Assume you sold short 100 shares of common stock at $70 per share. The initial margin

is 50%. What would be the maintenance margin if a margin call is made at a stock price

of $85?

A. 40.5%

B. 20.5%

C. 35.5%

D. 23.5%

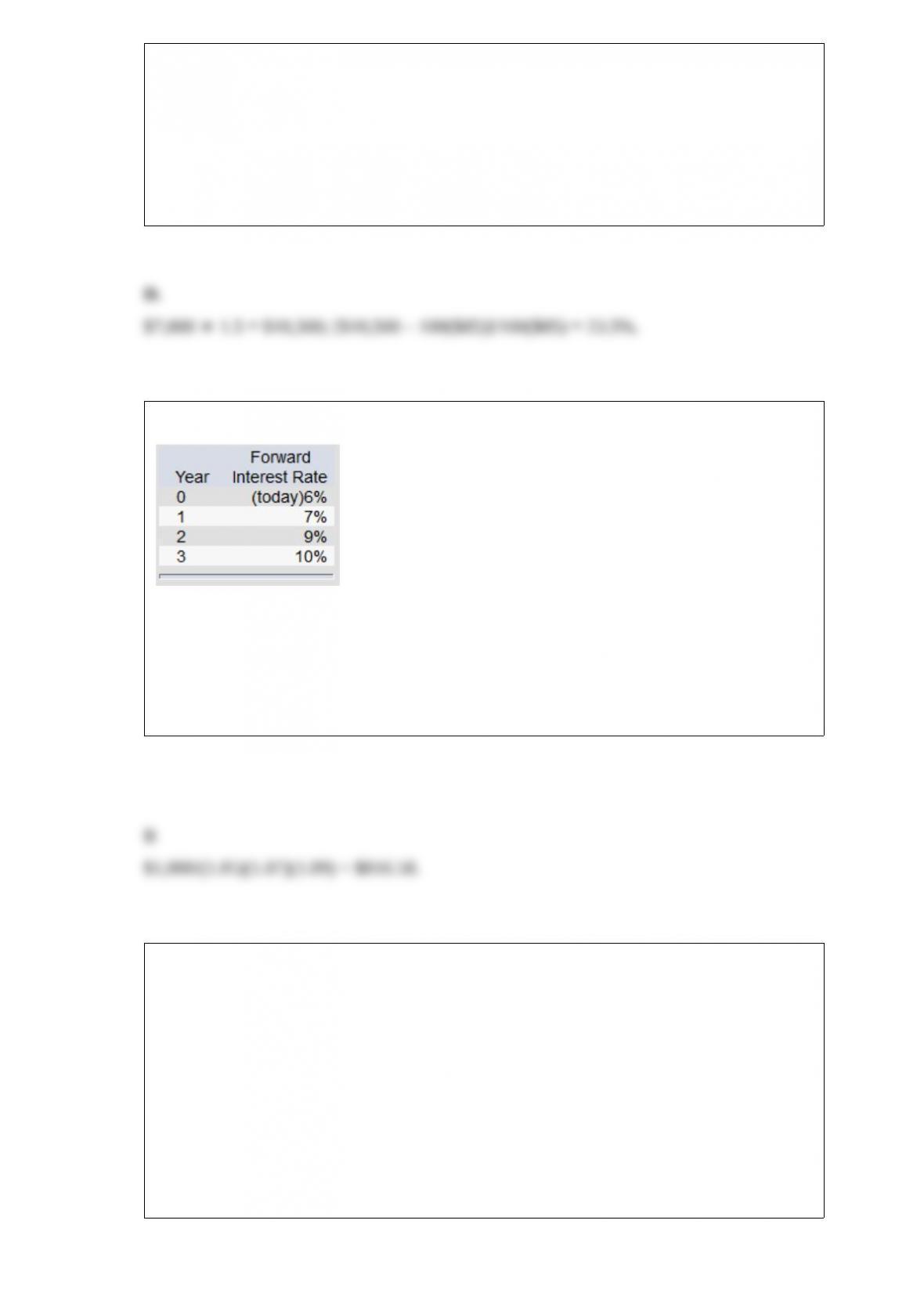

Suppose that all investors expect that interest rates for the 4 years will be as follows:

What is the price of a 3-year zero-coupon bond with a par value of $1,000?

A. $863.83

B. $816.58

C. $772.18

D. $765.55

E. None of the options are correct.

To build an indifference curve, we can first find the utility of a portfolio with 100% in

the risk-free asset, then

A. find the utility of a portfolio with 0% in the risk-free asset.

B. change the expected return of the portfolio and equate the utility to the standard

deviation.

C. find another utility level with 0% risk.

D. change the standard deviation of the portfolio and find the expected return the

investor would require to

maintain the same utility level.

E. change the risk-free rate and find the utility level that results in the same standard

deviation.

_______ are examples of financial intermediaries.

A. Commercial banks

B. Insurance companies

C. Investment companies

D. Credit unions

E. All of the options

Standard deviation and beta both measure risk, but they are different in that beta

measures

A. both systematic and unsystematic risk.

B. only systematic risk, while standard deviation is a measure of total risk.

C. only unsystematic risk, while standard deviation is a measure of total risk.

D. both systematic and unsystematic risk, while standard deviation measures only

systematic risk.

E. total risk, while standard deviation measures only nonsystematic risk.

____________ can be used to measure forecast quality and guide in the proper

adjustment of forecasts.

A.Regression analysis

B. Exponential smoothing

C. ARIMA

D. Moving average models

E. GAUSS

Assume an investor with the following utility function: U = E(r) – 3/2(s2).

To maximize her expected utility, she would choose the asset with an expected rate of

return of _______ and a

standard deviation of ________, respectively.

A. 12%; 20%

B. 10%; 15%

C. 10%; 10%

D. 8%; 10%

In an efficient market the correlation coefficient between stock returns for two

nonoverlapping time periods should be

A. positive and large.

B. positive and small.

C. zero.

D. negative and small.

E. negative and large.

To adjust for stock splits

A.the exercise price of the option is reduced by the factor of the split, and the number of

options held is increased by that factor.

B.the exercise price of the option is increased by the factor of the split, and the number

of options held is reduced by that factor.

C. the exercise price of the option is reduced by the factor of the split, and the number

of options held is reduced by that factor.

D. the exercise price of the option is increased by the factor of the split, and the number

of options held is increased by that factor.

The __________ the proportion of total return that is in the form of price appreciation,

the __________ will be the value of the taxdeferral option for taxable investors.

A. greater; greater

B. greater; lower

C. lower; greater

D. The answer cannot be determined from the information provided.

E. None of the options are correct.

The ____ index represents the performance of the German stock market.

A. DAX

B. FTSE

C. Nikkei

D. Hang Seng

If the currency of your country is depreciating, the result should be to ______ exports

and to _______ imports.

A. increase; increase

B.-increase; decrease

C. decrease; increase

D. decrease; decrease

E. not affect; not affect

WACC is the most appropriate discount rate to use when applying a ______ valuation

model.

A. FCFF

B. FCFE

C. DDM

D. FCFF or DDM, depending on the debt level of the firm,

E. P/E

The interest-rate risk of a bond is

A. the risk related to the possibility of bankruptcy of the bond’s issuer.

B. the risk that arises from the uncertainty of the bond’s return caused by changes in

interest rates.

C. the unsystematic risk caused by factors unique in the bond.

D.the risk related to the possibility of bankruptcy of the bond’s issuer, and the risk that

arises from the uncertainty of the bond’s return caused by changes in interest rates.

E. All of the options are correct.

The security market line (SML) is

A. the line that describes the expected return-beta relationship for well-diversified

portfolios only.

B. also called the capital allocation line.

C. the line that is tangent to the efficient frontier of all risky assets.

D. the line that represents the expected return-beta relationship.

E. All of the options.

Which of the following investments doesnot allow the investor to choose how to

allocate assets?

A. Variable Life insurance policies

B. Keogh plans

C. Personal funds

D. Taxqualified defined contribution plans

E. Universal Life policies

The open interest on silver futures at a particular time is the

A. number of silver futures contracts traded during the day.

B. number of outstanding silver futures contracts for delivery within the next month.

C. number of silver futures contracts traded the previous day.

D. number of all long or short silver futures contracts outstanding.

Hedge funds are typically set up as ______ and provide ______ information about

portfolio composition and strategy to their investors.

A. limited liability partnerships; minimal

B. limited liability partnerships; extensive

C. investment trusts; minimal

D. investment trusts; extensive

WEBS portfolios

A. are passively managed.

B. are shares that can be sold by investors.

C. are free from brokerage commissions.

D. are passively managed and are shares that can be sold by investors. E. All of the

options are correct.

A zero-investment portfolio with a positive expected return arises when

A. an investor has downside risk only.

B. the law of prices is not violated.

C. the opportunity set is not tangent to the capital-allocation line.

D. a risk-free arbitrage opportunity exists.

Financial intermediaries exist because small investors cannot efficiently

A. diversify their portfolios.

B. assess credit risk of borrowers.

C. advertise for needed investments.

D. diversify their portfolios and assess credit risk of borrowers.

E. All of the options.

A trin ratio of less than 1.0 is considered as a

A. bearish signal.

B. bullish signal.

C. bearish signal by some technical analysts and a bullish signal by other technical

analysts.

D. bullish signal by some fundamentalists.

E. bearish signal by some technical analysts, a bullish signal by other technical analysts,

and a bullish signal by some fundamentalists.

A hedge ratio for a put is always

A. equal to one.

B. greater than one.

C. between zero and one.

D. between negative one and zero.

E. of no restricted value.

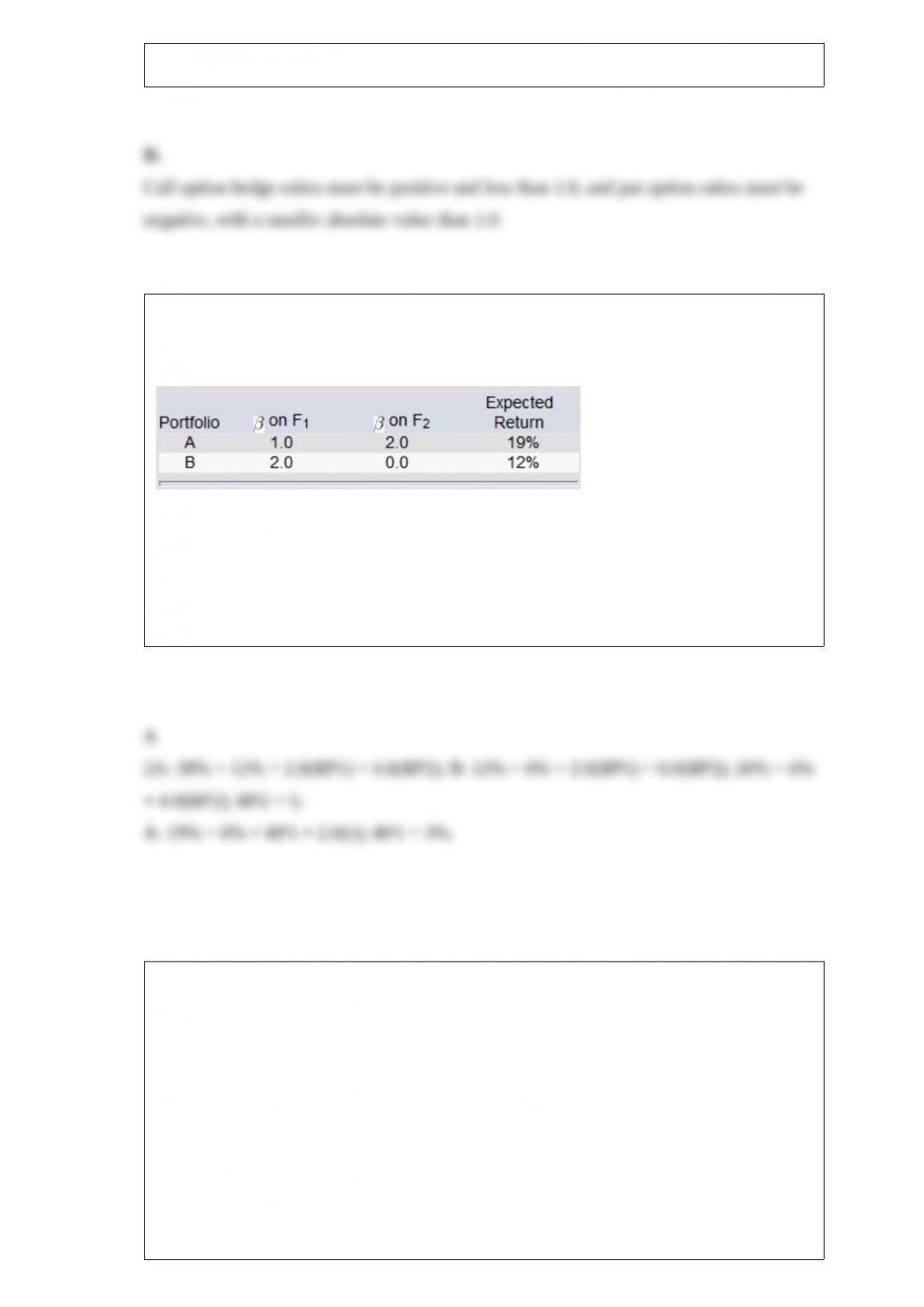

Consider the multifactor APT. There are two independent economic factors, F1 and F2.

The risk-free rate of return is 6%. The following information is available about two

well-diversified portfolios:

Assuming no arbitrage opportunities exist, the risk premium on the factor F1 portfolio

should be

A. 3%.

B. 4%.

C. 5%.

D. 6%.

Steve is more risk-averse than Edie. On a graph that shows Steve and Edie’s

indifference curves, which of the

following is true? Assume that the graph shows expected return on the vertical axis and

standard deviation on

the horizontal axis.

I) Steve and Edie’s indifference curves might intersect.

II) Steve’s indifference curves will have flatter slopes than Edie’s.

III) Steve’s indifference curves will have steeper slopes than Edie’s.

IV) Steve and Edie’s indifference curves will not intersect.

V) Steve’s indifference curves will be downward sloping, and Edie’s will be upward

sloping.

A. I and V

B. I and III

C. III and IV

D. I and II

E. II and IV

Suppose two portfolios have the same average return and the same standard deviation

of returns, but Aggie Fund has a higher beta than Raider Fund. According to the Sharpe

measure, the performance of Aggie Fund

A. is better than the performance of Raider Fund.

B. is the same as the performance of Raider Fund.

C. is poorer than the performance of Raider Fund.

D. cannot be measured as there are no data on the alpha of the portfolio.

As diversification increases, the unsystematic risk of a portfolio approaches

A. 1.

B. 0.

C. infinity.

D. (n – 1) × n.

During periods of inflation, the use of FIFO (rather than LIFO) as the method of

accounting for inventories causes

A. higher reported sales.

B. higher incomes taxes.

C. lower ending inventory.

D. higher incomes taxes and lower ending inventory.

E. None of the options are correct.

Which of the following would increase the net asset value of a mutual fund share,

assuming all other things remain unchanged?

A. An increase in the number of fund shares outstanding

B. An increase in the fund’s accounts payable

C. A change in the fund’s management

D. An increase in the value of one of the fund’s stocks

Suppose you are working with two factor portfolios, portfolio 1 and portfolio 2. The

portfolios have expected returns of 15% and 6%, respectively. Based on this

information, what would be the expected return on well-diversified portfolio A, if A has

a beta of 0.80 on the first factor and 0.50 on the second factor? The risk-free rate is 3%.

A. 15.2%

B. 14.1%

C. 13.3%

D. 10.7%

E. 8.4%