Prior to the financial crisis of 2008, the return on equity for small community banks had

been larger than for large money center banks.

Answer:

GNMA will sponsor any pool of loans regardless of the size of each individual loan in

the pool.

Answer:

The interest rate paid on money market deposit accounts by U.S. DIs must directly

reflect the rates earned on investments in commercial paper, bankers acceptances,

repurchase agreement, and T-bills.

Answer:

Performing loans in the LDC debt market are loans on which the foreign country is

making promised payments.

Answer:

The current market value or contingent claim value of OBS items overestimates their

notional value.

Answer:

Duration of a zero coupon bond is equal to the bond’s maturity.

Answer:

One advantage of RiskMetrics over back simulation is that RiskMetrics provides a

worst case scenario value.

Answer:

Contingent credit risk is more serious for futures contracts than forward contracts

because the over-the-counter arrangements necessary to replicate the guarantees at a

later date.

Answer:

The larger the interest rate shock, the smaller the interest rate risk exposure of an FI.

Answer:

The interbank funds market is a potential source for increasing reserves to meet

required reserves.

Answer:

The ability to provide loan commitments is a signal to borrowers that the FI has a lower

risk portfolio.

Answer:

The gain to a buyer of bond call options is unlimited, even if interest rates decrease to

zero.

Answer:

Commercial paper has become an acceptable substitute source for bank loans formany

large corporations.

Answer:

The move by regulators toward market value accounting of the loan portfolios will

likely encourage sales of loans in the secondary markets.

Answer:

Rescheduling may cause the borrower to lose future borrowing opportunities for

investment projects.

Answer:

The principal reasons for the growth in profitability of the securities industry in the

middle 1990s were the trading profits from fixed income securities and the growth in

new issue underwriting.

Answer:

Which of the following is NOT TRUE of loan assignments?A. All rights are

transferred on sale.

B. The loan buyer holds a direct claim on the borrower.

C. Transfer of U.S. domestic loans is normally associated with a Uniform Commercial

Code filing.

D. Ownership rights are generally much clearer in a loan sale by assignment.

E. Contract terms are unrestrictive from the seller’s perspective.

Answer:

Because of compensating balances and fees used to increase return on a loan, the credit

risk premium is not the fundamental factor driving the promised return once the base

rate on the loan has been set.

Answer:

According to the American Bankers Association, the tax-exempt status of credit unions

is the equivalent of a $1 billion per-year subsidy to the industry.

Answer:

Market making involves creating a primary market in a financial asset.

Answer:

In the BIS standardized framework model, the general market risk weights reflect the

product of the modified durations and interest rate shocks.

Answer:

The Volker Rule became effective in early 20

Answer:

The use of subordinated debt as a replacement for common stock has been proposed as

a method of increasing stockholder discipline.

Answer:

Perfect matching of the maturities of the assets and liabilities will always achieve

perfect immunization for the equity holders of an FI against interest rate risk.

Answer:

The gap ratio is useful because it indicates the scale of the interest rate exposure by

dividing the gap by the asset size of the institution.

Answer:

Agency transactions of market makers are two-way transactions on behalf of customers

Answer:

The dollar value of a foreign exchange portfolio equals the FX position times the spot

exchange rate.

Answer:

Fees of load funds that are used to cover the costs of trading in securities are called

12b-1 fees.

Answer:

The Bank for International Settlements has stated that banks should carry extra capital

as a cushion against operational risks.

Answer:

The Tier I leverage ratio measures the amount of an FI’s total capital relative to total

assets.

Answer:

A deficiency of the risk-based capital ratio is that it measures the ability of a bank to

meet both the on- and off-balance-sheet credit risk, but not the interest rate or market

risks.

Answer:

Which of the following observations concerning concentration limits is not TRUE?A.

Limits are set by assessing the borrower’s current portfolio, its operating unit’s business

plans, its economists’ economic projections, and its strategic plans.

B. FIs set concentration limits to reduce exposures to certain industries and increase

exposures to others.

C. When two industry groups’ performances are highly correlated, an FI may set an

aggregate limit of less than the sum of the two individual industry limits.

D. FIs may set aggregate portfolio limits or combinations of industry and geographic

limits.

E. Bank regulators in recent years have limited loan concentrations to individual

borrowers to a maximum of 30 percent of a bank’s capital.

Answer:

A liquid asset can be converted to cash quickly, but will require a discount from market

value.

Answer:

Which of the following is NOT used as a method of measuring liquidity risk? A.

Liquidity coverage ratio.

B. Liquidity index.

C. Financing gap and financing requirement.

D. Peer group ratio comparison.

E. Current ratio.

Answer:

Which of the following ratios do FIs and regulators often use as a simple measure of

solvency? A. Current ratio.

B. Capital to assets.

C. Earnings before interest and taxes to total assets.

D. Quick ratio.

E. Asset turnover ratio.

Answer:

If stored liquidity is used by a DI to fund an exercised loan commitmentA. the balance

sheet will decrease by the amount of the new loan.

B. only the asset side of the balance sheet will increase.

C. the balance sheet will increase by the amount of the new loan.

D. only the liability side of the balance sheet will increase.

E. there will be no effect on the balance sheet.

Answer:

A criticism of the Basel I risk-based capital ratio is A. the incorporation of

off-balance-sheet risk exposures.

B. the application of a similar capital requirement across major banks in international

banking centers across the world.

C. the more systematic accounting of credit risk differences.

D. the lack of appropriate consideration of the portfolio diversification effects of credit

risk.

E. Answers B and C only.

Answer:

What will be the net after-swap yield on assets for the thrift? A. Variable-rate at

LIBOR.

B. Fixed-rate at 8 percent.

C. Fixed-rate at 1 percent.

D. Fixed-rate at 2 percent.

E. None of the above.

Answer:

Assume that the hedge was placed as indicated in a prior question, and that the BP

futures contract is trading at $1.62/≤. Assume the futures contract has some days

remaining to maturity. What will be the gain or loss on the hedge if it is unwound at this

price? A. $4,280,000 loss.

B. $4,000,000 loss.

C. $4,280,000 gain.

D. $4,000,000 gain.

E. $6,400,000 gain.

Answer:

What is the end-of-year profit or loss on the bank’s cash position if in one year

Canadian bond rates increase to 7.5 percent? Assume no change in either current U.S.

interest rates or current exchange rates. (Choose the closest answer) A. Loss of US

$5,000.

B. Profit of US $15,000.

C. Loss of C $119,000.

D. Profit of C $50,000.

E. Loss of C $50,000.

Answer:

If the exchange rate had fallen from $1.60/≤1 at the beginning of the year to $1.50/≤1 at

the end of the year, the weighted return on the FI’s asset portfolio would be A. 13.29%.

B. 12.56%.

C. 16%.

D. 8.75%.

E. 9.375%.

Answer:

The reasons nondepository FIs have less FX risk than major money center banks

includeA. Smaller asset sizes.

B. Prudent person concerns.

C. Regulations.

D. All of the above.

E. Answers A and C only.

Answer:

The underlying GNMA 15-year mortgage pool has a principal amount of $50 million

and an annual yield of 6 percent (paid monthly). Assume that there are no prepayments.

What is the first monthly payment on the Interest Only (IO) strip? A. $3,000,000.

B. $421,928.

C. $250,000.

D. $299,775.

E. $171,928.

Answer:

A bank threatens to credit ration unless the customer agrees to let the bank’s securities

affiliate do its securities underwritings. Identify the conflict of interest in this scenario.

A. Salesperson’s Stake.

B. Stuffing fiduciary accounts.

C. Tie-ins.

D. Third-party loans.

E. Information transfer.

Answer:

What is the essential idea behind RAROC? A. Evaluating the actual or contractually

promised annual ROA on a loan.

B. Analyzing historic or past default risk experience.

C. Balancing expected interest and fee income less the cost of funds against the loan’s

expected risk.

D. Extracting expected default rates from the current term structure of interest rates.

E. Dividing net interest and fees by the amount lent.

Answer:

What is the expected return on the loan at the end of the year if 50 percent of the loan is

drawn? Estimate using future values of fee and interest income received, that is, return

is defined as all fee and interest income earned at year-end as a percentage of funds

used. Assume the cost of funds to the bank is 8 percent. A. 13.45 percent.

B. 13.57 percent.

C. 13.60 percent.

D. 13.72 percent.

E. 13.90 percent.

Answer:

What is the probability that two-year B-rated corporate debt will be fully repaid?A.

92.9 percent.

B. 95.6 percent.

C. 97.2 percent.

D. 7.10 percent.

E. 4.40 percent.

Answer:

For mutual funds outside the United States, total amounts invested in this fund category

topped the list in 2012. A. Equity funds.

B. Bond funds.

C. Hybrid funds.

D. Money market funds.

E. Hedge funds.

Answer:

A significant recent trend in the provision of financial services is that households

increasingly prefer denomination intermediation and information services provided by

A. mutual funds and money market mutual funds.

B. commercial banks.

C. insurance companies.

D. hedge funds.

E. investment banks.

Answer:

In applying the loan loss ratio models, the loss rate “β” for the whole loan portfolio is

A. 0.

B. 0.5.

C. 1.

D. 2.

E. negative.

Answer:

If the spot foreign exchange rate remains constant at $1.60 to ≤1 throughout the year,

the return from the U.K. investment will be A. 15%.

B. 12%.

C. 16%.

D. 13%.

E. 7%.

Answer:

If losses on a particular line of medical malpractice insurance were $650 million and

premiums earned were $575 million, the loss ratio would be A. 1.13 implying that this

line of insurance is profitable.

B. 1.13 implying that this line of insurance is unprofitable.

C. 0.88 implying that this line of insurance is profitable.

D. 0.88 implying that this line of insurance is unprofitable.

Answer:

Immunization of a portfolio implies that changes in _____ will not affect the value of

the portfolio. A. book value of assets

B. maturity

C. market prices

D. interest rates

E. duration

Answer:

The shortcomings of this strategy are the following except A. duration changes as the

time to maturity changes, making it difficult to maintain a continuous hedge.

B. estimation of duration is difficult for some accounts such as demand deposits and

passbook savings account.

C. it ignores convexity which can be distorting for large changes in interest rates.

D. it is difficult to compute market values for many assets and liabilities.

E. it does not assume a flat term structure, so its estimation is imprecise.

Answer:

Which of the following is the regulation that allowed the SEC to restrict program

trading when it deems necessary? A. Securities Exchange Act.

B. Investment Advisers Act.

C. Investment Company Act.

D. Insider Trading and Securities Fraud Enforcement Act.

E. Market Reform Act.

Answer:

Discount brokersA. are securities firms focused on providing research support for

customers.

B. conduct trades for customers but do not offer investment advice.

C. allow customers to receive investment advice at very low rates.

D. effect trades for customers on- or offline while offering investment advice.

E. are electronic trading securities firms that allow customers to trade without the use

of a broker.

Answer:

The use of expected shortfall (ES) to measure market risk of a portfolio assumes which

of the following? A. There is a very small sample size (<30 observations) used to

estimate probability distributions.

B. That the probability distribution is skewed to the left.

C. That changes in asset prices are normally distributed but with fat tails.

D. That the probability distribution is skewed to the right.

E. That changes in asset prices follow a standard normal probability distribution.

Answer:

What will be the impact, if any, on the market value of the bank’s equity if all interest

rates increase by 75 basis points? (i.e., ΔR/(1 + R) = 0.0075) A. The market value of

equity will decrease by $15,750.

B. The market value of equity will increase by $15,750.

C. The market value of equity will decrease by $426,825.

D. The market value of equity will increase by $426,825.

E. There will be no impact on the market value of equity.

Answer:

Which of the following is the practice that involves short-term trading of mutual funds

seeking to take advantage of short-term discrepancies between the price of a mutual

fund’s shares and out-of-date values on the securities in the fund’s portfolio?A. Market

timing.

B. Insider trading.

C. Late trading.

D. Directed brokerage.

E. Spinning.

Answer:

During the financial crisis of 2008-2009, the FASB provided guidance on asset

valuation that allowed A. DI management to use internal cash flow models and

assumptions to estimate fair value when there is limited market data available.

B. regulatory capital of banks to deviate from industry norms.

C. excess reserves with the Fed to be included as regulatory capital.

D. DIs to choose either book value treatment or market value treatment of asset

valuation.

E. DI management the option to postpone asset write-downs until adequate capital was

available.

Answer:

Calculate the annual cash flows of a $500,000, 12-year fixed-payment deferred annuity

earning a guaranteed 5 percent per year if annual payments are to begin at the end of

year 4. A. $32,652.38.

B. $79,018.76.

C. $62,195.01.

D. $65,304.76.

E. $31,097.50.

Answer:

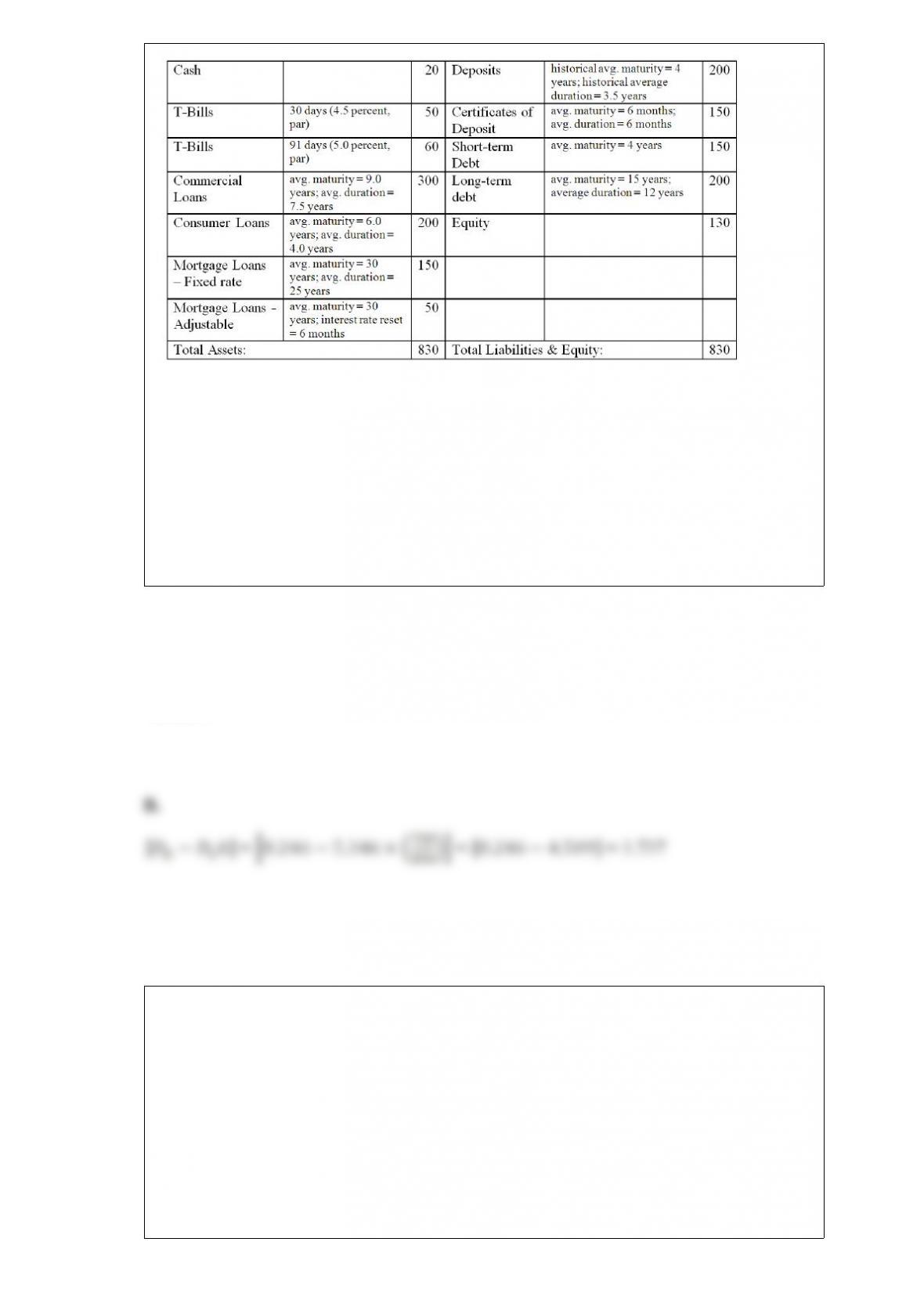

The numbers provided are in millions of dollars and reflect market values:

What is

the leverage-adjusted duration gap of the FI?A. 3.61 years.

B. 3.74 years.

C. 4.01 years.

D. 4.26 years.

E. 4.51 years.

Answer:

Which of the following is NOT a back-office service function in the securities industry?

A. Correspondent banking services.

B. Escrow services.

C. Clearance of securities transactions.

D. Research services.

E. Services related to settlement of securities transactions.

Answer:

Which of the following describes the condition known as runoff in the repricing model

approach to measuring interest rate risk of an FI?A. Periodic cash flow of interest and

principal amortization payments on long-term assets that can be reinvested at market

rates.

B. The effect that a change in the spread between rates on RSAs and RSLs has on net

interest income as interest rates change.

C. Mismatch of asset and liabilities within a maturity bucket.

D. The relations between changes in interest rates and changes in net interest income.

E. Those deposits that act as an FI’s long-term sources of funds.

Answer:

In regard to a CMO, which of the following have the shortest average life with a

minimum of prepayment protection? A. Class A bonds.

B. Class B bonds.

C. Class C bonds.

D. Class Z bonds.

E. Class R bonds.

Answer:

The returns obtained by investors of mutual funds include the following except A.

interest income earned on assets.

B. dividend income earned on assets.

C. capital gains on assets sold by the fund.

D. capital appreciation in the underlying value of the assets held in the portfolio.

E. refunds of load charges and management fees.

Answer:

The repricing gap does not accurately measure FI interest rate risk exposure because A.

FIs cannot accurately predict the magnitude change in future interest rates.

B. FIs cannot accurately predict the direction of change in future interest rates.

C. accounting systems are not accurate enough to allow the calculation of precise gap

measures.

D. it does not recognize timing differences in cash flows within the same maturity

grouping.

E. equity is omitted.

Answer:

Offering bank deposit-like accounts to individual customers by a securities firm

involves A. the function of investing.

B. the function of cash management.

C. the function of market making.

D. the function of trading.

E. the function of investment banking.

Answer: