Hedge ratios for long calls are always __________.

A. between -1 and 0

B. between 0 and 1

C. 1

D. greater than 1

A security with normally distributed returns has an annual expected return of 18% and

standard deviation of 23%. The probability of getting a return between -28% and 64%

in any one year is _____.

A. 68.26%

B. 95.44%

C. 99.74%

D. 100%

Rational risk-averse investors will always prefer portfolios _____________.

A. located on the efficient frontier to those located on the capital market line

B. located on the capital market line to those located on the efficient frontier

C. at or near the minimum-variance point on the efficient frontier

D. that are risk-free to all other asset choices

The _________ reward-to-variability ratio is found on the ________ capital market

line.

A. lowest; steepest

B. highest; flattest

C. highest; steepest

D. lowest; flattest

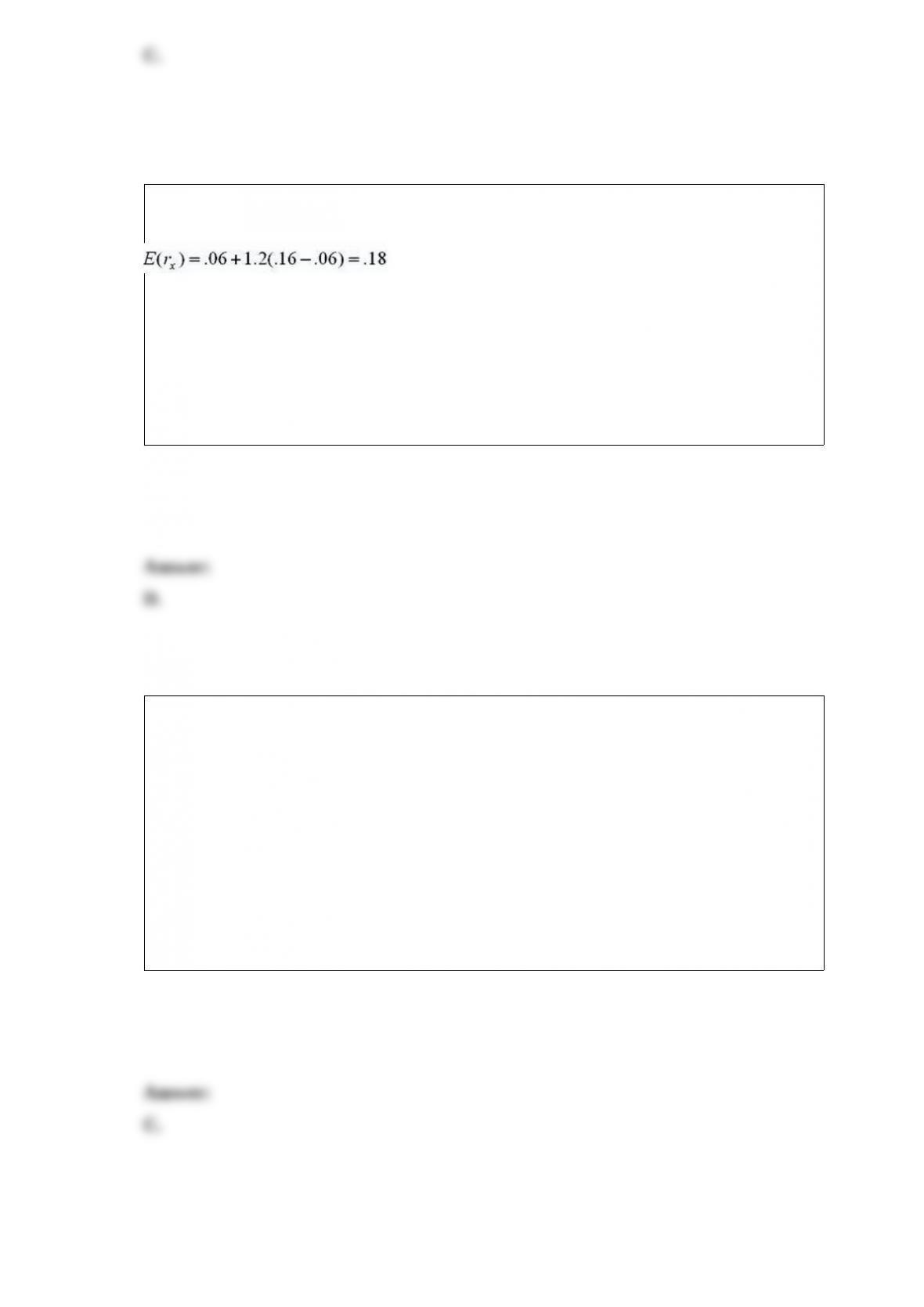

The risk-free rate and the expected market rate of return are 6% and 16%, respectively.

According to the capital asset pricing model, the expected rate of return on security X

with a beta of 1.2 is equal to _________.

A. 12%

B. 17%

C. 18%

D. 23%

(p. $$pageTag$$) A loan for a new car costs the

borrower .8% per month. What is the EAR?

A. .80%

B. 6.87%

C. 9.6%

D. 10.03%

The margin requirement on a stock purchase is 25%. You fully use the margin allowed

to purchase 100 shares of MSFT at $25. If the price drops to $22, what is your

percentage loss?

A. 9%

B. 15%

C. 48%

D. 57%

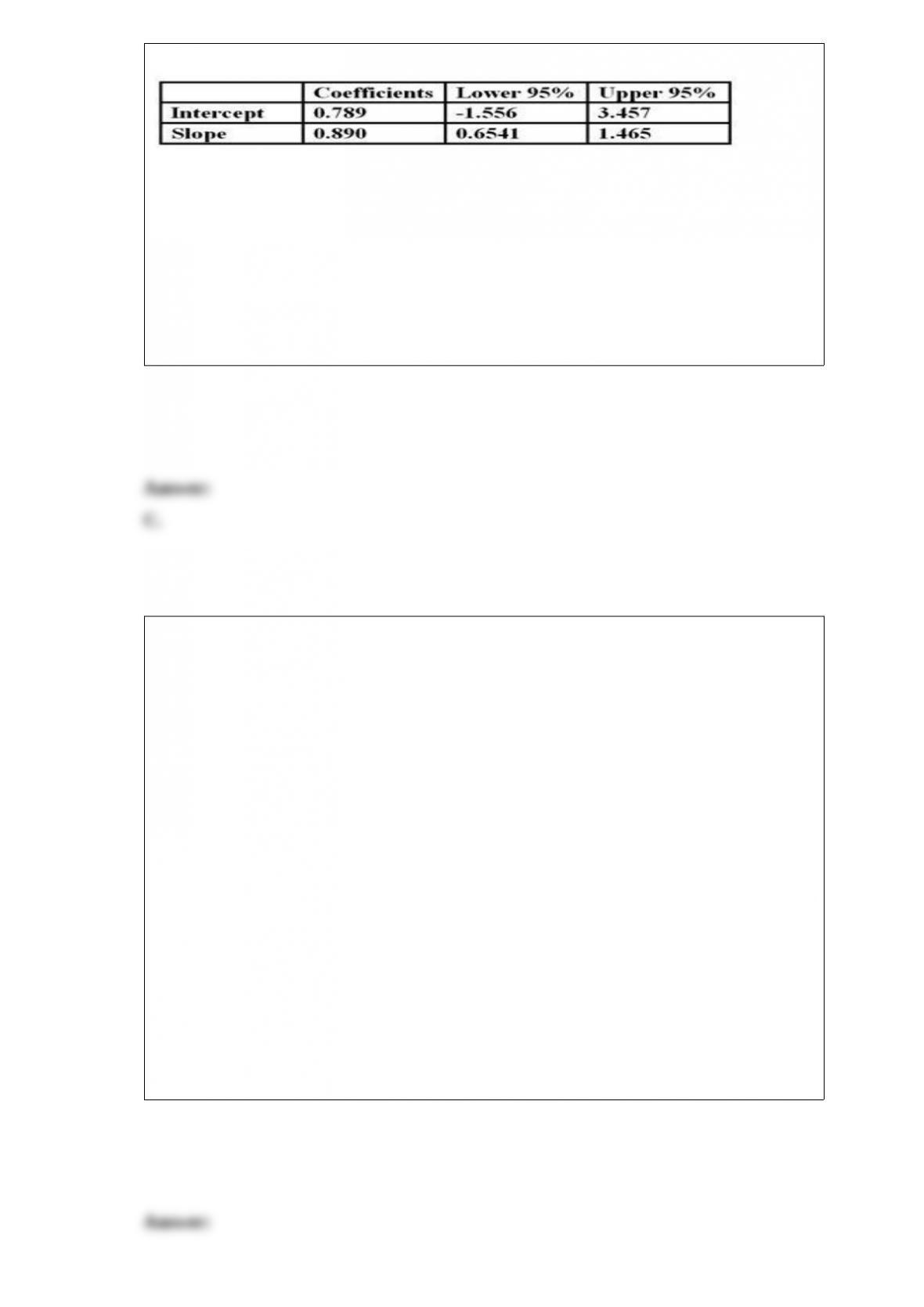

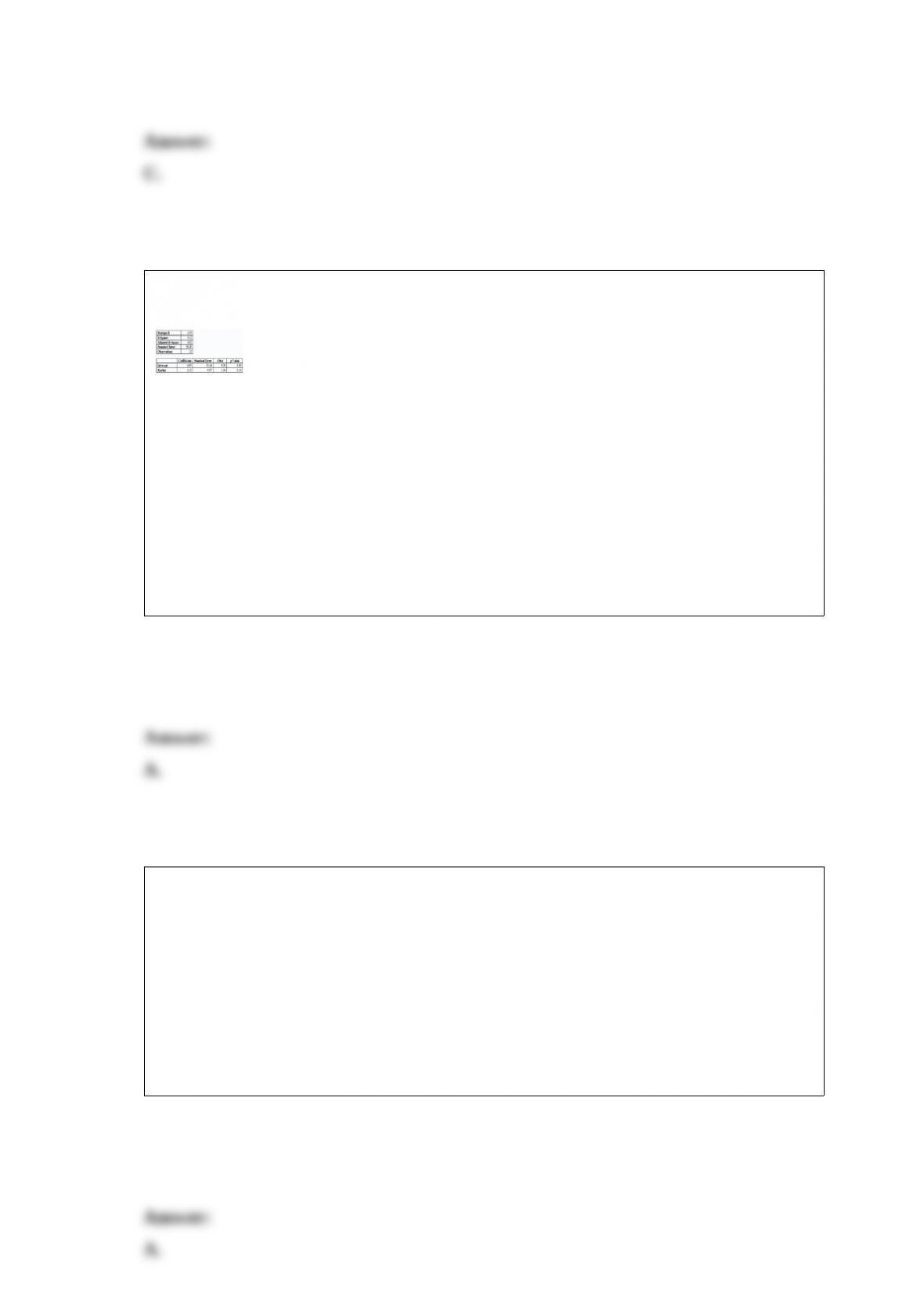

You run a regression of a stock’s returns versus a market index and find the following:

Based on the data, you know that the stock _____.

A. earned a positive alpha that is statistically significantly different from zero

B. has a beta precisely equal to .890

C. has a beta that is likely to be anything between .6541 and 1.465 inclusive

D. has no systematic risk

Medfield College’s $10 million endowment fund is not allowed to spend any

contributed capital or any capital gains. The fund may spend only investment earnings.

The fund is expected to need between $500,000 and $1,000,000 to pay for new lab

equipment for the science building. Which of the following is (are) true?

I. The fund should have a target rate of return of at least 10%.

II. The limitations on spending require that the fund limit its considerations to growth

stocks.

III. The requirement to spend money out of the fund this year provides a liquidity

constraint that may reduce the fund’s rate of return.

A. I only

B. II only

C. I and III only

D. I, II, and III

The exchange of one bond for a bond that has similar attributes but is more attractively

priced is called ______________.

A. a substitution swap

B. an intermarket spread swap

C. a rate anticipation swap

D. a pure yield pickup swap

A bond has a current price of $1,030. The yield on the bond is 8%. If the yield changes

from 8% to 8.1%, the price of the bond will go down to $1,025.88. The modified

duration of this bond is _________.

A. 4.32

B. 4

C. 3.25

D. 3.75

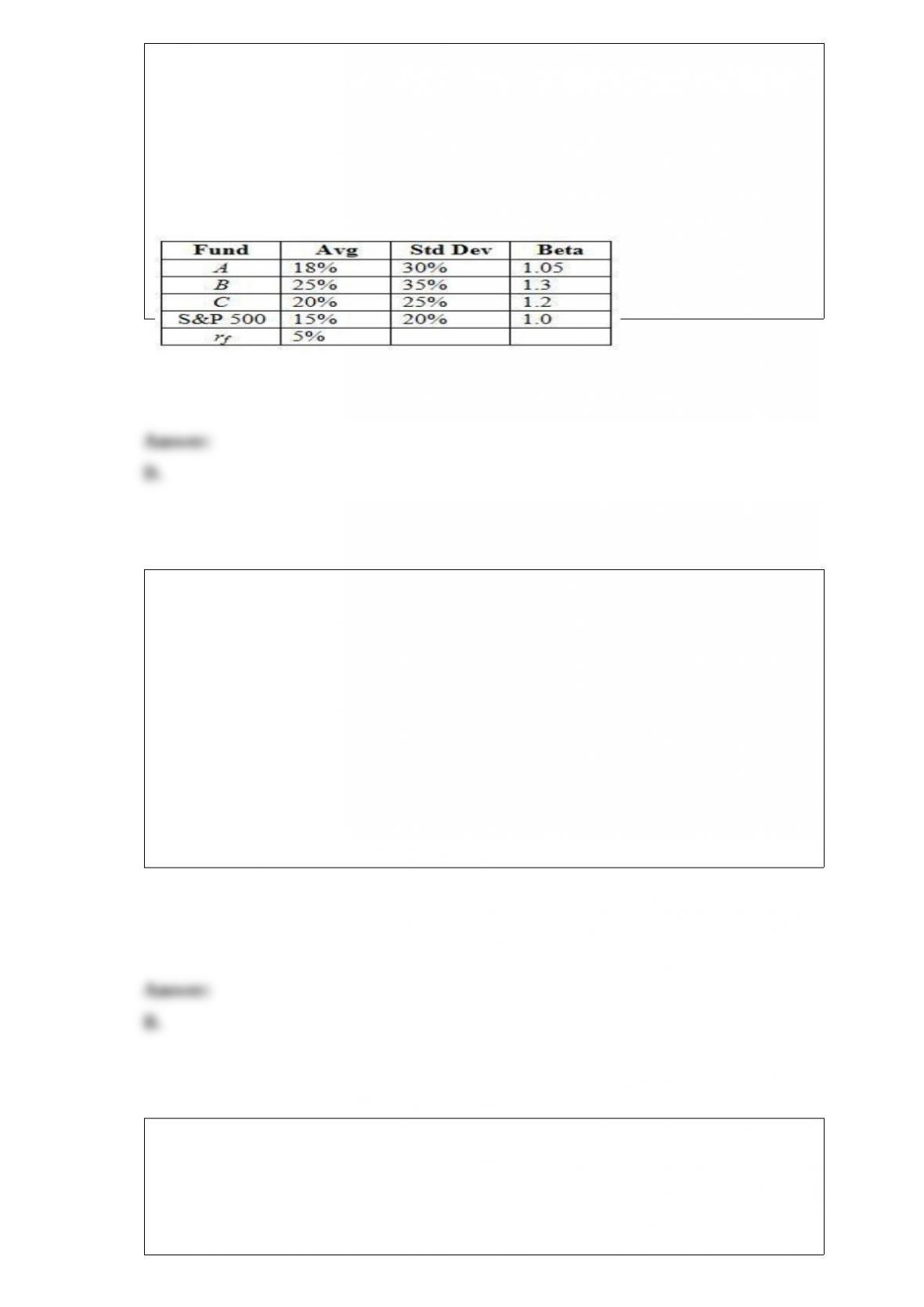

The risk-free rate, average returns, standard deviations, and betas for three funds and

the S&P 500 are given below.

What is the M2 measure for portfolio B?

A. .43%

B. 1.25%

C. 1.77%

D. 1.43%

You invest in a mutual fund that charges a 3% front-end load, 1% total annual fees, and

a 0% back-end load on Class A shares. The same fund charges a 0% front-end load, 1%

total annual fees, and a 2% back-end load on Class B shares. What are the total fees in

year 1 on a Class A investment of $20,000 with no growth in value?

A. $658

B. $794

C. $885

D. $902

According to the capital asset pricing model, a fairly priced security will plot

_________.

A. above the security market line

B. along the security market line

C. below the security market line

D. at no relation to the security market line

An 8%, 30-year bond has a yield to maturity of 10% and a modified duration of 8 years.

If the market yield drops by 15 basis points, there will be a __________ in the bond’s

price.

A. 1.15% decrease

B. 1.2% increase

C. 1.53% increase

D. 2.43% decrease

If the nominal rate of return on investment is 6% and inflation is 2% over a holding

period, what is the real rate of return on this investment?

A. 3.92%

B. 4%

C. 4.12%

D. 6%

If a firm has a positive tax rate and a positive operating ROA, and the interest rate on

debt is the same as the operating ROA, then operating ROA will be _________.

A. greater than zero, but it is impossible to determine how operating ROA will compare

to ROE

B. equal to ROE

C. greater than ROE

D. less than ROE

You are considering investing $1,000 in a complete portfolio. The complete portfolio is

composed of Treasury bills that pay 5% and a risky portfolio, P, constructed with two

risky securities, X and Y. The optimal weights of X and Y in P are 60% and 40%,

respectively. X has an expected rate of return of 14%, and Y has an expected rate of

return of 10%. To form a complete portfolio with an expected rate of return of 11%, you

should invest __________ of your complete portfolio in Treasury bills.

A. 19%

B. 25%

C. 36%

D. 50%

The values of beta coefficients of securities are __________.

A. always positive

B. always negative

C. always between positive 1 and negative 1

D. usually positive but are not restricted in any particular way

Duration measures

A. the effective maturity of a bond.

B. the weighted average of the time until each payment is received, with weights

proportional to the present value of the payment.

C. the average maturity of the bond’s promised cash flows.

D. all of the options.

Which one of the following is not a U.S. supply shock?

A. unions force an increase in national wage rates.

B. the oil supply from the Middle East drops 30%.

C. extended droughts reduce U.S. food production 25%.

D. chinese purchases of U.S. exports increase.

You invest in the stock of Valleyview Corp. and purchase a put option on Valleyview

Corp. This strategy is called a _________.

A. long straddle

B. naked put

C. protective put

D. short stroll

At a 4% yield, the duration of a perpetuity that pays $100 once a year forever is

_______.

A. 3.85 years

B. 4 years

C. 26 years

D. 100 years

This stock has greater systematic risk than a stock with a beta of ___.

A. .50

B. 1.5

C. 2

D. 3

In performance measurement, the bogey portfolio is designed to _________.

A. measure the returns to a completely passive strategy

B. measure the returns to a similar active strategy

C. measure the returns to a given investment style

D. equal the return on the S&P 500

You manage a $15 million hedge fund portfolio with beta = 1.2 and alpha = 2% per

quarter. Assume the risk-free rate is 2% per quarter and the current value of the S&P

500 Index is 1,200. You want to exploit the positive alpha, but you are afraid that the

stock market may fall and you want to hedge your portfolio by selling 3-month S&P

500 future contracts. The S&P contract multiplier is $250.

What is the expected quarterly return on the hedged portfolio?

A. 0%

B. 2%

C. 3%

D. 4%

You have $500,000 available to invest. The risk-free rate, as well as your borrowing

rate, is 8%. The return on the risky portfolio is 16%. If you wish to earn a 22% return,

you should _________.

A. invest $125,000 in the risk-free asset

B. invest $375,000 in the risk-free asset

C. borrow $125,000

D. borrow $375,000

__________ fund is defined as one in which the fund charges a sales commission to

either buy into or exit from the fund.

A. A load

B. A no-load

C. An index

D. A specialized-sector

Which one of the following represents local consumption smoothing?

I. Saving during your working years for retirement

II. Borrowing money to buy a car

III. Putting off a vacation for a year until you can afford it

A. I only

B. II and III only

C. I and II only

D. I, II, and III

According to market technicians, a TRIN statistic of less than 1 is considered a

__________.

A. bearish signal

B. bullish signal

C. volume decline

D. signal reversal

You write a put option on a stock. The profit at contract maturity of the option position

is ___________, where X equals the option’s strike price, ST is the stock price at

contract expiration, and P0 is the original premium of the put option.

A. max (P0, X – ST – P0)

B. min (-P0, X – ST – P0)

C. min (P0, ST – X + P0)

D. max (0, ST – X – P0)

Firms that specialize in helping companies raise capital by selling securities to the

public are called _________.

A. pension funds

B. investment banks

C. savings banks

D. REITs