11-1

Chapter 11

Answers to Review Problems

Finance For Executives – 4th Edition

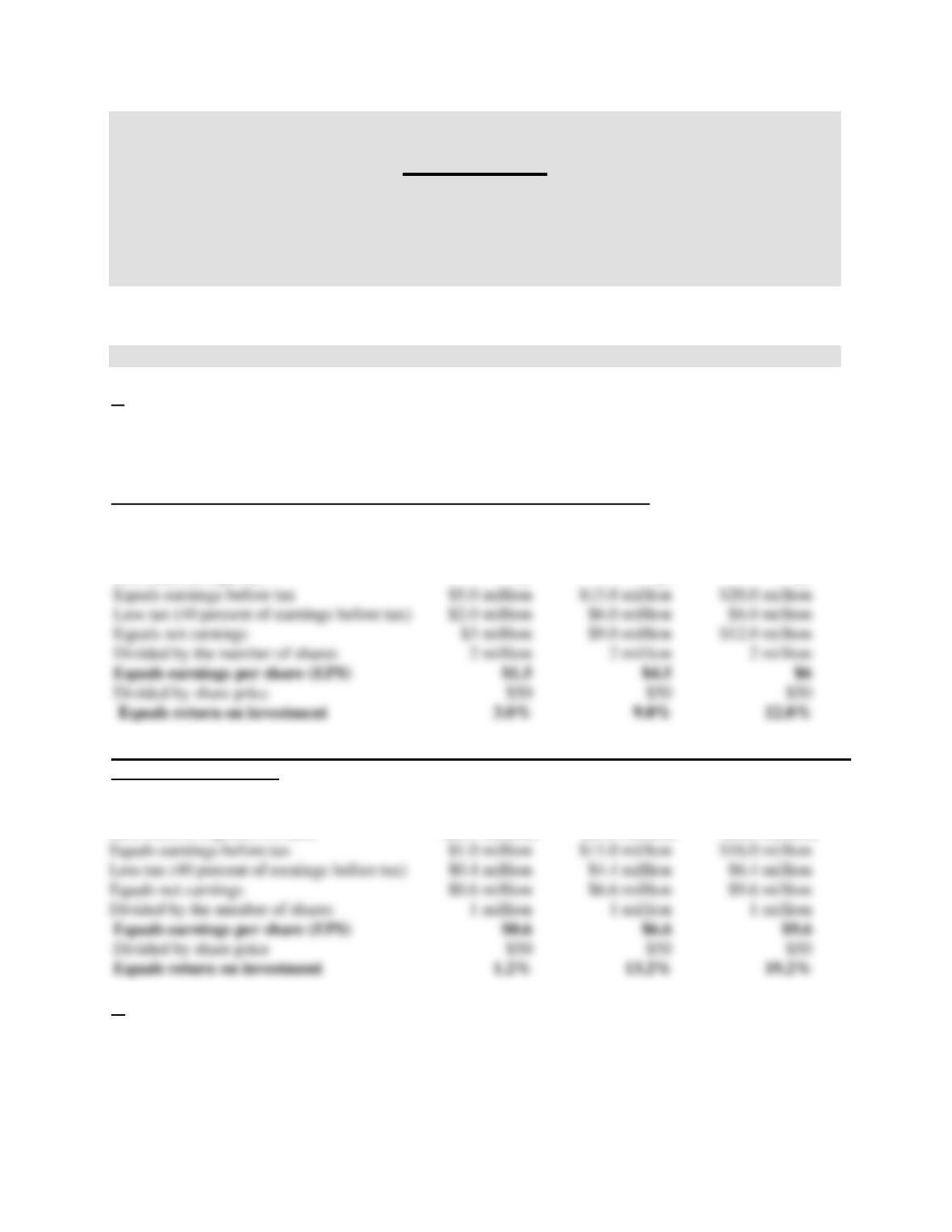

1. EBIT–EPS analysis.

a.

The following tables show the calculations of Chloroline’s EPS and return on investment as a function of

the firm’s EBIT, without debt and with debt.

Current Capital Structure: No Debt and Two Million Shares Outstanding

Recession Expected Expansion

Earnings before interest and tax (EBIT) $5.0 million $15.0 million $20.0 million

Less interest expenses $0 $0 $0

Proposed Capital Structure: Borrow $50 million at 8 percent and use the cash to repurchase 1 million

shares at $50 per share

Recession Expected Expansion

Earnings before interest and tax (EBIT) $5.0 million $15.0 million $20.0 million

Less interest expenses on debt ($4.0 million) ($4.0 million) ($4.0 million)

b.

The analysis shows that a substitution of debt for equity will increase Chloroline’s EPS and return on

investment in the expected and expansion scenarios, but will decrease EPS and return on investment in

the recession scenario. These results, however, are insufficient to make a recommendation on whether the

firm should recapitalize for the following reasons:

11-2

2. Firm value and capital structure in the absence of tax.

This statement is false. An increase in debt financing has two consequences: (1) an increase in risk for

3. Homemade leverage.

a.

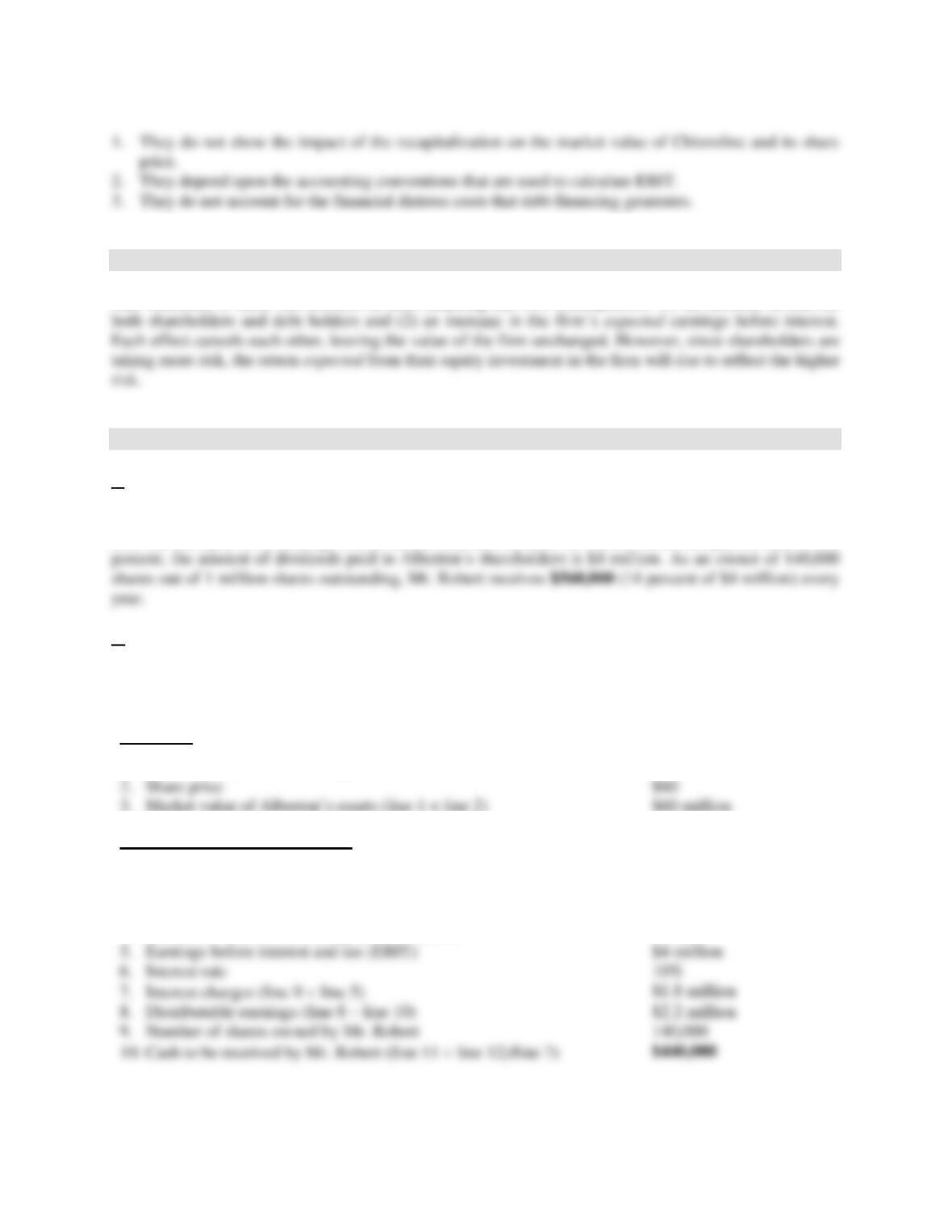

Currently, Alberton does not have any debt outstanding and it does pay any tax. Therefore, its earnings

after tax are equal to its earnings before interest and tax, which is $4 million. Since the payout ratio is 100

b.

Under the proposed capital structure, the number of shares outstanding will be reduced since the proceeds

of the debt issue will be used to buy back shares.

Currently

1. Number of shares outstanding

1 million

2. Share price

$60

3. Market value of Alberton’s assets (line 1 × line 2)

$60 million

Under the new capital structure

1. Debt-to-assets ratio

30 %

2. Amount of debt issued (line 4 line 3)

$18 million

3. Number of shares repurchased (line 5/line 2)

300,000

4. Number of shares outstanding (line 1 – line 6)

700,000

5. Earnings before interest and tax (EBIT)

$4 million

6. Interest rate

10%

7. Interest charges (line 9 line 5)

$1.8 million

8. Distributable earnings (line 8 – line 10)

$2.2 million

9. Number of shares owned by Mr. Robert

140,000

10. Cash to be received by Mr. Robert (line 11 line 12)/line 7)

11-3

c.

Mr. Robert will receive less cash under the new capital structure than under the current one ($440,000

versus $560,000). This is because the interest rate on the debt, 10 percent, is higher than Alberton’s return

on assets, 6.67 percent ($4 million of EBIT divided by $60 million of assets).

Mr. Robert can keep receiving $560,000 from his investment in Alberton if he does the following:

1. Number of shares outstanding

700,000

2. Number of shares owned by Mr. Robert

98,000

3. Distributable earnings (see line 8 above)

$2.2 million

4. Amount of dividend to be received by Mr. Robert (line 3 line 2)/line 1)

$308,000

5. Amount of debt subscribed by Mr. Robert

$2.52 million

6. Interest rate

10%

7. Amount of interest to be received by Mr. Robert (line 6 line 5)

$252,000

8. Total amount of cash to be received by Mr. Robert (line 4 + line 7)

4. Cost of debt versus cost of equity.

The argument is irrelevant. Using more debt relative to equity makes the firm riskier for both

shareholders and bondholders, thus increasing the return expected by them from investing in the firm.

Both the cost of debt and the cost of equity increase with more debt financing, especially the latter since

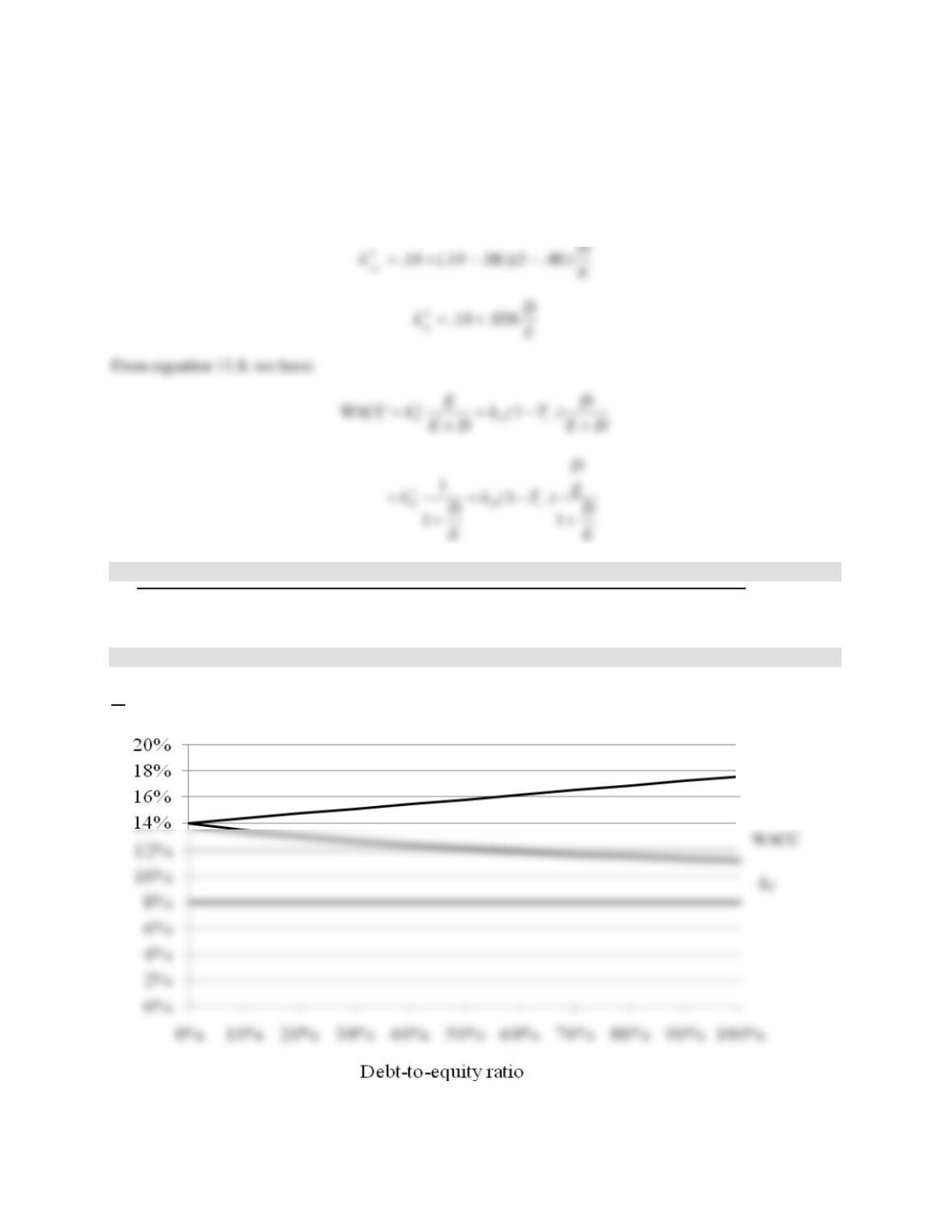

5. Changes in capital structure and the cost of capital.

a.

In the absence of debt, the cost of equity of Starline is equal to the return from its assets because the

shareholders are the only claimants to the cash flows generated by these assets. Thus, Starline’s return on

11-4

where:

L

E

k

= cost of equity

rA = return on assets = 14%

kD = cost of debt = 8%

Tc = corporate tax rate = 40%

D/E = debt-to-equity ratio

D/E 0 25% 50% 75% 100%

kD 0.08 0.08 0.08 0.08 0.08

L

E

k

0.14 0.149 0.158 0.167 0.176

WACC 0.14 0.129 0.121 0.116 0.112

b.

L

E

k

11-5

c.

According to the above analysis, you would be tempted to recommend that Starline increase its

indebtedness as much as possible because the higher the level of debt, the lower the weighted average

6. The cost of equity, the weighted average cost of capital, and financial leverage.

a.

From equation 11.2:

E

D

)kr(rk DAA

L

E−+=

where:

L

E

k

L

E

k

= cost of equity

rA = expected return on the firm’s assets

kD = cost of debt

D/E = debt-to–equity ratio

b.

From equation 11.7:

E

D

)T)(kr(rk cDAA

L

E−−+= 1

where:

11-6

When the target debt ratio is 1:

L

E

k

= 12% + (12% – 8%) (1 – .40) 1 = 14.4%

and WACC = 14.4% .50 + 8% (1 – .40) .50 = 9.6%

7. The value of the interest tax shield.

a.

The annual tax savings, or interest tax shield (ITS), is:

ITS = Tax rate Interest rate Amount of debt

= .35 .08 $25,000,000 = $700,000

Note that the value of the tax shield would represent 8.75 percent of the market value of the firm, since

the firm has currently no debt and its market value is $100,000,000.

11-7

b.

If the interest rate increases immediately after the debt is issued:

PV(ITS)permanent =

000,700$

= $7,777,778

8. Industry influence on the capital structure.

The probability that an electric utility goes bankrupt is quite small because (1) it is usually a local

monopoly and (2) most of its valuable assets are tangible ones. It should exhibit the highest debt ratio

among the three firms. At the opposite, a biotechnology firm’s most valuable assets are intangible and its

9. Board of directors and management.

It is in the interest of the managers to maintain a low debt–to-equity ratio when the board of directors

exercise little power on them. By keeping financial leverage low, they reduce the probability of the firm

10. Agency costs.

Shareholders expropriate wealth from bondholders when they induce management to (1) make

investments which are riskier than anticipated by bondholders, (2) increase debt at a higher level than