Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:29 AM

60. Martin Manufacturing is considering two normal, equally risky, mutually exclusive, but not repeatable projects.

Martin’s cost of capital is 10%. The two projects have the same investment costs, but Project A has an IRR of 15%, while

Project B has an IRR of 20%. Assuming the projects’ NPV profiles cross in the upper right quadrant, which of the

following statements is CORRECT?

a.

Since the projects are mutually exclusive, the firm should always select Project B.

b.

If the crossover rate is 8%, Project B will have the higher NPV.

c.

Only one project has a positive NPV.

d.

If the crossover rate is 8%, Project A will have the higher NPV.

e.

Each project must have a negative NPV.

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

61. Projects A and B are mutually exclusive and have normal cash flows. Project A has an IRR of 15% and B’s IRR is

20%. The company’s cost of capital is 12%, and at that rate Project A has the higher NPV. Which of the following

statements is CORRECT?

a.

Assuming the timing pattern of the two projects’ cash flows is the same, Project B probably has a higher cost

(and larger scale).

b.

Assuming the two projects have the same scale, Project B probably has a faster payback than Project A.

c.

The crossover rate for the two projects must be 12%.

d.

Since B has the higher IRR, then it must also have the higher NPV if the crossover rate is less than the cost of

capital of 12%.

e.

The crossover rate for the two projects must be less than 12%.

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:30 AM

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:29 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

62. Hart Corp. is considering a project that has the following cash flow data. What is the project’s IRR? Note that a

project’s IRR can be less than the cost of capital or negative, in both cases it will be rejected.

Year

0

1

2

3

Cash flows

−$1,000

$425

$425

$425

a.

12.55%

b.

13.21%

c.

13.87%

d.

14.56%

e.

15.29%

Difficulty: Easy

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:31 AM

JFND-GO4G-EO4D-OQJO

4OTI-GO4W-NQNBEE

63. Spence Company is considering a project that has the following cash flow data. What is the project’s IRR? Note that a

project’s IRR can be less than the cost of capital or negative, in both cases it will be rejected.

Year

0

1

2

3

4

Cash flows

−$1,050

$400

$400

$400

$400

a.

14.05%

b.

15.61%

c.

17.34%

d.

19.27%

e.

21.20%

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

Difficulty: Easy

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:32 AM

JFND-GO4G-EO4D-OQJZ

64. Nichols Inc. is considering a project that has the following cash flow data. What is the project’s IRR? Note that a

project’s IRR can be less than the cost of capital or negative, in both cases it will be rejected.

Year

0

1

2

3

4

5

Cash flows

−$1,250

$325

$325

$325

$325

$325

a.

9.43%

b.

9.91%

c.

10.40%

d.

10.92%

e.

11.47%

a

Difficulty: Easy

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

capital

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:34 AM

JFND-GO4G-EO4D-OQJS

4OTI-GO4W-NQNBEE

65. Kiley Electronics is considering a project that has the following cash flow data. What is the project’s IRR? Note that a

project’s IRR can be less than the cost of capital (and even negative), in which case it will be rejected.

Year

0

1

2

3

Cash flows

−$1,100

$450

$470

$490

a.

9.70%

b.

10.78%

c.

11.98%

d.

13.31%

e.

14.64%

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:35 AM

JFND-GO4G-EO4D-OQJI

4OTI-GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

66. Modern Refurbishing Inc. is considering a project that has the following cash flow data. What is the project’s IRR?

Note that a project’s IRR can be less than the cost of capital (and even negative), in which case it will be rejected.

Year

0

1

2

3

4

Cash flows

−$850

$300

$290

$280

$270

a.

13.13%

b.

14.44%

c.

15.89%

d.

17.48%

e.

19.22%

a

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:36 AM

JFND-GO4G-EO4D-OQJW

67. Pet World is considering a project that has the following cash flow data. What is the project’s IRR? Note that a

project’s IRR can be less than the cost of capital (and even negative), in which case it will be rejected.

Year

0

1

2

3

4

5

Cash flows

−$9,500

$2,000

$2,025

$2,050

$2,075

$2,100

a.

2.08%

b.

2.31%

c.

2.57%

d.

2.82%

e.

3.10%

c

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

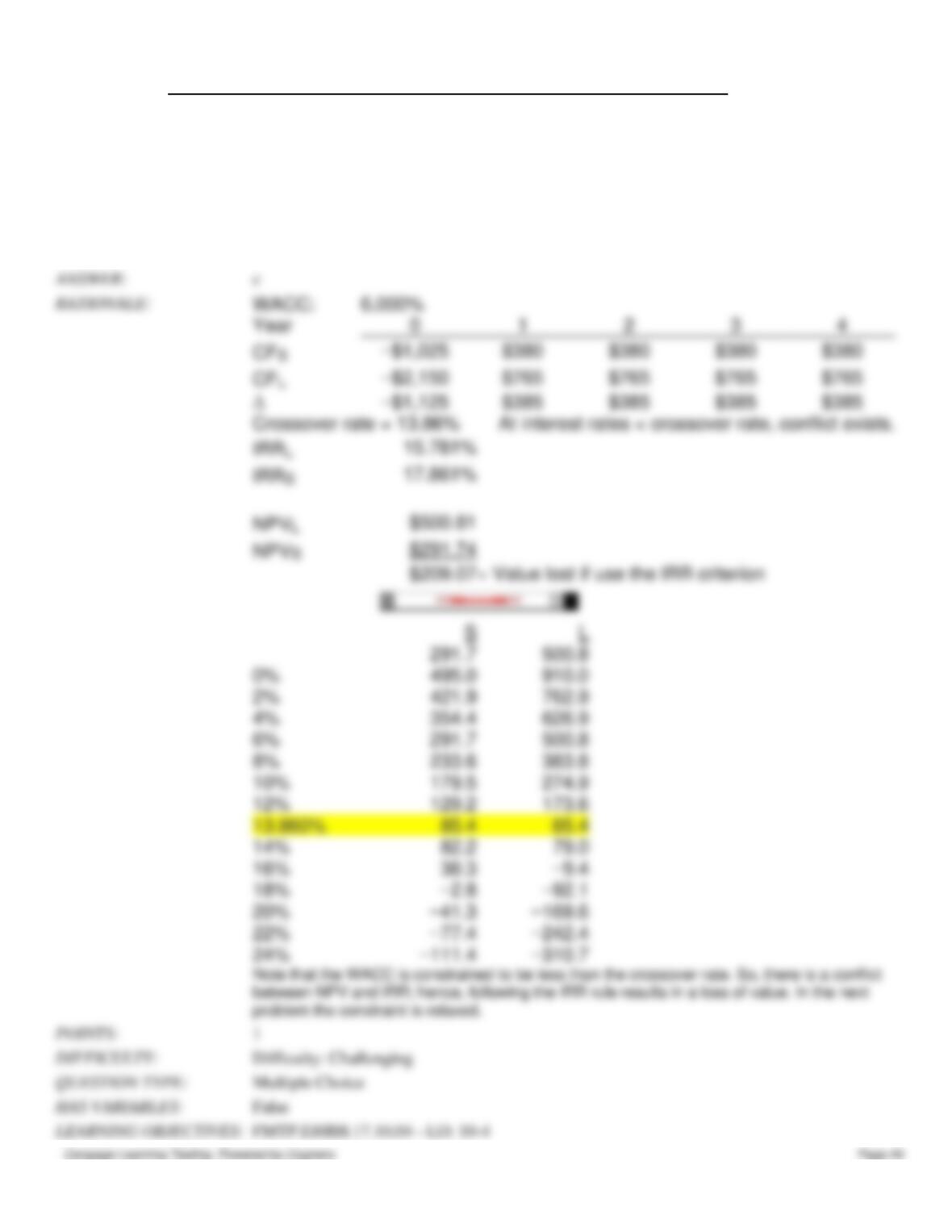

68. Current Design Co. is considering two mutually exclusive, equally risky, and not repeatable projects, S and L. Their

cash flows are shown below. The CEO believes the IRR is the best selection criterion, while the CFO advocates the NPV.

If the decision is made by choosing the project with the higher IRR rather than the one with the higher NPV, how much, if

any, value will be forgone, i.e., what’s the chosen NPV versus the maximum possible NPV? Note that (1) “true value” is

measured by NPV, and (2) under some conditions the choice of IRR vs. NPV will have no effect on the value gained or

lost.

r:

7.50%

Year

0

1

2

3

4

CFS

−$1,100

$550

$600

$100

$100

CFL

−$2,700

$650

$725

$800

$1,400

a.

$138.10

b.

$149.21

c.

$160.31

d.

$171.42

e.

$182.52

a

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:36 AM

JFND-GO4G-EO4D-OTKN

GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

69. Murray Inc. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. The CEO wants to use the IRR criterion, while the CFO favors the NPV

method. You were hired to advise Murray on the best procedure. If the wrong decision criterion is used, how much

potential value would Murray lose?

r:

6.00%

Year

0

1

2

3

4

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. IRR

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:38 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

CFS

−$1,025

$380

$380

$380

$380

CFL

−$2,150

$765

$765

$765

$765

a.

$188.68

b.

$198.61

c.

$209.07

d.

$219.52

e.

$230.49

c

False

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

70. Projects S and L, whose cash flows are shown below, are mutually exclusive, equally risky, and not repeatable.

Hooper Inc. is considering which of these two projects to undertake. If the decision is made by choosing the project with

the higher IRR, how much value will be forgone? Note that under certain conditions choosing projects on the basis of the

IRR will not cause any value to be lost because the project with the higher IRR will also have the higher NPV, so no value

will be lost if the IRR method is used.

r:

10.25%

Year

0

1

2

3

4

CFS

−$2,050

$750

$760

$770

$780

CFL

−$4,300

$1,500

$1,518

$1,536

$1,554

a.

$134.79

b.

$141.89

c.

$149.36

d.

$164.29

e.

$205.36

c

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. IRR

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:39 AM

JFND-GO4G-EO4D-OTJ3

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

71. Markman & Sons is considering Projects S and L. These projects are mutually exclusive, equally risky, and not

repeatable and their cash flows are shown below. If the decision is made by choosing the project with the higher IRR, how

much value will be forgone? Note that under certain conditions choosing projects on the basis of the IRR will not cause

any value to be lost because the project with the higher IRR will also have the higher NPV, i.e., no conflict will exist.

r:

10.00%

Year

0

1

2

3

4

CFS

−$1,025

$650

$450

$250

$50

CFL

−$1,025

$100

$300

$500

$700

a.

$5.47

b.

$6.02

c.

$6.62

d.

$7.29

e.

$7.82

e

IRRL

15.66%

IRRS

19.86%

Difficulty: Challenging

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. IRR

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:40 AM

JFND-GO4G-EO4D-OTJA

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

Difficulty: Challenging

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. IRR

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:41 AM

JFND-GO4G-EO4D-OTKG

72. Carolina Company is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and are not repeatable. If the decision is made by choosing the project with the higher IRR, how

much value will be forgone? Note that under some conditions choosing projects on the basis of the IRR will cause $0.00

value to be lost.

r:

7.75%

Year

0

1

2

3

4

CFS

−$1,050

$675

$650

CFL

−$1,050

$360

$360

$360

$360

a.

$11.45

b.

$12.72

c.

$14.63

d.

$16.82

e.

$19.35

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

73. Silverman Co. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. If the decision is made by choosing the project with the higher MIRR rather

than the one with the higher NPV, how much value will be forgone? Note that under some conditions choosing projects

on the basis of the MIRR will cause $0.00 value to be lost.

r:

8.75%

Year

0

1

2

3

4

CFS

−$1,100

$375

$375

$375

$375

CFL

−$2,200

$725

$725

$725

$725

a.

$32.12

b.

$35.33

c.

$38.87

d.

$40.15

e.

$42.16

Difficulty: Challenging

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. IRR

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:42 AM

JFND-GO4G-EO4D-OTKF

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

False

JFND-GO4G-EO4D-OTKR

74. Farmer Co. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. If the decision is made by choosing the project with the shorter payback,

some value may be forgone. How much value will be lost in this instance? Note that under some conditions choosing

projects on the basis of the shorter payback will not cause value to be lost.

r =

10.25%

Year

0

1

2

3

4

CFS

−$950

$500

$800

$0

$0

CFL

−$2,100

$400

$800

$800

$1,000

a.

$24.14

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

b.

$26.82

c.

$29.80

d.

$33.11

e.

$36.42

Difficulty: Challenging

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV vs. payback

TYPE: Multiple Choice: Problem

8/26/2015 10:46 AM

8/28/2015 10:44 AM

JFND-GO4G-EO4D-OTKD

75. Langton Inc. is considering Projects S and L, whose cash flows are shown below. These projects are mutually

exclusive, equally risky, and not repeatable. The CEO believes the IRR is the best selection criterion, while the CFO

advocates the MIRR. If the decision is made by choosing the project with the higher IRR rather than the one with the

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

higher MIRR, how much, if any, value will be forgone. In other words, what’s the NPV of the chosen project versus the

maximum possible NPV? Note that (1) “true value” is measured by NPV, and (2) under some conditions the choice of

IRR vs. MIRR will have no effect on the value lost.

r =

7.00%

Year

0

1

2

3

4

CFS

−$1,100

$550

$600

$100

$100

CFL

−$2,750

$725

$725

$800

$1,400

a.

$185.90

b.

$197.01

c.

$208.11

d.

$219.22

e.

$230.32

a

NPV based on

NPV based on

NPV using

False

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

76. For a project with one initial cash outflow followed by a series of positive cash inflows, the modified IRR (MIRR)

method involves compounding the cash inflows out to the end of the project’s life, summing those compounded cash flows

to form a terminal value (TV), and then finding the discount rate that causes the PV of the TV to equal the project’s cost.

a.

True

b.

False

True

False

JFND-GO4G-EO4D-OTJ1

GO4W-NQNBEE

77. Both the regular and the modified IRR (MIRR) methods have wide appeal to professors, but most business executives

prefer the NPV method to either of the IRR methods.

a.

True

b.

False

False

False

JFND-GO4G-EO4D-OTJU

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

78. When evaluating mutually exclusive projects, the modified IRR (MIRR) always leads to the same capital budgeting

decisions as the NPV method, regardless of the relative lives or sizes of the projects being evaluated.

a.

True

b.

False

False

False

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OTJO

79. The primary reason that the NPV method is conceptually superior to the IRR method for evaluating mutually

exclusive investments is that multiple IRRs may exist, and when that happens, we don’t know which IRR is relevant.

a.

True

b.

False

False

JFND-GO4G-EO4D-OTJT

GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

80. The NPV and IRR methods, when used to evaluate two independent and equally risky projects, will lead to different

accept/reject decisions and thus capital budgets if the projects’ IRRs are greater than their cost of capital.

a.

True

b.

False

False

False

JFND-GO4G-EO4D-OTJS

GO4W-NQNBEE

81. The NPV and IRR methods, when used to evaluate two equally risky but mutually exclusive projects, will lead to

different accept/reject decisions and thus capital budgets if the cost of capital at which the projects’ NPV profiles cross is

less than the projects’ cost of capital.

a.

True

b.

False

False

False

JFND-GO4G-EO4D-OTJZ

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

82. No conflict will exist between the NPV and IRR methods, when used to evaluate two equally risky but mutually

exclusive projects, if the projects’ cost of capital exceeds the rate at which the projects’ NPV profiles cross.

a.

True

b.

False

True

Difficulty: Moderate

True / False

False

FMTP.EHRH.17.10.05 – LO: 10-5

United States – BUSPROG: Reflective Thinking

United States – OH – Default City – TBA

NPV vs. IRR

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OTJW

83. Which of the following statements is CORRECT? Assume that the project being considered has normal cash flows,

with one cash outflow at t = 0 followed by a series of positive cash flows.

Difficulty: Moderate

True / False

False

FMTP.EHRH.17.10.05 – LO: 10-5

United States – BUSPROG: Reflective Thinking

United States – OH – Default City – TBA

NPV vs. IRR

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OTJI

GO4W-NQNBEE