Which statement is not true regarding the capital market line (CML)?

A. The CML is the line from the risk-free rate through the market portfolio.

B. The CML is the best attainable capital allocation line.

C. The CML is also called the security market line.

D. The CML always has a positive slope.

E. The risk measure for the CML is standard deviation.

HighFlyer Stock currently sells for $48. A one-year call option with strike price of $55

sells for $9, and the risk-free interest rate is 6%. What is the price of a one-year put with

strike price of $55?

A. $9.00

B.$12.89

C. $16.00

D. $18.72

E. $15.60

If information processing was perfect, many studies conclude that individuals would

tend to make __________ decisions using that information due to __________.

A. less than fully rational; behavioral biases

B. fully rational; behavioral biases

C. less than fully rational; fundamental risk

D. fully rational; fundamental risk

E. fully rational; utility maximization

You wish to earn a return of 10% on each of two stocks, C and D. Each of the stocks is

expected to pay a dividend of $2 in the upcoming year. The expected growth rate of

dividends is 9% for stock C and 10% for stock D. The intrinsic value of stock C

A. will be greater than the intrinsic value of stock D.

B. will be the same as the intrinsic value of stock D.

C. will be less than the intrinsic value of stock D.

D. will be the same or greater than the intrinsic value of stock D.

E. None of the options are correct.

Systematic risk is also referred to as

A. market risk or nondiversifiable risk.

B. market risk or diversifiable risk.

C. unique risk or nondiversifiable risk.

D. unique risk or diversifiable risk.

E. None of the options are correct.

Suppose that Chicken Express, InC. has an ROA of 7% and pays a 6% coupon on its

debt. Chicken Express has a capital structure that is 70% equity and 30% debt. Relative

to a firm that is 100% equity-financed, Chicken Express’s net profit will be ________,

and its ROE will be ________.

A. lower; lower

B. higher; higher

C. higher; lower

D. lower; higher

E. It is impossible to predict.

Suppose the 1-year risk-free rate of return in the U.S. is 6%. The current exchange rate

is 1 pound = U.S. $1.62. The 1-year forward rate is 1 pound = $1.53. What is the

minimum yield on a 1-year risk-free security in Britain that would induce a U.S.

investor to invest in the British security?

A. 15.44%

B. 13.50%

C. 12.24%

D. 7.62%

E. None of the options

If an investment provides a 1.25% return quarterly, its effective annual rate is

A. 5.23%.

B. 5.09%.

C. 4.02%.

D. 4.04%.

A year ago, you invested $10,000 in a savings account that pays an annual interest rate

of 5%. What is your

approximate annual real rate of return if the rate of inflation was 3.5% over the year?

A. 1.5%

B. 10%

C. 7%

D. 3%

E. None of the options are correct.

A mutual fund had year-end assets of $560,000,000 and liabilities of $26,000,000.

There were 23,850,000 shares in the fund at year end. What was the mutual fund’s net

asset value?

A. $22.87

B. $22.39

C. $22.24

D. $17.61

E. $19.25

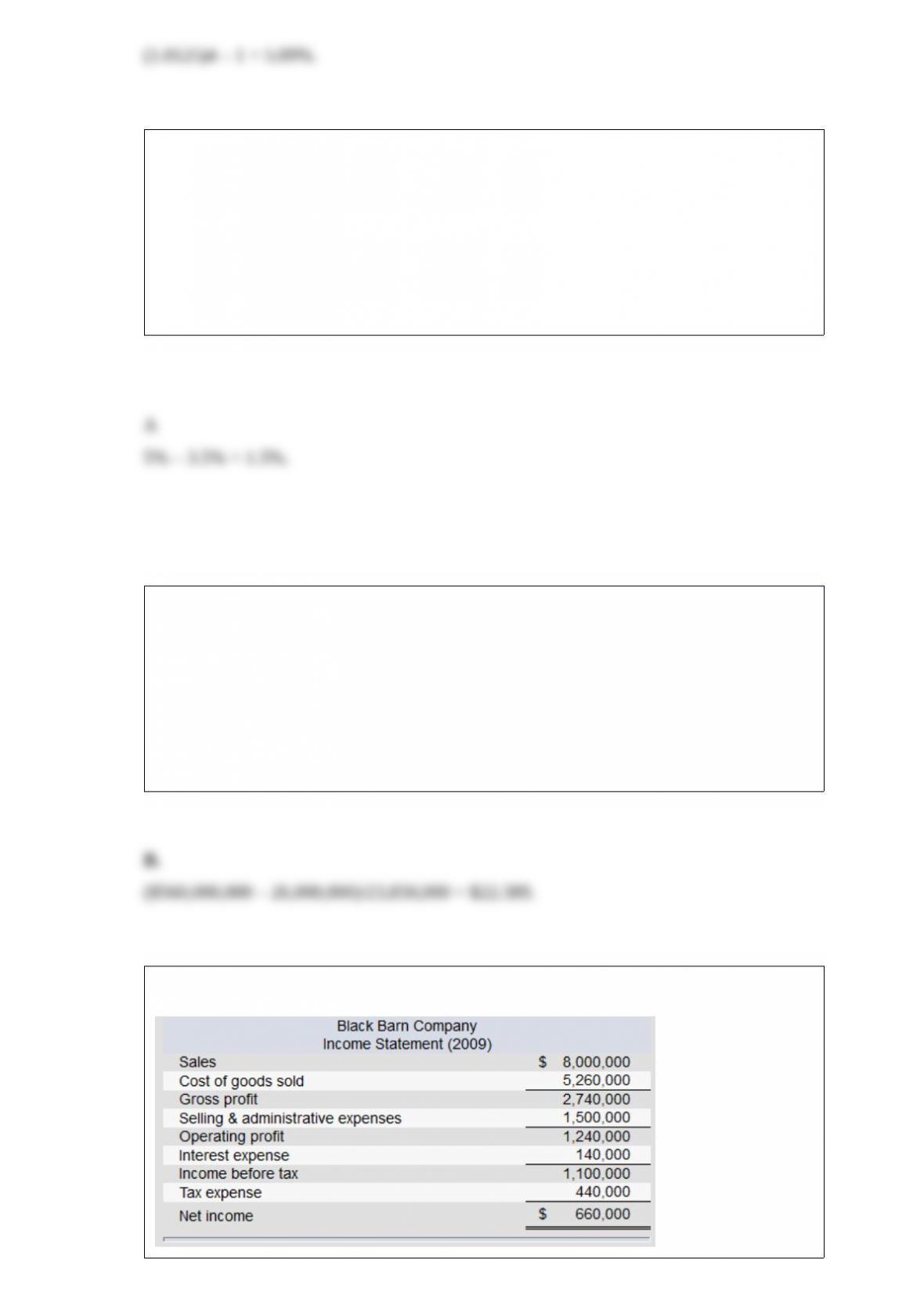

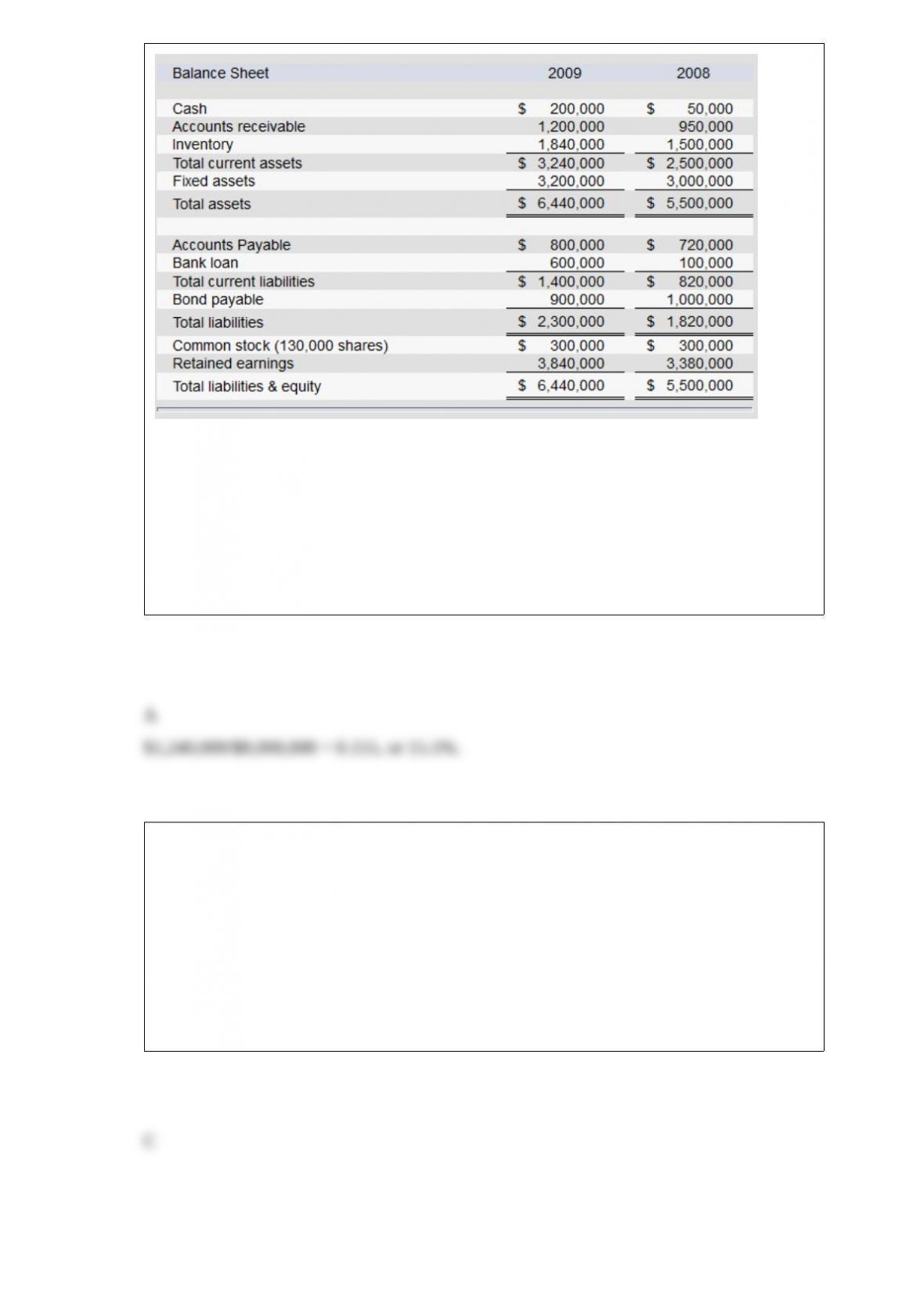

The financial statements of Black Barn Company are given below.

Note: The common shares are trading in the stock market for $40 each.

Refer to the financial statements of Black Barn Company. The firm’s return on sales

ratio for 2009 is

A. 15.5%.

B. 14.6%.

C. 14.0%.

D. 15.0%.

E. 16.5%.

JCPenney Company is expected to pay a dividend in year 1 of $1.65, a dividend in year

2 of $1.97, and a dividend in year 3 of $2.54. After year 3, dividends are expected to

grow at the rate of 8% per year. An appropriate required return for the stock is 11%. The

stock should be worth _______ today.

A. $33.00

B. $40.67

C. $71.80

D. $66.00

E. None of the options are correct.

Which of the following statement(s) is(are) true regarding the variance of a portfolio of

two risky securities?

I) The higher the coefficient of correlation between securities, the greater the reduction

in the portfolio variance.

II) There is a linear relationship between the securities’ coefficient of correlation and the

portfolio variance.

III) The degree to which the portfolio variance is reduced depends on the degree of

correlation between

securities.

A. I only

B. II only

C. III only

D. I and II

E. I and III

Targetdate retirement funds are not

A. inappropriate for most investors.

B. very high in fees.

C. designed to function much like hedge funds.

D. inappropriate for most investors or very high in fees.

E. All of the options are correct.

A bet on particular mispricing across two or more securities with extraneous sources of

risk, such as general market exposure hedged away, is a

A. pure play.

B. relative play.

C. long shot.

D. sure thing.

E. relative play and sure thing.

In 2016, ____________ was the most significant financial asset of U.S. households in

terms of total value.

A. real estate

B. mutual fund shares

C. debt securities

D. life insurance reserves

E. pension reserves

Duration measures

A. weighted-average time until a bond’s half-life.

B. weighted-average time until cash flow payment.

C. the time required to make excessive profit from the investment.

D. weighted-average time until a bond’s half-life and the time required to make

excessive profit from the investment.

E. weighted-average time until cash flow payment and the time required to make

excessive profit from the

investment.

__________ is a report of the cash flow generated by the firm’s operations, investments,

and financial activities.

A. The balance sheet

B. The income statement

C. The statement of cash flows

D. The auditor’s statement of financial condition

E. None of the options are correct.

NASDAQ subscriber levels

A. permit those with the highest level, 3, to “make a market” in the security.

B. permit those with a level 2 subscription to receive all bid and ask quotes but not to

enter their own quotes.

C. permit level 1 subscribers to receive general information about prices.

D. include all OTC stocks.

E. permit those with the highest level, 3, to “make a market” in the security; permit

those with a level 2 subscription to receive all bid and ask quotes but not to enter their

own quotes; and permit level 1 subscribers to receive general information about prices.

Certificates of deposit are insured for up to ____________ in the event of bank

insolvency.

A. $10,000

B. $100,000

C. $250,000

D. $500,000

An example of ________ is that it is not as painful to have purchased a blue chip stock

that decreases in value as it is to lose money on an unknown start up firm.

A. mental accounting

B. regret avoidance

C. overconfidence

D. conservatism

Given an optimal risky portfolio with expected return of 12%, standard deviation of

26%, and a risk free rate of

5%, what is the slope of the best feasible CAL?

A. 0.64

B. 0.27

C. 0.08

D. 0.33

E. 0.36

In the event of the firm’s bankruptcy,

A. the most shareholders can lose is their original investment in the firm’s stock.

B. common shareholders are the first in line to receive their claims on the firm’s assets.

C. bondholders have claim to what is left from the liquidation of the firm’s assets after

paying the shareholders.

D. the claims of preferred shareholders are honored before those of the common

shareholders.

E.the most shareholders can lose is their original investment in the firm’s stock and the

claims of preferred shareholders are honored before those of the common shareholders.

A put option on a stock is said to be in the money if

A.the exercise price is higher than the stock price.

B. the exercise price is less than the stock price.

C. the exercise price is equal to the stock price.

D. the price of the put is higher than the price of the call.

E. the price of the call is higher than the price of the put.

Holding other factors constant, the interest-rate risk of a coupon bond is higher when

the bond’s

A. term to maturity is lower.

B. coupon rate is lower.

C. yield to maturity is higher.

D. term to maturity is lower and yield to maturity is higher.

E. None of the options are correct.

You purchased 1000 shares of CSCO common stock on margin at $19 per share.

Assume the initial margin is 50%, and the maintenance margin is 30%. Below what

stock price level would you get a margin call? Assume the stock pays no dividend;

ignore interest on margin.

A. $12.86

B. $15.75

C. $19.67

D. $13.57

If a 7% coupon bond that pays interest every 182 days paid interest 32 days ago, the

accrued interest would be

A. $5.67.

B. $7.35.

C. $6.35.

D. $6.15.

E. $7.12.

When stocks are held in street name,

A. the investor receives a stock certificate with the owner’s street address.

B. the investor receives a stock certificate without the owner’s street address.

C. the investor does not receive a stock certificate.

D. the broker holds the stock in the brokerage firm’s name on behalf of the client.

E. the investor does not receive a stock certificate, and the broker holds the stock in the

brokerage firm’s name on behalf of the client.

Empirical tests of the Black-Scholes option pricing model

A. show that the model generates values fairly close to the prices at which options

trade.

B. show that the model tends to overvalue deep in-the-money calls and undervalue deep

out-of-the-money calls.

C. indicate that the mispricing that does occur is due to the possible early exercise of

American options on dividend-paying stocks.

D. show that the model generates values fairly close to the prices at which options trade

and indicate that the mispricing that does occur is due to the possible early exercise of

American options on dividend-paying stocks.

E. All of the options are correct.

A year ago, you invested $1,000 in a savings account that pays an annual interest rate of

6%. What is your

approximate annual real rate of return if the rate of inflation was 2% over the year?

A. 4%

B. 2%

C. 6%

D. 3%

A firm in the early stages of the industry life cycle will likely have

A. high market penetration.

B. high risk.

C. rapid growth.

D. high market penetration and rapid growth.

E.-high risk and rapid growth.