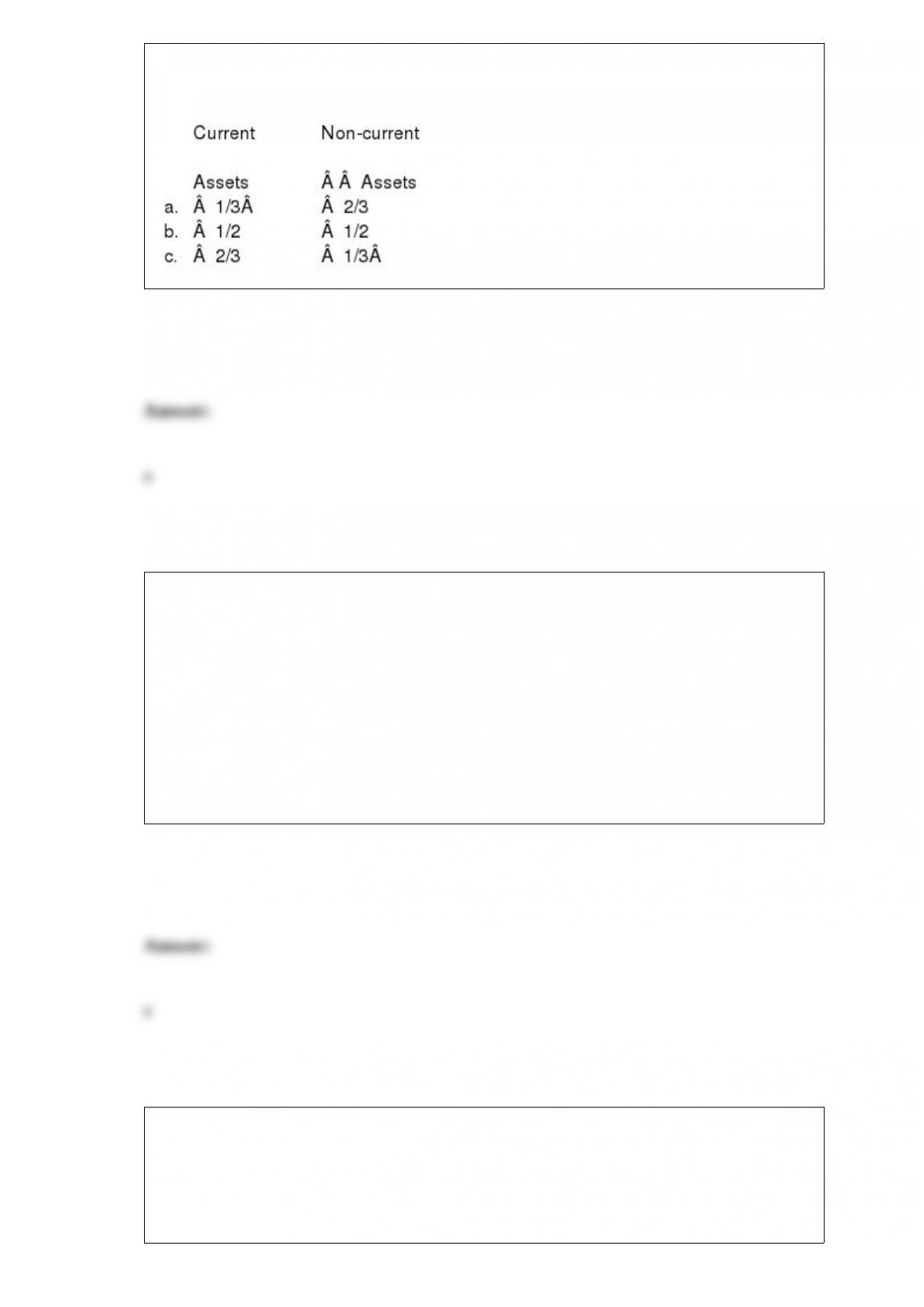

For public U.S. nonfinancial firms in composite, the fractions of current assets and

non-current assets (all in book values; year-end 2000) are approximately:

Which of the following is NOT one of the six fundamental factors that determine the

optimal source of debt funding for a firm?

a. the firm’s debt ratio

b. lender’s need to monitor the borrower’s operations

c. information asymmetry, and specifically the problem of assessing creditworthiness

d. the firm’s need for flexibility

Regarding components and elements of the firm’s business architecture, which of the

following represents the logical direction of causality (i.e., in terms of which

component/element drives another component/element) generally runs as follows

(indicated by arrows):

a. macroeconomic & fin. market environments →internal legal & governance

structures.

b. diversification versus focus→industry characteristics.

c. business strategies and growth opportunities→financial market environment.

d. size and capital intensity→ macroeconomic & financial market environments.

Monitoring is one means by which creditors can control a borrower’s incentive to

expropriate wealth from the creditors. However, direct monitoring of a borrower’s

actions is more difficult in a public bond issue than in a private bond issue because of

the:

a. free-rider problem.

b. requirement of registration with the SEC for a public bond issue.

c. moral hazard problem.

d. adverse selection problem.

One shortcoming of the traditional capital budgeting paradigm is that:

a. it does not recognize that projects must be evaluated on the basis of their NPVs.

b. it does not recognize that the firm may face capital rationing.

c. it does not deal with why some firms have multiple activities

The two constructs that form a firm’s organizational architecture are:

a. business architecture and economic architecture.

b. economic architecture and financial architecture.

c. business architecture and financial architecture.

d. organizational hierarchy and financial structure.

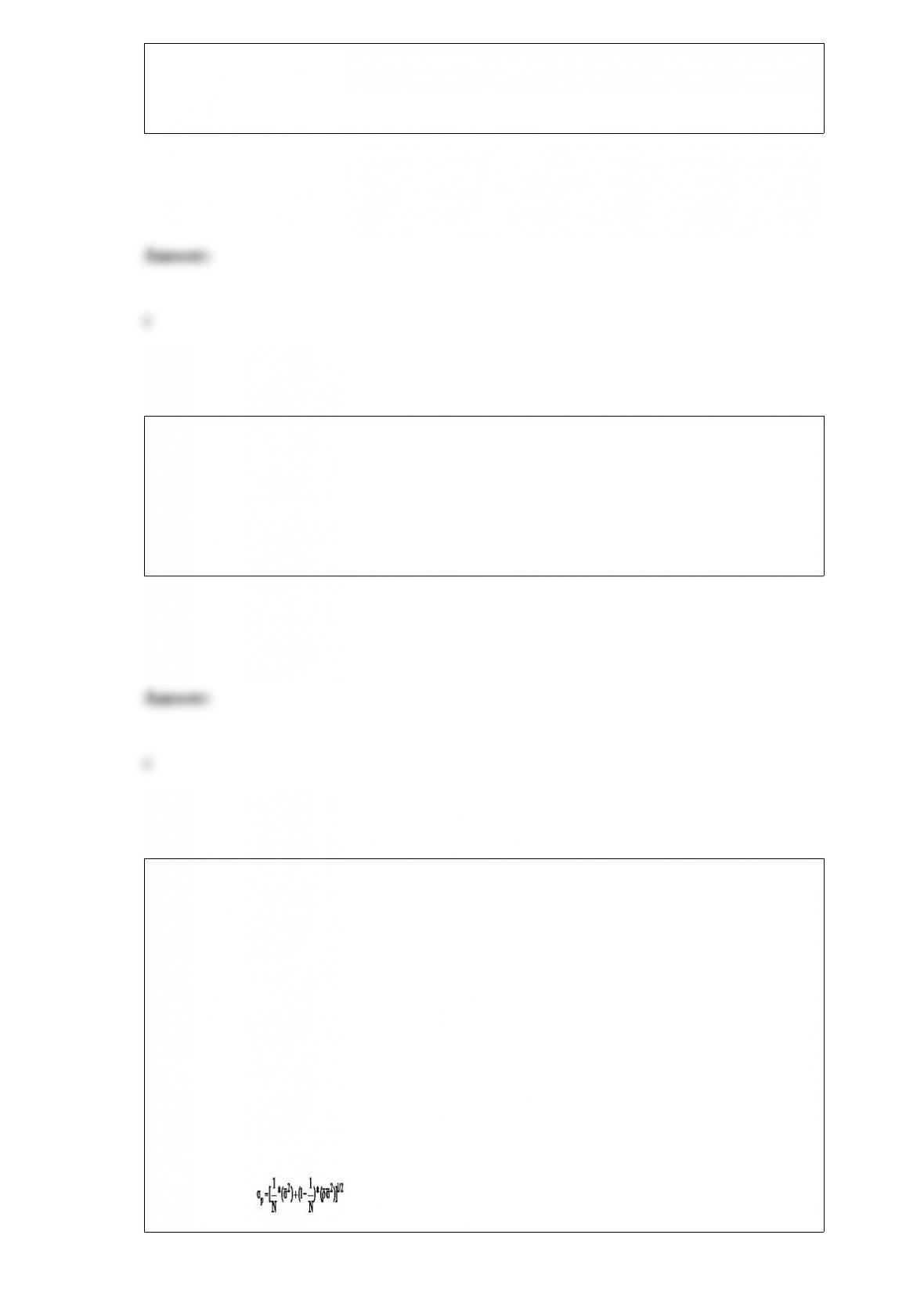

Suppose you develop a mutual fund that includes 78 stocks, all with equal weights in

the fund’s portfolio. The average standard deviation of the stocks is 44%, and the

average pair-wise correlation among the stocks is 0.30. What is your estimate of the

standard deviation of the fund’s portfolio?

a. 19.5%

b. 24.5%

c. 29.5%

d. 34.5%

FORMULA:

What is a unit IPO?

a. An IPO of a previous unit (or division) of a firm that is being spun off of its parent.

b. A package that includes both common stock and warrants.

c. An IPO of common shares that is sold in bulk (i.e., as a unit) to a single investor.

Investment banks form a temporary alliance, called a ______, to underwrite a bond

issue.

a. selling group

b. syndicate

c. coalition

d. pricing association

In response to competition from the Eurobond market, the SEC adopted _______ in

1990, which allows firms to issue bonds in the U.S. market with minimal regulatory red

tape as long as they are sold only to qualified investors (e.g., financial institutions).

a. the Nonregistration Exception

b. Qualified Investors Rule (QIR)

c. Rule 99B

d. Rule 144A

For which of the periods below was U.S. macroeconomic performance poorest?

a. 1960-1973

b. 1974-1982

c. 1983-2000

Which of the following is NOT a valid reason for a firm to establish subsidiaries?

a. to better control risk exposure of either parent-to- subsidiary or subsidiary-to-parent.

b. to enhance the company’s ability to evaluate individual performance and to create

different compensation systems for a diverse set of its businesses.

c. to obfuscate financial reporting.

d. to conform with regulatory requirements specific to a particular business

environment.

TRUE or FALSE: For distressed firms with both bank and public debt outstanding,

banks never make concessions unless public debtholders also restructure their claims.

a. TRUE

b. FALSE

Suppose a venture requires $7 mn. in equity financing to move to the next stage of

development. The firm’s management is negotiating with a venture capital firm (VC)

for the funding. Assuming that the firm’s business goals are achieved, it will generate

earnings of $21 mn. per year into perpetuity starting beginning on the harvest date, four

years from now, when the firm will go public. At that time, the firm will be valued in

the market according to a P/E ratio of 18. Thus, the harvest -date value of the firm,

assuming that it is successful, will be $378 mn.(=18[$21 mn.]). However, the

probability that the firm will be successful is only 25%, while the probability of total

failure of the venture is 75%. Therefore, the expected harvest-date value of the firm is

$94.5 mn. (=0.25[$378]). A discount rate of 33% is applied to this value to determine

the present value of the venture, yielding a value of V=$30.2 mn. (=$94.5 mn. /[1.33]4).

Based on this value and the VC’s contribution of $7 mn., what fraction of the firm’s

equity shares should the VC receive?

a. 13.2%

b. 23.2%

c. 33.2%

d. 43.2%

If a firm attempts tocall an outstanding convertible bond, the bondholders:

a. have the preemptory right to convert the bonds into stock.

b. must tender their bonds immediately and receive the call price.

c. must challenge management’s decision to call the bonds via a proxy contest.

d. have the option to keep their bonds outstanding.

In a ________, both firms cease to exist, and a new corporation is established with a

new name, a new board, and/or a new management team.

a. merger

b. acquisition

c. consolidation

d. buyout

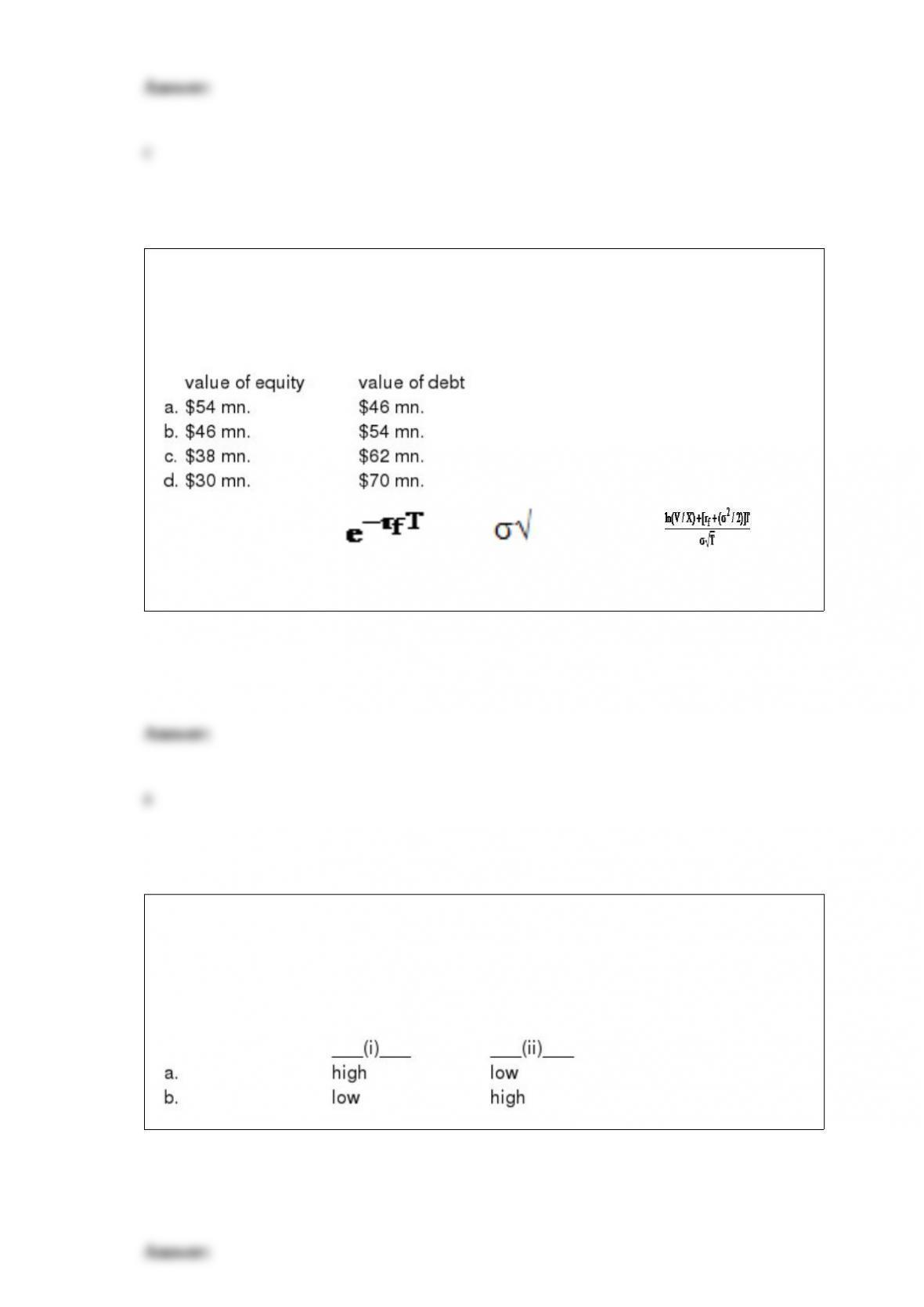

The market value of Delaware East’s assets is $100 mn. The firm has one issue of

pure-discount debt outstanding which promises to pay $60 mn. in 5 years. If the

standard deviation of the firm’s assets is 22% and the risk-free rate is 5%, what are the

values of the firm’s equity and debt, based on the Black-Scholes model?

FORMULA: C=VN(d) – XN(d- T), where d=

(Also need Cum. Normal Distr. Fn. table)

Perhaps the best circumstance that would lead to gains for the shareholders of both the

bidder and the target in a takeover is when a well-managed firm takes over a poorly

managed firm. Thus, the greatest gains in those takeovers in which the bidder has a

___(i)___ Tobin’s q ratio (is well managed) and the target has a ___(ii)___ q ratio (is

poorly managed). Evidence supports this argument.

What types of firms are most likely to go public via a unit IPO?

a. larger, older, more established firms

b. smaller, younger, more speculative firms

According to the composite sources-and-uses data presented in Chapter 1, the main net

source of funds for U.S. nonfinancial firms over the years 1980-2000 is:

a. proceeds from debt offerings.

b. proceeds from equity offerings.

c. retained earnings (net cash flow from operations).

d. sales of investments (net of increases in investments).

Economies of scale are present where the cost of producing each unit declines as the

quantity of product produced increases. In this environment, large-scale firms have a

cost advantage. Thus, economies of scale serve to _______ the cost of entry into an

industry.

a. increase

b. decrease

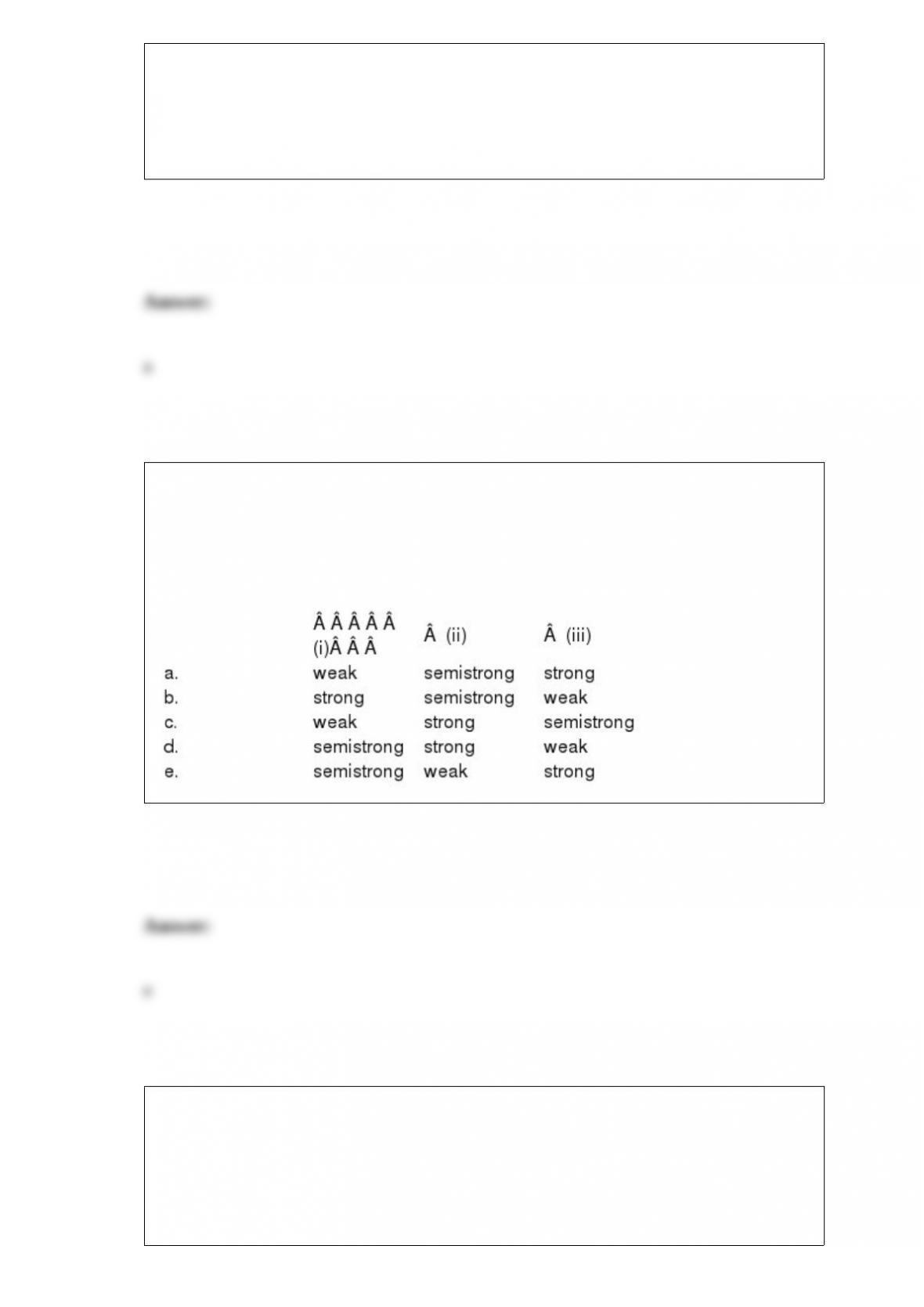

In the ____(i)____ of the efficient market hypothesis (EMH), a security’s price reflects

all publicly available information. In the _____(ii)____ form of the EMH, a security’s

price reflects all information that may be contained in the historical prices of a security.

In the ____(iii)____ of the EMH, a security’s price reflects all information, whether it is

public information or information held privately.

The VC industry did not become a major force in financing ventures until which TWO

problems were solved?

a. informational asymmetry and principal-agent problems

b. legislation allowed institutional investors to provide significant capital backing, and

an effective legal-liability arrangement for contributing parties was devised

c. contracting problems with the venture and compensation for executives

d. financing problems (i.e., debt vs. equity) and the underinvestment problem

The bidder in a takeover generally should take advantage of temporary anonymity to

purchase shares of the target before its intentions are publicly known and the target

firm’s price rises. Such initial purchases establish a _______.

a. foothold

b. leghold

c. armhold

d. toehold

Which of the following is NOT an element of investors’ preferences that influences a

firm’s financial architecture?

a. preferences for work vs. leisure

b. liquidity needs

c. investment horizon

d. risk tolerance

TRUE or FALSE: A merger announcement induces a substantial positive abnormal

return on the acquiring firm’s stock (approximately 20%, on average), while the target

firm’s stockholders are either unaffected or sustain small losses, on average.

a. TRUE

b. FALSE

The __________ provision in a corporate bond contract requires the firm to retire a

specified percentage of the bonds each year, typically after a deferment period of 5 to

10 years.

a. sinking fund

b. call

c. put

d. conversion

The public market for newspeculative-grade bonds, also known as high-yield or junk

bonds, was created virtually single-handedly by Michael Milken and his firm, Drexel

Burnham Lambert, in the late 1970s. Prior to that time, the only corporate bonds that

carried a speculative-grade rating were so-called _______, bonds that initially garnered

an investment-grade rating, but later the issuer experienced financial distress so that

their rating fell into the speculative-grade category.

a. discount bonds

b. concession bonds

c. fallen angels

d. cut rate bonds

Which of the following was NOT mentioned by Akerlof to mitigate the lemons

problem?

a. certification

b. using a costly signal

c. private negotiation

d. establishing a reputation

e. contract enforcement

A speculative-grade bond that had an investment-grade rating when it was originally

issued is called a ___(i)___, while an original-issue speculative-grade bond is called a

___(ii)___.

According to the finance literature related to informational asymmetry, one of the most

important roles of an investment-banking firm (in terms of assisting a firm in issuing

securities to the public) is to vouch for the value of the security, after it has obtained

confidential information from the firm’s management about its business strategy. This

vouching is known as:

a. certification

b. using a costly signal

c. private negotiation

d. establishing a reputation

e. contract enforcement

An IPO firm has a choice of two methods of selling shares. In the ___(i)___ method,

the underwriter essentially acts as a ___(ii)___, agreeing to purchase all shares offered

at a fixed price, and then takes the risk of reselling the shares to the public. In the

___(iii)___ method, the underwriter essentially acts as a ___(iv)___, agreeing only to

conduct a search for interested buyers.

_________ obtains in a merger if some aspect of the financial configuration of the

merged firm causes its market value to be greater than the sum of the market values of

the separate firms.

a. Operating synergy

b. Financial synergy

c. Business synchronization

d. Economies of scope

In the configuration of an efficient financial system architecture, both banks and capital

markets offer lending to firms. Borrowers who pose relatively onerous

asset-substitution moral hazard prefer ___(i)___ financing, while borrowers who pose

less serious moral hazards go directly to ___(ii)___.