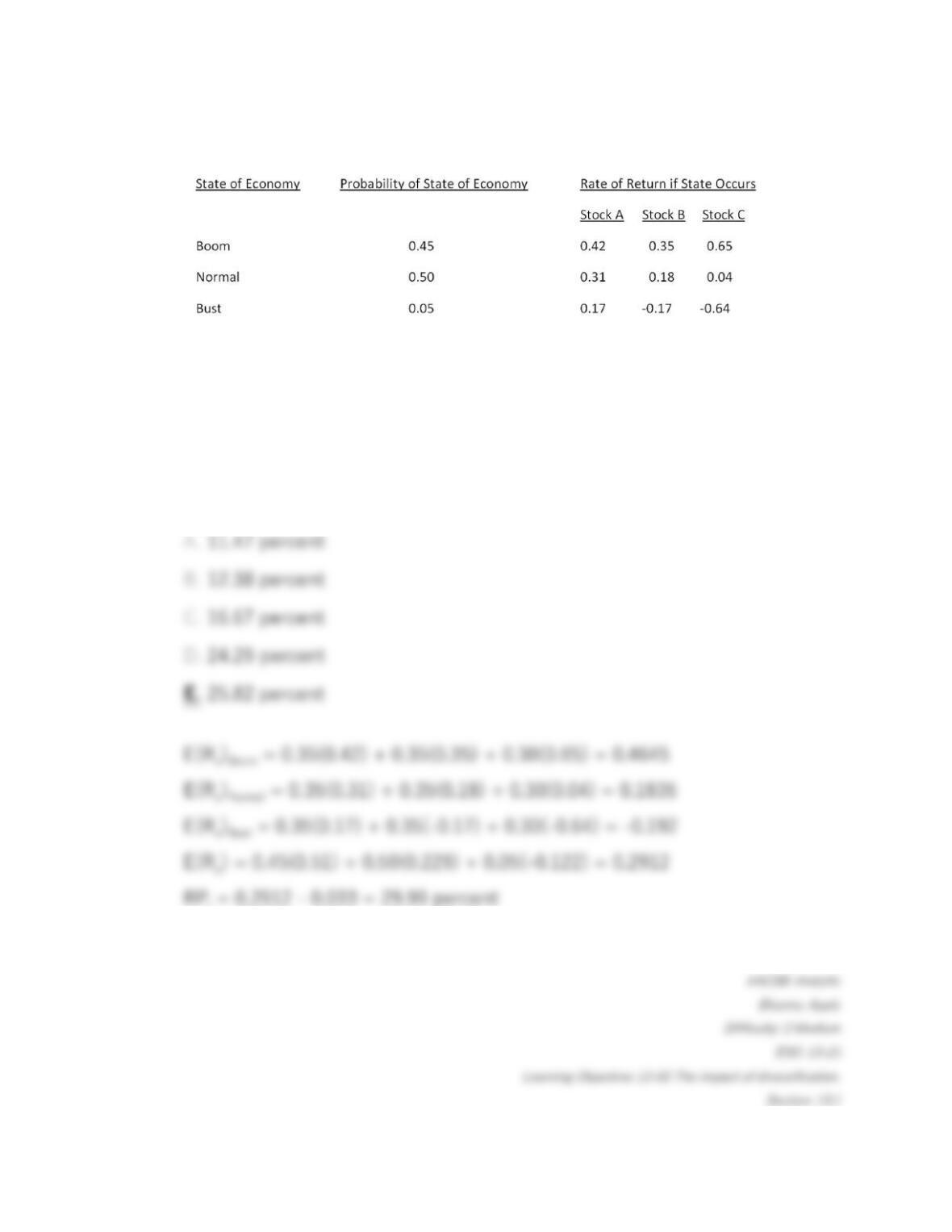

101.

Consider the following information on three stocks:

A portfolio is invested 35 percent each in Stock A and Stock B and 30

percent in Stock C. What is the expected risk premium on the portfolio if the

expected T-bill rate is 3.3 percent?

102.

Suppose you observe the following situation:

Assume these securities are correctly priced. Based on the CAPM, what is

the return on the market?

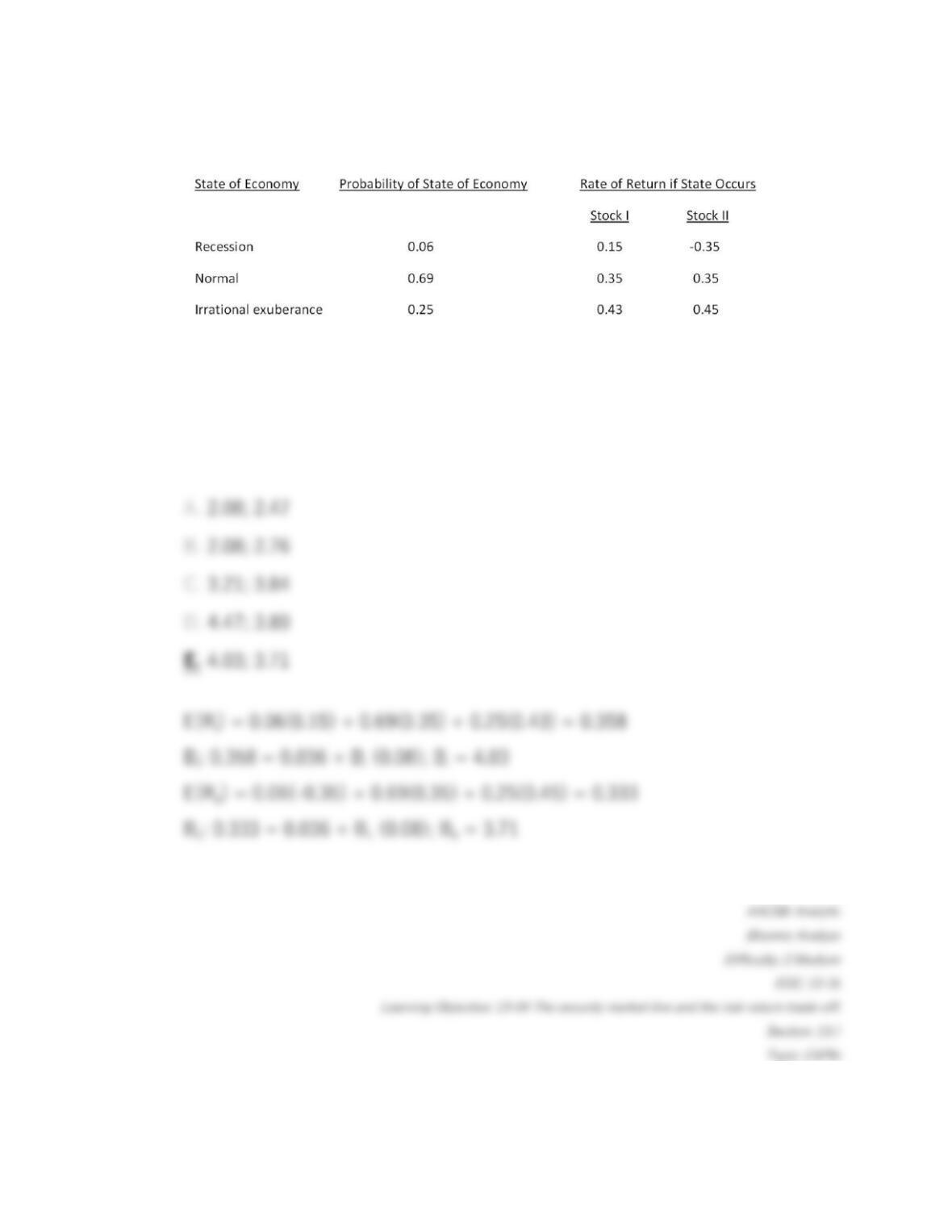

103.

Consider the following information on Stocks I and II:

The market risk premium is 8 percent, and the risk-free rate is 3.6 percent.

The beta of stock I is _____ and the beta of stock II is _____.

104.

Suppose you observe the following situation:

Assume the capital asset pricing model holds and stock A’s beta is greater

than stock B’s beta by 0.21. What is the expected market risk premium?

Essay Questions

105.

According to CAPM, the expected return on a risky asset depends on three

components. Describe each component and explain its role in determining

expected return.

106.

Explain how the slope of the security market line is determined and why

every stock that is correctly priced, according to CAPM, will lie on this line.

107.

Explain how the beta of a portfolio can equal the market beta if 50 percent

of the portfolio is invested in a security that has twice the amount of

systematic risk as an average risky security.

108.

Explain the difference between systematic and unsystematic risk. Also

explain why one of these types of risks is rewarded with a risk premium

while the other type is not.

109.

A portfolio beta is a weighted average of the betas of the individual

securities which comprise the portfolio. However, the standard deviation is

not a weighted average of the standard deviations of the individual

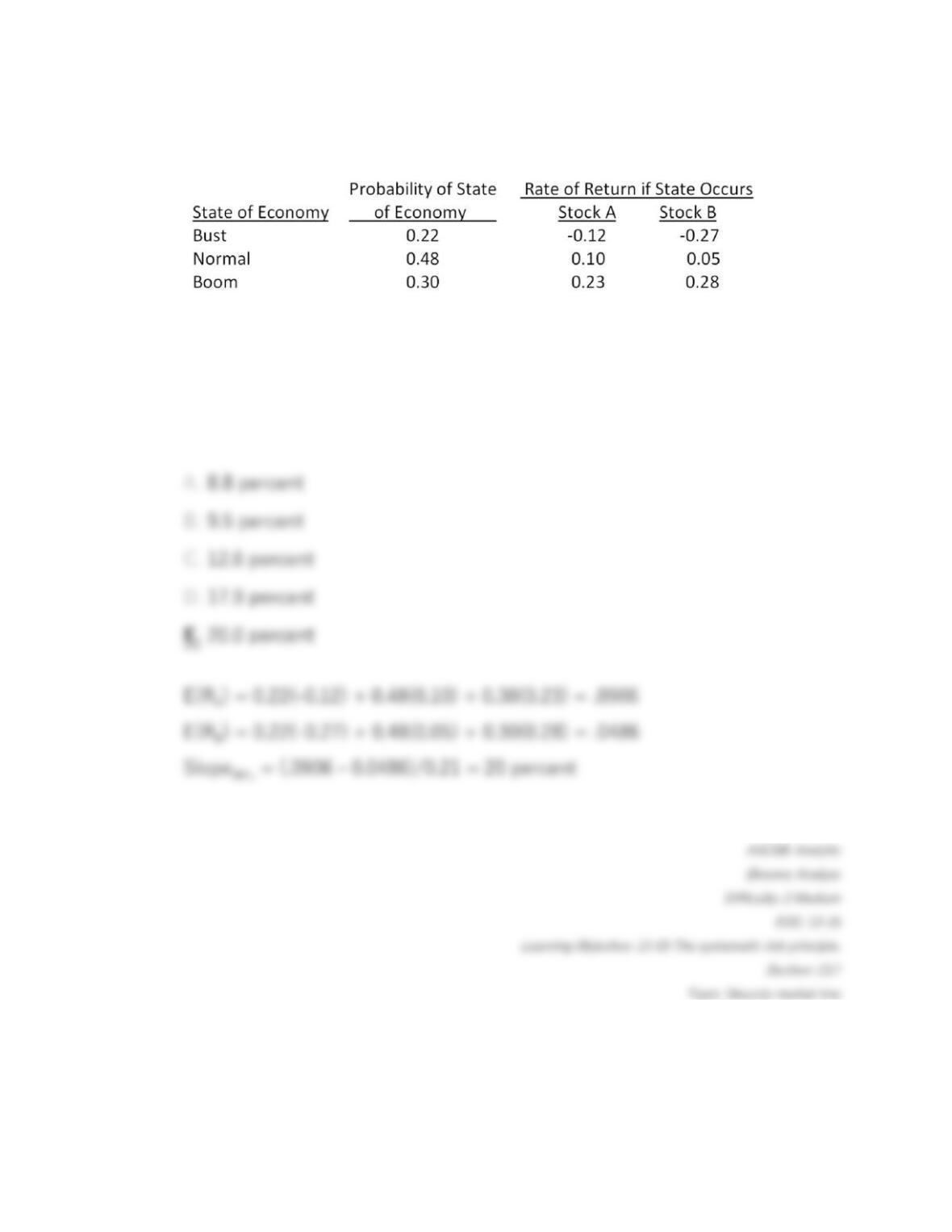

securities which comprise the portfolio. Explain why this difference exists.