Larger coupon payments on a fixed-income asset cause the present value weights of the

cash flows to be lower in the duration calculation.

Answer:

The Insurance Regulatory Information System (IRIS) is a standardized examination

system used to measure the profitability of insurance companies.

Answer:

The Federal Reserve System has regulatory supervision over all holding company

banks whether they include national- or state-chartered banks.

Answer:

The market value of a fixed-rate liability will decrease as interest rates rise, just as the

market value of a fixed-rate asset will decrease as interest rates rise.

Answer:

The number of investment banks and securities firms expanded rapidly from 1980 to

October 198

Answer:

Which of the following is TRUE of off-balance-sheet activities?A. They involve

generation of fees without exposure to any risk.

B. They include contingent activities recorded in the current balance sheet.

C. They invite regulatory costs and additional “taxes.”

D. They have both risk-reducing as well as risk-increasing attributes.

E. The risk involved is best represented by notional or face value.

Answer:

The foreign exchange market in Tokyo is the largest FX trading market.

Answer:

Market value accounting often is criticized because the error in market valuation of

nontraded assets likely will be greater than the error using the original book valuation.

Answer:

The penalty for undershooting the minimum reserve requirements may include explicit

interest rate charges as well as implicit costs in the form of more frequent monitoring

and examinations.

Answer:

When computing the liquidity coverage ratio, high-quality liquid assets are divided into

two levels.

Answer:

Principal transactions allow the market maker to always make a profit regardless of

whether the market price for a specific stock is rising or falling.

Answer:

Assets and liabilities that are expected to require extensive time to liquidate are

normally placed in the investment portfolio.

Answer:

Credit risk applies only to bond investment and loan portfolios of FIs and banks.

Answer:

Which of the following is TRUE of sovereign bonds?A. They are bonds backed by

collateral.

B. Brady bonds are replacing them because of their higher interest rates.

C. Their benefit is the ‘saving” from not having to pledge U.S. Treasury bonds as

collateral.

D. Their value partly reflects the value of collateral underlying the principal and/or

interest on the issue.

E. They are not a segment in the secondary market for sovereign debt.

Answer:

The adverse effects on the economy that can occur because of major disturbances to the

special functions or services provided by financial institutions are negative

externalities.

Answer:

General macroeconomic risks may affect all risks of a financial institution.

Answer:

Investing in a zero-coupon asset with a maturity equal to the desired investment horizon

is one method of immunizing against changes in interest rates.

Answer:

Banks in the countries that are members of the BIS must use the standardized

framework to measure market risk exposures.

Answer:

The regulatory practice of excessive capital forbearance is a method of reducing the

short-run and long-run costs to deposit insurance funds.

Answer:

The error from using duration to estimate the new price of a fixed-income security will

be less as the amount of convexity increases.

Answer:

The use of off-balance-sheet activities allows banks to practice regulatory

tax-avoidance.

Answer:

The expected loss potential is more difficult to determine with low-severity,

high-frequency events.

Answer:

The proportion of financial assets controlled by depository institutions has been

increasing in recent years.

Answer:

One way to boost the capital to assets ratio of an FI is through loan sales.

Answer:

Technology risk is the uncertainty that economies of scale or scope will be realized

from the investment in new technologies.

Answer:

Passbook savings accounts normally receive a lower interest rate than NOW accounts.

Answer:

The change to decimalization of stock market transactions has lead to an increase in

income from the market making activity of investment banks and securities firms.

Answer:

The policy that will pay a specific dollar benefit to beneficiaries and remains in effect

as long as premiums are paid is called whole life.

Answer:

Success in a merger from revenue enhancement is more likely if the markets into which

expansion occurs are less than fully competitive.

Answer:

Under FDICIA, regulators are required to take prompt corrective action steps when a

DI falls outside of Zone 1.

Answer:

GNMA is a privately-owned entity.

Answer:

The mergers of Citicorp with Travelers Insurance is an example of an attempt to exploit

economies of scope.

Answer:

If losses on a particular line of fire insurance were $430 million, premiums earned were

$595 million, and loss adjustment expenses were $95 million, the combined ratio would

beA. 0.88 implying that this line of insurance is profitable.

B. 0.88 implying that this line of insurance is unprofitable.

C. 1.13 implying that this line of insurance is profitable.

D. 1.13 implying that this line of insurance is unprofitable.

E. 0.22 implying that this line of insurance is profitable.

Answer:

As commercial banks move from their traditional banking activities of deposit taking

and lending and shift more of their activities to trading, they are more subject to A.

credit risk.

B. market risk.

C. political risk.

D. sovereign risk.

E. liquidity risk.

Answer:

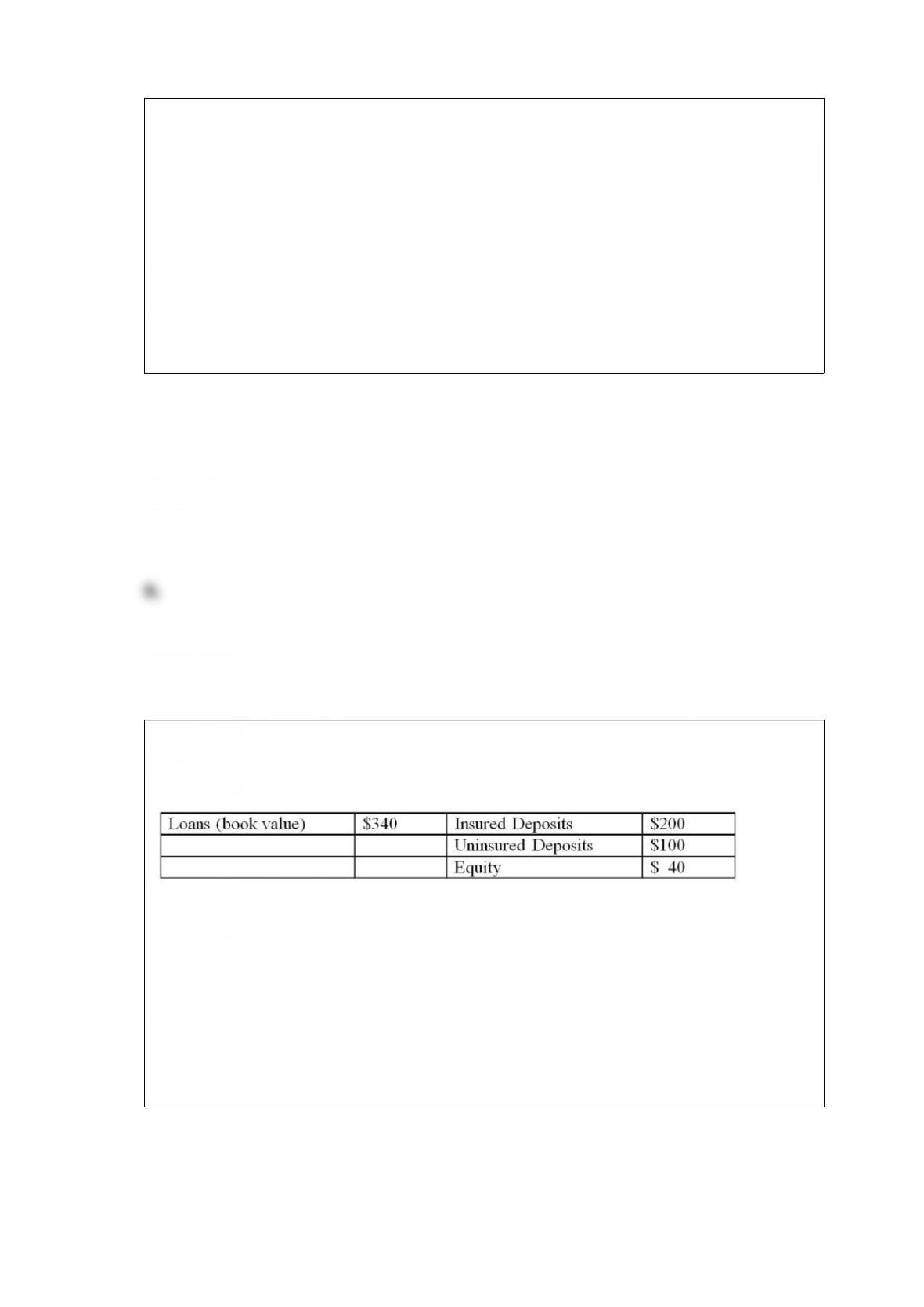

As a result of loan write-offs, Bank A has to be liquidated by the regulators. The book

value of the assets and liabilities of the bank is presented below (in millions of dollars).

The market value of the loans has been estimated at $240 million.

What is

the current net worth (market value) of the bank? A. +$40 million.

B. $0 million.

C. -$40 million.

D. -$60 million.

E. -$100 million.

Answer:

The average maturity of the liabilities of an FI’s balance sheet is equal toA. the

weighted-average of the liabilities where the weights are determined relative to the total

liabilities and equity of the FI.

B. the weighted-average of the liabilities where the weights are determined relative to

the total liabilities of the FI.

C. the weighted-average of the liabilities where the weights are determined relative to

the total assets of the FI.

D. the weighted-average of the liabilities where the weights are determined using

market values of liabilities.

E. None of the above.

Answer:

The largest asset on property-casualty insurers’ balance sheet as of 2012 was A. cash.

B. bonds.

C. common stock.

D. short-term securities.

E. mortgages and mortgage-backed investments.

Answer:

Depository institutions (DIs) play an important role in the transmission of monetary

policy from the Federal Reserve to the rest of the economy primarily because A. loans

to corporations are part of the money supply.

B. bank loans are highly regulated.

C. savings institutions provide a large amount of credit to finance residential real

estate.

D. DI deposits are a major portion of the money supply.

E. U.S. DIs compete with foreign financial institutions.

Answer:

Bank risk taking can be controlled by increasing A. stockholder discipline by charging

stockholders a surcharge.

B. stockholder discipline by setting risk adjusted deposit insurance premiums.

C. depositor discipline by increasing the ceiling for deposit insurance coverage.

D. regulatory discipline by increasing the budgets of the regulatory agencies.

E. depositor discipline by expanding the doctrine of “too big to fail.”

Answer:

One of the primary reasons that investment banks were allowed to convert to bank

holding companies during the recent financial crisis was recognition that A. their

operating activities were too risky and they needed the cushion of bank deposits to

alleviate funding risks.

B. the industry had acquired too much capital during the previous decade.

C. bank holding companies needed the ability to underwrite new issues of corporate

securities.

D. it was the only way an investment bank could qualify for federal bailout funds.

E. the Federal Reserve was unable to purchase troubled assets from investment banks,

but they could from bank holding companies.

Answer:

Which of the following statements does not reflect a borrower-specific factor often used

in qualitative default risk models? A. Reputation is an implicit contract regarding

borrowing and repayment that extends beyond the formal explicit legal contract.

B. A borrower’s leverage ratio is positively related to the probability of default over all

levels of debt.

C. Firms with high earnings variance are less attractive credit risks than those firms

that have a history of stable earnings.

D. Loans can be collateralized or uncollateralized.

E. Reputation is a key reason why initial public offering of debt securities by small

firms have a higher interest rate than do debt issues of more seasoned borrowers.

Answer:

Why are the class C bonds highly attractive to insurance companies and pension funds?

A. Because of their ability to offer perfect prepayment protection.

B. Because of the shortest average life with a minimum of prepayment protection.

C. Because of their long expected duration.

D. Because they are basically zero coupon bonds and hence carry a minimum amount

of risk.

E. Answers A and D only.

Answer:

Using a strict market value accounting might cause regulators to A. revert to book

value accounting in order to determine net worth.

B. close banks too early under prompt corrective action requirements.

C. exempt Dis from prompt corrective action.

D. allow banks to operate without oversight even with negative net worth.

E. suspend regulatory capital requirements during temporary spikes in interest rates.

Answer:

It is common to include A. both the interest and principal payments in an interest rate

swap.

B. only the interest payments in a currency swap.

C. both the interest and principal payments in a currency swap.

D. only the principal payments in an interest rate swap.

E. only the principal payments in a currency swap.

Answer:

According to studies, which of the following may better explain cost differences and

operating cost efficiencies among FIs? A. Diseconomies of scale.

B. Economies of scale.

C. Economies of scope.

D. X-inefficiencies.

E. Diseconomies of scope.

Answer:

Which of the following refers to the regulators’ policy of allowing an FI to continue

operating even when its capital funds are fully depleted? A. Capital forbearance.

B. Prompt corrective action.

C. Risk-based deposit insurance.

D. Too-big-to-fail.

E. Regulatory oversight.

Answer:

Managing the reserve position of a U.S. bank requires knowing A. the target reserve

ratio.

B. the time period over which average deposits are calculated.

C. the time period over which average reserves must be maintained.

D. the asset and liability methods that may be used to meet required reserves.

E. All of the above.

Answer:

What is spread effect?A. Periodic cash flow of interest and principal amortization

payments on long-term assets that can be reinvested at market rates.

B. The effect that a change in the spread between rates on RSAs and RSLs has on net

interest income as interest rates change.

C. The effect of mismatch of asset and liabilities within a maturity bucket.

D. The premium paid to compensate for the future uncertainty in a security’s value.

E. The value of an FI to its owners.

Answer:

An open-ended fund has stocks of three companies: 200 shares of IBM currently valued

at $50.00, 100 shares of GE currently values at $20 and 100 shares of Digital currently

valued at $30. The fund has 500 shares outstanding. What is the net asset value (NAV)

of the fund? A. $30.00.

B. $60.00.

C. $120.00.

D. $12.00.

E. $37.50.

Answer:

Which of the following rely on non-distressed HLT loan purchases as a means of

diversifying without the high cost of developing costly nationwide banking networks?

A. Bank loan mutual funds.

B. Credit unions.

C. Foreign banks.

D. Investment banks.

E. Vulture funds.

Answer:

If the portfolio manager put on the hedge when T-bond futures were quoted at

89-00/32nds, what is the profit/loss on the futures position if the settlement price is

81-27/32nds? A. Profit of $2,146,875.

B. Loss of $2,146,875.

C. Profit of $1,270,000.

D. Loss of $1,270,000.

E. Loss of $812,700.

Answer:

Loan loss reserves are classified as A. on-balance-sheet assets.

B. off-balance-sheet assets.

C. off-balance-sheet liabilities.

D. on-balance-sheet liabilities.

E. equity capital.

Answer:

The first regional banking pact in the U.S. was in A. the Southeast.

B. New England.

C. the Northwest.

D. the Southwest.

E. the Midwest.

Answer:

Which of the following is the primary sellers of credit risk protection? A. Insurance

companies.

B. Mutual funds.

C. Depository institutions.

D. Vulture funds.

E. Commercial banks.

Answer:

As of June 2012, commercial banks had listed for sale option contracts with a notational

value of approximately A. $16.2 trillion.

B. $33.6 trillion.

C. $8.1 trillion.

D. $51.0 trillion.

E. $36.9 trillion.

Answer:

By how much should operating costs of the combined entity (Bank A + Bank B) be

reduced in order to stay competitive in the local market, ceteris paribus?A. $900,000.

B. $600,000.

C. $500,000.

D. $400,000.

E. $300,000.

Answer:

Overseas bank is pooling 50 similar and fully amortized mortgages into a pass-through

security. The face value of each mortgage is $100,000 paying 180 monthly interest and

principal payments at a fixed rate of 9 percent per annum.

What is the monthly payment received by investors of the mortgage pass-through if the

FI deducts a 50 basis points servicing fee? A. $49,237.

B. $50,713.

C. $50,459.

D. $51,200.

E. $52,100.

Answer:

Correspondent banking may involve A. providing banking services to other banks

facing shortage of staff.

B. providing foreign exchange trading services to individuals.

C. holding and managing assets for individuals or corporations.

D. acting as transfer and disbursement agents for pension funds.

E. providing hedging services to corporations.

Answer:

Which of the following is NOT a source of operational risk for an FI? A. Capital assets.

B. Customer relationships.

C. Technology.

D. Employees.

E. Positive duration gap.

Answer:

An FI funds a $5 million residential mortgage in 2012 by allocating capital and by

issuing demand deposits. The mortgage represents a loan-to-value of 70 percent. The

demand deposits have a reserve requirement of 10 percent and a deposit insurance

premium of 23 basis points.

What amount of demand deposits are needed to fund the mortgage? A. $5,500,000.

B. $400,000.

C. $5,555,555.

D. $500,000.

E. $5,000,000.

Answer:

Which of the following currently manages the insurance funds for both commercial

banks and savings institutions? A. FDIC.

B. FSLIC.

C. OCC.

D. FRS.

E. State authorities.

Answer:

Which of the following assets have not been securitized by FIs? A. Mortgages.

B. Credit card receivables.

C. Auto loans.

D. Debts of Lesser Developed Countries (LCD debt).

E. Student loans.

Answer:

A swap that often involves an up-front fee or payment as compensation for nonstandard

terms is A. a pure credit swap.

B. a total return swap.

C. an off-market swap.

D. a plain vanilla swap.

E. an interest rate swap.

Answer:

Mutual funds that purchase Treasury bills, bank negotiable certificates of deposit,

commercial paper, and other short-term securities would be classified as A. contractual

institutions.

B. investment institutions.

C. money market funds.

D. securities dealers.

E. PC insurance companies.

Answer: