16) Assuming that Tom wants to maintain the current expected return on his portfolio, then the amount

that Tom should invest in the market portfolio to minimize his volatility is closest to:

A) 100%

B) 90%

C) 125%

D) 110%

17) Assuming that Tom wants to maintain the current expected return on his portfolio, then the

minimum volatility that Tom could achieve by investing in the market portfolio and risk-free

investment is closest to:

A) 20%

B) 25%

C) 22%

D) 18%

18) You currently own $100,000 worth of Wal-Mart stock. Suppose that Wal-Mart has an expected

return of 14% and a volatility of 23%. The market portfolio has an expected return of 12% and a

volatility of 16%. The risk-free rate is 5%. Assuming the CAPM assumptions hold, what alternative

investment has the lowest possible volatility while having the same expected return as Wal-Mart? What

is the volatility of this portfolio?

19) You currently own $100,000 worth of Wal-Mart stock. Suppose that Wal-Mart has an expected

return of 14% and a volatility of 23%. The market portfolio has an expected return of 12% and a

volatility of 16%. The risk-free rate is 5%. Assuming the CAPM assumptions hold, what alternative

investment has the highest possible expected return while having the same volatility as Wal-Mart?

What is the expected return of this portfolio?

20) Which of the following statements is FALSE?

A) The risk premium of a security is equal to the market risk premium (the amount by which the

market’s expected return exceeds the risk-free rate), divided by the amount of market risk present in the

security’s returns measured by its beta with the market.

B) We refer to the beta of a security with the market portfolio simply as the securities beta.

C) There is a linear relationship between a stock’s beta and its expected return.

D) A security with a negative beta has a negative correlation with the market, which means that this

security tends to perform well when the rest of the market is doing poorly.

21) Which of the following statements is FALSE?

A) The expected return of a portfolio should correspond to the portfolio’s beta.

B) Graphically the line through the risk-free investment and the market portfolio is called the capital

market line (CML).

C) The beta of a portfolio is the weighted average beta of the securities in the portfolio.

D) By holding a negative beta security, an investor can reduce the overall market risk of her portfolio.

22) Which of the following statements is FALSE?

A) To improve the performance of their portfolios, investors who are holding the market portfolio will

compare the expected return of each security with its required return from the security market line.

B) The Sharpe ratio of a portfolio will increase if we sell stocks with positive alphas.

C) When a stock’s alpha is not zero, investors can improve upon the performance of the market

portfolio.

D) When the market portfolio is efficient, all stocks are on the security market line and have an alpha of

zero.

23) Which of the following statements is FALSE?

A) We can improve the performance of our portfolio by selling stocks with negative alphas.

B) The market portfolio is on the SML, and according to the CAPM, since all other portfolios are

inefficient they will not fall on the SML.

C) The difference between a stock’s expected return and its required return according to the security

market line is called the stock’s alpha.

D) The risk premium for any security is proportional to its beta with the market.

24) Which of the following statements is FALSE?

A) The market portfolio is the efficient portfolio.

B) Many practitioners believe it is sensible to use the CAPM and the security market line as a practical

means to estimate a stock’s required return and therefore a firm’s equity cost of capital.

C) If we plot individual securities according to their expected return and beta, the CAPM implies that

they should all fall along the CML.

D) As savvy investors attempt to trade to improve their portfolios, they raise the price and lower the

expected return of the positive alpha stocks, and they depress the price and raise the expected return of

negative alpha stocks, until the stocks are once again on the security market line and the market

portfolio is efficient.

25) The beta for the market portfolio is closest to:

A) 1

B) 0

C) Unable to answer this question without knowing the markets expected return

D) Unable to answer this question without knowing the markets volatility

26) The beta for the risk free investment is closest to:

A) 1

B) 0

C) Unable to answer this question without knowing the risk free rate

D) Unable to answer this question without knowing the markets volatility

Use the information for the question(s) below.

Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a

volatility of 18%. Monsters Inc. has a 24% volatility and a correlation with the market of .60, while

California Gold Mining has a 32% volatility and a correlation with the market of -.7. Assume the CAPM

assumptions hold.

27) Monsters’ beta with the market is closest to:

A) 1.3

B) 1.0

C) 0.6

D) 0.8

28) Monsters’ required return is closest to:

A) 10.0%

B) 13.0%

C) 11.5%

D) 15.5%

29) Suppose that Monsters’ expected return is 12%. Then Monsters’ alpha is closest to:

A) -2.0%

B) -1.0%

C) 1.0%

D) 0.5%

30) California Gold Mining’s beta with the market is closest to:

A) 0.9

B) 1.25

C) -0.9

D) -1.25

31) California Gold Mining’s required return is closest to:

A) –5%

B) 13%

C) 15%

D) 5%

32) Suppose that California Gold Mining’s expected return is 2%. Then California Gold Mining’s alpha

is closest to:

A) –3%

B) –13%

C) 7%

D) –11%

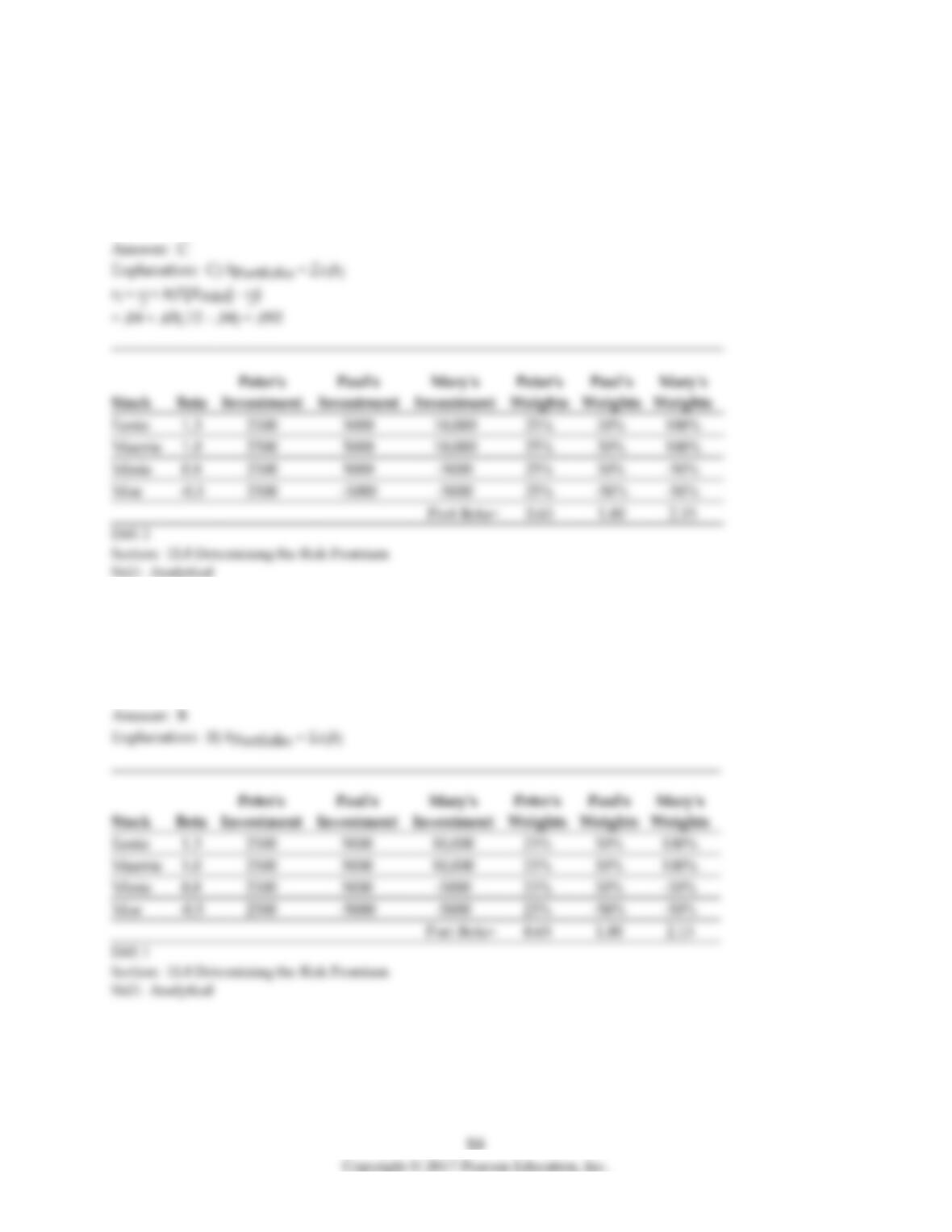

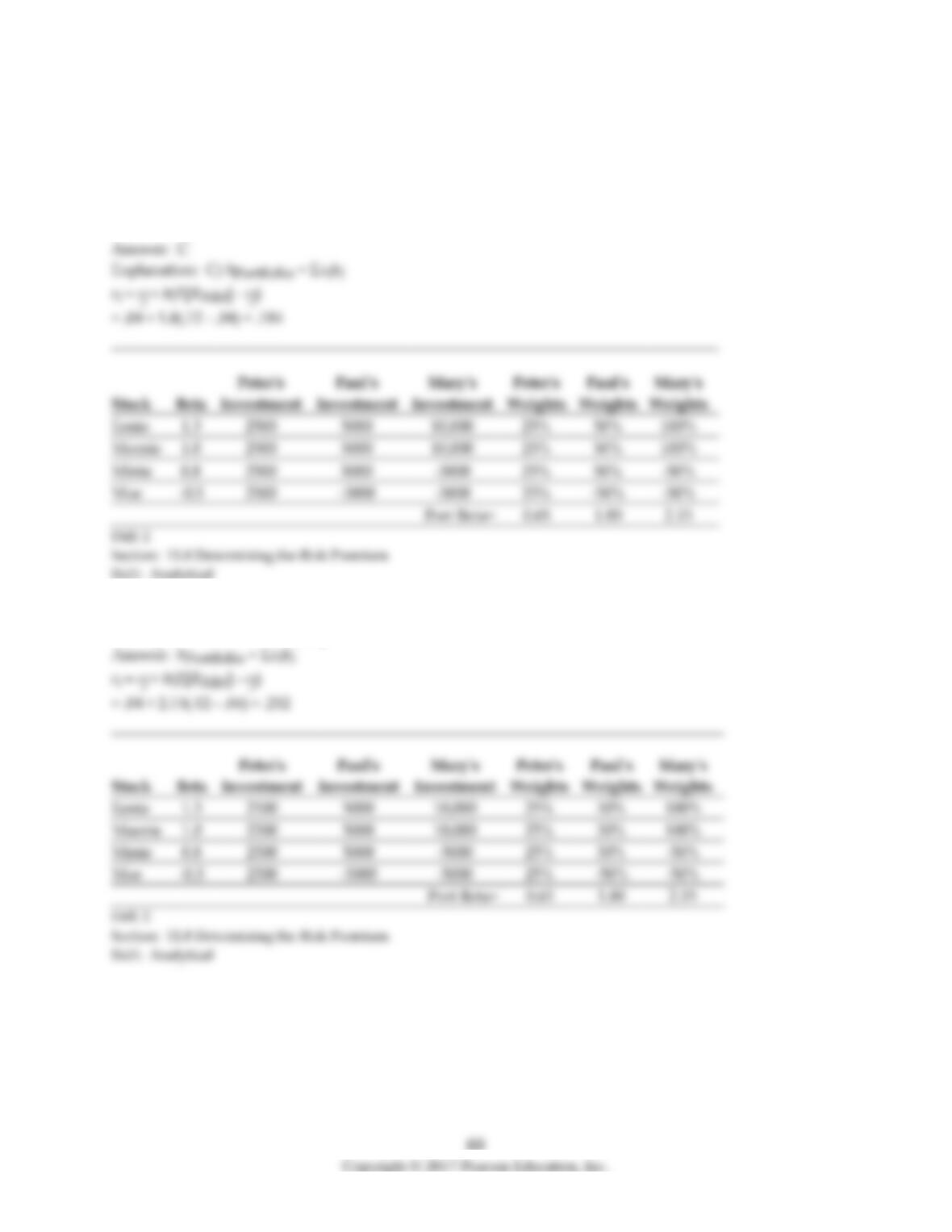

Use the table for the question(s) below.

Consider the following three individuals portfolios consisting of investments in four stocks:

Stock

Beta

Peter’s

Investment

Paul’s

Investment

Mary’s

Investment

Eenie

1.3

2500

5000

10,000

Meenie

1.0

2500

5000

10,000

Minie

0.8

2500

5000

-5000

Moe

-0.5

2500

-5000

-5000

33) The beta on Peter’s Portfolio is closest to:

A) 0.7

B) 0.8

C) 1.8

D) 1.0

Eenie

Meenie

Minie

-5000

Moe

-5000

-5000

34) Assuming that the risk-free rate is 4% and the expected return on the market is 12%, then required

return on Peter’s Portfolio is closest to:

A) 10%

B) 12%

C) 9%

D) 8%

35) The beta on Paul’s Portfolio is closest to:

A) 1.5

B) 1.8

C) 1.3

D) 1.0

36) Assuming that the risk-free rate is 4% and the expected return on the market is 12%, then required

return on Peter’s portfolio is closest to:

A) 20%

B) 22%

C) 18%

D) 16%

37) Assuming that the risk-free rate is 4% and the expected return on the market is 12%, then calculate

the required return on Mary’s portfolio.

38) Suppose that the risk-free rate is 5% and the market portfolio has an expected return of 13% with a

volatility of 18%. Luther Industries has a volatility of 24% and a correlation with the market of .5. If

you assume that the CAPM assumptions hold, then what is the expected return on Luther stock?

39) Which of the following statements is FALSE?

A) Investors may have different information regarding expected returns, correlations, and volatilities,

but they correctly interpret that information and the information contained in market prices and they

adjust their estimates of expected returns in a rational way.

B) Investors may learn different information through their own research and observations, but as long

as they understand the differences in information and learn from other investors by observing prices,

the CAPM conclusions still stand.

C) Every investor, regardless of how much information he has access to, can guarantee himself an alpha

of zero by holding the market portfolio.

D) The CAPM requires making the strong assumption of homogeneous expectations.

40) Which of the following statements is FALSE?

A) Because of the higher and uncompensated risk involved, no investor should choose a portfolio with

a negative alpha.

B) Because the average portfolio of all investors is the market portfolio, the average alpha for all

investors is zero.

C) The market portfolio can be inefficient if a significant number of investors misinterpret information

and believe they are earning a positive alpha when they are actually earning a negative alpha.

D) If no investor earns a positive alpha, then no investor can earn a negative alpha, and the market

portfolio must be efficient.

41) Explain how having different interest rates for borrowing and lending affects the CAPM and the

SML.

11.9 Appendix: The CAPM with Differing Interest Rates

1) How is the optimal portfolio choice affected if there are different rates for borrowers and savers?