Ch 11 Cash Flow Estimation and Risk Analysis

67. Laramie Labs uses a risk-adjustment when evaluating projects of different risk. Its overall (composite) WACC is 10%,

which reflects the cost of capital for its average asset. Its assets vary widely in risk, and Laramie evaluates low-risk

projects with a risk-adjusted project cost of capital of 8%, average-risk projects at 10%, and high-risk projects at 12%.

The company is considering the following projects:

Project

Risk

Expected Return

A

High

15%

B

Average

12%

C

High

11%

D

Low

9%

E

Low

6%

Which set of projects would maximize shareholder wealth?

a.

A and B.

b.

A, B, and C.

c.

A, B, and D.

d.

A, B, C, and D.

e.

A, B, C, D, and E.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.11.03 – LO: 11-3

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Risk-adjusted discount rate

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 1:03 PM

Ch 11 Cash Flow Estimation and Risk Analysis

68. The coefficient of variation, calculated as the standard deviation of expected returns divided by the expected return, is

a standardized measure of the risk per unit of expected return.

a.

True

b.

False

True

False

JFND-GO4G-EO4D-OCBS

4OTI-GO4W-NQNBEE

69. The standard deviation is a better measure of risk than the coefficient of variation if the expected returns of the

securities being compared differ significantly.

a.

True

b.

False

False

False

JFND-GO4G-EO4D-OCBI

Ch 11 Cash Flow Estimation and Risk Analysis

70. Erickson Inc. is considering a capital budgeting project that has an expected return of 25% and a standard deviation of

30%. What is the project’s coefficient of variation?

a.

1.20

b.

1.26

c.

1.32

d.

1.39

e.

1.46

a

False

JFND-GO4G-EO4D-OCBW

4OTI-GO4W-NQNBEE

71. McLeod Inc. is considering an investment that has an expected return of 15% and a standard deviation of 10%. What

is the investment’s coefficient of variation?

a.

0.67

b.

0.73

c.

0.81

d.

0.89

e.

0.98

a

Ch 11 Cash Flow Estimation and Risk Analysis

72. Sensitivity analysis measures a project’s stand-alone risk by showing how much the project’s NPV (or IRR) is affected

by a small change in one of the input variables, say sales. Other things held constant, with the size of the independent

variable graphed on the horizontal axis and the NPV on the vertical axis, the steeper the graph of the relationship line, the

more risky the project, other things held constant.

a.

True

b.

False

True

Difficulty: Moderate

True / False

False

FMTP.EHRH.17.11.05 – LO: 11-5

United States – BUSPROG: Reflective Thinking

United States – OH – Default City – TBA

Sensitivity analysis

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OCKB

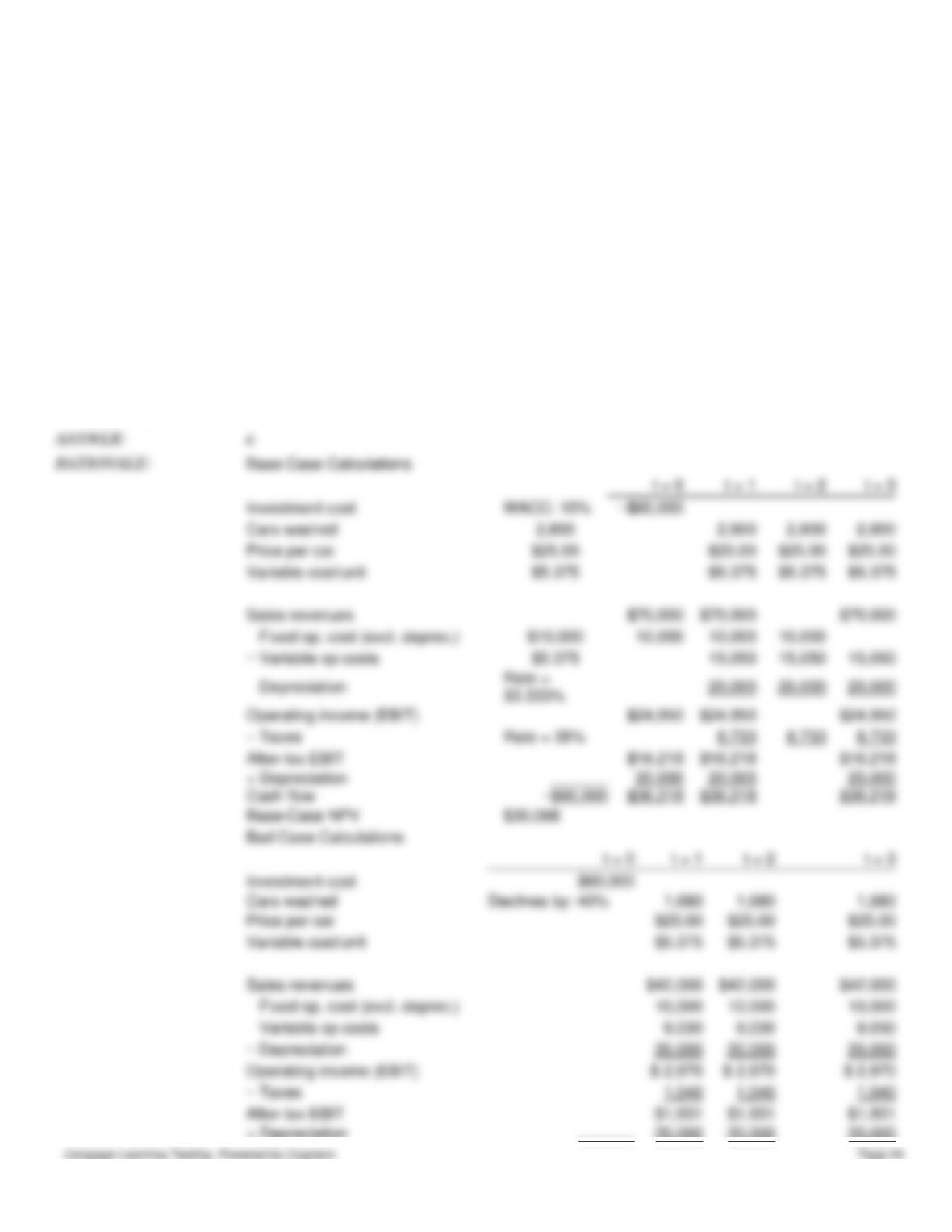

73. Spot-Free Car Wash is considering a new project whose data are shown below. The equipment to be used has a 3-year

tax life, would be depreciated on a straight-line basis over the project’s 3-year life, and would have a zero salvage value

after Year 3. No new working capital would be required. Revenues and other operating costs will be constant over the

project’s life, and this is just one of the firm’s many projects, so any losses on it can be used to offset profits in other units.

False

FMTP.EHRH.17.11.06 – LO: 11-6

United States – BUSPROG: Analytic

United States – AK – DISC: Risk and return

United States – OH – Default City – TBA

Coefficient of variation

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OCKN

Ch 11 Cash Flow Estimation and Risk Analysis

If the number of cars washed declined by 40% from the expected level, by how much would the project’s NPV decline?

(Hint: Note that cash flows are constant at the Year 1 level, whatever that level is.)

Project cost of capital (r)

10.0%

Net investment cost (depreciable basis)

$60,000

Number of cars washed

2,800

Average price per car

$25.00

Fixed op. cost (excl. deprec.)

$10,000

Variable op. cost/unit (i.e., VC per car washed)

$5.375

Annual depreciation

$20,000

Tax rate

35.0%

a.

$28,939

b.

$30,462

c.

$32,066

d.

$33,753

e.

$35,530

e

Base Case Calculations

Investment cost

WACC: 10%

Cars washed

Price per car

Variable cost/unit

Sales revenues

Operating income (EBIT)

Rate = 35%

After-tax EBIT

+ Depreciation

Cash flow

$36,218

Base-Case NPV

Bad Case Calculations

Investment cost

Cars washed

Declines by: 40%

Price per car

Variable cost/unit

Sales revenues

+ Depreciation

20,000

20,000

20,000

Ch 11 Cash Flow Estimation and Risk Analysis

74. Because of differences in the expected returns on different investments, the standard deviation is not always an

adequate measure of risk. However, the coefficient of variation adjusts for differences in expected returns and thus allows

investors to make better comparisons of investments’ stand-alone risk.

a.

True

b.

False

True

False

Bad-Case NPV

Decline in NPV

False

JFND-GO4G-EO4D-OCJ3

Ch 11 Cash Flow Estimation and Risk Analysis

8/26/2015 10:46 AM

4OTI-GO4W-NQNBEE

75. Which of the following statements is CORRECT?

a.

One advantage of sensitivity analysis relative to scenario analysis is that it explicitly takes into account the

probability of specific effects occurring, whereas scenario analysis cannot account for probabilities.

b.

Well-diversified stockholders do not need to consider market risk when determining required rates of return.

c.

Market risk is important, but it does not have a direct effect on stock prices because it only affects beta.

d.

Simulation analysis is a computerized version of scenario analysis where input variables are selected randomly

on the basis of their probability distributions.

e.

Sensitivity analysis is a good way to measure market risk because it explicitly takes into account

diversification effects.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.11.07 – LO: 11-7

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Sensitivity, scenario, & sim.

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

76. Which of the following statements is CORRECT?

a.

In comparing two projects using sensitivity analysis, the one with the steeper lines would be considered less

risky, because a small error in estimating a variable such as unit sales would produce only a small error in the

project’s NPV.

b.

The primary advantage of simulation analysis over scenario analysis is that scenario analysis requires a

relatively powerful computer, coupled with an efficient financial planning software package, whereas

simulation analysis can be done efficiently using a PC with a spreadsheet program or even with just a

calculator.

c.

Sensitivity analysis is a type of risk analysis that considers both the sensitivity of NPV to changes in key input

variables and the probability of occurrence of these variables’ values.

Ch 11 Cash Flow Estimation and Risk Analysis

d.

As computer technology advances, simulation analysis becomes increasingly obsolete and thus less likely to

be used as compared to sensitivity analysis.

e.

Sensitivity analysis as it is generally employed is incomplete in that it fails to consider the probability of

occurrence of the key input variables.

e

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.11.07 – LO: 11-7

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

Sensitivity, scenario, & sim.

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OCKF

GO4W-NQNBEE

77. Which of the following procedures does the text say is used most frequently by businesses when they do capital

budgeting analyses?

a.

Differential project risk cannot be accounted for by using “risk-adjusted discount rates” because it is highly

subjective and difficult to justify. It is better to not risk adjust at all.

b.

Other things held constant, if returns on a project are thought to be positively correlated with the returns on

other firms in the economy, then the project’s NPV will be found using a lower discount rate than would be

appropriate if the project’s returns were negatively correlated.

c.

Monte Carlo simulation uses a computer to generate random sets of inputs, those inputs are then used to

determine a trial NPV, and a number of trial NPVs are averaged to find the project’s expected NPV. Sensitivity

and scenario analyses, on the other hand, require much more information regarding the input variables,

including probability distributions and correlations among those variables. This makes it easier to implement a

simulation analysis than a scenario or a sensitivity analysis, hence simulation is the most frequently used

procedure.

d.

DCF techniques were originally developed to value passive investments (stocks and bonds). However, capital

budgeting projects are not passive investments⎯managers can often take positive actions after the investment

has been made that alter the cash flow stream. Opportunities for such actions are called real options. Real

options are valuable, but this value is not captured by conventional NPV analysis. Therefore, a project’s real

options must be considered separately.

e.

The firm’s corporate, or overall, WACC is used to discount all project cash flows to find the projects’ NPVs.

Then, depending on how risky different projects are judged to be, the calculated NPVs are scaled up or down

to adjust for differential risk.

Ch 11 Cash Flow Estimation and Risk Analysis

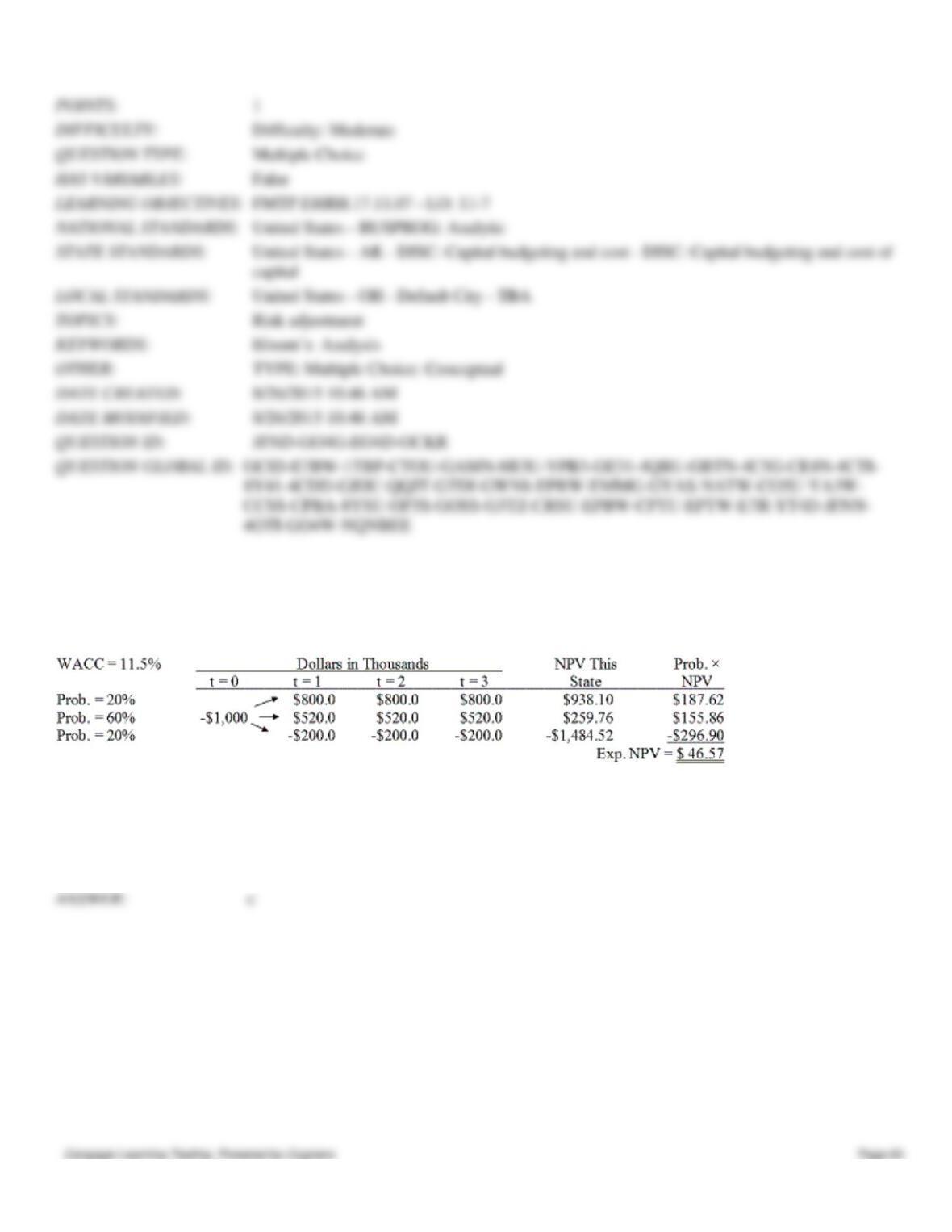

78. Brandt Enterprises is considering a new project that has a cost of $1,000,000, and the CFO set up the following simple

decision tree to show its three most likely scenarios. The firm could arrange with its work force and suppliers to cease

operations at the end of Year 1 should it choose to do so, but to obtain this abandonment option, it would have to make a

payment to those parties. How much is the option to abandon worth to the firm?

a.

$55.08

b.

$57.98

c.

$61.03

d.

$64.08

e.

$67.29

c

False

JFND-GO4G-EO4D-OCKR

4OTI-GO4W-NQNBEE

Ch 11 Cash Flow Estimation and Risk Analysis