Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 18

Ex. 72 (Cont.)

The balance in the Accounts Payable control account of $41,580 has been verified as correct.

Also assume that the journals references in the Post Ref. columns of the accounts payable

subsidiary ledger have been verified as correct.

Instructions

Determine the errors in the preceding accounts payable subsidiary accounts and prepare a

corrected schedule of accounts payable.

Ex. 73

On October 1, the accounts receivable control account balance in the general ledger of Helms

Company was $9,000. The accounts receivable subsidiary ledger contained the following detailed

customer balances: Able $2,000, Bravo $1,600, Charlie $3,600, and Gamma $1,800. The

following information is available from the company’s special journals for the month of October:

Cash Receipts Journal: Cash received from Charlie $1,900, from Able $2,600, from Sigma

$1,700, and from Bravo $1,500.

Sales Journal: Sales to Sigma $2,300, to Charlie $2,700, to Able $2,300, and to Gamma $2,000.

Additionally, Charlie returned defective merchandise for credit for $900. Able returned defective

merchandise for $600 which he had purchased for cash.

Subsidiary Ledgers and Special Journals

G – 19

Ex. 73 (Cont.)

Instructions

(a) Using T-accounts for Accounts Receivable Control and the detail customer accounts, post

the activity for the month of December.

(b) Reconcile the accounts receivable control account with the subsidiary ledger by preparing a

detail list of customer balances at December 31.

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 20

Ex. 74

Sadat Company uses a sales journal, a cash receipts journal, and a general journal to record

transactions with its customers. Record the following transactions in the appropriate journals. The

cost of all merchandise sold was 70% of the sales price.

July 2 Sold merchandise for $20,000 to B. Rock on account. Credit terms 2/10, n/30. Sales

invoice No. 100.

July 5 Received a check for $800 from R. Budd in payment of his account.

July 8 Sold merchandise to F. Truman for $700 cash.

July 10 Received a check in payment of Sales invoice No. 100 from B. Rock minus the 2%

discount.

July 15 Sold merchandise for $9,000 to J. Weilmann on account. Credit terms 2/10, n/30.

Sales invoice No. 101.

July 18 Borrowed $25,000 cash from United Bank signing a 6-month, 10% note.

July 20 Sold merchandise for $15,000 to C. Warden on account. Credit terms 2/10, n/30.

Sales invoice No. 102.

July 25 Issued a credit memorandum for $600 to C. Warden as an allowance for damaged

merchandise previously sold on account.

July 31 Received a check from J. Weilmann for $5,000 as payment on account.

SADAT COMPANY

Sales Journal

S1

——————————————————————————————————————————

Invoice Acct. Rec. Dr. C. of G.S. Dr.

Date Account Debited No. Ref. Sales Rev. Cr. Inventory Cr.

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

SADAT COMPANY

General Journal

G1

——————————————————————————————————————————

Date Explanations Ref. Debit Credit

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

——————————————————————————————————————————

Subsidiary Ledgers and Special Journals

G – 21

Ex. 74 (Cont.)

SADAT COMPANY

Cash Receipts Journal

CR1

———————————————————————————————————————————

Sales Accounts Other C. of G.S. Dr.

Accounts Cash Discounts Rec. Sales Rev. Accounts Inventory Cr.

Date Credited Ref. Dr. Dr. Cr. Cr. Cr.

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

Ans: N/A, LO: 2, Bloom: AP, Difficulty: Medium, Min: 20, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Solution 74 (20 min.)

———————————————————————————————————————————

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 22

Solution 74 (Cont.)

Ex. 75

Lighthouse Ltd. uses a single-column purchases journal, a cash payments journal, and a general

journal to record transactions with its suppliers and others. Record the following transactions in

the appropriate journals.

Transactions

Oct. 5 Purchased merchandise on account for $35,000 from O’Connor Company. Terms:

2/10, n/30; FOB shipping point.

Oct. 6 Paid $7,200 to Freedom Insurance Company for a two-year fire insurance policy.

Oct. 8 Purchased store supplies on account for $700 from Martin Supply Company. Terms:

2/10, n/30.

Oct. 11 Purchased merchandise on account for $14,000 from Darlington LLC. Terms: 2/10,

n/30; FOB shipping point.

Oct. 13 Issued a debit memorandum for $2,000 to Darlington LLC for merchandise

purchased on October 11 and returned because of damage.

Oct. 15 Paid O’Connor Company for merchandise purchased on October 5, less discount.

Oct. 16 Purchased merchandise for $8,000 cash from Kaye Company.

Oct. 21 Paid Darlington LLC for merchandise purchased on October 11, less merchandise

returned on October 13, less discount.

Oct. 25 Purchased merchandise on account for $22,000 from Willard Company. Terms:

2/10, n/30; FOB shipping point.

Oct. 31 Purchased office equipment for $30,000 cash from Wilcoxen Office Supply

Company.

Subsidiary Ledgers and Special Journals

G – 23

Ex. 75 (Cont.)

LIGHTHOUSE LTD.

Purchases Journal

P1

———————————————————————————————————————————

Inventory. Dr.

Date Account Credited Ref. Accounts Payable Cr.

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

LIGHTHOUSE LTD.

General Journal

G1

———————————————————————————————————————————

Date Explanation Ref. Debit Credit

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

LIGHTHOUSE LTD.

Cash Payments Journal

CP1

———————————————————————————————————————————

Other Accounts

Accounts Accounts Payable Inventory Cash

Date Debited Ref. Dr. Dr. Cr. Cr.

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

———————————————————————————————————————————

Ans: N/A, LO: 2, Bloom: AP, Difficulty: Medium, Min: 20, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 24

Solution 75 (20 min.)

Subsidiary Ledgers and Special Journals

G – 25

Ex. 76

Below are some typical transactions incurred by Kuo Company.

____ 1. Purchase of merchandise on account.

____ 2. Collection on account from customers.

____ 3. Payment of employee’s wages.

____ 4. Sales of merchandise for cash.

____ 5. Close Income Summary to Retained Earnings.

____ 6. Adjusting entry for depreciation on machinery.

____ 7. Payment of creditors on account.

____ 8. Purchase of office equipment on credit.

____ 9. Sales discount taken on goods sold on credit.

____ 10. Sales of merchandise on account.

____ 11. Purchase of a delivery truck for cash.

____ 12. Return of merchandise purchased on credit.

____ 13. Payment of rent in advance.

____ 14. Adjusting entry for accrued interest expense.

____ 15. Purchase of office supplies for cash.

For each transaction, indicate by the code letter the appropriate journal where the transaction

would be journalized.

CR — Cash Receipts Journal

CP — Cash Payments Journal

S — Sales Journal

P — Single-Column Purchases Journal

G — General Journal

Ans: N/A, LO: 2, Bloom: AN, Difficulty: Medium, Min: 12, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Solution 76 (12 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 26

Ex. 77

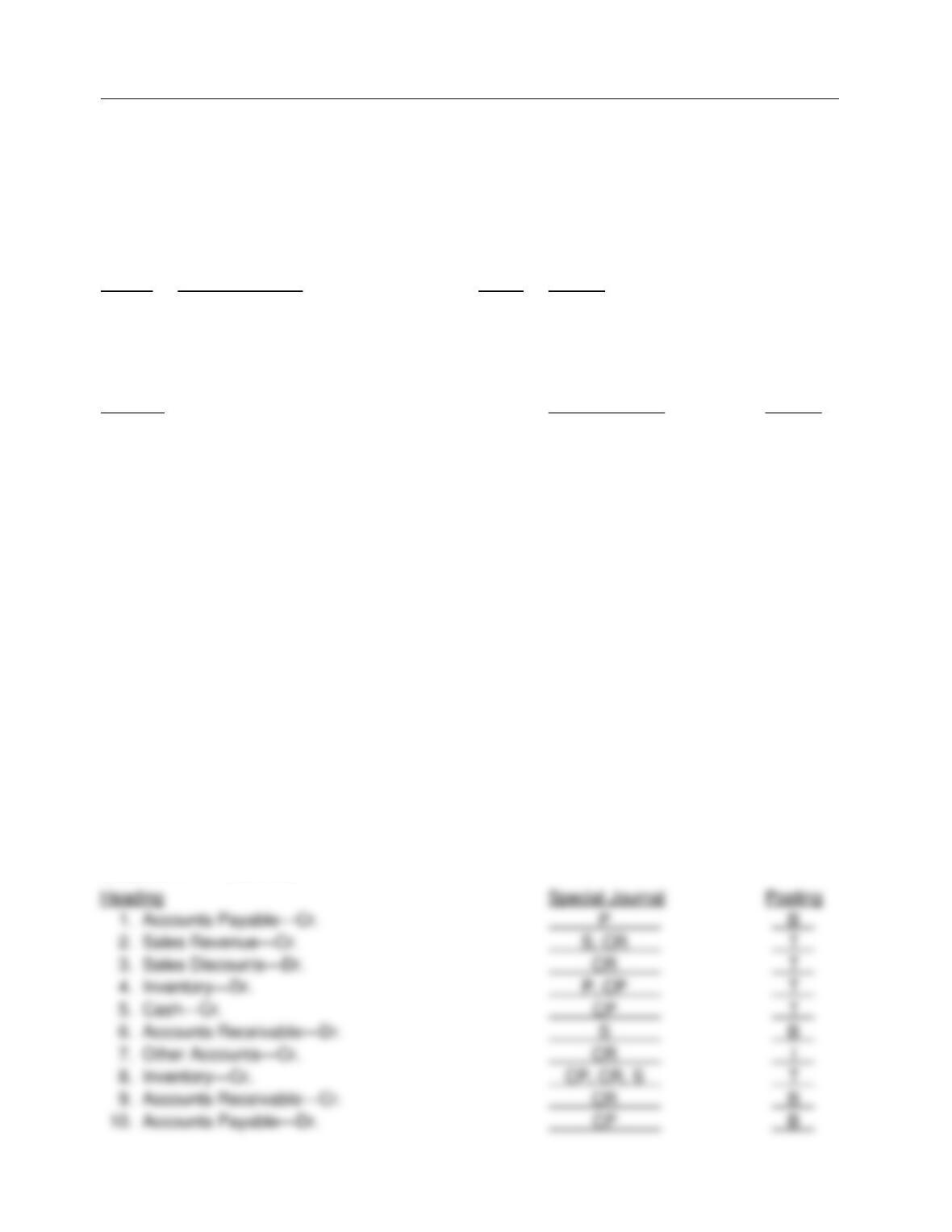

Listed below are various column headings that may appear in special journals. Using the

following code letters, identify for each column heading (1) the special journal where the column

heading would appear, and (2) whether the amounts entered under the column heading would be

posted in total, individually, or both in total and individually. (Note: column headings may appear

in more than one special journal)

Code: Special Journals Code: Posting

S = Sales journal I = Individual posting

P = Single-column purchases journal T = Total posting

CR = Cash receipts journal B = Both individual and total posting

CP = Cash payments journal

Heading Special Journal Posting

1. Accounts Payable—Cr. ___________ ___

2. Sales Revenue—Cr. ___________ ___

3. Sales Discounts—Dr. ___________ ___

4. Inventory—Dr. ___________ ___

5. Cash—Cr. ___________ ___

6. Accounts Receivable—Dr. ___________ ___

7. Other Accounts—Cr. ___________ ___

8. Inventory—Cr. ___________ ___

9. Accounts Receivable—Cr. ___________ ___

10. Accounts Payable—Dr. ___________ ___

Ans: N/A, LO: 3, Bloom: AN, Difficulty: Medium, Min: 15, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Solution 77 (15 min.)

Subsidiary Ledgers and Special Journals

G – 27

Ex. 78

Sirius LLC uses four special journals, (cash receipts, cash payments, sales, and purchases

journal) in addition to a general journal. On November 1, 2013, the control accounts in the

general ledger had the following balances: Cash $12,000, Accounts Receivable $200,000 and

Accounts Payable $42,000. Selected information on the final line of the special journals for the

month of November is presented below:

Cash Receipts Journal:

Sales Accounts Sales Other Accounts

Cash Discounts Receivable Rev. Cr. C. of G. S. Dr.

Dr. Dr. Cr. Cr. Acct. Ref. Amount Inventory Cr.

? $600 $6,400 $31,000 (X) $1,000 $17,400

Cash Payments Journal:

Other Accounts Accounts

Dr. Payable Supplies Inventory Cash

Acct. Ref. Amount Dr. Dr. Cr. Cr.

(X) $1,600 ? $2,400 $700 $19,600

Purchases Journal:

Accounts Other Accounts

Payable Inventory Supplies Dr.

Cr. Dr. Dr. Acct. Ref. Amount

? $36,000 $1,450 (X) $3,300

Additional Data:

The Sales Journal total was $45,000. A customer returned merchandise for credit for $360 and

Leo Company returned store supplies to a supplier for credit for $400.

Instructions

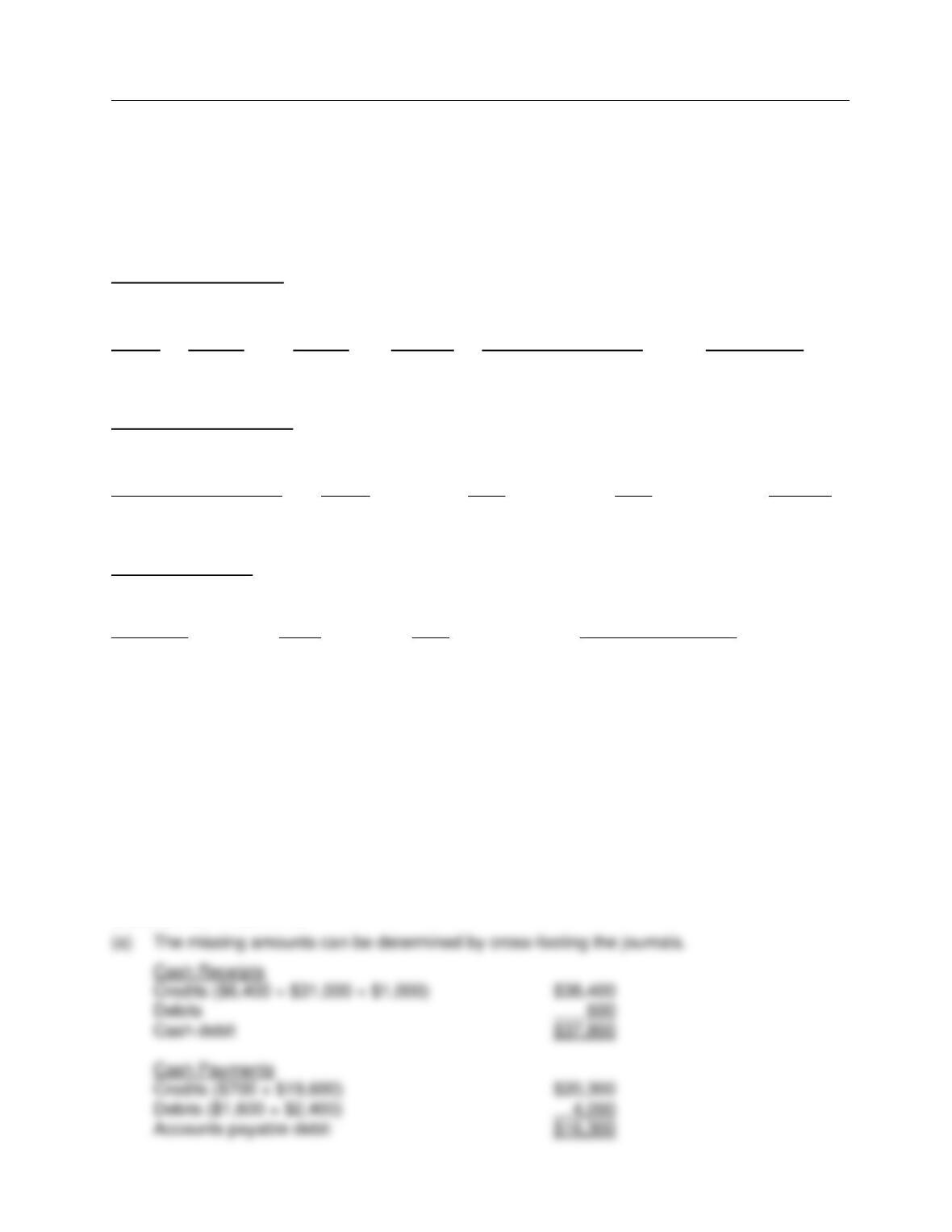

(a) Determine the missing amounts in the special journals.

(b) Determine the balances in the general ledger accounts (Cash, Accounts Receivable, and

Accounts Payable) at the end of November.

Ans: N/A, LO: 3, Bloom: AN, Difficulty: Medium, Min: 20, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Solution 78 (20 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 28

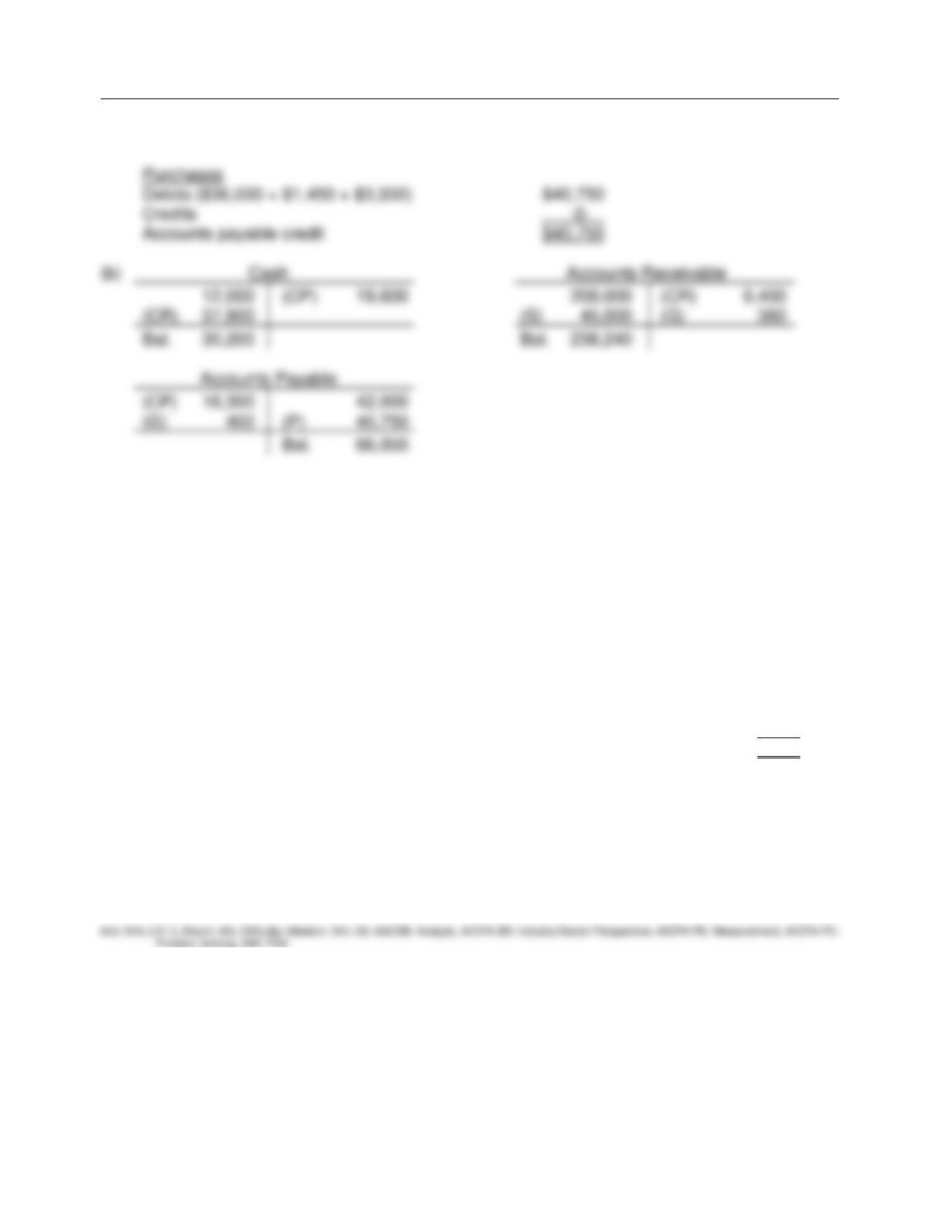

Solution 78 (Cont.)

Ex. 79

Wood Furnishings Inc. began business on April 1. The sales journal, as it appeared at the end of

the month, follows:

SALES JOURNAL Page 1

———————————————————————————————————————————

Invoice Post.

Date Account Debited Number Ref. Amount

———————————————————————————————————————————

Apr. 5 Jack Sago 10001 475

11 Leo Lauer 10002 535

16 Jack Sago 10003 818

19 Christy Sage 10004 447

26 Irene Walz 10005 1,884

4,159

1. Open general ledger T-accounts for Accounts Receivable (No. 112) and Sales (No. 401) and

an accounts receivable subsidiary T-account ledger with an account for each customer. Make

the appropriate postings from the sales journal. Fill in the appropriate posting references in

the sales journal above.

2. Prove the accounts receivable subsidiary ledger by preparing a schedule of accounts

receivable.

Subsidiary Ledgers and Special Journals

G – 29

Solution 79 (20 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 30

Ex. 80

CASH PAYMENTS JOURNAL Page 45

———————————————————————————————————————————

Other Accounts

Ck. Account Post. Accounts Payable Inventory Cash

Date No. Debited Ref. Dr. Dr. Cr. Cr.

———————————————————————————————————————————

2013

Jan. 4 659 N & R Inc, (a) 4,000 40 3,960

11 660 Prepaid Rent (b) 2,000 2,000

13 661 Inventory. (c) 565 565

14 662 Dividends (d) 1,000 1,000

18 663 Keene (e) 2,300 2,300

20 664 Inventory. (f) 450 450

29 665 Equipment (g) 2,400 2,400

6,415 6,300 40 12,675

(h) (i) (j) (k)

Using the cash payments journal above, identify each of the posting references indicated by a

letter, as representing:

(1) a posting to a general ledger account.

(2) a posting to a subsidiary ledger account.

(3) that no posting is required.

Ans: N/A, LO: 3, Bloom: AN, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Measurement, AICPA PC:

Problem Solving, IMA: FSA

Solution 80 (10 min.)

Ex. 81

Shown below is a page from a special journal.

1. What is the name of this journal?

2. Give an explanation for each of the transactions in this journal.

3. Explain the following:

(a) the numbers under the bottom lines.

(b) the checks entered into the Post. Ref. column.

(c) the numbers 113 and 416 in the Post. Ref. column.

(d) the (x) below the Other Accounts column.

Subsidiary Ledgers and Special Journals

G – 31

———————————————————————————————————————————

Sales Accounts Sales Other C.of G.S. Dr.

Accounts Post Cash Discounts Receivable Rev. Accounts Inventory Cr.

Date Credited Ref. Dr. Dr. Cr. Cr. Cr.

———————————————————————————————————————————

May 27 Jim Cale 980 20 1,000

Ex. 81 (Cont.)

28 Notes Receivable 113 3,000

Interest Revenue 416 3,360 360

29 370 370 260

31 Jim McHugh 400 400

5,110 20 1,400 370 3,360 260

(111) (412) (114) (411) (x) (505)(120)

Ans: N/A, LO: 3, Bloom: AN, Difficulty: Medium, Min: 10, AACSB: Analytic, AICPA BB: Industry/Sector Perspective, AICPA FN: Research, AICPA PC:

Problem Solving, IMA: Business Applications

Solution 81 (10 min.)

Test Bank for Accounting: Tools for Business Decision Making, Fifth Edition

G – 32

COMPLETION STATEMENTS

82. The accounts receivable _____________ provides detailed information about customer

accounts which is summarized in one ______________ account in the general ledger.

83. If a certain type of transaction occurs with great frequency, it is more efficient to create a

______________ to record that type of transaction.

84. If a company maintains special journals, sales of merchandise on credit should be

recorded in a _______________ whereas sales of merchandise for cash should be

recorded in the _______________.

85. The use of special journals often saves time in the _______________ process.

86. The entries in the Accounts Receivable Credit column of the cash receipts journal must be

posted _______________ to the accounts in the accounts receivable subsidiary ledger

and in _______________ to the control account in the general ledger.

87. Transactions that cannot be entered in a special journal are recorded in the

_______________, and if control and subsidiary accounts are involved, there must be a

_______________ posting.

Answers to Completion Statements

Subsidiary Ledgers and Special Journals

G – 33

MATCHING

88. Match the items below by entering the appropriate code letter in the space provided.

A. Accounts payable ledger D. Subsidiary ledger

B. Columnar journal E. Control account

C. Special journals

____ 1. A general ledger account that summarizes detailed information in a subsidiary ledger.

____ 2. A subsidiary ledger that contains accounts with individual creditors.

____ 3. A special journal with more than one column.

____ 4. Detailed information about a group of accounts with a common characteristic.

____ 5. Used to record high volume, similar type transactions.

Answers to Matching

SHORT-ANSWER ESSAY

S-A E 89

At the end of the month, the accountant for Golden Company prepared a schedule of accounts

receivable from the accounts receivable subsidiary ledger. Its total did not agree with the balance

in the Accounts Receivable control account in the general ledger. Briefly describe the procedure

that should be followed in reconciling the two balances.