106. The CAPM provides a model of determining expected security returns that is:

107. How can you measure and interpret the market risk, or beta, of a security?

108. What is the relationship between the market risk of a security and the rate of return that

investors demand of that security?

109. How can a manager calculate the opportunity cost of capital for a project?

110. How are the terms “defensive” and “aggressive” applied to individual stocks or

portfolios?

111. Discuss how betas are measured for individual stocks.

112. Why is beta thought to be a more relevant measure of risk than standard deviation for a

diversified investor?

113. Discuss the capital asset pricing model in general, the CAPM method of determining

expected returns, and how the SML can be used to help predict the movement of a stock’s price.

114. The stock of Newmont Mining, the world’s largest gold producer, has above-average

volatility but a relatively low beta. Why?

115. Calculate the expected rate of return for the following portfolio, based on a Treasury bill

yield of 4% and an expected market return of 13%: (Show your work)

116. A portfolio of three stocks with total market value of $1,000,000 currently has a beta of

1.4. In light of an expected market downturn, you wish to reduce the portfolio beta to no more

than 1.0. Two stocks are likely candidates for sale, one with a beta of 1.8 and a market value of

$200,000 and the other with a beta of 1.5 and a market value of $250,000. Assuming that you

could find one appropriate stock to replace these two, what should be its beta? (Show your

work)

117. Stock A has a current price of $25, a beta of 1.25, and a dividend yield of 6%. If the

Treasury bill yield is 5% and the market portfolio is expected to return 14%, what should stock A

sell for at the end of an investor’s 2-year investment horizon?

118. Why is it important to make the distinction between company opportunity cost of capital

and project opportunity cost of capital when evaluating projects?

119. Where will the following projects plot in relation to the security market line if the risk-free

rate is 6% and the market risk premium is 9%? Which projects should be undertaken?

120. The manager of Star Performer Mutual Fund expects the fund to earn a rate of return of

12% this year. The beta of the fund’s portfolio is 0.8. If the rate of return available on risk-free

assets is 5% and you expect the rate of return on the market portfolio to be 15%, should you

invest in Star Performer? Can you create a portfolio with the same risk as Star Performer Mutual

Fund, but with a higher expected rate of return? Explain why in reality, a mutual fund must be

able to provide an expected rate of return that is higher than that predicted by the security

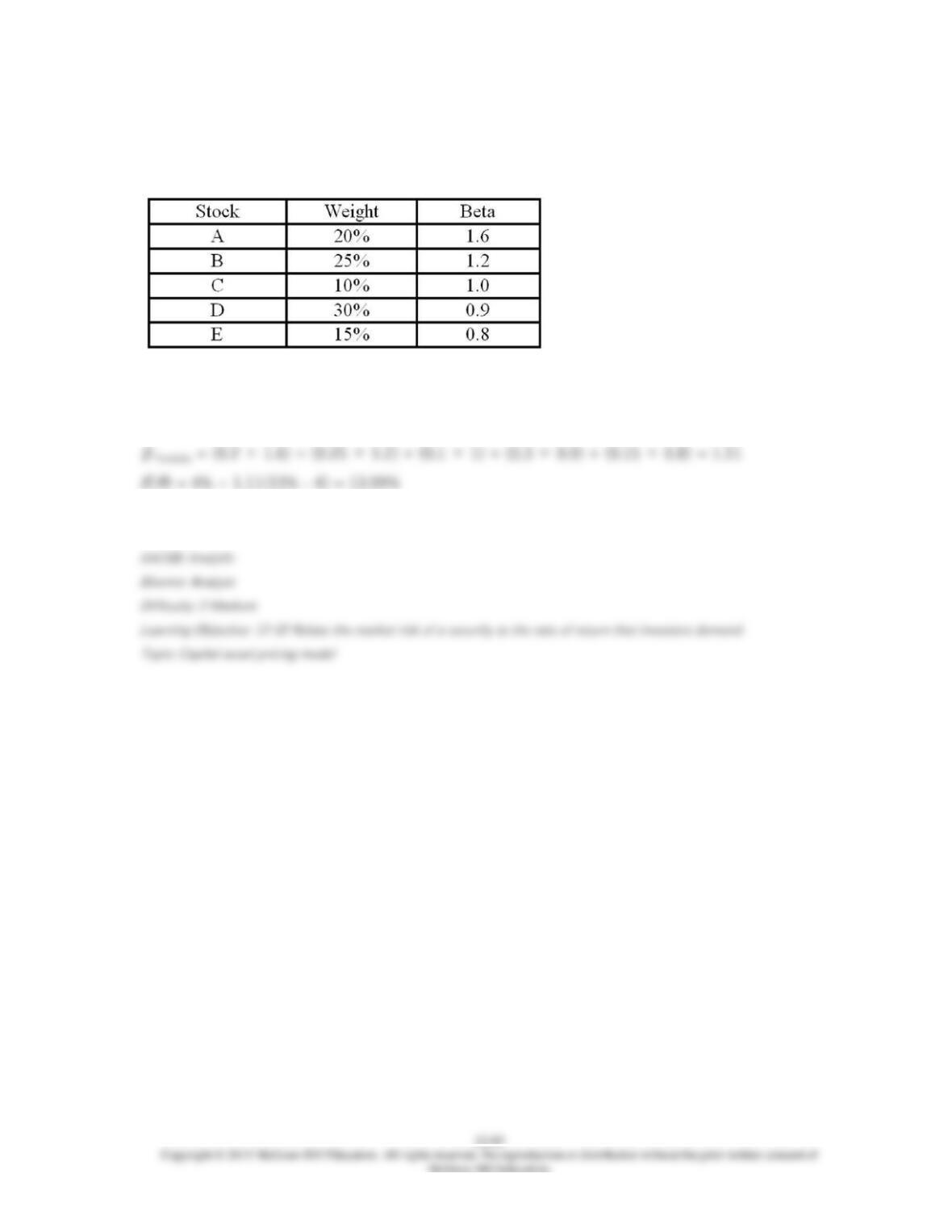

market line in order for investors to consider the fund an attractive investment opportunity.