An FI can hold assets denominated in a foreign country, but it cannot issue foreign

liabilities.

Answer:

Unexpected increases in inflation cause loss rates to increase more for long-tail risk

than for short-tail risks.

Answer:

The hedge ratio measures the impact that tailing-the-hedge will have on the number of

contracts necessary to hedge the cash position.

Answer:

Buying a fixed-rate asset whose duration is exactly equal to the desired investment

horizon immunizes against interest rate risk.

Answer:

Foreign exchange risk includes interest rate risk and credit risk as well as changes in the

foreign exchange rate between two countries.

Answer:

For any given country risk variable, the greater the size of the systematic risk relative to

the unsystematic risk, the less important the variable is to the lender.

Answer:

The specialized nature in which credit intermediation is performed by shadow banks

makes the process less cost efficient than if done by traditional banks.

Answer:

A loan commitment is an agreement involving the amount of loan available and the

amount of time during which the loan can be initiated.

Answer:

A strategy to increase reservable deposits on a Friday and decrease reservable deposits

on the following Monday is called the weekend game.

Answer:

The payoff values on bond options are positively linked to the changes in interest rates.

Answer:

An FI can protect itself against insolvency resulting from off-balance sheet activities by

purchasing insurance.

Answer:

Funding a portion of assets with equity capital means that hedging risk does not require

perfect matching of the assets and liabilities.

Answer:

In international finance, the variance of export revenue is based solely on the quantity

of product available for export.

Answer:

Directly matching foreign asset and liability books in the same FX currency will allow

an FI to hedge or lock in a profit spread regardless of future changes in exchange rates.

Answer:

CMOs are typically created from existing GNMA pass-through securities that are held

in trust.

Answer:

Settlement risk on wire transfers involves intraday credit risk.

Answer:

The advantage to the borrowing country of a Brady bond versus a loan from an FI is the

much longer maturity and thus the lower payment schedule of a Brady bond.

Answer:

The FDIC allows its member banks to participate in payday lending.

Answer:

One way to completely protect the lender against interest rate risk on a loan

commitment is for the lender to price the loan at a variable rate against some index.

Answer:

Savings banks and savings associations are savings institutions; with savings banks

serving as the primary providers of residential mortgage loans, and savings associations

concentrating on commercial loans and corporate bonds as well as mortgage assets.

Answer:

To be immunized against foreign currency and foreign interest rate risk, an FI should

match both the size and maturities of its foreign assets and foreign liabilities.

Answer:

The credit risk on an interest rate swap is generally much less than on an individual

loan.

Answer:

Monte-Carlo simulation is a process of creating asset returns based on actual trading

days so that the probabilities of occurrence are consistent with recent historical

experience.

Answer:

The value for duration describes the percentage increase in the price of an asset for a

given increase in the required yield or interest rate.

Answer:

Money market mutual funds have attracted large amounts of retail savings and retail

time deposits from commercial banks in recent years.

Answer:

Regulation of FIs is an attempt to enhance the social welfare benefits and mitigate the

social costs of providing FI services.

Answer:

The call option held by the residential mortgage holder is in the money when market

interest rates are less than the interest rate on an existing mortgage.

Answer:

The effect of the International Banking Act of 1978 was to accelerate the expansion of

foreign bank activities in the U.S. primarily because of their access to the Federal

Reserve’s discount window, Fedwire, and FDIC insurance.

Answer:

A secured loan has a claim to specific assets of the borrower in the case of default.

Answer:

An off-balance-sheet activity does not appear on the current balance sheet because it

does not involve holding a current primary claim or the issuance of a current secondary

claim.

Answer:

In recent years, U.S. banks have alone spent $20 billion per year in technology related

expenditures.

Answer:

When compared to swap and option contracts, credit risk exposure is greatest with a

futures contract.

Answer:

Which of the following is an advantage of converting from a mutual insurance company

to a stockholder-controlled company? A. Publicly held companies have access to

equity markets for additional capital for future business expansion.

B. Mutual organizations are subject to higher regulatory standards than public

companies.

C. Ability to offer more insurance products than those allowed under mutual

ownership.

D. Publicly held insurance companies can convert to federal charters but mutual

organizations cannot.

E. Mutual organizations can only underwrite policies in the state in which they are

chartered while publicly held organizations can expand nationwide.

Answer:

The asset transformation function of FIs typically involves A. receipt of securities

through electronic payments systems.

B. altering the liquidity and maturity features of funds sources used to finance the FI’s

asset portfolio.

C. granting loans to transform funds deficit units into funds surplus units.

D. investing short-term funds in off-balance sheet activities.

E. transferring of funds from one generation to another.

Answer:

For reserve computation purposes, Friday balances A. are excluded from the

calculations.

B. are included in the calculations.

C. receive triple weights in the calculations.

D. receive double weights in the calculations.

E. are averaged with Monday balances to get Saturday and Sunday balances.

Answer:

At the end of year 2, LIBOR rates are 6 percent and the exchange rate is $1.50/£. What

is the net payment paid or received in dollars by the U.S. bank? A. The U.S. bank paid

$9 million and received $9 million for a net payment of $0 million.

B. The U.S. bank paid $9 million and received $15 million for a net receipt of $6

million.

C. The U.S. bank paid $12 million and received $9 million for a net payment of $3

million.

D. The U.S. bank paid $12 million and received $12 million for a net payment of $0

million.

E. The U.S. bank paid $12 million and received $15 million for a net receipt of $3

million.

Answer:

Suppose the minimum balance to earn interest was lowered from $500 to $300 and she

now pays a service charge of 5 cents per check. Note that it costs the bank 10 cents to

process each check. What is her annual gross interest return?A. $53.75.

B. $54.63.

C. $52.06.

D. $51.54.

E. $55.37.

Answer:

If the manager buys a one-year option with an exercise price equal to the expected price

of the bond in one year, what will be the exercise price of the option? A. $84.00.

B. $85.99.

C. $86.21.

D. $85.74.

E. $85.96.

Answer:

Negative externalities exist in the depository sector when A. the fear of DI insolvency

leads to bank deposit runs.

B. lending activity is impaired or constrained.

C. there are delays in disbursements from insolvent DIs.

D. banks that are healthy suffer when another bank nears insolvency.

E. All of the above.

Answer:

An FI manager purchases a zero-coupon bond that has two years to maturity. The

manager paid $826.45 per $1,000 for the bond. The current yield on a one-year bond of

equal risk is 9 percent, and the one-year rate in one year is expected to be either 11.60

percent or 10.40 percent. Either rate is equally probable.

What is the yield to maturity for the two-year bond if held to maturity? A. 11.00

percent.

B. 10.00 percent.

C. 13.54 percent.

D. 11.60 percent.

E. 10.40 percent.

Answer:

Which of the following hedge fund objectives would be classified under the “risk

avoidance” category? A. Special situations funds.

B. Opportunistic funds.

C. Fund of funds.

D. Market timing funds.

E. Value funds.

Answer:

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a firm commitment basis. The investment banker pays $31.50 per

share to NetChoice, Inc. for the 5 million shares of stock. It then sells those shares to

the public for $30.00 per share.

What is the profit (loss) to the investment banker? A. Profit of $7,500,000.

B. Profit of $2,000,000.

C. Profit of $7,000,000.

D. Loss of $7,500,000.

E. Loss of $2,000,000.

Answer:

Which of the following are the two basic approaches to analyzing the cost functions of

FIs? A. Basic indicator approach and standardized approach.

B. Standardized approach and advanced measurement approach.

C. Production approach and intermediation approach.

D. Basic indicator approach and advanced measurement approach.

E. Intermediation approach and advanced measurement approach.

Answer:

Identify the procompetitive effect of banks’ expansion of their securities activities.A.

Reduces the degree of underpricing of new issues.

B. Encourages stuffing of fiduciary accounts.

C. Increased provision of cheap loans on the implicit condition that this loan is used to

purchase securities.

D. Use of lending powers by a bank to coerce a customer to buy the products sold by

its securities affiliate.

E. Use of inside information by a bank to set the prices, or help the distribution of

securities offerings by its affiliate.

Answer:

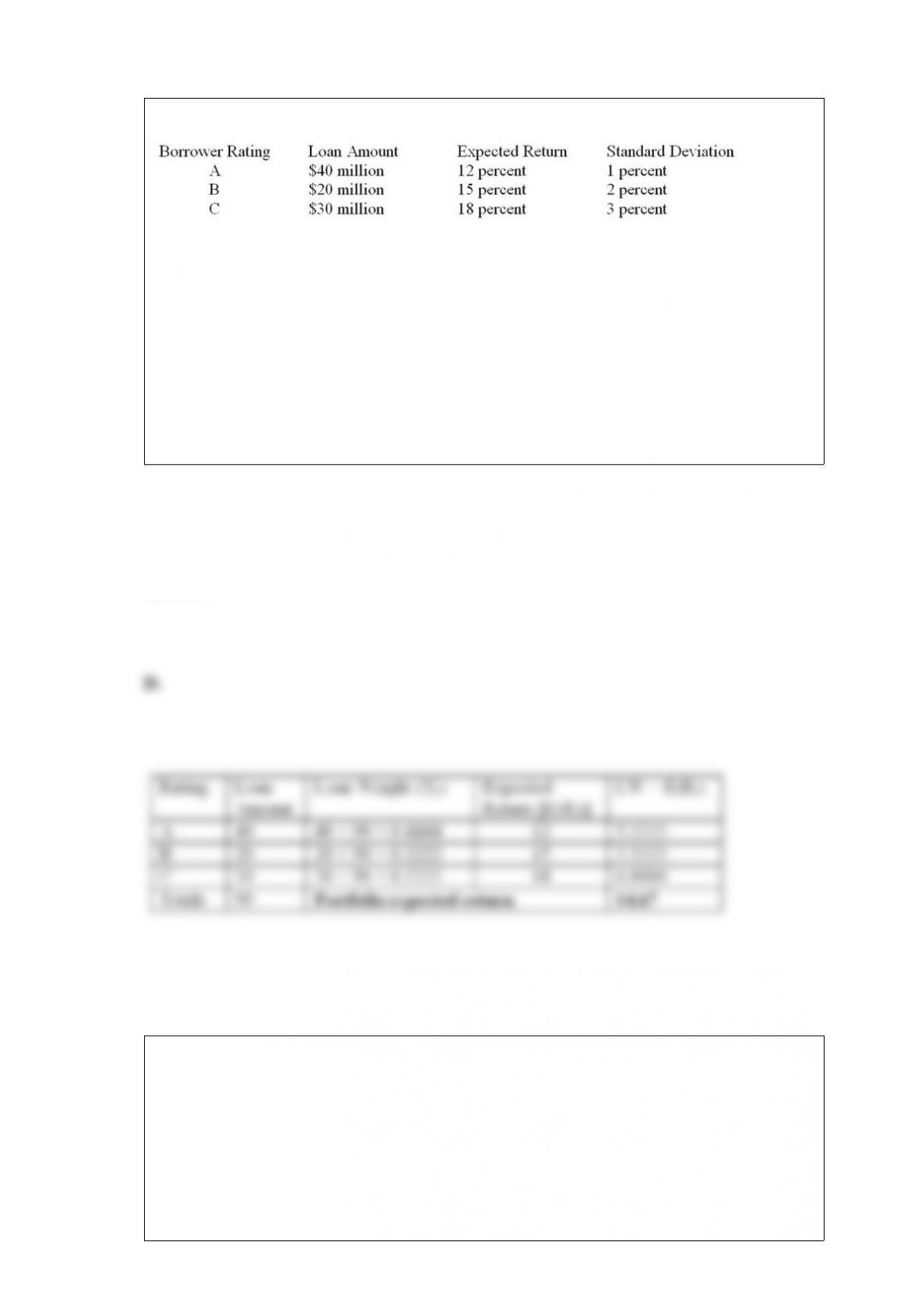

What is the FI’s expected return on its loan portfolio? A. 15.00 percent.

B. 18.00 percent.

C. 12.00 percent.

D. 14.67 percent.

E. 13.33 percent.

Answer:

Compared to commercial banks, why do finance companies often have substantial

industry and product expertise? A. Because they have no bank-type regulators looking

directly over their shoulders.

B. Because they are specialized in market research and analysis.

C. Because they are often subsidiaries of corporate-sector holding companies.

D. Because they are more often willing to accept risky customers.

E. All of the above.

Answer:

A loan made to finance a merger and acquisition that usually results in a high leverage

ratio for the borrower is a A. loan sold without recourse.

B. highly leveraged transaction loan.

C. loan sold with recourse.

D. loan assignment transaction.

E. loan participation transaction.

Answer:

An FI has entered a $100 million swap agreement with a counterparty. The

fixed-payment portion of the swap is similar to a government bond with maturity of 6

years and duration of 5 years. The swap payment interval is 1 year. If the relative shock

to interest rates [ΔR/(1 + R)] is a decline of 50 basis points, what will be the change in

market value of the swap contract? A. +$2.0 million.

B. -$2.0 million.

C. +$2.5 million.

D. -$2.5 million.

E. More information is needed.

Answer:

Which of the following liabilities have a high degree of withdrawal risk? A. Passbook

savings.

B. NOW Accounts.

C. Demand deposits.

D. Time deposits.

E. Wholesale CDs.

Answer:

Factors that affect the predictability of claims loss exposure includeA. unexpected

increases in inflation.

B. the frequency and severity of loss.

C. the concept of long-tail risk.

D. property versus liability coverage.

E. All of the above.

Answer:

A bond is scheduled to mature in five years. Its coupon rate is 9 percent with interest

paid annually. This $1,000 par value bond carries a yield to maturity of 10 percent.

Calculate the leverage-adjusted duration gap to four decimal places and state the FI’s

interest rate risk exposure of this institution.A. +1.0308 years; exposed to interest rate

increases.

B. -0.3232 years; exposed to interest rate increases.

C. +0.8666 years; exposed to interest rate increases.

D. +0.4875 years; exposed to interest rate increases.

E. -1.3232 years; exposed to interest rate decreases.

Answer:

An agreement between a buyer and a seller at time 0 to exchange a standardized,

pre-specified asset for cash at a specified later date is characteristic of a A. spot

contract.

B. forward contract.

C. futures contract.

D. put options contract.

E. call options contract.

Answer:

At the end of the year, the exchange rate is €2/$. What are the losses and gains to each

bank as a result of this swap compared to the scenario without the swap. A. With the

agreement, Bank Dresdner pays €2.5 million less while Bank USA pays $1.25 million

more.

B. With the agreement, Bank Dresdner pays €2.5 million more while Bank USA pays

$1.25 million less.

C. With the agreement, Bank USA pays $3.75 million less while Bank Dresdner pays

€7.5 million more.

D. With the agreement, Bank USA pays $3.75 million more while Bank Dresdner pays

€7.5 million less.

E. Each bank pays the same because the exchange rate affects both parties equally.

Answer:

What type of risk focuses upon future contingencies? A. Liquidity risk.

B. Interest rate risk.

C. Credit risk.

D. Foreign exchange rate risk.

E. Off-balance sheet risk.

Answer:

In situations where the required reserve shortfall exceeds 4 percent, the bank may be A.

assessed explicit monetary penalties by the Federal Reserve Bank.

B. assessed implicit penalties in the form of more frequent monitoring and

examinations.

C. allowed to carry 4 percent of the required reserves to the next maintenance period.

D. declared insolvent.

E. Answers A, B, and C only.

Answer:

As of 2012, the top 25 U.S. commercial banks accounted for ________ percent of OBS

derivative contracts among FDIC-insured institutions. A. 100

B. 99.8

C. 92.6

D. 81.9

E. 60.7

Answer:

If Bank A acquires Bank B, what is the new Herfindahl Index? A. 60.

B. 100.

C. 5,800.

D. 5,050.

E. 6,525.

Answer:

The primary benefit of a futures exchange is A. always knowing its exact location.

B. indemnifying counterparties against credit or default risk.

C. guarantee of trading volume.

D. intervention on the trader’s behalf with government regulators.

E. availability of free legal services.

Answer:

What is the end-of-year profit or loss on the bank’s cash position if in one year the

exchange rate falls to US $0.765/C $1? Assume there is no change in interest rates.

(Choose the closest answer) A. Loss of US $75,000.

B. Profit of C $274,000.

C. Loss of US $7,000.

D. Profit of C $9,000.

E. Loss of US $5,000.

Answer:

An investment banker agrees to underwrite an issue of 5 million shares of stock for

NetChoice, Inc. on a firm commitment basis. The investment banker pays $31.50 per

share to NetChoice, Inc. for the 5 million shares of stock. It then sells those shares to

the public for $30.00 per share.

If the investment bank can sell the shares for $34 per share, how much money does

NetChoice, Inc. receive? A. $150,000,000.

B. $157,500,000.

C. $112,000,000.

D. $125,000,000.

E. $105,000,000.

Answer:

The market-making function of investment banking can be described as A. agency

transactions are two-way transactions on behalf of customers, such as a dealer working

for a fee or commission.

B. agency transactions are when market makers take long or short positions and seek

profits on price movements.

C. market makers take inventory positions to stabilize the market in the securities.

D. Answers A and C only.

E. Answers B and C only.

Answer:

The duration of a soon to be approved loan of $10 million is four years. The 99th

percentile increase in risk premium for bonds belonging to the same risk category of the

loan has been estimated to be 5.5 percent.

What is the capital (loan) risk of the loan if the current average level of interest rates for

this category of bonds is 12 percent? A. -$550,000.

B. -$1,564,280.

C. -$1,964,280.

D. -$2,000,000.

E. -$2,200,000.

Answer:

Which of the following is NOT a reason for using a bad bank as a vehicle to add value

in the loan sale process? A. Contracts for managers can be created to maximize the

incentives to generate enhanced values from loan sales.

B. The bad bank enables bad assets to be managed by loan workout specialists.

C. The bad bank does not need to be concerned about liquidity needs since it does not

have any deposits.

D. Moving the bad loans off the balance sheet of the good bank will improve the

markets perception, and thus performance, of the good bank.

E. The good bank-bad bank structure increases information asymmetries regarding the

value of the good bank’s assets.

Answer:

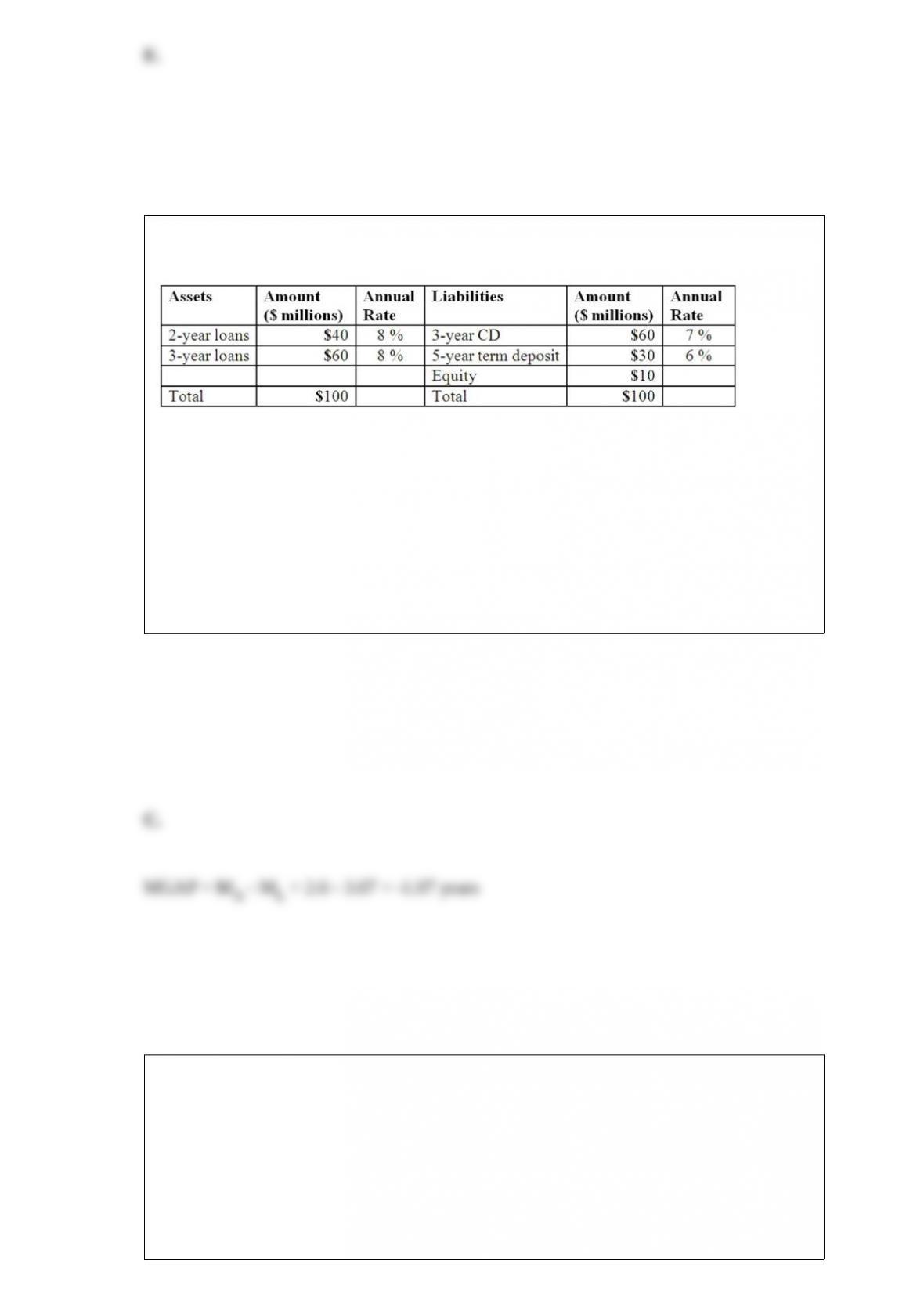

Duration Bank has the following assets and liabilities as of year-end. All assets and

liabilities are currently priced at par and pay interest annually.

What is

the FI’s maturity gap? A. -2.03 years.

B. -2.50 years.

C. -1.07 years.

D. -0.70 years.

E. -0.40 years.

Answer:

The Pecora Commission’s findings about the 1929 stock market crash resulted in the A.

Financial Services Modernization Act.

B. Glass-Steagall Act.

C. Federal Reserve Act.

D. International Banking Act.

E. Garn St. Germain Depository Institutions Act.

Answer:

The Basel I capital requirements as currently implemented includeA. different credit

risks of on-balance-sheet assets.

B. different credit risks of off-balance-sheet assets.

C. the consideration of market risk in 1998.

D. All of the above.

E. Only two of the above.

Answer: