Chapter 11: Stockholders’ Equity

217. [APPENDIX] Fowler Company opened business as a sole proprietorship on January 1, 2016. The owner contributed

$525,000 cash on that date. During the year, the company had a net income of $20,000. The company purchased

equipment of $120,000 during the year. The owner also withdrew $75,000 to pay for personal expenses during 2016.

Required:

Determine the company’s owner’s equity at December 31, 2016.

ANSWER:

Initial investment

$525,000

Plus: Net income

20,000

Less: Withdrawal

(75,000)

Owner’s equity, December 31, 2016

$470,000

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-11 – LO: 11-11

KEYWORDS:

Bloom’s: Analyzing

218. [APPENDIX] Body Sports is a surf shop owned by Chris, Nicole, and Dan in partnership. On January 1, 2016, their

capital balances were as follows:

Chris, Capital

$30,000

Nicole, Capital

60,000

Dan, Capital

40,000

During 2016, Chris withdrew $10,000; Nicole, $20,000; and Dan, $15,000. Income for the partnership for 2016 was

$75,000.

Required:

If the partners agreed to allocate income equally, what was the ending balance in each of their capital accounts on

December 31, 2016?

ANSWER:

Chris

Nicole

Dan

Beginning balance

$30,000

$60,000

$40,000

Add: Allocation of net

income

25,000*

25,000

25,000

$55,000

$85,000

$65,000

Less: Withdrawals

(10,000)

(20,000)

(15,000)

Ending balance

$45,000

$65,000

$50,000

*$75,000/3 = $25,000

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-11 – LO: 11-11

KEYWORDS:

Bloom’s: Analyzing

219. Stella Gregson received a windfall from one of her investments. She would like to invest $100,000 of the money in

Shoreline Industries, which is offering common stock, preferred stock, and bonds on the open market. The common stock

has paid $8 per share in dividends for the past three years, and the company expects to be able to perform as well in the

current year. The current market price of the common stock is $100 per share. The preferred stock has an 8% dividend

rate, cumulative and nonparticipating. The bonds are selling at par with an 8% stated rate.

Required:

1. What are the advantages and disadvantages of each type of investment?

2. Recommend one type of investment over the others to Stella and justify your reason.

ANSWER:

1. Common stock has ownership privileges. The residual of the company belongs to the

common shareholders. Preferred stock has preference over common stockholders in dividend

payouts. Bonds earn interest that is a legal obligation of the company.

2. The return on the preferred stock depends upon its issue price. If it is assumed that the

stock is issued at par value, the return is 8%. Since all three instruments yield the same rate of

return, 8%, Stella should choose to invest in the bonds because they carry the lowest risk. As

risk increases, the expected rate of return on an investment should increase.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-02 – LO: 11-02

KEYWORDS:

Bloom’s: Applying

220. On May 1, 2016, Xiu Inc. had common stock of $345,000, additional paid-in capital of $1,298,000, and retained

earnings of $3,013,000. Xiu did not purchase or sell any common stock during the year. The company reported net

income of $556,000 and declared dividends in the amount of $78,000 during the year ended April 30, 2017.

Required:

Prepare a financial statement that explains the differences between the beginning and ending balances for the accounts in

the Stockholders’ Equity category of the balance sheet.

ANSWER:

Xiu Inc.

Statement of Stockholder’s Equity

for the Year Ended April 30, 2017

Common

Stock

Add. Pd–in

Cap.

Retained

Earnings

Total

Stockholders’

Equity

Balance May 1,

2016

$345,000

$1,298,000

$3,013,000

$4,656,000

Net Income

556,000

556,000

Dividends

(78,000)

(78,000)

2017

$5,134,000

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-08 – LO: 11-08

221. Assume that Cosmo Company’s Stockholders’ Equity category of the balance sheet appears as follows as of

December 31, 2016:

Common stock, $10 par, 60,000 shares issued and outstanding

$ 600,000

Additional paid-in capital—Common

480,000

Retained earnings

1,240,000

Total stockholders’ equity

$2,320,000

On May 1, 2017, Cosmo declared and issued a 15% stock dividend, when the stock was selling for $20 per share. Then on

November 1, it declared and issued a 2-for-1 stock split.

Required:

1. How many shares of stock are outstanding at year-end?

2. What is the par value per share of these shares?

3. Develop the Stockholders’ Equity category of Cosmo’s balance sheet as of December 31, 2017.

ANSWER:

1. Jan. 1 Balance………..……………………….. 60,000 shares

May 1 60,000 × 15%…………………………. 9,000

69,000

Nov. 1 ……………..…………………………….. × 2

Total shares outstanding………………………. 138,000 shares

2. $10/2 = $5 per share

3. Stockholders’ Equity:

Common stock, $5 par value, 138,000 shares

issued and outstanding……………………….…… $ 690,000

Additional paid-in capital………………………….... 570,000*

Retained earnings [$1,240,000 – (9,000 × $20)].. 1,060,000

Total stockholders’ equity………..…………….. $2,320,000

*9,000 shares × ($20 – $10) = $90,000 from May 1

$90,000 + $480,000 = $570,000

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-07 – LO: 11-07

KEYWORDS:

Bloom’s: Analyzing

222. Falcon Company has 1,000 shares of $100 par value, 9% preferred stock and 10,000 shares of $10 par value common

stock outstanding. The preferred stock is cumulative and nonparticipating. Dividends were paid in 2014. Since 2014,

Falcon has declared and paid dividends as follows:

2015

$ 0

2016

10,000

2017

20,000

2018

25,000

Required:

1. Determine the amount of the dividends to be allocated to preferred and common stockholders for each year 2016 to

2018.

2. If the preferred stock had been noncumulative, how much would have been allocated to the preferred and common

stockholders each year?

ANSWER:

1. Preferred Dividends per Year = 1,000 × $100 × 9% = $9,000

Year Preferred Dividends Common Dividends

2015 $ 0 $ 0

2016 10,000* 0

2017 17,000** 3,000

2018 9,000 16,000

*$9,000 (from 2015) + $1,000 (for 2016) = $10,000.

**$8,000 (from 2016) + $9,000 (for 2017) = $17,000.

2. Year Preferred Dividends Common Dividends

2015 $ 0 $ 0

2016 9,000 1,000

2017 9,000 11,000

2018 9,000 16,000

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-05 – LO: 11-05

KEYWORDS:

Bloom’s: Analyzing

223. At December 31, 2016, Forgione Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 8,000 issued, 7,000 outstanding

Preferred Stock, $100 par, 7%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

Required:

1. Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if the company

declared a dividend of $50,000.

2. How many shares of treasury stock does Forgione have?

3. What are the dividends per share of common stock as a result of this distribution?

4. What are the dividends per share of Preferred stock as a result of this distribution?

ANSWER:

1. Preferred dividend in arrears ($100,000 × 7% × 2 years) $14,000

Preferred dividend for current year ($100,000 × 7%)…… 7,000

Total………………..……………………………………………….. $21,000

Common stock ($50,000 – $21,000 = $29,000)

2. 8,000 – 7,000 = 1,000 shares of treasury stock

3. $29,000 / 7,000 = $4.14 / share of common stock

4. $21,000 / 1,000 = $21 / share of preferred stock (including cumulative

amounts)

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-05 – LO: 11-05

KEYWORDS:

Bloom’s: Analyzing

224. At December 31, 2016, Marley Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Required:

Indicate whether the following would increase, decrease, or have no effect on (a) assets, (b) retained earnings, and (c) total

stockholders’ equity.

1. A company declares and pays a cash dividend of $25,000.

2. A company declares and issues a 10% stock dividend.

ANSWER:

1. Decrease assets

Decrease retained earnings

Decrease total stockholders’ equity

2. No change in assets

Decrease retained earnings

No change in total stockholders’ equity

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-06 – LO: 11-06

KEYWORDS:

Bloom’s: Analyzing

225. At December 31, 2016, North Company and South Company have identical amounts of common stock and retained

earnings as follows:

Common Stock, $10 par, 50,000 shares authorized, 9,000 issued, 9,000 outstanding

Retained Earnings, $500,000

At December 31, 2016, North Company declares and issues a 100% stock dividend, while South Company declares and

issues a 2-for-1 stock split.

Required:

Determine for each company the following amounts as of January 1, 2017:

_______ Number of shares of common stock outstanding

_______ Par value per share of the common stock

_______ Total amount reported in Common Stock account

_______ Retained earnings

ANSWER:

North Company:

Number of shares outstanding

18,000

Par value per share

$10

Common Stock account

$180,000

Retained earnings

$410,000

South Company:

Number of shares outstanding

18,000

Par value per share

$5

Common Stock account

$90,000

Retained earnings

$500,000

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-07 – LO: 11-07

KEYWORDS:

Bloom’s: Analyzing

226. At December 31, 2016, Corning Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

Required:

Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if the company

declared a dividend of $24,000.

ANSWER:

Preferred dividend in arrears ($100,000 × 8% × 2 years)…….. $16,000

Preferred dividend for current year ($100,000 × 8%)…. 8,000

Total………………………………………………………..… $24,000

Common stock (0)

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-05 – LO: 11-05

227. At December 31, 2016, Corning Company has the following:

Common Stock, $10 par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, 1,000 shares authorized, issued, and outstanding

The company did not pay any dividend during 2015 or 2014.

Required:

Compute the amount of dividend to be received by the common and preferred stockholders in 2016 if the company

declared a dividend of $60,000.

ANSWER:

Preferred dividend in arrears ($100,000 × 8% × 2 years)…… $16,000

Preferred dividend for current year ($100,000 × 8%).. 8,000

Total……………………………………………………….... $24,000

Common stock ($60,000 – $24,000 = $36,000)

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-05 – LO: 11-05

KEYWORDS:

Bloom’s: Analyzing

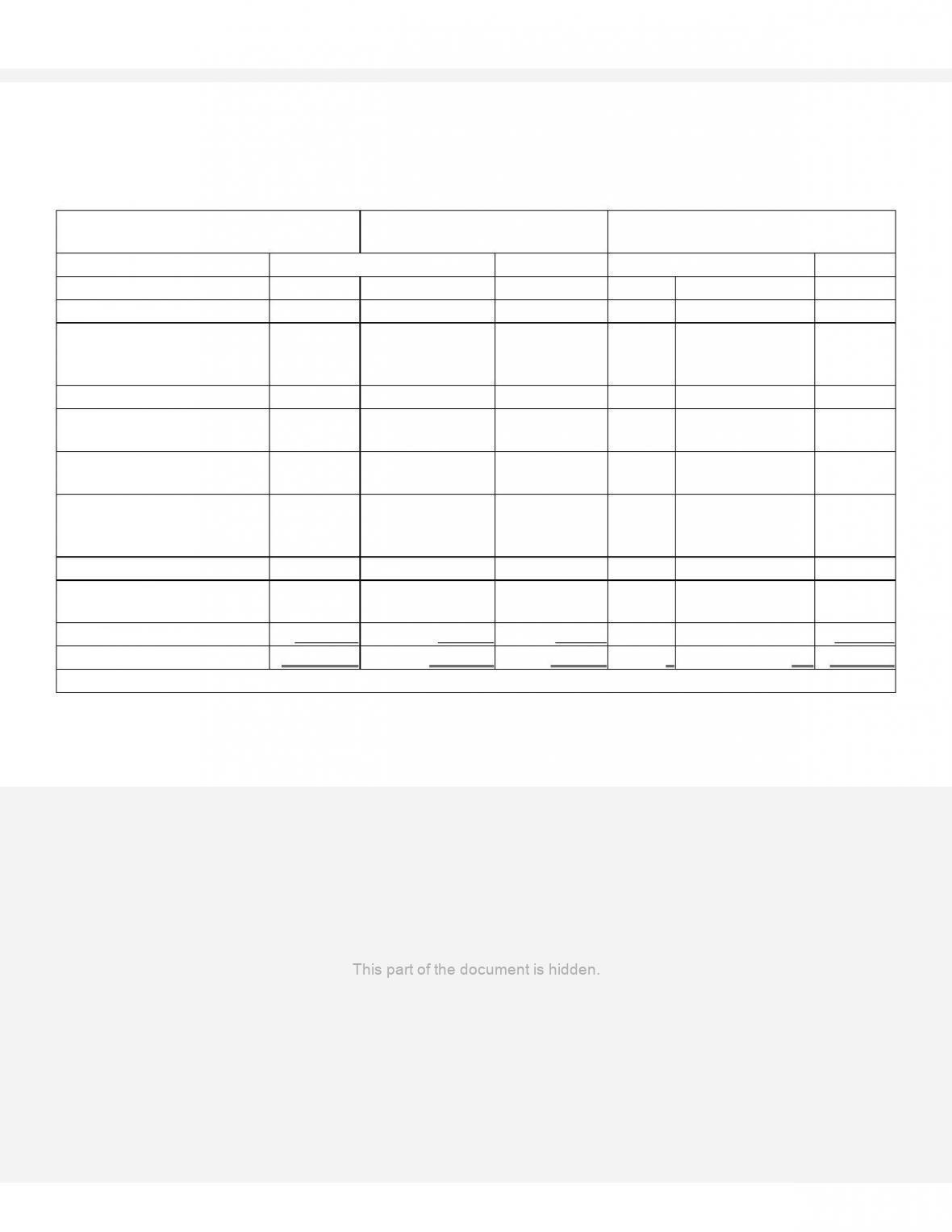

228. Use the comparative financial statements of Penny Company for the year ended December 31, 2016 to answer the

following question(s).

Penny Company

Statement of Stockholder’s Equity

for the Year Ended December 31, 2016

in thousands, except share data

Common Stock

Retained

Treasury Stock

Shares

Amount

Earnings

Shares

Amount

Total

Balance, Jan. 1, 2016

57,936,988

$ 89,861

$20,037

$109,898

Exercise of stock options

including tax benefit of

$4,754

945,780

7,911

7,911

Sale of common stock

12,050,000

163,873

163,873

Stock subscription notes

repayments

3,671

3,671

Conversion of convertible

debentures, net

6,798

100

100

Sale of common stock under

employee stock purchase

plan

17,424

263

263

Net earnings

26,102

26,102

Unrealized holding gains,

net

141

141

Translation adjustment

272

272

Balance Dec. 31, 2016

70,956,990

$265,679

$46,552

0

$ 0

$312,231

See notes to consolidated financial statements.

Required:

Prepare a statement of retained earnings for the year ended December 31, 2016.

ANSWER:

Penny Company

Statement of Retained Earnings

for the Year Ended December 31, 2016

(in thousands)

Beginning retained earnings, January 1, 2016

$20,037

Net earnings

26,102

Ending retained earnings, December 31, 2016

$46,139

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-08 – LO: 11-08

KEYWORDS:

Bloom’s: Analyzing

234. Explain the difference between authorized, issued, and outstanding shares.

ANSWER:

The corporation charter specifies a number of shares that are said to be authorized. This is the

maximum number of shares that can be issued. If the corporation wishes to issue shares in

excess of this number, the charter must be amended. Issued shares are those which have been

sold or transferred to stockholders. Outstanding shares are those which have been issued and

are still in the hands of stockholders.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-01 – LO: 11-01

KEYWORDS:

Bloom’s: Applying

235. What is the difference between par value and market value? Which is the better indicator of the true worth of the

stock?

ANSWER:

Par value is an arbitrary amount stated on the face of the stock certificate and is needed to

satisfy legal requirements. Market value is the amount that each share of stock is selling for

on the market. Market value is the better indicator since par value is chosen only to establish

a minimum legal liability.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-01 – LO: 11-01

FACC.PONO.13.11-09 – LO: 11-09

KEYWORDS:

Bloom’s: Applying

236. What is meant by the balance in the retained earnings account?

ANSWER:

Retained earnings represents the net income that the firm has earned but not paid out as

dividends. It is accumulated over the life of the corporation.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-01 – LO: 11-01

KEYWORDS:

Bloom’s: Applying

237. What is substance over form and how does this concept relate to the presentation of preferred stock?

ANSWER:

Substance over form means that a company must look not only at the legal form but also at

the economic substance of the security to decide whether it is debt or equity. When preferred

stock carries certain provisions, the stock is very similar to bonds and notes payable. Using

this concept, management must evaluate whether such securities represent debt and should be

presented in the Liability category of the balance sheet or whether they represent equity and

should be presented in the Equity category.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-02 – LO: 11-02

KEYWORDS:

Bloom’s: Applying

238. Explain the two ways that a dividend rate on preferred stock may be stated by giving examples.

ANSWER:

The examples in student answers may vary but can include something similar to the

following:

1. It may be stated as a percentage of the stock’s par value. For example, if a stock is

presented on the balance sheet as $100 par, 7% preferred stock, its dividend rate is $7 per

share ($100 × 7%).

2. The dividend may be stated as a per-share amount. For example, a stock may appear on the

balance sheet as $100 par, $7 preferred stock, meaning that the dividend rate is $7 per share.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-02 – LO: 11-02

KEYWORDS:

Bloom’s: Applying

239. Gemini Company has the following accounts in the Stockholders’ Equity category of the balance sheet:

Common Stock, $10 no par, 10,000 shares authorized, 9,000 issued, 8,000 outstanding

Preferred Stock, $100 par, 8%, cumulative, participating, 1,000 shares authorized, issued, and outstanding

Required:

1. Explain how the issuance of stock affects the financial statements when the stock has no par value.

2. Why would preferred stockholders want to have a cumulative feature in preferred stock?

3. When a participating feature is present in preferred stock, how does it affect the amount of dividends that preferred

stockholders can expect to receive?

ANSWER:

1. When no par stock is issued, the entire amount of the issuance is in the stock account.

There is no distinction between the stock amount and the additional paid-in capital amount.

2. The cumulative feature gives the stockholders some assurance that a dividend will

eventually be received. If the dividends on preferred stock are cumulative, then the dividends

that are not paid are considered to be in arrears. Before a dividend on common stock can be

declared in a subsequent period, the dividends in arrears as well as the current year’s

dividend must be paid to the preferred stockholders.

3. If a participating feature is present in preferred stock, then it allows the preferred

stockholders to receive a dividend in excess of the regular rate when the firm has been

particularly profitable and declares an abnormally large dividend.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-02 – LO: 11-02

KEYWORDS:

Bloom’s: Applying

240. Name two different examples of items that can be received (in addition to cash) in exchange for issuing stock.

Describe how the value of each item affects additional paid-in capital.

ANSWER:

Some examples are land, a machine, equipment, or a building. The best indicator of the value

DIFFICULTY:

Moderate

KEYWORDS:

Bloom’s: Applying

241. Chad Darrow, CFO of your company is considering constructing a deal with Extreme Industries, whereby stock is

issued in exchange for an asset (custom extrusion equipment valued at $400,000 by an outside appraiser). The stock to be

exchanged is a new class of preferred stock that has not yet been traded in the open market. He has asked that you draft a

memo to Marc Lyon, CEO about the valuation of the asset to be used in the exchange. In your memo address the reporting

amount for the asset and how fair market value could be determined.

ANSWER:

INTERNAL MEMORANDUM

TO: Marc Lyon, CEO

FROM: Chad Darrow, CFO

I have determined that the best way to construct the deal with Extreme Industries is by

issuing our stock in exchange for the custom extrusion equipment. The asset should be

recorded at the fair market value of the consideration given (the stock) or the fair market

value of the consideration received (the asset), whichever is more readily determinable. Fair

market value may be determined by reference to sales of the stock on the stock exchange or,

in some cases, by an appraisal of the asset. In this case, since the new class of preferred stock

does not have a readily determinable market value, we will be recording the custom extrusion

equipment at $400,000, which was the value determined by an independent appraiser.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-03 – LO: 11-03

KEYWORDS:

Bloom’s: Applying

242. What is treasury stock? How is it reported on the financial statements?

ANSWER:

Treasury stock is issued stock that is repurchased by a company. It is reported as a deduction

from total stockholders’ equity on the balance sheet.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-04 – LO: 11-04

KEYWORDS:

Bloom’s: Applying

243. a. Explain what the dividend payout ratio is and which firms typically have a high ratio and which firms may have

the lowest.

b. Many firms operate at a dividend payout ratio of less than 50%. Why do many firms not pay a larger percentage of

income as dividends?

ANSWER:

a. The dividend payout ratio is calculated as the annual dividend amount divided by the

annual net income. Typically, utilities pay a high proportion of their earnings as dividends. In

contrast, fast-growing companies in technology often pay nothing to stockholders.

b. Many firms do not pay out all of their income as dividends because there are other

alternative uses of the income. Management’s objective should be to maximize the wealth of

the stockholders. Sometimes that can be achieved by paying dividends; other times it can be

achieved by retaining the income and reinvesting it in alternatives such as purchasing

replacement fixed assets or equipment which could be vital to the continuing operations of

the company.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-05 – LO: 11-05

KEYWORDS:

Bloom’s: Applying

244. Contrast stock dividends and stock splits.

ANSWER:

Stock dividends involve the issuance of additional shares of stock. The dividend normally

reflects the fair market value of the additional shares. A stock split is similar to a stock

dividend except that stock splits reduce the par value per share of the stock. No accounting

transaction is necessary for a stock split.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-06 – LO: 11-06

FACC.PONO.13.11-07 – LO: 11-07

KEYWORDS:

Bloom’s: Applying

245. What is comprehensive income and what is contained in a statement of comprehensive income?

ANSWER:

Comprehensive income is the total change in net assets from all sources except investments

by or distributions to the owners. These include “income–type” items that escape the income

statement. In other words, the statement of comprehensive income includes all of the

revenues and expenses that are presented on the income statement to calculate net income

and includes items that are not presented on the income statement but that affect total

stockholders’ equity. For example, these include transactions such as unrealized gains that

affect stockholders’ equity.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-08 – LO: 11-08

KEYWORDS:

Bloom’s: Applying

246. What is the difference between book value and market value of stock?

ANSWER:

Market value is the amount that each share of stock is selling for on the market. Market value

is the best indicator of true value since par value is chosen only to establish a minimum legal

liability. Book value is calculated as net assets divided by the number of shares of common

stock outstanding. It indicates the rights that stockholders have, based on recorded values, to

the net assets in the event of liquidation. It is therefore not a measure of the market value of

the stock.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-09 – LO: 11-09

KEYWORDS:

Bloom’s: Applying

247. What section of the statement of cash flows is related to the Stockholders’ Equity section of the balance sheet? Name

four different transactions that are reported in that section that relate to the statement of cash flows.

ANSWER:

The section of the statement of cash flows that is related to the statement of stockholders’

equity is the Financing Activities section. Some transactions are: payments of dividends, sale

of common or preferred stock for cash, cash paid for the retirement of stock, sale of treasury

stock, and purchase of treasury stock.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-10 – LO: 11-10

KEYWORDS:

Bloom’s: Applying

248. [APPENDIX] Explain the differences between a partnership and sole proprietorship. Include in your discussion

whether either is considered a separate legal entity.

ANSWER:

A partnership is a company owned by two or more persons. A proprietorship is owned by

only one person. Neither is considered a separate legal entity.

DIFFICULTY:

Moderate

LEARNING OBJECTIVES:

FACC.PONO.13.11-11 – LO: 11-11

KEYWORDS:

Bloom’s: Applying

249. [APPENDIX] What are the advantages of organizing a company as a corporation instead of a partnership or sole

proprietorship?

ANSWER:

Sole proprietorships and partnerships are not considered separate entities for legal or tax

purposes. Owners of corporations are not liable for debts of the corporation, whereas owners

of sole proprietorships and partnerships are. The owners of sole proprietorships and

partnerships pay their individual share of the business’s income taxes, while stockholders of

corporations do not. This may or may not be an advantage.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-11 – LO: 11-11

KEYWORDS:

Bloom’s: Applying

250. [APPENDIX] Which accounts are used by a sole proprietorship that are not used by a corporation?

ANSWER:

A sole proprietorship uses a capital account instead of the common stock, additional paid-in

capital, and retained earnings accounts, which are used by corporations. It also utilizes a

withdrawals account instead of a dividends account.

DIFFICULTY:

Easy

LEARNING OBJECTIVES:

FACC.PONO.13.11-11 – LO: 11-11

KEYWORDS:

Bloom’s: Applying