An individual investor has either sufficient wealth or sufficient borrowing capacity to

purchase or sell a substantial proportion of a given firm’s securities, so that investor’s

trades may affect the market value of these securities. This is an example of the

violation of which of the assumptions of an ideal capital market?

a. Capital Markets are frictionless

b. Homogeneous expectations

c. Atomistic competition

d. The firm has a fixed investment program

e. Once chosen, the firm’s financing is fixed

A _____________ merger involves the combination of two firms in unrelated

industries.

a. conglomerate

b. vertical

c. diagonal

d. horizontal

_______ has become an important means by which huge infrastructure projects are

privately financed.

a. Private placement financing

b. Infrastructure funding

c. Project finance

d. Country finance

Regarding corporate bonds, if the issuing firm does not pledge specific assets as

collateral, the bond is called a _______.

a. debenture

b. mortgage

c. chattel mortgage

d. note

Over the years 1981-2000, 4,770 nonfinancial firmsexited the U.S. markets for publicly

traded equity. Which of the following was the most frequent reason for a firm’s exit?

a. Merger or acquisition

b. Bankruptcy or liquidation

c. The firm reverted to private equity ownership

d. The firm changed its listing to a foreign stock exchange

All of the following were mentioned in the text as means by which the manager of a

firm may increase his or her compensation (on a self-serving basis) EXCEPT:

a. having the firm purchase his-her principal private residence.

b. excessive consumption of perquisites.

c. manipulation of earnings and dividends.

d. maximizing the size of the firm, rather than its value.

To preserve the value of a distressed firm, it is generally important for the firm to

continue operating throughout Chapter 11 proceedings. Generally, the firm’s current

management is allowed to run the firm during the proceedings under a restrictive

arrangement called

a. the value-preservation dictum.

b. debtor-in-possession.

c. managerial discretion.

d. trustee assignment.

In an equity carve-out, the parent of a multiple-subsidiary firm issues equity claims

against a particular subsidiary via a

a. private placement.

b. pro-rata distribution to the parent’s current stockholders.

c. public offering.

d. unit distribution.

Empirical evidence indicates that the majority of distressed public firms that do not

remain public:

a. file for Chapter 11 bankruptcy (reorganization).

b. file for Chapter 7 bankruptcy (liquidation).

c. are acquired.

d. undergo a going-private transaction (i.e., a buyout).

Underwriter generally places non-solicitation advertisements in the Wall Street Journal

and/or other important newspapers notifying the public of the availability of an issue.

These are called _______.

a. tombstone ads

b. headstone ads

c. notifications of availability

d. bond issue schedules

Some pre-IPO shareholders may wish to take the opportunity afforded by the IPO to

cash out some or all of their shares in the ___(i)___ portion of the IPO. IPO firms also

generally raise funds for the firm in the ___(ii)___ portion of the offering.

Bankruptcy risk plays a role in the propagation of recessions by:

a. causing a backlog in the caseloads of bankruptcy courts.

b. causing firms to increase capital expenditures as the economy begins to slow.

c. forcing firms to pay down debt.

d. straining the liquidity positions of both individuals and firms, both of which try to

avoid bankruptcy by maintaining liquidity.

In January, 2002, Jones Company issues a pure-discount bond with a promised payment

of X=$1000 that matures in T=5 years. The market price of the bond is P=$777. The

bond is default- risky. Specifically, the probability is 0.8 that Jones Company will pay

the full amount of X at maturity, and is 0.2 that the firm will default, in which case the

payoff to bondholders will be only $555. Calculate the bond’s promised yield to

maturity, y, and expected return to maturity, rD.

FORMULAS: y = [X/P]1/T“1; rD= [E(PAY)/P]1/T“1, where E(PAY)= p[X] + (1-p)[X”]

In a dual-class recapitalization (or “recap”), a firm

a. creates two classes of managersoperational and financial.

b. establishes two classes of securitiesdebt and equity.

c. establishes two classes of debt securitiessenior and subordinated.

d. creates a second class of common stock that has limited voting rights and generally a

preferential claim to the firm’s cash flows.

The literature emphasizes three motives for a buyout, including all of the following

EXCEPT:

a. to increase access to capital markets.

b. to increase managerial incentives.

c. to avert a takeover.

d. to realize tax-reduction benefits.

Capacity surpluses result in (i) product prices and (ii) profit margins.

Empirical evidence indicates that the market equity value of a multiple-segment firm

generally is ___(i)___ than the sum of the imputed market values of its individual

segments, a phenomenon called the ___(ii)___.

A _______ contract is a private, tailored, bilateral agreement between two parties in

which one party agrees to purchase, and the other to sell, a specified number of units of

a specified asset at a given future date and at a specified price.

a. swap

b. forward

c. futures

d. warrant

The _______ hypothesis posits that a firm may choose high leverage as a competitive

strategy to either win market share from rivals or to deter entry into the industry.

a. long-purse

b. strategic capital structure

c. competitive leverage

d. leverage aggressiveness

In a______, the claimants have already worked out the terms of the reorganization, and

basically file just to make the agreement official.

a. perfunctory filing

b. token filing

c. prepackaged bankruptcy

d. gesture filing

A _______ merger occurs between two firms that had been doing business in different

stages of the production process in a given industry.

a. conglomerate

b. vertical

c. diagonal

d. horizontal

TRUE or FALSE. Underwriter spreads on corporate bonds reflect substantial

economies of scale.

a. TRUE

b. FALSE

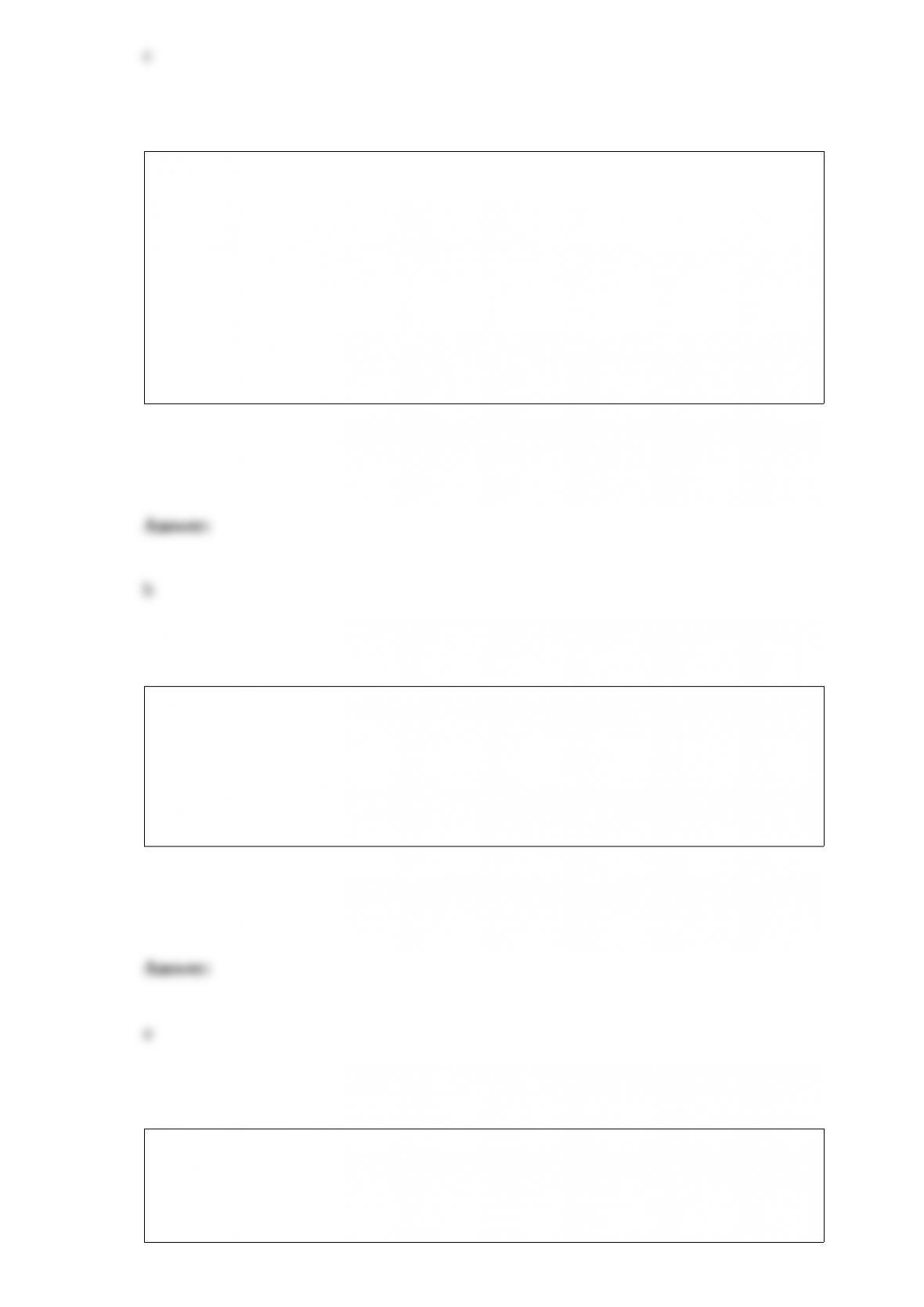

Suppose a firm wants to borrow $200 million for 10 years to fund capital expenditures,

and is considering the choice of a private placement with several insurance companies

or a public issue through an investment banking firm as underwriter. For simplicity, we

will assume that in either case the firm will issue pure-discount bonds. The insurance

companies demand interest at a rate of 10 percent, with a 3% flotation cost, while the

underwriter states that the interest cost will be 9.25% with 5% flotation costs. What is

the effective cost of the loan in each case? (ANSWERS: 10.325% and 9.785%,

respectively)

When the Federal Reserve Board’s open market committee buys T-bills, it is pursuing

a. contractionary monetary policy.

b. expansionary monetary policy.

c. fiscal discipline.

d. a policy of balancing the federal budget.

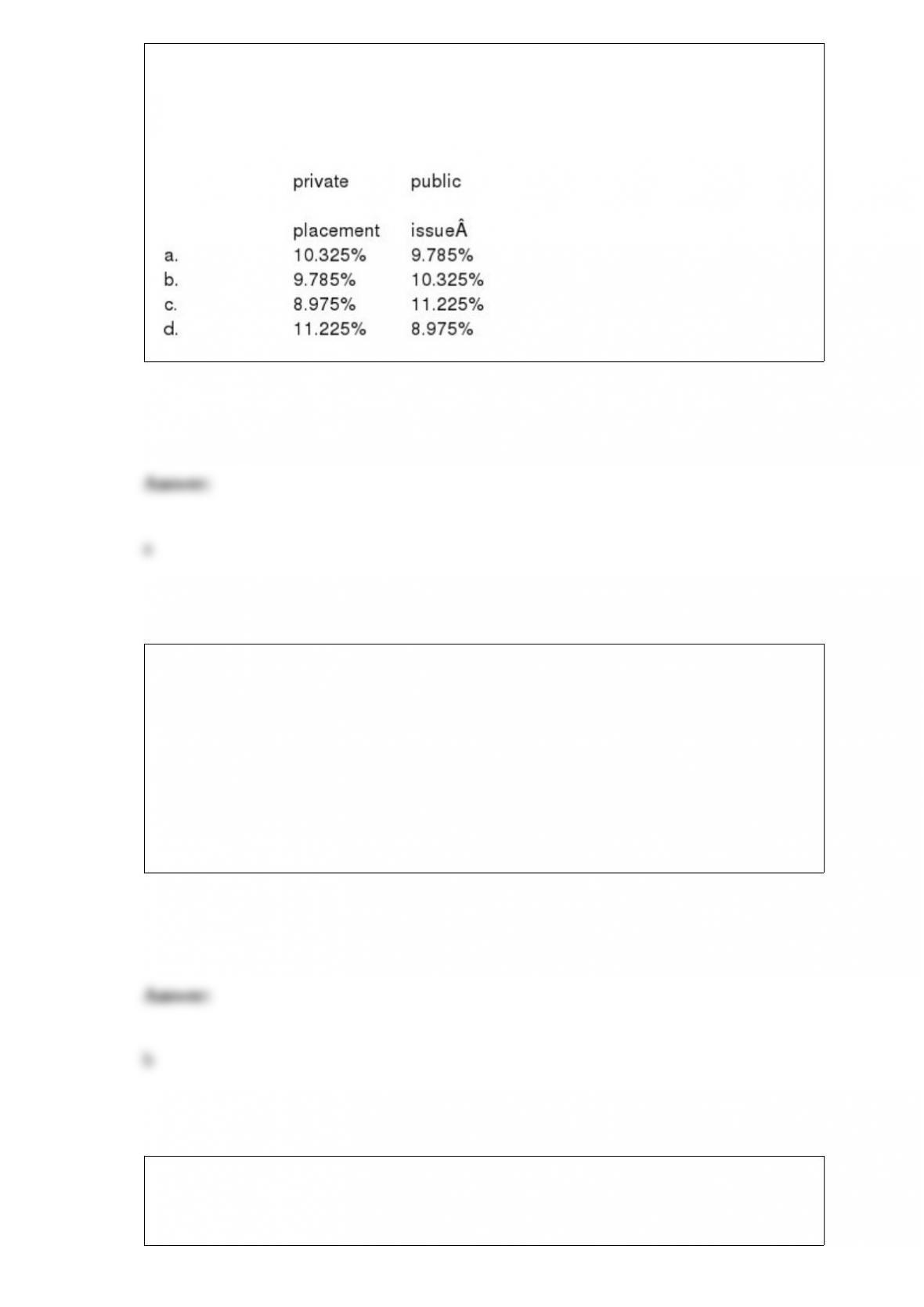

Suppose you develop a mutual fund that includes 500 NYSE stocks, all with equal

weights in the fund’s portfolio. The average standard deviation of the stocks is 36%, and

the average pair-wise correlation among the stocks is 0.40. What is your estimate of the

standard deviation of the fund’s portfolio?

a. 19.9%

b. 22.8%

c. 26.2%

d. 32.1%

FORMULA:

If one firm in a given industry declares bankruptcy, the market may lower the values of

other firms in a given industry because the reveals new, negative information about the

status of the industry as a whole. This phenomenon is called:

a. the contagion effect.

b. the intra-industry wealth transfer effect.

c. irrational behavior.

d. the sympathy effect.

A swap contract is in essence a portfolio, or series, of _________

a. forward contracts.

b. futures contracts.

c. repurchase agreements.

d. resettlement agreements.

TRUE or FALSE: In Chapter 11 proceedings, the court almost always strictly adheres

to the Absolute Priority Rule (APR).

a. TRUE

b. FALSE

According to the ___________ hypothesis, short-term assets should be financed with

short-term capital and long-term assets with long-term capital.

a. maturity matching

b. hedging

c. risk-return

d. capital asset

A typical ______ involves changing some aspect the firm’s internal corporate

governance, such as the structure or composition of a firm’s board of directors.

a. proxy contest

b. shareholder-initiated proposal

c. initiation procedure

d. takeover contest

Which of the following is NOT considered an advantage of going public?

a. Sharing corporate control with outsiders.

b. Better access to both equity and debt markets in the future

c. Better liquidity for the firm’s shares

d. The firm’s entrepreneurs have a chance to liquidate part of their investment and

diversify.

The current market value of the assets of levered firm ABC, Inc. is $100 million. The

annual standard deviation of returns on the assets is 30%. The firm’s capital structure

consists of equity and pure discount debt for which payment of $80 million is due in 5

years. The risk-free rate is 5%. Using the Black-Scholes Option Pricing Model to

calculate the value of the firm’s debt.

a. $44

b. $55

c. $66

d. $77

(The BSOPM formula and cumulative normal distribution function values must be

supplied.)

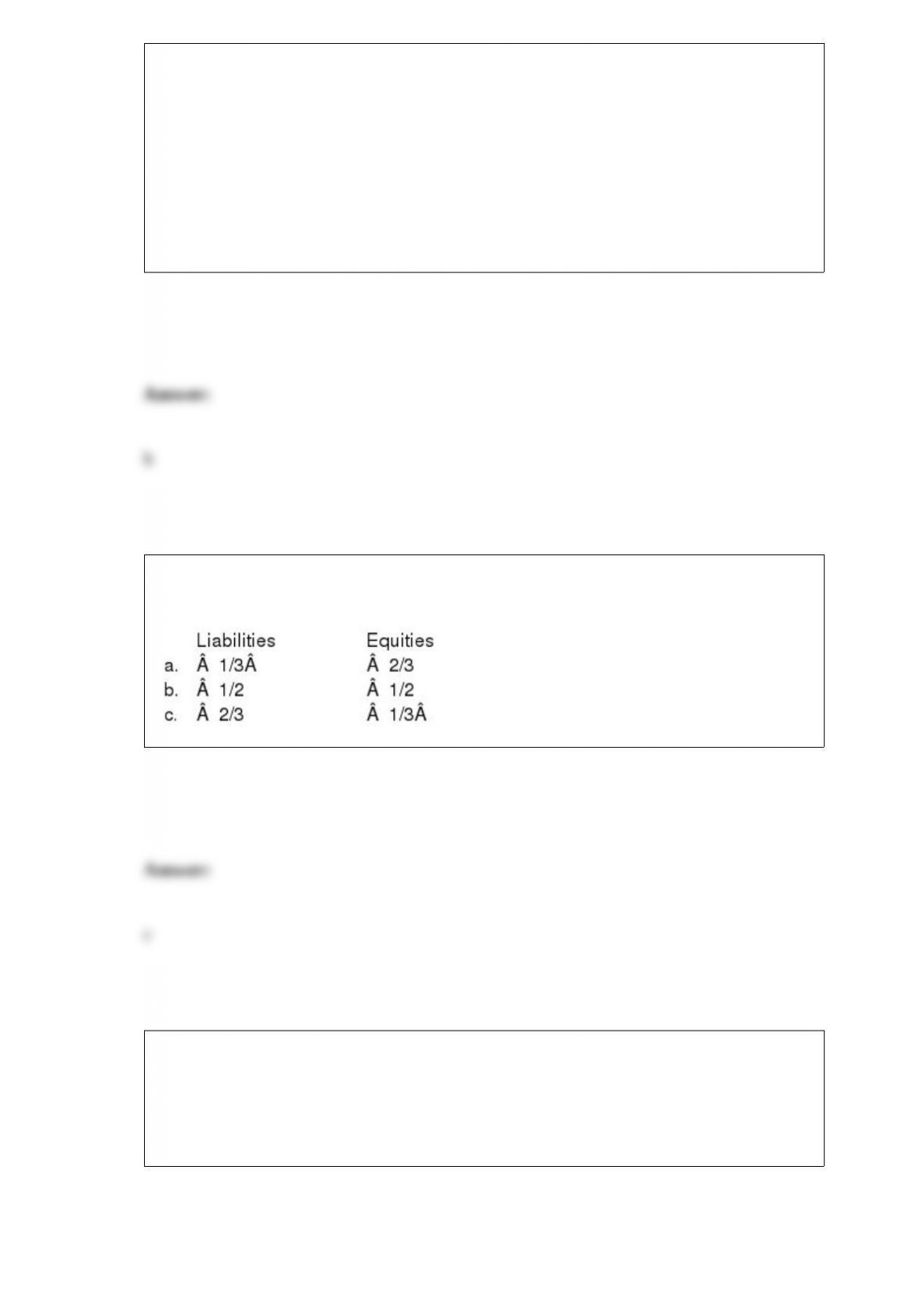

For public U.S. nonfinancial firms in composite, the fractions of liabilities (current plus

non- current), and equities (all in book values, year-end 2000) are approximately:

TRUE or FALSE. The dollar value of aggregate share repurchases has grown relative to

aggregate dividends in recent years.

a. TRUE

b. FALSE

Until now, Delaware East, Inc. has been an all-equity firm; its most recent market

equity value was $80 mn., and its cost of equity (and cost of assets) is 15%. Now, the

firm decides to increase its leverage by issuing $40 mn. in debt, with the proceeds being

used to pay a dividend to shareholders. The cost of the debt is rD=7%. What is the firm’s

new cost of equity capital, according to Modigliani and Miller’s Proposition II?

a. 15.33%

b. 18.20%

c 20.33%

d. 23.00%

FORMULA: rE= rA+ (D/E)[rA– rD].