Basis risk occurs on a loan commitment because the spread of a pricing index over the

cost of funds may vary.

Answer:

A run on a bank is not necessarily a bad occurrence.

Answer:

Retail banking services and products in recent years have moved strongly toward

electronic payment technology.

Answer:

A bank must be ready to pay out all demand deposit liabilities on any given day.

Answer:

A hedge with a futures contract reduces volatility in payoff gains on both the upside and

downside of interest rate movements.

Answer:

All fixed-income assets exhibit convexity in their price-yield relationships.

Answer:

If the value of equity is less than zero on a mark-to-market accounting basis, liquidation

of the FI would result in losses to the shareholders.

Answer:

Hedging effectiveness often is measured by the squared correlation between past

changes in the spot asset prices and futures prices.

Answer:

The ability of savers to transfer wealth between youth and old age and across

generations is called maturity intermediation.

Answer:

Banks are limited by regulation to using the historic or back simulation method to

quantify market risk exposure.

Answer:

The leverage ratio specified under FDICIA does not account for the risks of

off-balance-sheet activities.

Answer:

The leverage adjusted duration of a typical depository institution is positive.

Answer:

The “too big to fail” policy doctrine prevalent through the 1980s and most of the 1990s

is remised on the separation of small depositors who would receive deposit insurance

and large depositors who would not receive the benefits of deposit insurance.

Answer:

Delaware and South Dakota have become leading states in the distribution of some

financial services because of liberal regulations.

Answer:

Regulators in the U.S. do not allow government securities to perform the role of a

required reserve.

Answer:

Under Basel II (2006), operational risk can be measured by four different approaches.

Answer:

LIBOR, the London Interbank Offered Rate, is the rate for short-term interbank dollar

loans in the domestic money-center bank market.

Answer:

Up to six percent of excess reserves may be carried forward to the next reserve

maintenance period.

Answer:

One function of bank capital is to protect uninsured depositors, bondholders, and

creditors in the event of insolvency and liquidation.

Answer:

Setting the duration of the assets higher than the duration of the liabilities will exactly

immunize the net worth of an FI from interest rate shocks.

Answer:

The policy of forbearance practiced by the FSLIC in the late 1980s allowed many

commercial banks to remain open even in the face of continuing losses and insolvency.

Answer:

The existence of the “too big to fail” doctrine may encourage large banks to take

excessive risks in securities underwriting activities.

Answer:

Money supply growth and the import ratio tend to have low systematic risk elements in

a CRA analysis.

Answer:

The loss to the buyer of a bond option is unlimited.

Answer:

Mutual funds achieve economies of scale for individual investors by realizing the

benefits of lower transaction costs and commissions as compared to those incurred by

individual investors.

Answer:

As of 2012, U.S. FIs held assets totaling over $27 trillion

Answer:

Similar to Basel II, Basel III will require banks to assign on-balance-sheet assets to one

of four categories of credit risk exposure.

Answer:

Off-balance sheet activities can have both positive and negative effects on the risk of

the FI.

Answer:

The cost in terms of both time and money to restructure the balance sheet of large and

complex FIs has decreased over time.

Answer:

Defining buckets of time over wider intervals creates greater accuracy in the use of the

repricing model because fewer calculations are required.

Answer:

The assets of PC insurers are relatively short term and more liquid than those of life

insurance companies.

Answer:

As a percent of total assets, savings institutions hold lower amounts of cash and U.S.

Treasury securities than commercial banks.

Answer:

A major difference between banks and other nonfinancial firms is the low amount of

leverage in commercial banks.

Answer:

The payoff of a credit spread call option increases as the yield spread on a specified

benchmark bond increases above some exercise spread.

Answer:

Two important input factors in financial intermediation are capital and labor.

Answer:

The NAFTA agreement and other agreements reached through the help of the World

Trade Organization should reduce some of the restrictions that have face U.S. banks in

attempts to enter emerging market countries.

Answer:

Which of the following is closely associated with credit allocation regulation?A.

Support the FI’s lending to socially important sectors.

B. Transmission of monetary policy from the Federal Reserve to the economy.

C. Ensure the safety and soundness of the FI.

D. Prevent discrimination in lending on the basis of age, race, sex, or income.

E. Protect investors against abuses.

Answer:

In a world without FIs, households will be less willing to invest in corporate securities

because they A. are not able to monitor the activities of the corporation more closely

than FIs.

B. tend to prefer shorter, more liquid securities.

C. are subject to price risk when corporate securities are sold.

D. may not have enough funds to purchase corporate securities.

E. All of the above.

Answer:

What is the advantage of a futures hedge over an options hedge? A. The futures hedge

has lower credit risk exposure.

B. The futures hedge reduces volatility in profit gains on both sides.

C. The futures hedge is marked to market less frequently.

D. The futures hedge offers the least downside risk protection.

E. The futures hedge completely offsets losses but only partly offsets gains.

Answer:

An investment banker agrees to underwrite an issue of 10 million shares of stock for

Rochester Industries on a best-efforts basis. The investment banker is able to sell 8

million shares for $10.50 per share, and it charges Rochester Industries $0.225 per share

sold.

If the investment bank sells 8 million shares for $9.75 per share, how much money does

Rochester Industries receive? A. $76,200,000.

B. $84,000,000.

C. $105,000,000.

D. $82,200,000.

E. $78,000,000.

Answer:

Which of the following FX trading activities is used for purposes of speculation? A.

The purchase and sale of foreign currencies for the purpose of profiting from

forecasting or anticipating future movements in FX rates.

B. The purchase and sale of foreign currencies to allow customers to partake in and

complete international commercial trade transactions.

C. The purchase and sale of foreign currencies for the purpose of offsetting customer

exposure in any given currency.

D. The purchase and sale of foreign currencies to allow customers to take positions in

foreign real and financial investments.

E. None of the above.

Answer:

Requiring minimum reserves to be held at the central bank is the equivalent of A.

buffer reserves.

B. a reserve requirement tax.

C. the target reserve ratio.

D. contagious effects of liquidity risk.

E. None of the above.

Answer:

Many households place funds with financial institutions because many FI accounts

provideA. lower denominations than other securities.

B. flexible maturities verses other interest-earning securities.

C. better liquidity than directly negotiated debt contracts.

D. less price risk if interest rates change.

E. All of the above.

Answer:

A contract that pays the par value of a loan in the event of default is a A. put option.

B. call option.

C. digital default option.

D. futures option.

E. credit spread call option.

Answer:

If a bank’s concentration limit (as a percent of capital) is 20 percent, and its expected

recovery from defaulted loans is 50 percent, what is the maximum loss it permits to

affect its capital in the event of a default? A. 5 percent.

B. 10 percent.

C. 15 percent.

D. 20 percent.

E. 25 percent.

Answer:

As a result of illegal and abusive activities in recent years, new rules and regulations

were imposed on mutual fund companies in 2004. These rules were intended to A.

close legal loopholes that some fund managers had abused.

B. improve fund governance.

C. give investors more information about conflicts of interest.

D. ensure the accuracy of information given to regulators.

E. All of the above.

Answer:

The type of swap that is in the largest segment of the global swap market is A. a

commodity swap.

B. a credit swap.

C. a currency swap.

D. an equity swap.

E. an interest rate swap.

Answer:

In calculating the value at risk (VAR) of fixed-income securities in the RiskMetrics

modelA. the VAR is related in a linear manner to the DEAR.

B. the price volatility is the product of the modified duration and the adverse yield

change.

C. the yield changes are assumed to be normally distributed.

D. All of the above.

E. Answers B and C only.

Answer:

These organizations were originated to avoid the legal definition of a bank. A. Money

center banks.

B. Savings associations.

C. Nonbank banks.

D. Financial services holding companies.

E. Savings banks.

Answer:

Which of the following is NOT a potential conflict of interest identified by regulators

and academics? A. Salesperson’s stake.

B. Stuffing fiduciary accounts.

C. Bankruptcy risk transference.

D. Procompetitive effects.

E. Third-party loans.

Answer:

Which action of the holding company to help its securities affiliate can damage the

financial health of its banking subsidiary?A. Downstreaming funds from the subsidiary

and then upstreaming it to the securities affiliate.

B. Upstreaming funds from the securities affiliate and then downstreaming it to the

bank subsidiary.

C. Indulging in product diversification.

D. Upstreaming funds from the bank subsidiary and then downstreaming it to the

securities affiliate.

E. Diversifying the earnings stream of a banking company geographically.

Answer:

The tendency of the variance of a bond’s price to decrease as maturity approaches is

called A. open interest.

B. pull-to-par.

C. digital default option.

D. futures option.

E. credit spread call option.

Answer:

What is the estimated risk-adjusted return on capital (RAROC) of this loan. A. 6.36

percent.

B. 7.00 percent.

C. 7.13 percent.

D. 10.55 percent.

E. 25.45 percent.

Answer:

The largest category of assets for broker-dealers as of the beginning of 2012 was A.

receivables from other broker-dealers.

B. securities purchased under agreement to resell.

C. receivables from customers.

D. exchange membership.

E. long position in securities and commodities.

Answer:

Through August 2012, which of the following approximates the amount of dividends

and assessments that the U.S. Treasury has received from entities participating in the

TARP Capital Purchase Program? A. $2.1 billion.

B. $1.2 billion.

C. $12.2 billion.

D. $16.0 billion.

E. $26.25 billion.

Answer:

Given the exercise price of the option, what premium should be paid for this option?A.

$0.2143 per $100 of bond option purchased.

B. $0.4420 per $100 of bond option purchased.

C. $1.2768 per $100 of bond option purchased.

D. $0.2321 per $100 of bond option purchased.

E. $1.1652 per $100 of bond option purchased.

Answer:

Overseas bank is pooling 50 similar and fully amortized mortgages into a pass-through

security. The face value of each mortgage is $100,000 paying 180 monthly interest and

principal payments at a fixed rate of 9 percent per annum.

What is the market (present) value of the mortgage pass-through to the investor if the

interest rates on this risk category of securities decrease to 7 percent? (Note that

investors receive payments net of the 50 basis points servicing fees.)A. $4,892,200.

B. $5,000,000.

C. $5,152,189.

D. $5,477,910.

E. $5,675,005.

Answer:

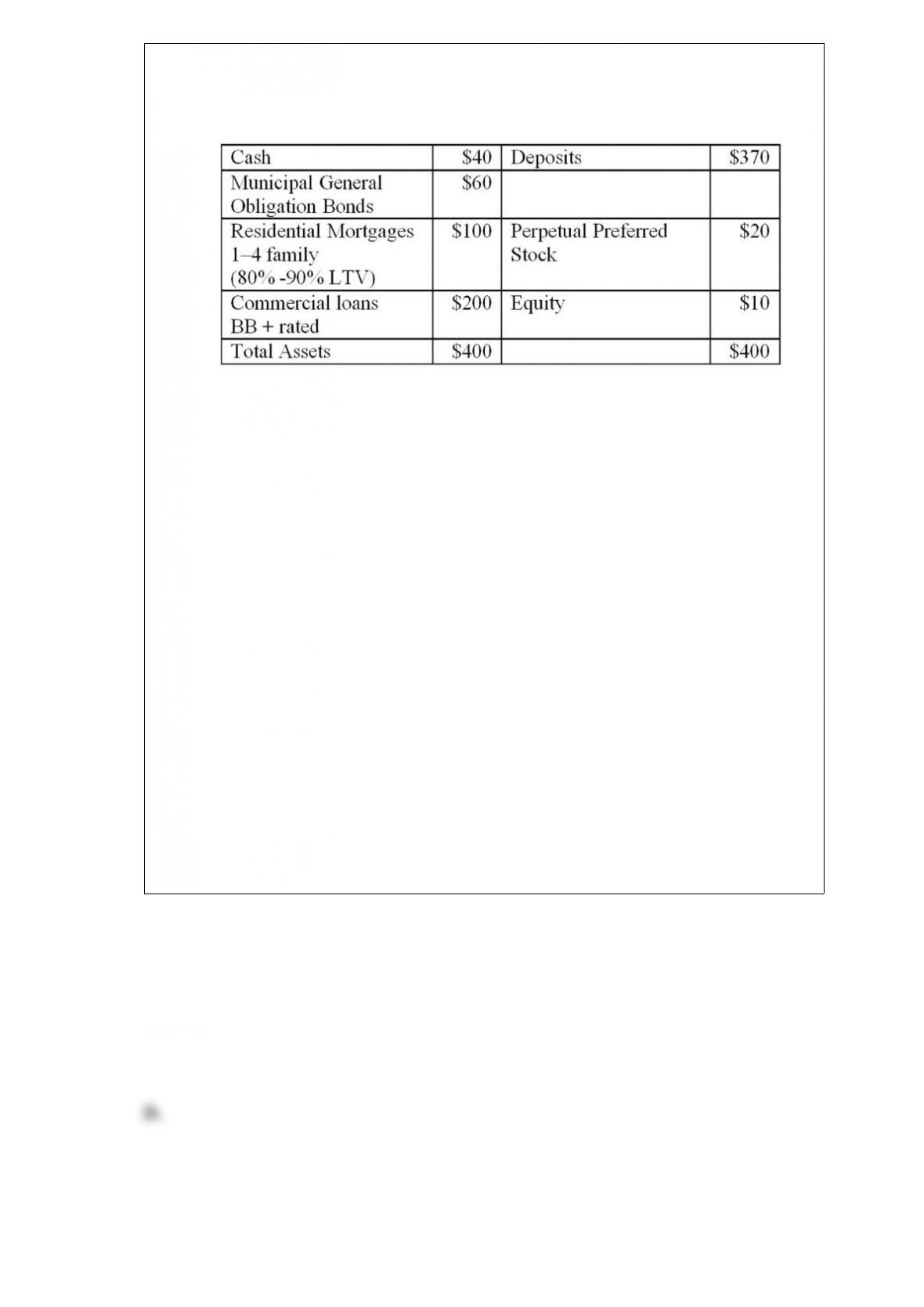

Sigma Bank has the following balance sheet in millions of dollars. Unless mentioned

otherwise, all assets are associated with corporate customers (not governments or

sovereigns). Values are in millions of dollars. Refer to table 20-8 for appropriate risk

weights.

Off balance sheet contingent liabilities (Refer to Table 20-10)

$40 million direct-credit substitute standby letters of credit issued to a U.S. corporation.

$40 million commercial letters of credit issued to a corporation

Off-balance sheet derivatives (Refer to Table 20-11)

$200 million 10-year interest rate swaps

$100 million 2-year forward DM contracts

What is Sigma Bank’s risk-adjusted assets as defined by the Basel standards for its

on-balance-sheet assets only? A. $400 million.

B. $360 million.

C. $310 million.

D. $287 million.

E. $236 million.

Answer:

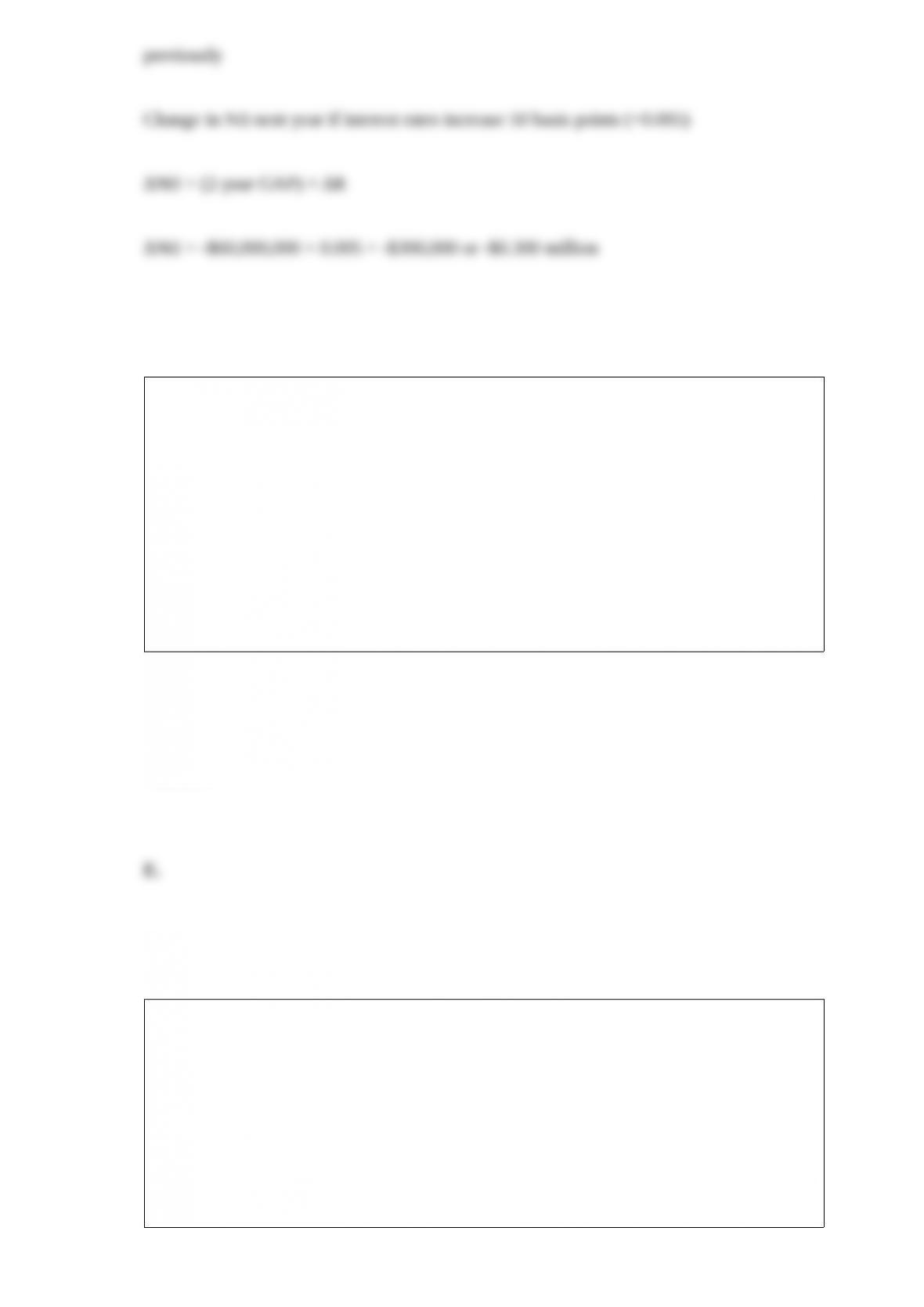

The following is the balance sheet of Boston Bank. The average maturity of demand

deposits is estimated at 2 years.

What is

the impact on net interest income in year two if interest rates increase by 50 basis points

at the end of year one? Ignore runoffs.A. +$0.210 million.

B. +$0.300 million.

C. -$0.300 million.

D. -$0.210 million.

E. +$0.600 million.

Answer:

From the perspective of an FI, which of the following is an advantage of a floating-rate

loan? A. Stable interest payments will be received throughout the loan period.

B. The pre-specified interest rate remains in force over the loan contract period no

matter what happens to market interest rates.

C. The bank can request repayment of a loan at any time in the contract period.

D. The default risk is completely eliminated.

E. The interest rate risk is transferred to the borrower.

Answer:

What is the duration of the commercial loans? A. 1.00 years.

B. 2.00 years.

C. 1.73 years.

D. 1.91 years.

E. 1.50 years.

Answer:

Why have purchased liquidity management techniques become very popular in spite of

its limitations?A. Because it insulates the assets of an FI from normal drains on

liability liquidity.

B. Because funds can be easily raised in the eventuality of a liquidity crunch.

C. Because of decrease in the cost of funds during periods of high interest rate

volatility.

D. Because the funds are covered by deposit insurance.

E. Because the adjustment to the deposit drain occurs on the liability side of the

balance sheet.

Answer:

Identify a condition under which conflicts of interest are exploitable. A. Market for

bank service is very competitive.

B. Banks have monopoly power over their customers.

C. Information flows between the customer and the bank are symmetric.

D. Bank does not possess any information advantage over its customers.

E. Bank places a relatively high value on its reputation.

Answer:

Traditionally, the percentage of depository institutions’ assets funded by some form of

liability is approximately A. 50 percent.

B. 75 percent.

C. 85 percent.

D. 90 percent.

E. 40 percent.

Answer:

Suppose Kansas Bank wants to ensure that its maximum loss on a secured

(collateralized) loan is 10 percent (as a percent of capital). If it wishes to keep a

concentration limit at 40 percent for secured loans, what is the estimated amount lost

per dollar of defaulted secured loan?A. 40 cents.

B. 35 cents.

C. 30 cents.

D. 25 cents.

E. 20 cents.

Answer:

The asset transformation function potentially exposes the FI to A. foreign exchange

risk.

B. technology risk.

C. operational risk.

D. trading risk.

E. interest rate risk.

Answer:

Which of the following is the primary factor that determines the fixed and floating rates

set at the time an interest rate swap is initiated? A. Actual market rates that materialized

over the life of the swap contract.

B. London interbank offer rate (LIBOR).

C. Upfront fee payments.

D. Market’s expectations of future short-term rates.

E. Varying notional values underlying the swap.

Answer:

What must be the minimum annual cost savings in order to accept this project? Assume

a five-year horizon and 8 percent discount rate. A. $200,000.

B. $222,256.

C. $250,456.

D. $279,724.

E. $500,913.

Answer:

Market interest rates are expected to increase 1 percent to 11 percent in the next year. If

this occurs, what will be the effect on the market value of equity of Allright? A.

-$801,818.

B. -$2,430,909.

C. -$6,529,091.

D. +$2,430,909.

E. +$2,532,727.

Answer:

Which of the following statements is FALSE? A. A financial intermediary specializes

in the production of information.

B. A financial intermediary reduces its risk exposure by pooling its assets.

C. A financial intermediary benefits society by providing a mechanism for payments.

D. A financial intermediary may act as a broker to bring together funds deficit and

funds surplus units.

E. A financial intermediary acts as a lender of last resort.

Answer: