Metals and energy currency futures contracts are actively traded on

A. copper.

B. platinum.

C. weather.

D. copper and platinum.

E. All of the options are correct.

If the interest rate on debt is lower than ROA, then a firm will __________ by

increasing the use of debt in the capital structurE.

A. increase the ROE

B. not change the ROE

C. decrease the ROE

D. change the ROE in an indeterminable manner

In 2016, the proportion of mutual funds (based on total assets) specializing in common

stocks was

A. 21.7%.

B. 28.0%.

C. 52.1%.

D. 73.4%.

E. 63.5%.

In the results of the earliest estimations of the security market line by Miller and

Scholes (1972), it was found that the average difference between a stock’s return and

the risk free rate was ________ to its nonsystematic risk and ________ to its beta.

A. positively related; negatively related

B. negatively related; positively related

C. positively related; positively related

D. negatively related; negatively related

E. not related; not related

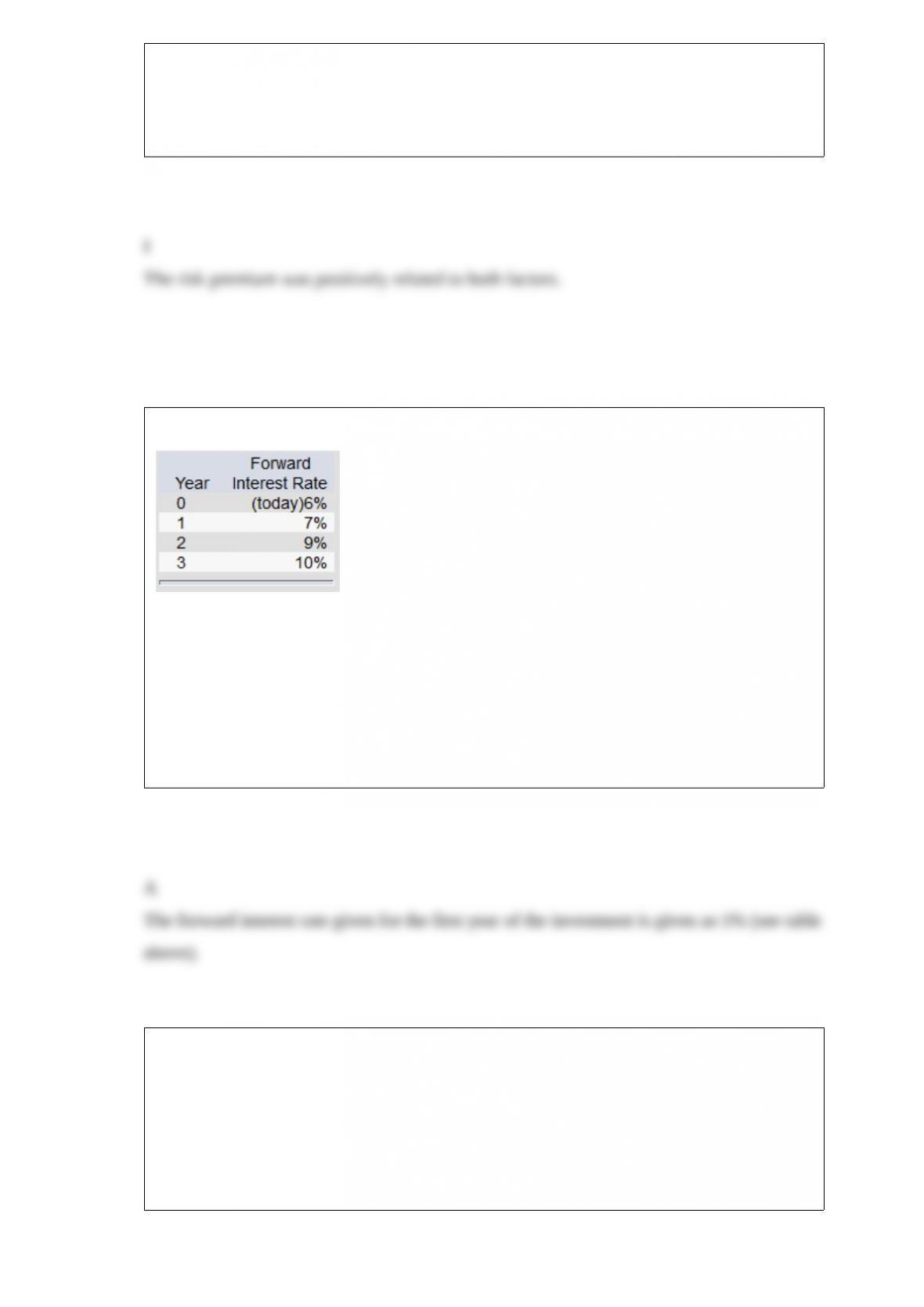

Suppose that all investors expect that interest rates for the 4 years will be as follows:

If you have just purchased a 4-year zero-coupon bond, what would be the expected rate

of return on your investment in the first year if the implied forward rates stay the same?

(Par value of the bond = $1,000)

A. 5%

B. 7%

C. 9%

D. 10%

E. None of the options are correct.

You sell short 100 shares of Loser Co. at a market price of $45 per share. Your

maximum possible loss is

A. $4,500.

B. unlimited.

C. zero.

D. $9,000.

E. Cannot be determined from the information given.

Given an optimal risky portfolio with expected return of 20%, standard deviation of

24%, and a risk free rate of

7%, what is the slope of the best feasible CAL?

A. 0.64

B. 0.14

C. 0.62

D. 0.33

E. 0.54

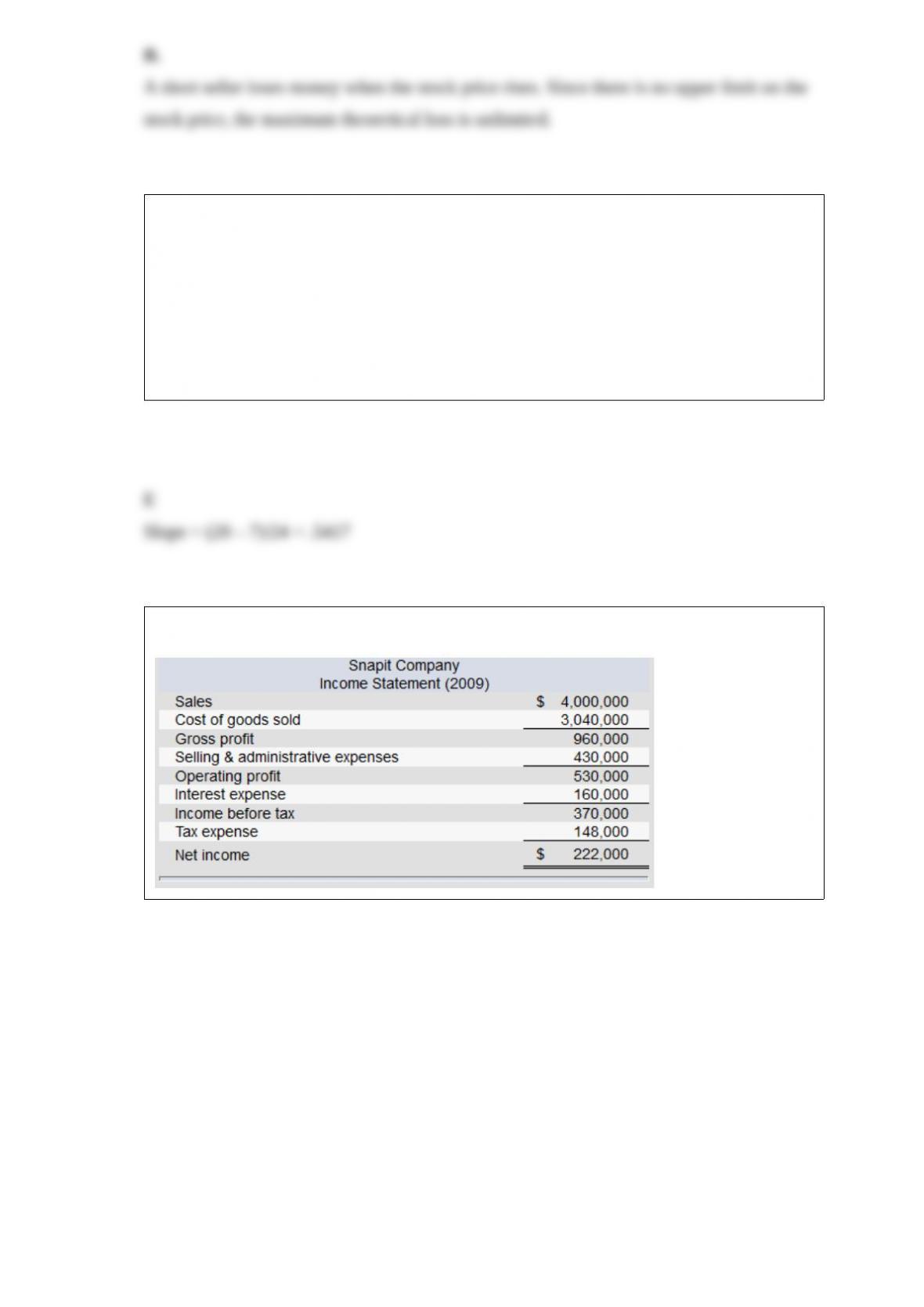

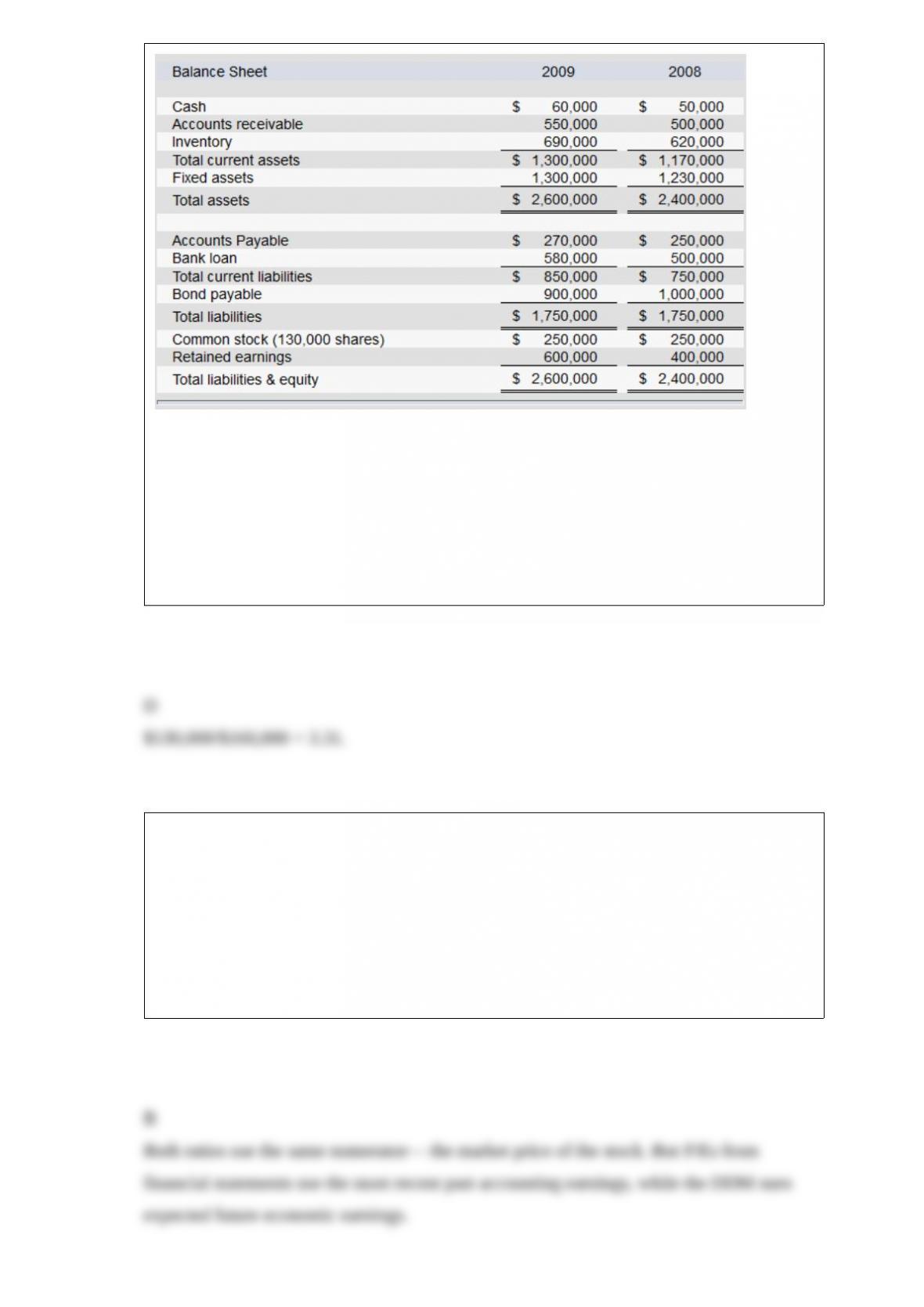

The financial statements of Snapit Company are given below.

Note: The common shares are trading in the stock market for $100 each.

Refer to the financial statements of Snapit Company. The firm’s times interest earned

ratio for 2009 is

A. 2.26.

B. 3.16.

C. 3.84.

D. 3.31.

E. None of the options are correct.

The P/E ratio that is based on a firm’s financial statements and reported in the

newspaper stock listings is different from the P/E ratio derived from the dividend

discount model (DDM) because

A. the DDM uses a different price in the numerator.

B. the DDM uses different earnings measures in the denominator.

C. the prices reported are not accurate.

D. the people who construct the ratio from financial statements have inside information.

E. They are not different— this is a “trick” question.

If a portfolio had a return of 18%, the risk-free asset return was 5%, and the standard

deviation of the portfolio’s

excess returns was 34%, the risk premium would be

A. 13%.

B. 18%.

C. 49%.

D. 12%.

E. 29%.

An American put option allows the holder to

A. buy the underlying asset at the striking price on or before the expiration date.

B.sell the underlying asset at the striking price on or before the expiration date.

C. potentially benefit from a stock price increase.

D. sell the underlying asset at the striking price on or before the expiration date and

potentially benefit from a stock price increase.

E. buy the underlying asset at the striking price on or before the expiration date and

potentially benefit from a stock price increase.

An American-style call option with six months to maturity has a strike price of $42. The

underlying stock now sells for $50. The call premium is $14. What is the time value of

the call?

A. $8

B. $12

C. $6

D. $4

E. Cannot be determined without more information

Hedge funds

I) are appropriate as a sole investment vehicle for an investor.

II) should only be added to an already well-diversified portfolio.

III) pose performance-evaluation issues due to nonlinear factor exposures.

IV) have down-market betas that are typically larger than up-market betas.

V) have symmetrical betas.

A. I only

B. II and V

C. I, III, and IV

D. II, III, and IV

E. I, III, and V

__________ refers to the possibility of expropriation of assets, changes in tax policy,

and the possibility of restrictions on foreign exchange transactions.

A. Default risk

B. Foreign exchange risk

C. Market risk

D. Political risk

E. None of the options are correct.

Consider the regression equation:

ritrft = ai + bi(rmtrft) + eit

where:

rit = return on stock i in month t

rft = the monthly risk free rate of return in month t

rmt = the return on the market portfolio proxy in month t

This regression equation is used to estimate

A. the security characteristic line.

B. benchmark error.

C. the capital market line.

D. All of the options are correct.

E. None of the options are correct.

Which of the following are commonly thought to be good general investment

guidelines?

I) Don’t try to outguess the market, buying and holding generally pays off.

II) Diversify investments to spread risk.

III) Investments should be highly concentrated in your company’s stock.

IV) 401K money is best placed in money market accounts because risk is very low.

V) Investments should be allocated to stocks, bonds, and moneymarket funds.

A. I, III, and IV

B. I, II, and V

C. II, IV, and V

D. III, IV, and V

E. I, II, IV, and V

The planning phase of the CFA Institute’s investment management process

A. uses data about the client and capital market.

B. uses details of optimal asset allocation and security selection.

C. uses changes in expectations and objectives.

D. All of the options are correct.

E. None of the options are correct.

Suppose you held a well-diversified portfolio with a very large number of securities,

and that the single index model holds. If the σ of your portfolio was 0.20 and σM was

0.16, the β of the portfolio would be approximately

A. 0.64.

B. 0.80.

C. 1.25.

D. 1.56.

A trough is

A. a transition from an expansion in the business cycle to the start of a contraction.

B.-a transition from a contraction in the business cycle to the start of an expansion.

C. a depression that lasts more than three years.

D. only something used by farmers to feed pigs and not an investment term.

Risk Metrics Company is expected to pay a dividend of $3.50 in the coming year.

Dividends are expected to grow at a rate of 10% per year. The risk-free rate of return is

5%, and the expected return on the market portfolio is 13%. The stock is trading in the

market today at a price of $90.00.

What is the approximate beta of Risk Metrics’s stock?

A. 0.8

B. 1.0

C. 1.1

D. 1.4

E. None of the options are correct.

A professional who searches for mispriced securities in specific areas such as

merger-target stocks, rather than one who seeks strict (risk-free) arbitrage opportunities

is engaged in

A. pure arbitrage.

B. risk arbitrage.

C. option arbitrage.

D. equilibrium arbitrage.

An American-style call option with six months to maturity has a strike price of $35. The

underlying stock now sells for $43. The call premium is $12. What is the time value of

the call?

A. $8

B. $12

C. $0

D. $4

E. Cannot be determined without more information

Firm-specific risk is also referred to as

A. systematic risk or diversifiable risk.

B. systematic risk or market risk.

C. diversifiable risk or market risk.

D. diversifiable risk or unique risk.

A convertible bond has a par value of $1,000 and a current market value of $1,150. The

current price of the issuing firm’s stock is $65, and the conversion ratio is 15 shares.

The bond’s conversion premium is

A. $40.

B. $150.

C. $175.

D. $200.

At expiration, the time value of an at-the-money call option is always

A. positive.

B. equal to zero.

C. negative.

D. equal to the stock price minus the exercise price.

Holding other factors constant, which one of the following bonds has the smallest price

volatility?

A. 20-year, 0% coupon bond

B. 20-year, 6% coupon bond

C. 20 year, 7% coupon bond

D. 20-year, 9% coupon bond

E. Cannot tell from the information given

____________ are good examples of the limits to arbitrage because they show that the

law of one price is violated.

I) Siamese twin companies

II) Unit trusts

III) Closed end funds

IV) Open end funds

V) Equity carve outs

A. I and II

B. I, II, and III

C. I, III, and V

D. IV and V

E. V

A preferred stock will pay a dividend of $6.00 in the upcoming year and every year

thereafter; i.e., dividends are not expected to grow. You require a return of 10% on this

stock. Use the constant growth DDM to calculate the intrinsic value of this preferred

stock.

A. $0.60

B. $6.00

C. $600

D. $60.00

E. None of the options are correct.

Assume that a security is fairly priced and has an expected rate of return of 0.13. The

market expected rate of

return is 0.13, and the risk-free rate is 0.04. The beta of the stock is

A. 1.25.

B. 1.7.

C. 1.

D. 0.95.

If the annual real rate of interest is 3.5%, and the expected inflation rate is 3.5%, the

nominal rate of interest

would be approximately

A. 0%.

B. 3.5%.

C. 12.25%.

D. 7%.

The individual investor’s optimal portfolio is designated by

A. the point of tangency with the indifference curve and the capital allocation line.

B. the point of highest reward to variability ratio in the opportunity set.

C. the point of tangency with the opportunity set and the capital allocation line.

D. the point of the highest reward to variability ratio in the indifference curve.

E. None of the options are correct.

Foreign currency futures contracts are actively traded on the

A. Japanese yen.

B. Australian dollar.

C. Brazilian real.

D. Japanese yen and Australian dollar.

E. All of the options are correct.

Which one of the following statements about convertibles is true?

A. The longer the call protection on a convertible, the less the security is worth.

B. The more volatile the underlying stock, the greater the value of the conversion

feature.

C. The smaller the spread between the dividend yield on the stock and the

yield-to-maturity on the bond, the more the convertible is worth.

D. The collateral that is used to secure a convertible bond is one reason convertibles are

more attractive than the underlying stock.

E. Convertibles are not callable.