Achievement Test 11: Chapters 21–22 Name __________________________

Accounting, 5e Instructor _______________________

Section # _______ Date _________

Part

I

II

III

IV

Total

Points

26

32

22

20

100

Score

PART I — MULTIPLE CHOICE (26 points)

Instructions: Designate the best answer for each of the following questions.

____ 1. Office Stuff produced 15,000 file cabinets at a cost of $80,000. Production for the

period was estimated at 14,000 file cabinets at a cost of $75,000. On which of the

following should the flexible budget be based?

a. Budgeted costs of actual production

b. Budgeted costs of budgeted production

c. Actual costs of budgeted production

d. Actual costs of actual production

____ 2. Which of the following is true with regard to budgeting vs. long-range planning?

a. Both tend to be very detailed.

b. They are the same in all significant aspects.

c. The maximum length for both usually is a year, with shorter periods of time also

common.

d. Budgeting is oriented more toward short-term goals; long-range planning toward

long–term goals.

____ 3. Which of the following is false with regard to budgetary planning?

a. The starting point for the budgets of a not-for-profit organization is generally

receipts, rather than expenditures.

b. A merchandising company uses a purchases budget instead of a production

budget.

c. Budgets may be used by manufacturing companies, merchandising companies,

service enterprises, and not–for-profit organizations.

d. For a service enterprise, the critical factor in budgeting is coordinating professional

staff needs with anticipated services.

____ 4. The manager of an investment center can improve ROI by

a. reducing variable and/or controllable fixed costs.

b. reducing average operating assets.

c. increasing sales.

d. all of the above.

Test Bank for Accounting, Fifth Edition

AT11- 2

____ 5. Which of the following is true with regard to budgetary planning?

a. Generally accepted accounting principles require the budgets be prepared at least

annually.

b. The cash budget is often considered to be the most important output in preparing

financial budgets.

c. The likelihood of a realistic budget is greater when the budget is developed from

top management down to lower management.

d. The human behavior aspects of budgeting, while they should not be ignored, are

generally of little real significance.

____ 6. A static budget is

a. applicable to cost budgets but not to a sales budget.

b. modified or adjusted for changes in activity during the year.

c. appropriate in evaluating a manager’s effectiveness in controlling fixed costs.

d. appropriate in evaluating a manager’s effectiveness in controlling variable costs.

____ 7. When considering controllable versus noncontrollable costs,

a. costs allocated to, and thus identifiable with, a particular responsibility level are

controllable.

b. costs incurred directly by a level of responsibility are controllable at that level.

c. controllable cost and noncontrollable cost, respectively, are synonymous with

variable cost and fixed cost.

d. more costs are controllable as one moves down to the lower levels where actual

production takes place.

____ 8. A responsibility report for a profit center shows

a. gross profit and income from operations.

b. contribution margin and controllable margin.

c. contribution margin, controllable margin, and return on investment.

d. gross profit, income from operations, and net income.

____ 9. A flexible budget

a. is, in essence, a series of static budgets at different levels of activity.

b. can be prepared for each of the types of budgets included in a master budget.

c. increases budget allowances both directly and proportionately for variable costs as

production increases.

d. all of the above.

____ 10. Responsibility centers are generally classified as either

a. divisions, departments, or branches.

b. segments, subunits, or subdivisions.

c. cost centers, profit centers, or divisions.

d. cost centers, profit centers, or investment centers.

____ 11. The initial budget prepared in the master budget is the

a. sales budget.

b. production budget.

c. budgeted balance sheet.

d. budgeted income statement.

Achievement Test 11

AT11- 3

____ 12. The ROI formula for an investment center is

a. Controllable Margin ÷ Sales.

b. Net Income ÷ Average Operating Assets.

c. Contribution Margin ÷ Average Operating Assets.

d. Controllable Margin ÷ Average Operating Assets.

____ 13. The Florida Division of Right Enterprises had an ROI of 18% when sales were

$1,500,000 and controllable margin was $118,800. What were the average operating

assets?

a. $270,000

b. $21,384

c. $291,384

d. $660,000

PART II — BUDGETARY PLANNING (32 points)

This problem consists of four independent mini-problems. Omit headings other than those already

given.

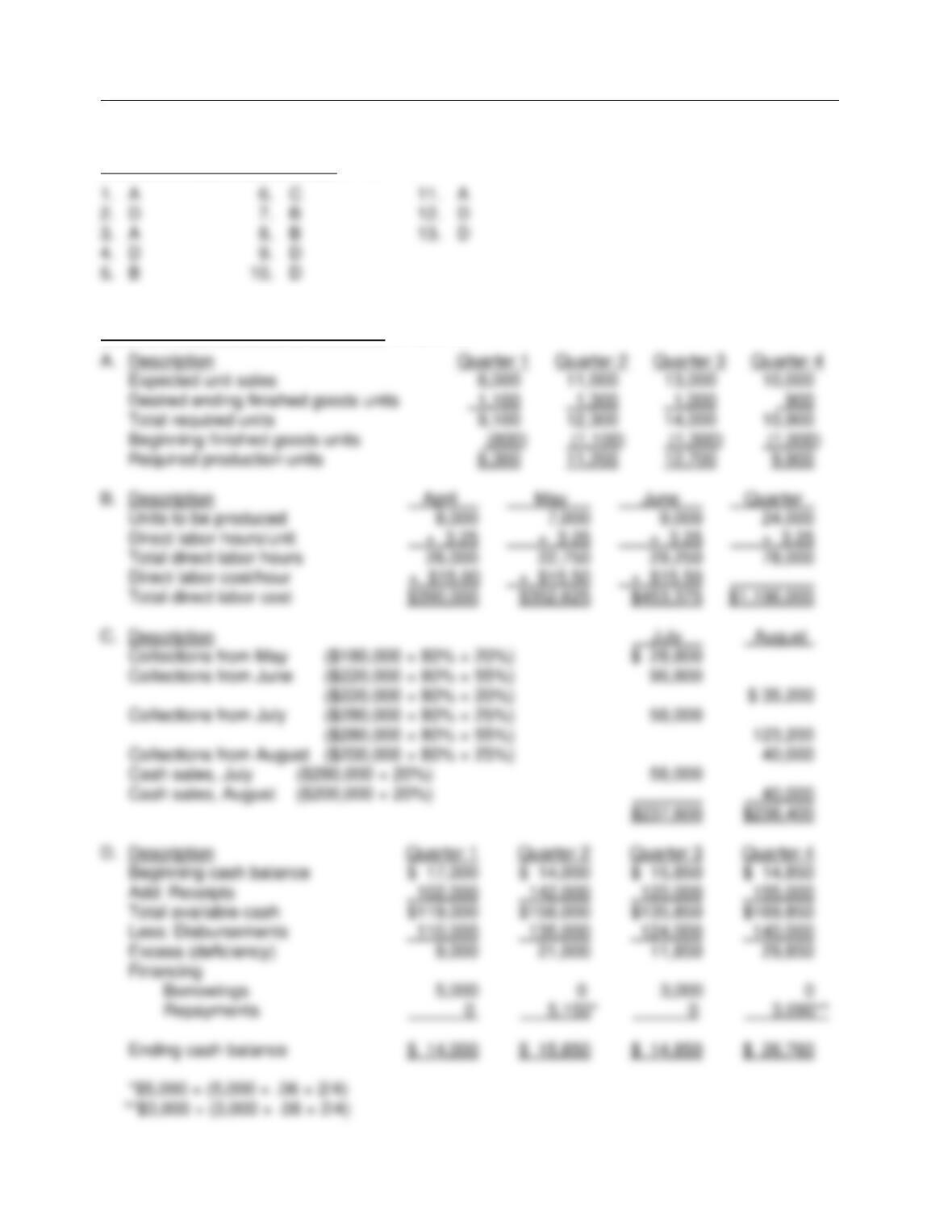

A. Kriter Kitchen Tools produces and sells insulated ice buckets. The sales budget for 2014 is as

follows:

1st quarter — 8,000 units 3rd quarter — 13,000 units

2nd quarter — 11,000 units 4th quarter — 10,000 units

Kriter desires an ending inventory equal to 10% of the next quarter’s sales. The January 1,

2014 inventory is 800 units. Unit sales during the 1st quarter of 2015 are estimated at 9,000

units.

Instructions: Compute required production for 2014, showing quarterly data.

Description Quarter 1 Quarter 2 Quarter 3 Quarter 4

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

Test Bank for Accounting, Fifth Edition

AT11- 4

B. Shanigan’s Manufacturers is preparing its direct labor budget for the second quarter of 2014

from the following budgeted production figures: April—8,000 units; May—7,000 units; and

June—9,000 units. Each unit requires 3.25 hour of direct labor. The hourly wage rates are

expected to be $15 in April, and $15.50 in May and June.

Instructions: Prepare a direct labor budget for the quarter, showing monthly data.

Description April May June Quarter

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

C. JetGreen Cleaners makes 80% of its sales on credit. Experience shows that 25% of the credit

customers pay in the month of sale, 55% within the following month, the rest during the next

month. Total sales for May, June, July, and August are estimated at $180,000; $220,000;

$280,000; and $200,000, respectively.

Instructions: Determine budgeted cash receipts for July and August.

Description July August

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

Achievement Test 11

AT11- 5

D. Southside Sports is preparing its annual cash budget, showing quarterly data, for 2014. A

$14,000 cash balance is desired at the end of each quarter. Borrowings and repayments are

in $1,000 increments at 6% annual interest. The company borrows at the beginning of a

quarter based on the estimated deficiency. Interest is paid only when principal is repaid at the

end of a quarter with excess cash. The maximum amount of principal was repaid in the

second and fourth quarters. The cash balance on December 31, 2013 is $17,000. Total

receipts and disbursements, other than borrowings and principal or interest payments, are

estimated at:

Quarter 1 Quarter 2 Quarter 3 Quarter 4

Disbursements: $110,000 $135,000 $124,000 $140,000

Receipts: 102,000 142,000 120,000 155,000

Instructions: Prepare a schedule of estimated borrowings and repayments of principal and

interest for the four quarters of 2014.

Description Quarter 1 Quarter 2 Quarter 3 Quarter 4

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

Test Bank for Accounting, Fifth Edition

AT11- 6

PART III — FLEXIBLE BUDGETS (22 points)

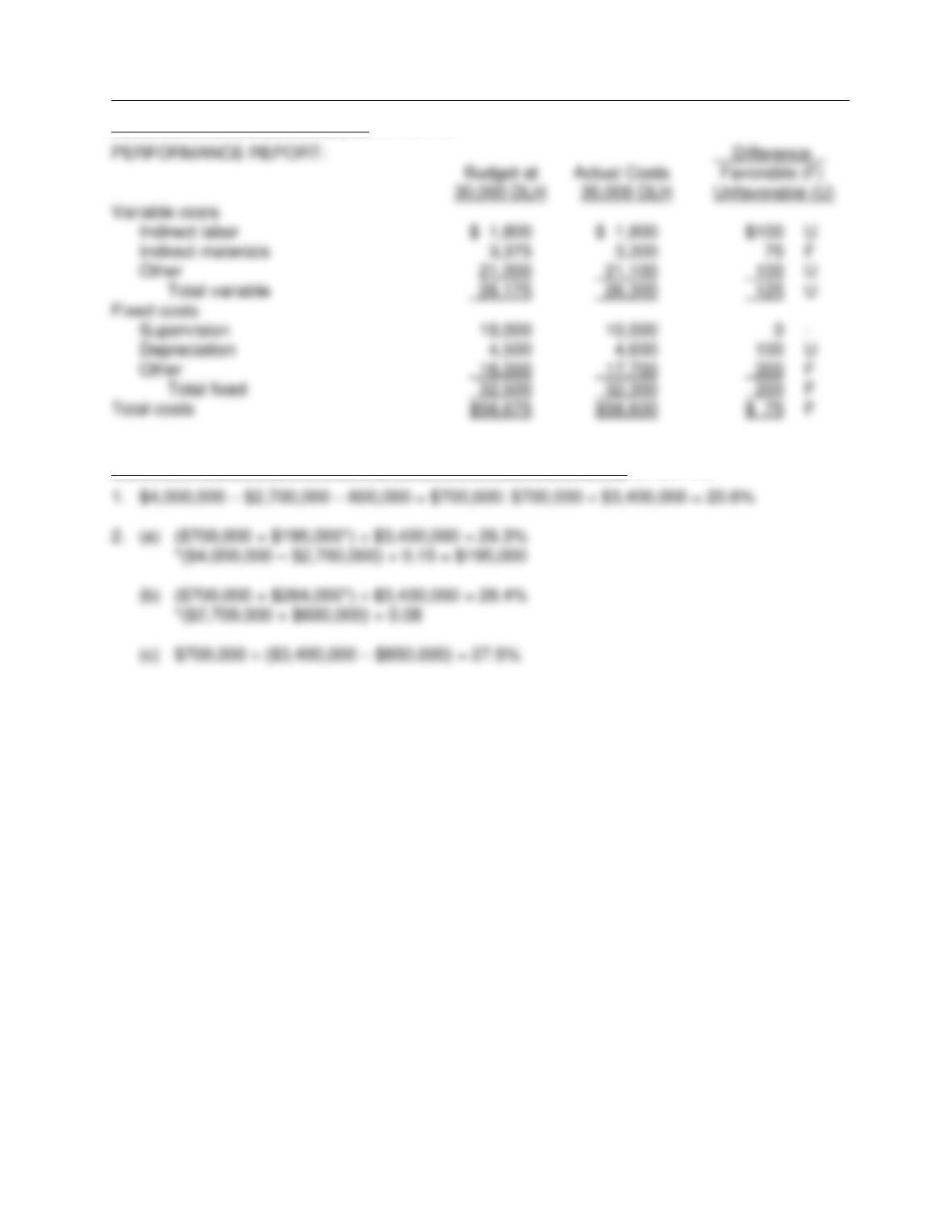

Handover Company uses a flexible budget for overhead based on direct labor hours (DLH).

Annual master budget figures, based on 400,000 direct labor hours, and actual overhead for

March, when 30,000 labor hours were worked, are as follows:

Master Budget March Actual

Variable:

Indirect labor $ 24,000 $ 1,900

Indirect materials 45,000 3,300

Other 280,000 21,100

Fixed:

Supervision 120,000 10,000

Depreciation 54,000 4,600

Other 216,000 17,700

Instructions: Prepare a flexible budget performance report for March. Omit headings other than

descriptive columnar headings.

FLEXIBLE BUDGET PERFORMANCE REPORT:

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

Achievement Test 11

AT11- 7

PART IV — COMPUTATION OF RETURN ON INVESTMENT (ROI) (20 points)

For the year ended December 31, 2014, SanaDune Tools reports the following:

Sales $4,000,000

Variable costs 2,700,000

Controllable fixed costs 600,000

Average operating assets 3,400,000

Instructions: Compute ROI for each of the following situations. Show all computations.

1. The year ended December 31, 2014.

_________________ ÷ _________________ = ________%

2. For 2015 assuming the following independent courses of action:

(a) Sales will increase 15% with no change in the contribution margin ratio.

_________________ ÷ _________________ = ________%

(b) Variable costs and controllable fixed costs will both be reduced 8%.

_________________ ÷ _________________ = ________%

(c) Average operating assets will be reduced 25%.

_________________ ÷ _________________ = ________%

Test Bank for Accounting, Fifth Edition

AT11- 8

Solutions — Achievement Test 11: Chapters 21–22

PART I — MULTIPLE CHOICE (26 points)

PART II — BUDGETARY PLANNING (32 points)

Achievement Test 11

AT11- 9

PART III — FLEXIBLE BUDGETS (22 points)

PART IV — COMPUTATION OF RETURN ON INVESTMENT (ROI) (20 points)