Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

dollar that will not be received until sometime in the future.

d.

One defect of the IRR method versus the NPV is that the IRR does not take proper account of differences in

the sizes of projects.

e.

One defect of the IRR method versus the NPV is that the IRR does not take account of cash flows over a

project’s full life.

Difficulty: Easy

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

IRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

33. Which of the following statements is CORRECT? Assume that the project being considered has normal cash flows,

with one outflow followed by a series of inflows.

a.

A project’s regular IRR is found by discounting the cash inflows at the cost of capital to find the present value

(PV), then compounding this PV to find the IRR.

b.

If a project’s IRR is greater than the WACC, then its NPV must be negative.

c.

To find a project’s IRR, we must solve for the discount rate that causes the PV of the inflows to equal the PV

of the project’s costs.

d.

To find a project’s IRR, we must find a discount rate that is equal to the cost of capital.

e.

A project’s regular IRR is found by compounding the cash inflows at the cost of capital to find the terminal

value (TV), then discounting this TV at the cost of capital.

Difficulty: Easy

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

34. Which of the following statements is CORRECT? Assume that the project being considered has normal cash flows,

with one outflow followed by a series of inflows.

a.

A project’s regular IRR is found by compounding the cash inflows at the cost of capital to find the present

value (PV), then discounting the TV to find the IRR.

b.

If a project’s IRR is smaller than the cost of capital, then its NPV will be positive.

c.

A project’s IRR is the discount rate that causes the PV of the inflows to equal the project’s cost.

d.

If a project’s IRR is positive, then its NPV must also be positive.

e.

A project’s regular IRR is found by compounding the initial cost at the cost of capital to find the terminal value

(TV), then discounting the TV at the cost of capital.

Difficulty: Easy

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

IRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/27/2015 6:55 PM

35. Which of the following statements is CORRECT?

a.

If a project has “normal” cash flows, then its MIRR must be positive.

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

IRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/27/2015 6:53 PM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

b.

If a project has “normal” cash flows, then it will have exactly two real IRRs.

c.

The definition of “normal” cash flows is that the cash flow stream has one or more negative cash flows

followed by a stream of positive cash flows and then one negative cash flow at the end of the project’s life.

d.

If a project has “normal” cash flows, then it can have only one real IRR, whereas a project with “nonnormal”

cash flows might have more than one real IRR.

e.

If a project has “normal” cash flows, then its IRR must be positive.

Difficulty: Easy

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

Normal vs. nonnormal CFs

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

36. Which of the following statements is CORRECT?

a.

Projects with “normal” cash flows can have two or more real IRRs.

b.

Projects with “normal” cash flows must have two changes in the sign of the cash flows, e.g., from negative to

positive to negative. If there are more than two sign changes, then the cash flow stream is “nonnormal.”

c.

The “multiple IRR problem” can arise if a project’s cash flows are “normal.”

d.

Projects with “nonnormal” cash flows are almost never encountered in the real world.

e.

Projects with “normal” cash flows can have only one real IRR.

Difficulty: Easy

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Normal vs. nonnormal CFs

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

37. Which of the following statements is CORRECT?

a.

One defect of the IRR method is that it does not take account of the time value of money.

b.

One defect of the IRR method is that it does not take account of the cost of capital.

c.

One defect of the IRR method is that it values a dollar received today the same as a dollar that will not be

received until sometime in the future.

d.

One defect of the IRR method is that it assumes that the cash flows to be received from a project can be

reinvested at the IRR itself, and that assumption is often not valid.

e.

One defect of the IRR method is that it does not take account of cash flows over a project’s full life.

Difficulty: Easy

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

Reinvestment rate

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OQB3

38. Which of the following statements is CORRECT?

a.

The NPV profile graph for a normal project will generally have a positive (upward) slope as the life of the

project increases.

b.

An NPV profile graph is designed to give decision makers an idea about how a project’s risk varies with its

life.

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OQNB

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

c.

An NPV profile graph is designed to give decision makers an idea about how a project’s contribution to the

firm’s value varies with the cost of capital.

d.

We cannot draw a project’s NPV profile unless we know the appropriate cost of capital for use in evaluating

the project’s NPV.

e.

An NPV profile graph shows how a project’s payback varies as the cost of capital changes.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:06 AM

39. Which of the following statements is CORRECT?

a.

If the cost of capital declines, this lowers a project’s NPV.

b.

The NPV method is regarded by most academics as being the best indicator of a project’s profitability; hence,

most academics recommend that firms use only this one method.

c.

A project’s NPV depends on the total amount of cash flows the project produces, but because the cash flows

are discounted at the cost of capital, it does not matter if the cash flows occur early or late in the project’s life.

d.

The NPV and IRR methods may give different recommendations regarding which of two mutually exclusive

projects should be accepted, but they always give the same recommendation regarding the acceptability of a

normal, independent project.

e.

The NPV method was once the favorite of academics and business executives, but today most authorities

regard the MIRR as being the best indicator of a project’s profitability.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

40. Which of the following statements is CORRECT? Assume that the project being considered has normal cash flows,

with one outflow followed by a series of inflows.

a.

If Project A has a higher IRR than Project B, then Project A must also have a higher NPV.

b.

The IRR calculation implicitly assumes that all cash flows are reinvested at the cost of capital.

c.

The IRR calculation implicitly assumes that cash flows are withdrawn from the business rather than being

reinvested in the business.

d.

If a project has normal cash flows and its IRR exceeds its cost of capital, then the project’s NPV must be

positive.

e.

If Project A has a higher IRR than Project B, then Project A must have the lower NPV.

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV and IRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:09 AM

JFND-GO4G-EO4D-OQNF

41. Which of the following statements is CORRECT?

a.

If two projects are mutually exclusive, then they are likely to have multiple IRRs.

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV and IRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:08 AM

JFND-GO4G-EO4D-OQNG

GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

b.

If a project is independent, then it cannot have multiple IRRs.

c.

Multiple IRRs can occur only if the signs of the cash flows change more than once.

d.

If a project has two IRRs, then the smaller one is the one that is most relevant, and it should be accepted and

relied upon.

e.

For a project to have more than one IRR, then both IRRs must be greater than the cost of capital.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

Multiple IRRs

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:09 AM

42. Which of the following statements is CORRECT?

a.

The NPV method assumes that cash flows will be reinvested at the risk-free rate, while the IRR method

assumes reinvestment at the IRR.

b.

The NPV method assumes that cash flows will be reinvested at the cost of capital, while the IRR method

assumes reinvestment at the risk-free rate.

c.

The NPV method does not consider all relevant cash flows, particularly cash flows beyond the payback period.

d.

The IRR method does not consider all relevant cash flows, particularly cash flows beyond the payback period.

e.

The NPV method assumes that cash flows will be reinvested at the cost of capital, while the IRR method

assumes reinvestment at the IRR.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

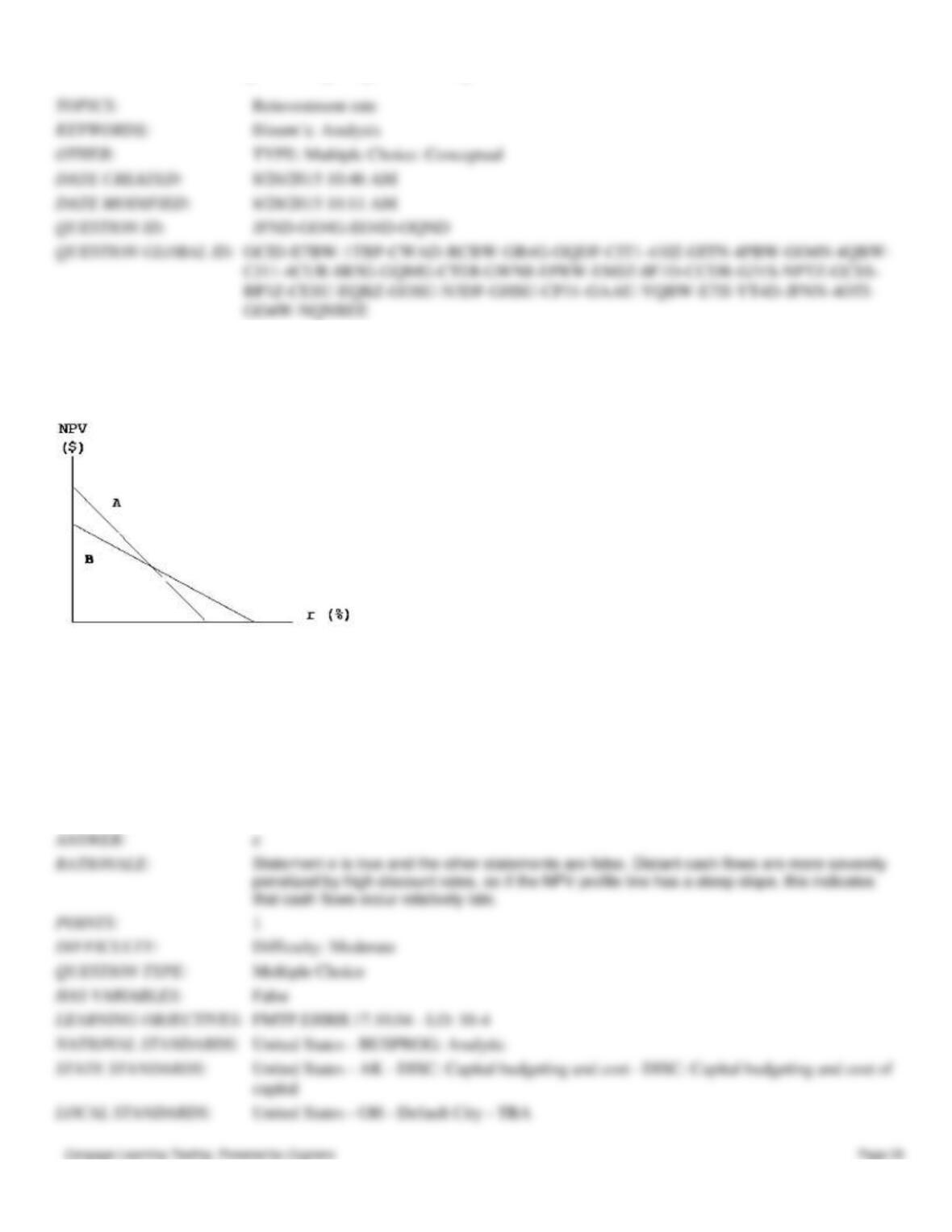

43. Projects A and B have identical expected lives and identical initial cash outflows (costs). However, most of one

project’s cash flows come in the early years, while most of the other project’s cash flows occur in the later years. The two

NPV profiles are given below:

Which of the following statements is CORRECT?

a.

More of Project B’s cash flows occur in the later years.

b.

We must have information on the cost of capital in order to determine which project has the larger early cash

flows.

c.

The NPV profile graph is inconsistent with the statement made in the problem.

d.

The crossover rate, i.e., the rate at which Projects A and B have the same NPV, is greater than either project’s

IRR.

e.

More of Project A’s cash flows occur in the later years.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

Reinvestment rate

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:11 AM

GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

44. Projects S and L are both normal projects with an initial cost of $10,000, followed by a series of positive cash inflows.

Project S’s undiscounted net cash flows total $20,000, while L’s total undiscounted flows are $30,000. At a cost of capital

of 10%, the two projects have identical NPVs. Which project’s NPV is more sensitive to changes in the cost of capital?

a.

Project L.

b.

Both projects are equally sensitive to changes in the cost of capital since their NPVs are equal at all costs of

capital.

c.

Neither project is sensitive to changes in the discount rate, since both have NPV profiles that are horizontal.

d.

The solution cannot be determined because the problem gives us no information that can be used to determine

the projects’ relative IRRs.

e.

Project S.

a

Difficulty: Moderate

Multiple Choice

False

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:12 AM

JFND-GO4G-EO4D-OQB1

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/26/2015 10:46 AM

JFND-GO4G-EO4D-OQBU

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

45. Projects C and D both have normal cash flows and are mutually exclusive. Project C has a higher NPV if the cost of

capital is less than 12%, whereas Project D has a higher NPV if the cost of capital exceeds 12%. Which of the following

statements is CORRECT?

a.

Project D is probably larger in scale than Project C.

b.

Project C probably has a faster payback.

c.

Project C probably has a higher IRR.

d.

The crossover rate between the two projects is below 12%.

e.

Project D probably has a higher IRR.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:13 AM

46. The cost of capital for two mutually exclusive projects that are being considered is 8%. Project K has an IRR of 20%

while Project R’s IRR is 15%. The projects have the same NPV at the 8% current cost of capital. However, you believe

that money costs and thus your cost of capital will also increase. You also think that the projects will not be funded until

the cost of capital has increased, and their cash flows will not be affected by the change in economic conditions. Under

these conditions, which of the following statements is CORRECT?

a.

You should delay a decision until you have more information on the projects, even if this means that a

competitor might come in and capture this market.

b.

You should recommend Project R, because at the new cost of capital it will have the higher NPV.

c.

You should recommend Project K, because at the new cost of capital it will have the higher NPV.

d.

You should recommend Project K because it has the higher IRR and will continue to have the higher IRR even

at the new cost of capital.

e.

You should reject both projects because they will both have negative NPVs under the new conditions.

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

47. The cost of capital for two mutually exclusive projects that are being considered is 12%. Project K has an IRR of 20%

while Project R’s IRR is 15%. The projects have the same NPV at the 12% current cost of capital. Interest rates are

currently high. However, you believe that money costs and thus your cost of capital will soon decline. You also think that

the projects will not be funded until the cost of capital has decreased, and their cash flows will not be affected by the

change in economic conditions. Under these conditions, which of the following statements is CORRECT?

a.

You should delay a decision until you have more information on the projects, even if this means that a

competitor might come in and capture this market.

b.

You should recommend Project R, because at the new cost of capital it will have the higher NPV.

c.

You should recommend Project K, because at the new cost of capital it will have the higher NPV.

d.

You should recommend Project R because it will have both a higher IRR and a higher NPV under the new

conditions.

e.

You should reject both projects because they will both have negative NPVs under the new conditions.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

TYPE: Multiple Choice: Conceptual

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:14 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

48. Which of the following statements is CORRECT?

a.

If Project A’s IRR exceeds Project B’s, then A must have the higher NPV.

b.

A project’s MIRR can never exceed its IRR.

c.

If a project with normal cash flows has an IRR less than the cost of capital, the project must have a positive

NPV.

d.

If the NPV is negative, the IRR must also be negative.

e.

If a project with normal cash flows has an IRR greater than the cost of capital, the project must also have a

positive NPV.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV, IRR, and MIRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:16 AM

JFNN-4OTI-GO4W-NQNBEE

49. Which of the following statements is CORRECT?

a.

The IRR method can never be subject to the multiple IRR problem, while the MIRR method can be.

b.

One reason some people prefer the MIRR to the regular IRR is that the MIRR is based on a generally more

reasonable reinvestment rate assumption.

c.

The higher the cost of capital, the shorter the discounted payback period.

d.

The MIRR method assumes that cash flows are reinvested at the crossover rate.

e.

The MIRR and NPV decision criteria can never conflict.

8/26/2015 10:46 AM

8/28/2015 10:16 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

50. Which of the following statements is CORRECT?

a.

To find the MIRR, we first compound cash flows at the regular IRR to find the TV, and then we discount the

TV at the cost of capital to find the PV.

b.

The NPV and IRR methods both assume that cash flows can be reinvested at the cost of capital. However, the

MIRR method assumes reinvestment at the MIRR itself.

c.

If two projects have the same cost, and if their NPV profiles cross in the upper right quadrant, then the project

with the higher IRR probably has more of its cash flows coming in the later years.

d.

If two projects have the same cost, and if their NPV profiles cross in the upper right quadrant, then the project

with the lower IRR probably has more of its cash flows coming in the later years.

e.

For a project with normal cash flows, any change in the cost of capital will change both the NPV and the IRR.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV, IRR, and MIRR

8/26/2015 10:46 AM

8/28/2015 10:18 AM

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV, IRR, and MIRR

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:17 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

51. Which of the following statements is CORRECT?

a.

One advantage of the NPV over the IRR is that NPV assumes that cash flows will be reinvested at the cost of

capital, whereas IRR assumes that cash flows are reinvested at the IRR. The NPV assumption is generally

more appropriate.

b.

One advantage of the NPV over the MIRR method is that NPV takes account of cash flows over a project’s full

life whereas MIRR does not.

c.

One advantage of the NPV over the MIRR method is that NPV discounts cash flows whereas the MIRR is

based on undiscounted cash flows.

d.

Since cash flows under the IRR and MIRR are both discounted at the same rate (the cost of capital), these two

methods always rank mutually exclusive projects in the same order.

e.

One advantage of the NPV over the IRR is that NPV takes account of cash flows over a project’s full life

whereas IRR does not.

Difficulty: Moderate

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

Capital budgeting: NPV

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:19 AM

52. Projects S and L are equally risky, mutually exclusive, and have normal cash flows. Project S has an IRR of 15%,

while Project L’s IRR is 12%. The two projects have the same NPV when the cost of capital is 7%. Which of the

following statements is CORRECT?

a.

If the cost of capital is 6%, Project S will have the higher NPV.

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

b.

If the cost of capital is 13%, Project S will have the lower NPV.

c.

If the cost of capital is 10%, both projects will have a negative NPV.

d.

Project S’s NPV is more sensitive to changes in cost of capital than Project L’s.

e.

If the cost of capital is 10%, both projects will have positive NPVs.

Difficulty: Moderate

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:20 AM

53. Lancaster Corp. is considering two equally risky, mutually exclusive projects, both of which have normal cash flows.

Project A has an IRR of 11%, while Project B’s IRR is 14%. When the cost of capital is 8%, the projects have the same

NPV. Given this information, which of the following statements is CORRECT?

a.

If the cost of capital is 9%, Project A’s NPV will be higher than Project B’s.

b.

If the cost of capital is 6%, Project B’s NPV will be higher than Project A’s.

c.

If the cost of capital is greater than 14%, Project A’s IRR will exceed Project B’s.

d.

If the cost of capital is 9%, Project B’s NPV will be higher than Project A’s.

e.

If the cost of capital is 13%, Project A’s NPV will be higher than Project B’s.

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

54. You are considering two mutually exclusive, equally risky, projects. Both have IRRs that exceed the cost of capital.

Which of the following statements is CORRECT? Assume that the projects have normal cash flows, with one outflow

followed by a series of inflows.

a.

If the cost of capital is greater than the crossover rate, then the IRR and the NPV criteria will not result in a

conflict between the projects. The same project will rank higher by both criteria.

b.

If the cost of capital is less than the crossover rate, then the IRR and the NPV criteria will not result in a

conflict between the projects. The same project will rank higher by both criteria.

c.

For a conflict to exist between NPV and IRR, the initial investment cost of one project must exceed the cost of

the other.

d.

For a conflict to exist between NPV and IRR, one project must have an increasing stream of cash flows over

time while the other has a decreasing stream. If both sets of cash flows are increasing or decreasing, then it

would be impossible for a conflict to exist, even if one project is larger than the other.

e.

If the two projects’ NPV profiles do not cross, then there will be a sharp conflict as to which one should be

selected.

Difficulty: Challenging

Multiple Choice

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:21 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

55. Consider two projects, X and Y. Project X’s IRR is 19% and Project Y’s IRR is 17%. The projects have the same risk

and the same lives, and each has constant cash flows during each year of their lives. If the cost of capital is 10%, Project Y

has a higher NPV than X. Given this information, which of the following statements is CORRECT?

a.

The crossover rate must be greater than 10%.

b.

If the cost of capital is 8%, Project X will have the higher NPV.

c.

If the cost of capital is 18%, Project Y will have the higher NPV.

d.

Project X is larger in the sense that it has the higher initial cost.

e.

The crossover rate must be less than 10%.

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:23 AM

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:22 AM

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

56. You are on the staff of O’Hara Inc. The CFO believes project acceptance should be based on the NPV, but Andrew

O’Hara, the president, insists that no project should be accepted unless its IRR exceeds the project’s risk-adjusted cost of

capital. Now you must make a recommendation on a project that has a cost of $15,000 and two cash flows: $110,000 at

the end of Year 1 and −$100,000 at the end of Year 2. The president and the CFO both agree that the appropriate cost of

capital for this project is 10%. At 10%, the NPV is $2,355.37, but you find two IRRs, one at 6.33% and one at 527%, and

a MIRR of 11.32%. Which of the following statements best describes your optimal recommendation, i.e., the analysis and

recommendation that is best for the company and least likely to get you in trouble with either the CFO or the president?

a.

You should recommend that the project be rejected because, although its NPV is positive, it has an IRR that is

less than the cost of capital.

b.

You should recommend that the project be accepted because (1) its NPV is positive and (2) although it has two

IRRs, in this case it would be better to focus on the MIRR, which exceeds the cost of capital. You should

explain this to the president and tell him that the firm’s value will increase if the project is accepted.

c.

You should recommend that the project be rejected. Although its NPV is positive it has two IRRs, one of

which is less than the cost of capital, which indicates that the firm’s value will decline if the project is

accepted.

d.

You should recommend that the project be rejected because, although its NPV is positive, its MIRR is less

than the cost of capital, and that indicates that the firm’s value will decline if it is accepted.

e.

You should recommend that the project be rejected because its NPV is negative and its IRR is less than the

cost of capital.

False

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

GO4W-NQNBEE

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

57. Consider projects S and L. Both have normal cash flows, and the projects have the same risk, hence both are evaluated

with the same cost of capital, 10%. However, S has a higher IRR than L. Which of the following statements is

CORRECT?

a.

If Project S has a positive NPV, Project L must also have a positive NPV.

b.

If the cost of capital falls, each project’s IRR will increase.

c.

If the cost of capital increases, each project’s IRR will decrease.

d.

If Projects S and L have the same NPV at the current cost of capital, 10%, then Project L, the one with the

lower IRR, would have a higher NPV if the cost of capital used to evaluate the projects declined.

e.

Project S must have a higher NPV than Project L.

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:26 AM

58. Which of the following statements is CORRECT? Assume that all projects being considered have normal cash flows

and are equally risky.

a.

If a project’s IRR is equal to its cost of capital, then under all reasonable conditions, the project’s IRR must be

negative.

Ch 10 The Basics of Capital Budgeting: Evaluating Cash Flows

b.

If a project’s IRR is equal to its cost of capital, then under all reasonable conditions the project’s NPV must be

zero.

c.

There is no necessary relationship between a project’s IRR, its cost of capital, and its NPV.

d.

When evaluating mutually exclusive projects, those projects with relatively long lives will tend to have

relatively high NPVs when the cost of capital is relatively high.

e.

If a project’s IRR is equal to its cost of capital, then, under all reasonable conditions, the project’s NPV must be

negative.

Difficulty: Challenging

Multiple Choice

FMTP.EHRH.17.10.04 – LO: 10-4

United States – BUSPROG: Analytic

United States – AK – DISC: Capital budgeting and cost – DISC: Capital budgeting and cost of

capital

United States – OH – Default City – TBA

NPV profiles

TYPE: Multiple Choice: Conceptual

8/26/2015 10:46 AM

8/28/2015 10:27 AM

59. Clifford Company is choosing between two projects. The larger project has an initial cost of $100,000, annual cash

flows of $30,000 for 5 years, and an IRR of 15.24%. The smaller project has an initial cost of $50,000, annual cash flows

of $16,000 for 5 years, and an IRR of 16.63%. The projects are equally risky. Which of the following statements is

CORRECT?

a.

Since the smaller project has the higher IRR, the two projects’ NPV profiles will cross, and the larger project

will look better based on the NPV at all positive values of the cost of capital.

b.

If the company uses the NPV method, it will tend to favor smaller, shorter-term projects over larger, longer-

term projects, regardless of how high or low the cost of capital is.

c.

Since the smaller project has the higher IRR but the larger project has the higher NPV at a zero discount rate,

the two projects’ NPV profiles will cross, and the larger project will have the higher NPV if the cost of capital

is less than the crossover rate.

d.

Since the smaller project has the higher IRR and the larger NPV at a zero discount rate, the two projects’ NPV

profiles will cross, and the smaller project will look better if the cost of capital is less than the crossover rate.

e.

Since the smaller project has the higher IRR, the two projects’ NPV profiles cannot cross, and the smaller

project’s NPV will be higher at all positive values of the cost of capital.