47) ________ is the risk that is reflected in fluctuations of the firm’s cash flows before considering any debt

financing.

A) Systematic risk

B) Business risk

C) Financial risk

D) Diversifiable risk

48) Which of the following affects business risk?

A) operating leverage

B) interest rate stability

C) preferred stock

D) financial lease

49) Revenue stability affects ________.

A) dividend risk

B) maturity risk

C) business risk

D) interest rate risk

50) Which of the following is a difference between debt and equity capital?

A) Debt capital does not require periodic payments, whereas equity capital requires period payments.

B) Debt capital requires returns in proportion to profits, whereas equity capital requires a fixed rate of

return.

C) Debt capital provides a tax shield, whereas equity capital does not provide a tax shield.

D) Debt capital affects operating leverage, whereas equity capital affects financial leverage.

51) Which of the following is a difference between debt and equity capital?

A) Debt capital does not require periodic payments, whereas equity capital requires period payments.

B) Debt capital requires a fixed rate of return, whereas equity capital requires returns in proportion to

profits.

C) Debt capital does not provides a tax shield, whereas equity capital provides a tax shield.

D) Debt capital affects operating leverage, whereas equity capital affects financial leverage.

52) After satisfying obligations to creditors, the government, and preferred stockholders, any remaining

earnings will most likely be allocated to ________.

A) common shareholders as cash dividends

B) common shareholders as stock dividends

C) other firms requiring capital

D) pay future preferred dividends

53) The conflict resulting from a manager’s desire to increase a firm’s risk without increasing current

borrowing costs and lenders’ desire to limit lending is one effect of the ________ problem.

A) agency

B) leverage

C) capital

D) variable cost

54) Operating and financial constraints placed on a corporation by loan provision are ________.

A) agency costs to lenders

B) agency costs to a firm

C) necessary to regulate ownership of a firm

D) necessary to control the risk of a firm

55) Management has just discovered an excellent investment for which it needs additional funding.

Relative to the discussion on asymmetric information, the firm will ________.

A) finance with new common stock if management believes the firm is undervalued

B) finance with debt if management believes the firm is undervalued

C) finance with debt if management believes the firm is overvalued

D) finance with preferred stock if the firm is at value

13.3 EBIT-EPS approach to capital structure

1) A corporation borrows $1,000,000 at 10 percent annual rate of interest. The firm has a 21 percent tax

rate. The yearly, after-tax cost of this debt is ________.

A) $21,000

B) $79,000

C) $100,000

D) $126,582

2) A corporation has $5,000,000 of 8 percent preferred stock outstanding and a 21 percent tax rate. The

after-tax cost of the preferred stock is ________.

A) $506,329

B) $1,904,762

C) $666,667

D) $400,000

3) A corporation has $10,000,000 of 10 percent preferred stock outstanding and a 21 percent tax rate. The

amount of earnings before interest and taxes (EBIT) required to pay the preferred dividends is ________.

A) $1,000,000

B) $210,000

C) $790,000

D) $1,265,823

4) A corporation has $5,000,000 of 6 percent bonds and $9,600,000 of 5 percent preferred stock

outstanding. The firm’s financial breakeven (assuming a 21 percent tax rate) is ________.

A) $637,595

B) $1,387,595

C) $907,595

D) $780,000

5) The EBIT-EPS approach to capital structure involves selecting the capital structure that maximizes

earnings before interest and taxes (EBIT) over the expected range of earnings per share (EPS).

6) The EBIT-EPS analysis tends to concentrate on maximization of earnings rather than maximization of

owners’ wealth.

7) The financial breakeven point represents the level of earnings after interest and taxes necessary for a

firm to cover its fixed operating and financial changes—that is, the point at which dividends per share is

equal to zero.

8) The higher the financial breakeven point and the steeper the slope of the capital structure line, the

greater the financial risk.

9) The higher the degree of financial leverage (DFL), the greater the leverage a given financing plan has,

and the steeper its slope when plotted on EBIT-EPS axes.

10) The steeper the slope of the EBIT-EPS capital structure line, the lower is the financial risk.

11) Because risk premiums increase with increases in financial leverage, maximizing EPS does not assure

owners’ wealth maximization.

12) The basic shortcoming of EBIT-EPS analysis is that this model focuses on the maximization of

earnings rather than on the maximization of owner wealth as reflected in a firm’s stock price.

13) The basic shortcoming of EBIT-EPS analysis is that this model focuses on the maximization of stock

returns rather than on the maximization of share price.

14) In the EBIT-EPS approach to capital structure, risk is represented by ________.

A) the slope of the capital market line

B) shifts in the cost of debt capital

C) the slope of the capital structure line

D) shifts in the times-interest-earned ratio

15) A firm has a current capital structure consisting of $400,000 of 6 percent annual interest debt and

50,000 shares of common stock. The firm’s tax rate is 21 percent on ordinary income. If the EBIT is

expected to be $200,000, the firm’s earnings per share will be ________.

A) $3.12

B) $0.74

C) $3.52

D) $2.78

16) The EBIT-EPS approach to capital structure proposes that an optimal capital structure be selected

which ________.

A) maximizes the weighted average cost of capital

B) minimizes the cost of debt

C) maximizes the EPS

D) minimizes dividends

17) A firm has interest expense of $145,000, preferred dividends of $25,000, and a tax rate of 21 percent.

The firm’s financial breakeven point is ________.

A) $25,000

B) $201,646

C) $176,646

D) $145,000

18) A firm has a current capital structure consisting of $400,000 of 6 percent annual interest debt and

50,000 shares of common stock. The firm’s tax rate is 21 percent on ordinary income. If the EBIT is

expected to be $200,000, two EBIT-EPS coordinates for the firm’s existing capital structure are ________.

A) ($24,000, $0) and ($200,000, $0.74)

B) ($24,000, $0) and ($200,000, $2.78)

C) ($0, $24,000) and ($200,000, $1.82)

D) ($24,000, $0) and ($200,000, $3.52)

19) The major shortcoming of the EBIT-EPS approach to capital structure is that ________.

A) the technique does not promote the maximization of shareholder wealth

B) the technique does not consider the cost of capital

C) the technique only considers leverage-related risk

D) the technique does not maximize earnings per share

20) The basic shortcoming of the EBIT-EPS approach to capital structure is ________.

A) that the optimal capital structure is difficult to compute

B) its disregard for the presence of preferred stock in the capital structure

C) its disregard for the firm’s dividend policy

D) that it concentrates on the maximization of EPS rather than the maximization of owner’s wealth

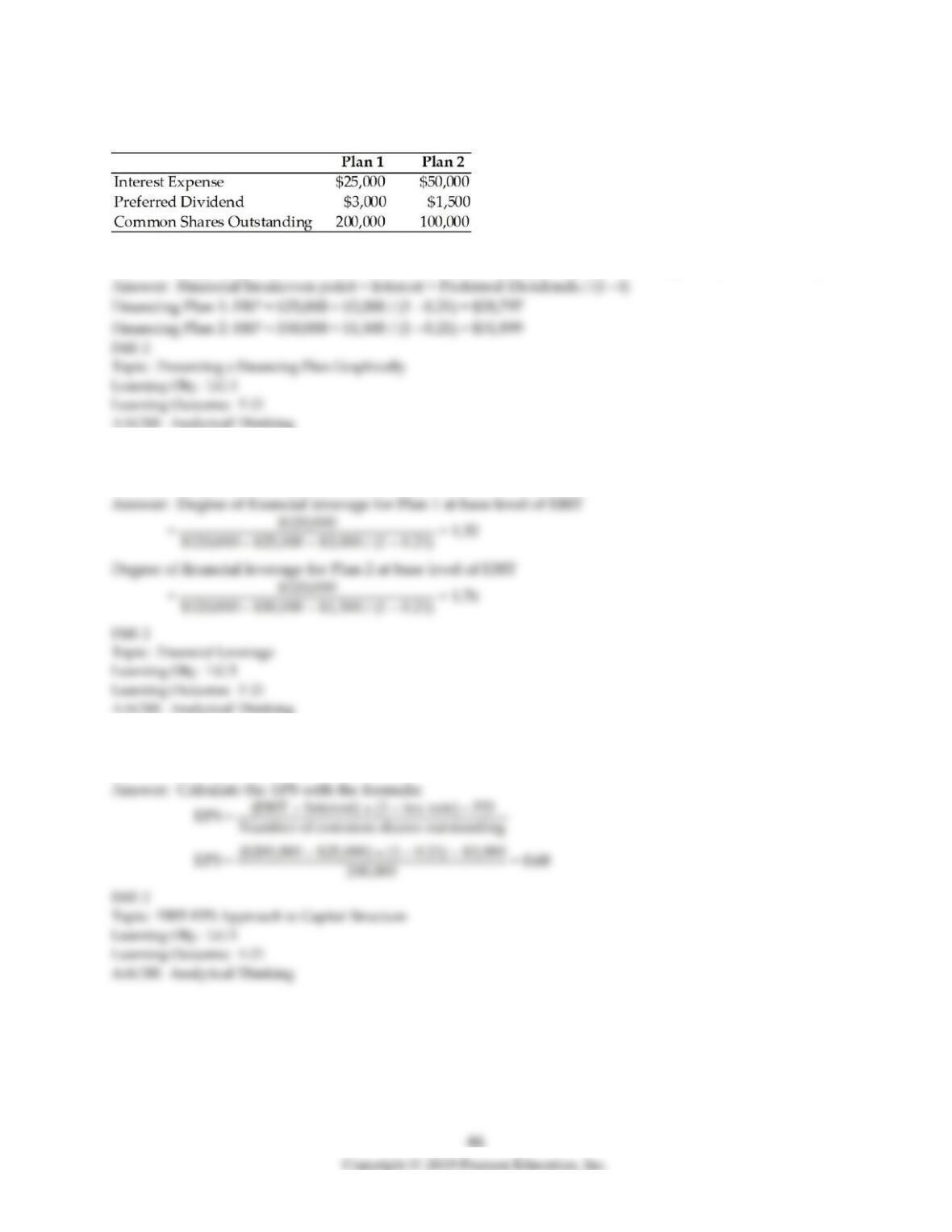

Table 13.1

21) Assuming a 21 percent tax rate, what is the financial breakeven point for each plan? (See Table 13.1)

22) What is the degree of financial leverage at a base level EBIT of $120,000 for both financing plans? The

firm has a 21 percent tax rate. (See Table 13.1)

23) What is the EPS under Financing Plan 1, if the firm projects EBIT of $200,000 and has a tax rate of 21

percent? (See Table 13.1)

24) At about what EBIT level should the financial manager be indifferent to either plan? (See Table 13.1)

25) Which plan has a higher degree of financial leverage and financial risk? (See Table 13.1)

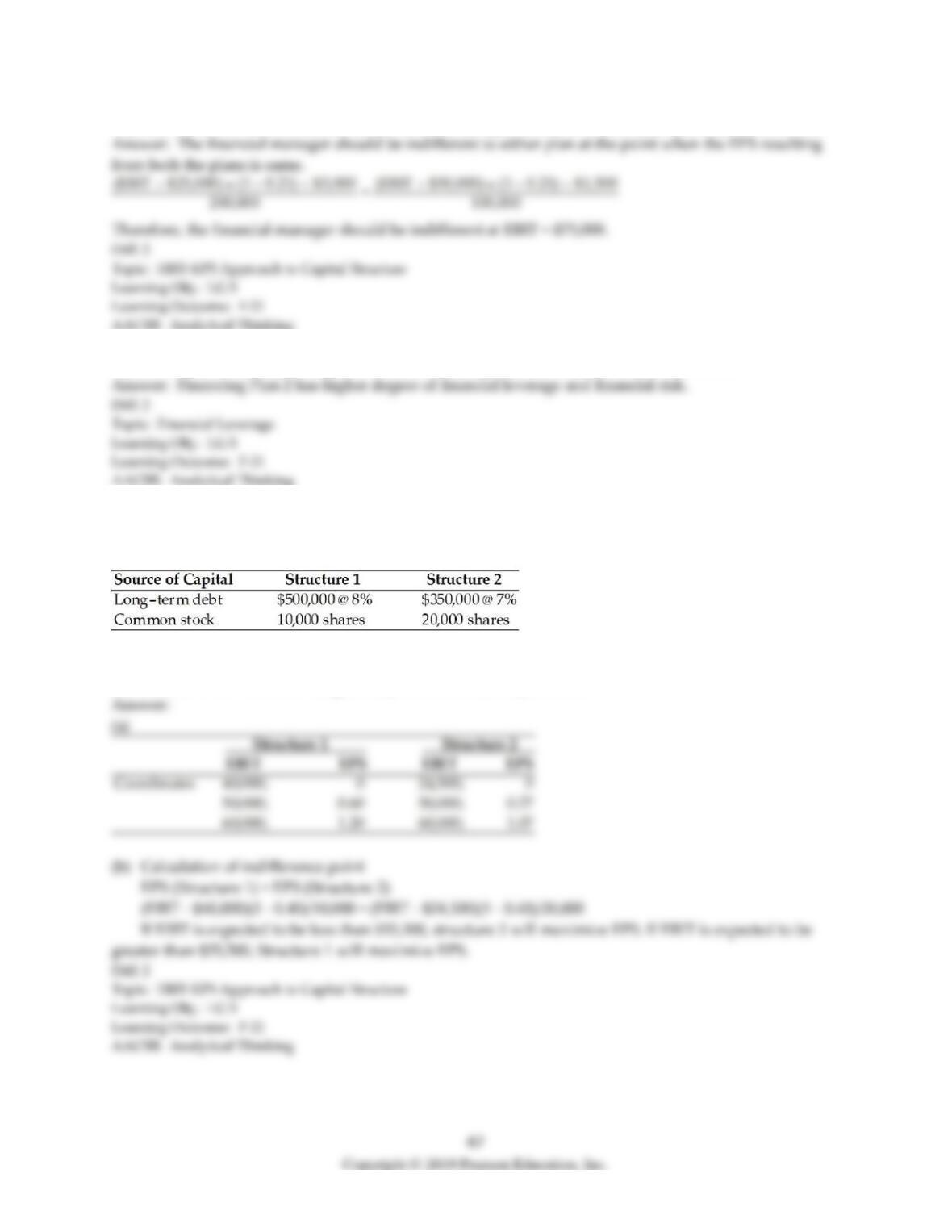

26) Frankline Coin, Inc. is considering two capital structures. The key information follows. Assume a 40

percent tax rate and expected EBIT of $50,000.

(a) Calculate two EBIT-EPS coordinates for each of the structures.

(b) Indicate over what EBIT range, if any, each structure is preferred.

13.4 Choosing the optimal capital structure

1) Minimizing the weighted average cost of capital allows management to undertake a larger number of

profitable projects, thereby further increasing the value of a firm.

2) Optimal capital structure is the capital structure at which the weighted average cost of capital is

minimized, thereby maximizing a firm’s value.

3) An increase in fixed operating and financial cost results in an increase in risk, since the firm will have

to achieve a higher level of sales just to break even.

4) The cost of equity is greater than the cost of debt and increases with increasing financial leverage, but

generally less rapidly than the cost of debt.

5) The cost of equity increases with increasing financial leverage in order to compensate the stockholders

for the higher degree of financial risk.

6) As financial leverage increases, the cost of debt initially remains constant and then rises, while the cost

of equity always rises.

7) If we assume that EBIT is constant, the value of a firm is maximized by minimizing the weighted

average cost of capital.

8) In theory, a firm’s optimal capital structure is that which minimized the firm’s overall cost of capital

resulting in a maximization of the market value of a firm.

9) The overriding objective of the capital structure decision should be to choose the level of debt that

results in the largest possible share price.

10) The optimal capital structure is the one that balances ________.

A) return and risk factors in order to maximize profits

B) return and risk factors in order to maximize earnings per share

C) return and risk factors in order to maximize market value

D) return and risk factors in order to maximize dividends

11) Beginning with a zero-leverage company, as debt is substituted for equity in the capital structure

________.

A) the overall cost of capital first rises, reaches a maximum, and then declines

B) the overall cost of capital declines

C) the overall cost of capital first declines, reaches a minimum, and then rises

D) the overall cost of capital rises

12) Poor capital structure decisions can result in ________ the cost of capital, resulting in ________

acceptable investments.

A) increasing; fewer

B) decreasing; more

C) increasing; more

D) decreasing; fewer

13) According to the traditional approach to capital structure, the value of a firm will be maximized when

________.

A) the financial leverage is maximized

B) the cost of debt is minimized

C) the weighted average cost of capital is minimized

D) the dividend payout is maximized

14) In the traditional approach to capital structure, as the amount of debt increases in a firm’s capital

structure, ________.

A) the cost of equity rises faster than the cost of debt

B) the cost of debt rises faster than the cost of equity

C) debt becomes less risky

D) equity cost is unaffected

15) The value of a firm at optimum capital structure is computed as ________.

A) earnings before interest and taxes times one less tax rate divided by one plus weighted average cost of

capital

B) earnings before interest and taxes times one less tax rate divided by weighted average cost of capital

C) operating cash flow divided by weighted average cost of capital

D) operating cash flow divided by one plus weighted average cost of capital

16) A firm has an operating profit of $300,000, interest of $35,000, and a tax rate of 40 percent. The firm

has an after-tax cost of debt of 5 percent and a cost of equity of 15 percent. The firm’s target capital

structure is set at a mix of 40 percent debt and 60 percent equity. Assuming this as the optimum capital

structure, the value of the firm is ________.

A) $1.4 million

B) $2.2 million

C) $1.8 million

D) $6.0 million

17) A firm is analyzing two possible capital structures—30 and 50 percent debt ratios. The firm has total

assets of $5,000,000 and common stock valued at $50 per share. The firm has a marginal tax rate of 40

percent on ordinary income. The number of common shares outstanding for each of the capital structures

would be ________.

A) 30 percent debt ratio: 30,000 shares and 50 percent debt ratio: 50,000 shares

B) 30 percent debt ratio: 50,000 shares and 50 percent debt ratio: 70,000 shares

C) 30 percent debt ratio: 70,000 shares and 50 percent debt ratio: 100,000 shares

D) 30 percent debt ratio: 70,000 shares and 50 percent debt ratio: 50,000 shares

18) A firm is analyzing two possible capital structures—30 and 50 percent debt ratios. The firm has total

assets of $5,000,000 and common stock valued at $50 per share. The firm has a marginal tax rate of 40

percent on ordinary income. If the interest rate on debt is 7 percent and 9 percent for the 30 percent and

the 50 percent debt ratios, respectively, the amount of interest on the debt under each of the capital

structures being considered would be ________.

A) 30 percent debt ratio: $105,000 and 50 percent debt ratio: $225,000

B) 30 percent debt ratio: $245,000 and 50 percent debt ratio: $225,000

C) 30 percent debt ratio: $105,000 and 50 percent debt ratio: $250,000

D) 30 percent debt ratio: $135,000 and 50 percent debt ratio: $175,000

19) Firms having stable and predictable revenues can more safely employ highly leveraged capital

structures than can firms with volatile patterns of sales revenue.

20) Harry Trading Company must choose its optimal capital structure. Currently, the firm has a 20

percent debt ratio and the firm expects to generate a dividend next year of $5.44 per share. Dividends are

expected to remain at this level indefinitely. Stockholders currently require a 12.1 percent return on their

investment. Harry is considering changing its capital structure if it would benefit shareholders. The firm

estimates that if it increases the debt ratio to 30 percent, it will increase its expected dividend to $5.82 per

share. Again, dividends are expected to remain at this new level indefinitely. However, because of the

added risk, the required return demanded by stockholders will increase to 12.6 percent. Based on this

information, should Harry make the change?

A) Yes, since the value of the firm will increase by $1.23 per share.

B) No, since the value of the firm will decrease by $1.23 per share.

C) Yes, since the value of the firm will increase by $0.25 per share.

D) No, since the value of the firm will decrease by $0.25 per share.

21) The reason why maximizing share value and maximizing EPS do not give the same optimal capital

structure is because ________.

A) EPS maximization does not consider risk

B) share value maximization does not consider risk

C) EPS maximization considers cash flows

D) EPS maximization does consider risk

22) Tangshan Mining Company must choose its optimal capital structure. Currently, the firm has a 40

percent debt ratio and the firm expects to generate a dividend next year of $4.89 per share and dividends

are expected to grow at a constant rate of 5 percent for the foreseeable future. Stockholders currently

require a 10.89 percent return on their investment. Tangshan Mining is considering changing its capital

structure if it would benefit shareholders. The firm estimates that if it increases the debt ratio to 50

percent, it will increase its expected dividend to $5.24 per share. Because of the additional leverage,

dividend growth is expected to increase to 6 percent and this growth will be sustained indefinitely.

However, because of the added risk, the required return demanded by stockholders will increase to 11.34

percent.

(a) What is the value per share for Tangshan Mining under the current capital structure?

(b) What is the value per share for Tangshan Mining under the proposed capital structure?

(c) Should Tangshan Mining make the capital structure change? Explain.