21

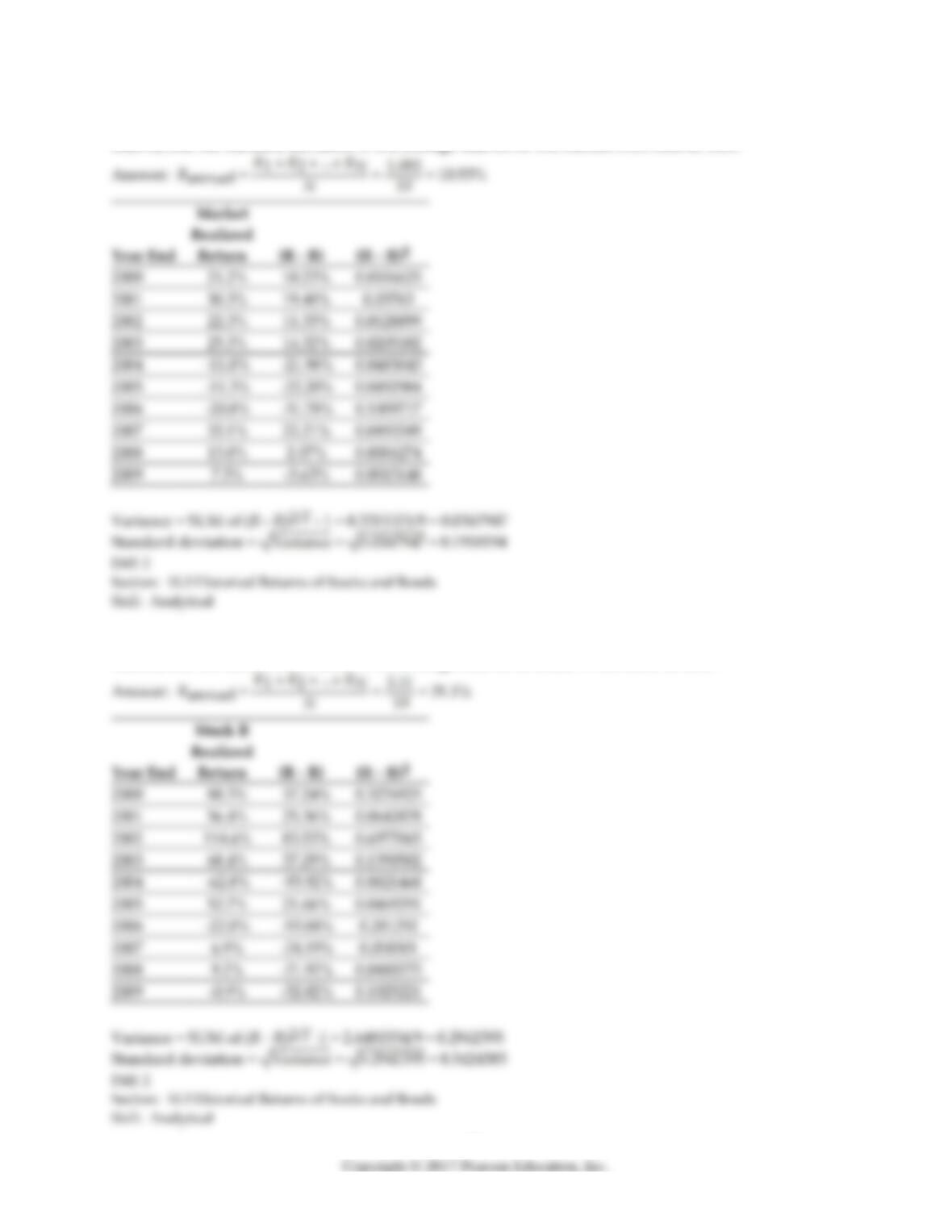

25) Using the data provided in the table, calculate the average annual return, the variance of the annual

returns, and the standard deviation of the average returns for the market from 2000 to 2009.

26) Using the data provided in the table, calculate the average annual return, the variance of the annual

returns, and the standard deviation of the average returns for Stock B from 2000 to 2009.

10.4 The Historical Trade-off Between Risk and Return

1) The excess return is the difference between the average return on a security and the average return

for:

A) Treasury Bonds.

B) a portfolio of securities with similar risk.

C) a broad based market portfolio like the S&P 500 index.

D) Treasury Bills.

2) Which of the following statements is FALSE?

A) Expected return should rise proportionately with volatility.

B) Investors would not choose to hold a portfolio that is more volatile unless they expected to earn a

higher return.

C) Smaller stocks have lower volatility than larger stocks.

D) The largest stocks are typically more volatile than a portfolio of large stocks.

3) Which of the following statements is FALSE?

A) Portfolios with higher volatility have historically rewarded investors with higher average returns.

B) Investments with higher volatility should have a higher risk premium and therefore higher returns.

C) Volatility seems to be a reasonable measure of risk when evaluating returns on large portfolios and

the returns of individual securities.

D) Riskier investments must offer investors higher average returns to compensate them for the extra

risk they are taking on.

4) Which of the following statements is TRUE?

A) Portfolios with lower volatility have historically rewarded investors with higher average returns.

B) Individual stocks with higher volatility have consistently rewarded investors with higher average

returns.

C) Volatility seems to be a reasonable measure of risk when evaluating returns on large portfolios.

D) Volatility seems to be a reasonable measure of risk when evaluating returns on individual stocks.

Use the table for the question(s) below.

Consider the following average annual returns:

Investment

Average Return

Small Stocks

23.2%

S&P 500

13.2%

Corporate Bonds

7.5%

Treasury Bonds

6.2%

Treasury Bills

4.8%

5) What is the excess return for the portfolio of small stocks?

A) 10.0%

B) 15.7%

C) 18.4%

D) 17.0%

Small Stocks

S&P 500

13.2%

Corporate Bonds

7.5%

Treasury Bonds

6.2%

Treasury Bills

4.8%

6) What is the excess return for the S&P 500?

A) 5.7%

B) 7.0%

C) 0%

D) 8.4%

Investment

Average Return

Small Stocks

23.2%

S&P 500

Corporate Bonds

Treasury Bonds

Treasury Bills

7) What is the excess return for corporate bonds?

A) 2.7%

B) 1.3%

C) -5.7%

D) 0%

8) What is the excess return for Treasury Bills?

A) 0%

B) -8.4%

C) -2.7%

D) -1.4%

9) Do expected returns for individual stocks increase proportionately with volatility?

10.5 Common Versus Independent Risk

1) Common risk is also called:

A) diversifiable risk.

B) correlated risk.

C) uncorrelated risk.

D) independent risk.

Use the following information to answer the problem(s) below.

Consider two banks. Bank A has 1000 loans outstanding each for $100,000, that it expects to be fully

repaid today. Each of Bank A’s loans have a 6% probability of default, in which case the bank will

receive $0 for each of the defaulting loans. Bank B has 100 loans of $1 million outstanding, which it also

expects to be fully repaid today. Each of Bank B’s loans have a 5% probability of default, in which case

the bank will receive $0 for each of the defaulting loans. The chance of default is independent across all

the loans.

2) The expected overall payoff to Bank A is:

A) $5,000,000

B) $6,000,000

C) $94,000,000

D) $95,000,000

3) The expected overall payoff to Bank B is:

A) $5,000,000

B) $6,000,000

C) $94,000,000

D) $95,000,000

4) The standard deviation of the overall payoff to Bank A is closest to:

A) $689,000

B) $751,000

C) $2,179,000

D) $2,375,000

5) The standard deviation of the overall payoff to Bank B is closest to:

A) $751,000

B) $2,179,000

C) $2,375,000

D) $21,794,000

Use the information for the question(s) below.

Big Cure and Little Cure are both pharmaceutical companies. Big Cure presently has a potential

“blockbuster” drug before the Food and Drug Administration (FDA) waiting for approval. If approved,

Big Cure’s blockbuster drug will produce $1 billion in net income for Big Cure. Little Cure has 10

separate less important drugs before the FDA waiting for approval. If approved, each of Little Cure’s

drugs would produce $100 million in net income for Little Cure. The probability of the FDA approving

a drug is 50%.

6) What is the expected payoff for Big Cure’s Blockbuster drug?

A) $100 million

B) $0

C) $1 billion

D) $500 million

7) What is the expected payoff for Little Cure’s ten drugs?

A) $500 million

B) $100 million

C) $1 billion

D) $0

8) What is the standard deviation of Big Cure’s average net income for their new blockbuster drug?

A) $0

B) $1 billion

C) $100 million

D) $500 million

9) The standard deviation of Little Cure’s average net income for their ten new drugs is closest to:

A) $50 million

B) $25 million

C) $16 million

D) $500 million

10) Which pharmaceutical company faces less risk?

10.6 Diversification in Stock Portfolios

1) Which of the following is NOT a diversifiable risk?

A) The risk that oil prices rise, increasing production costs

B) The risk of a product liability lawsuit

C) The risk that the CEO is killed in a plane crash

D) The risk of a key employee being hired away by a competitor

2) Which of the following is NOT a systematic risk?

A) The risk that oil prices rise, increasing production costs

B) The risk that the Federal Reserve raises interest rates

C) The risk that the economy slows, reducing demand for your firm‘s products

D) The risk that your new product will not receive regulatory approval

3) Which of the following types of risk doesn‘t belong?

A) Market risk

B) Unique risk

C) Idiosyncratic risk

D) Unsystematic risk

4) Which of the following types of risk doesn’t belong?

A) Idiosyncratic risk

B) Undiversifiable risk

C) Market risk

D) Systematic risk

5) Which of the following statements is FALSE?

A) Firm-specific news is good or bad news about the company itself.

B) Firms are affected by both systematic and firm-specific risk.

C) When firms carry both types of risk, only the firm-specific risk will be diversified when we combine

many firms’ stocks into a portfolio.

D) The risk premium for a stock is affected by its idiosyncratic risk.

6) Which of the following statements is FALSE?

A) Because investors are risk averse, they will demand a risk premium to hold unsystematic risk.

B) Over any given period, the risk of holding a stock is that the dividends plus the final stock price will

be higher or lower than expected, which makes the realized return risky.

C) The risk premium for diversifiable risk is zero, so investors are not compensated for holding firm–

specific risk.

D) Because investors can eliminate firm-specific risk “for free” by diversifying their portfolios, they will

not require a reward or risk premium for holding it.

7) Which of the following statements is FALSE?

A) Fluctuations of a stock’s returns that are due to firm–specific news are common risks.

B) The volatility in a large portfolio will decline until only the systematic risk remains.

C) When we combine many stocks in a large portfolio, the firm-specific risks for each stock will average

out and be diversified.

D) The risk premium of a security is determined by its systematic risk and does not depend on its

diversifiable risk.

8) Consider a portfolio that consists of an equal investment in 20 firms. For each of these firms, there is a

70% probability that the firms will have a 16% return and a 30% that they will have a -8% return. Each

of these firms’ returns is independent of all others. The standard deviation of this portfolio is closest to:

A) 2.5%

B) 4.2%

C) 8.8%

D) 11.0%

Use the information for the question(s) below.

Consider an economy with two types of firms, S and I. S firms always move together, but I firms move

independently of each other. For both types of firm there is a 70% probability that the firm will have a

20% return and a 30% probability that the firm will have a -30% return.

9) What is the expected return for an individual firm?

A) 14%

B) 3%

C) 5%

D) –5%

10) The standard deviation for the return on an individual firm is closest to:

A) 23.0%

B) 5.25%

C) 15.0%

D) 10.0%

11) The standard deviation for the return on a portfolio of 20 type S firms is closest to:

A) 5.10%

B) 23.0%

C) 15.0%

D) 5.25%

12) The standard deviation for the return on an portfolio of 20 type I firms is closest to:

A) 5.25%

B) 5.10%

C) 15.0%

D) 23.0%