Two basic assumptions of technical analysis are that security prices adjust

A. rapidly to new information, and market prices are determined by the interaction of

supply and demand.

B. rapidly to new information, and liquidity is provided by security dealers.

C. gradually to new information, and market prices are determined by the interaction of

supply and demand.

D. gradually to new information, and liquidity is provided by security dealers.

E. rapidly to information and to the actions of insiders.

Other things equal, the price of a stock call option is positively correlated with the

following factors except

A. the stock price.

B. the time to expiration.

C. the stock volatility.

D. the exercise price.

__________ developed a popular method for risk-adjusted performance evaluation of

mutual funds.

A. Eugene Fama

B. Michael Jensen

C. William Sharpe

D. Jack Treynor

E. Michael Jensen, William Sharpe, and Jack Treynor

A preferred stock will pay a dividend of $3.00 in the upcoming year and every year

thereafter; i.e., dividends are not expected to grow. You require a return of 9% on this

stock. Use the constant growth DDM to calculate the intrinsic value of this preferred

stock.

A. $33.33

B. $0.27

C. $31.82

D. $56.25

An income beneficiary is

A. a stockbroker who remained working on Wall Street after the 1987 crash.

B. an employee of a trustee.

C. one who receives interest and dividend income from a trust during their lifetime.

D. one who receives the principal of a trust when it is dissolved.

E. None of the options are correct.

The manager of Quantitative International Fund uses EAFE as a benchmark. Last year’s

performance for the fund and the benchmark were as follows:

Calculate Quantitative’s currency selection return contribution.

A. +20%

B. 5%

C. +15%

D. +5%

E. 10%

The separation property refers to the conclusion that

A. the determination of the best risky portfolio is objective, and the choice of the best

complete portfolio is

subjective.

B. the choice of the best complete portfolio is objective, and the determination of the

best risky portfolio is

objective.

C. the choice of inputs to be used to determine the efficient frontier is objective, and the

choice of the best CAL

is subjective.

D. the determination of the best CAL is objective, and the choice of the inputs to be

used to determine the

efficient frontier is subjective.

E. investors are separate beings and will, therefore, have different preferences regarding

the risk-return

tradeoff.

The Treynor-Black model is a model that shows how an investment manager can use

security analysis and

statistics to construct

A. a market portfolio.

B. a passive portfolio.

C.an active portfolio.

D. an index portfolio.

E. a balanced portfolio.

A firm’s earnings per share increased from $10 to $12, dividends increased from $4.00

to $4.80, and the share price increased from $80 to $90. Given this information, it

follows that

A. the stock experienced a drop in the P/E ratio.

B. the firm had a decrease in dividend-payout ratio.

C. the firm increased the number of shares outstanding.

D. the required rate of return decreased.

A coupon bond pays annual interest, has a par value of $1,000, matures in four years,

has a coupon rate of 8.25%, and has a yield to maturity of 8.64%. The current yield on

this bond is

A. 8.65%.

B. 8.45%.

C. 7.95%.

D. 8.36%.

E. None of the options are correct.

The capital asset pricing model assumes

A. all investors are price takers.

B. all investors have the same holding period.

C. investors pay taxes on capital gains.

D. all investors are price takers and have the same holding period.

E. all investors are price takers, have the same holding period, and pay taxes on capital

gains.

A market decline of 23% on a day when there is no significant macroeconomic event

______ consistent with the EMH because ________.

A. would be; it was a clear response to macroeconomic news

B. would be; it was not a clear response to macroeconomic news

C. would not be; it was a clear response to macroeconomic news

D. would not be; it was not a clear response to macroeconomic news

The ____ index represents the performance of the Japanese stock market.

A. DAX

B. FTSE

C. Nikkei

D. Hang Seng

Fama and French (2002) studied the equity premium puzzle by breaking their sample

into subperiods and found that

A. the equity premium was largest throughout the entire 1872 1999 period.

B. the equity premium was largest during the 1872 1949 subperiod.

C. the equity premium was largest during the 1950 1999 subperiod.

D. the differences in equity premiums for the three time periods were statistically

insignificant.

E. the constant growth dividend discount model never works.

_______ are financial assets.

A. Bonds

B. Machines

C. Stocks

D. Bonds and stocks

E. Bonds, machines, and stocks

What would the yield to maturity be on a four-year zero-coupon bond purchased today?

A. 5.75%

B. 6.30%

C. 5.65%

D. 5.25%

A version of earnings management that became common in the 1990s was

A. when management made changes in the operations of the firm to ensure that

earnings did not increase or decrease too rapidly.

B. reported “pro forma earnings.”

C. when management made changes in the operations of the firm to ensure that earnings

did not increase too rapidly.

D. when management made changes in the operations of the firm to ensure that

earnings did not decrease too rapidly.

A manager who uses the mean-variance theory to construct an optimal portfolio will

satisfy

A. investors with low risk-aversion coefficients.

B. investors with high risk-aversion coefficients.

C. investors with moderate risk-aversion coefficients.

D.all investors regardless of their level of risk aversion.

E. only clients with whom she has established long-term relationships because she

knows their personal

Which of the following is not a source of systematic risk?

A. The business cycle

B. Interest rates

C. Personnel changes

D. The inflation rate

E. Exchange rates

The unsystematic risk of a specific security

A. is likely to be higher in an increasing market.

B. results from factors unique to the firm.

C. depends on market volatility.

D. cannot be diversified away.

The longest time horizons are likely to be set by

A. banks.

B. property and casualty insurance companies.

C. endowment funds.

D. banks and endowment funds.

E. property and casualty insurance companies and endowment funds.

Benchmark risk

A. is inevitable and is never a significant issue in practice.

B. is inevitable and is always a significant issue in practice.

C. cannot be constrained to keep a Treynor-Black portfolio within reasonable weights.

D.can be constrained to keep a Treynor-Black portfolio within reasonable weights.

A mutual fund had year-end assets of $327,000,000 and liabilities of $46,000,000. If the

fund NAV was $30.48, how many shares must have been held in the fund?

A. 11,354,751

B. 8,412,642

C. 10,165,476

D. 9,165,414

E. 9,219,160

Which of the following factors were used by Fama and French in their multifactor

model?

A. Return on the market index

B. Excess return of small stocks over large stocks

C. Excess return of high book-to-market stocks over low book-to-market stocks

D. All of the factors were included in their model.

E. None of the factors were included in their model.

A security has an expected rate of return of 0.15 and a beta of 1.25. The market

expected rate of return is 0.10,

and the risk-free rate is 0.04. The alpha of the stock is

A. 1.7%.

B. –1.7%.

C. 8.3%.

D. 3.5%.

Suppose that you purchased a call option on the S&P 100 Index. The option has an

exercise price of 1,680, and the index is now at 1,720. What will happen when you

exercise the option?

A. You will have to pay $1,680.

B. You will receive $1,720.

C. You will receive $1,680.

D.You will receive $4,000.

E. You will have to pay $4,000.

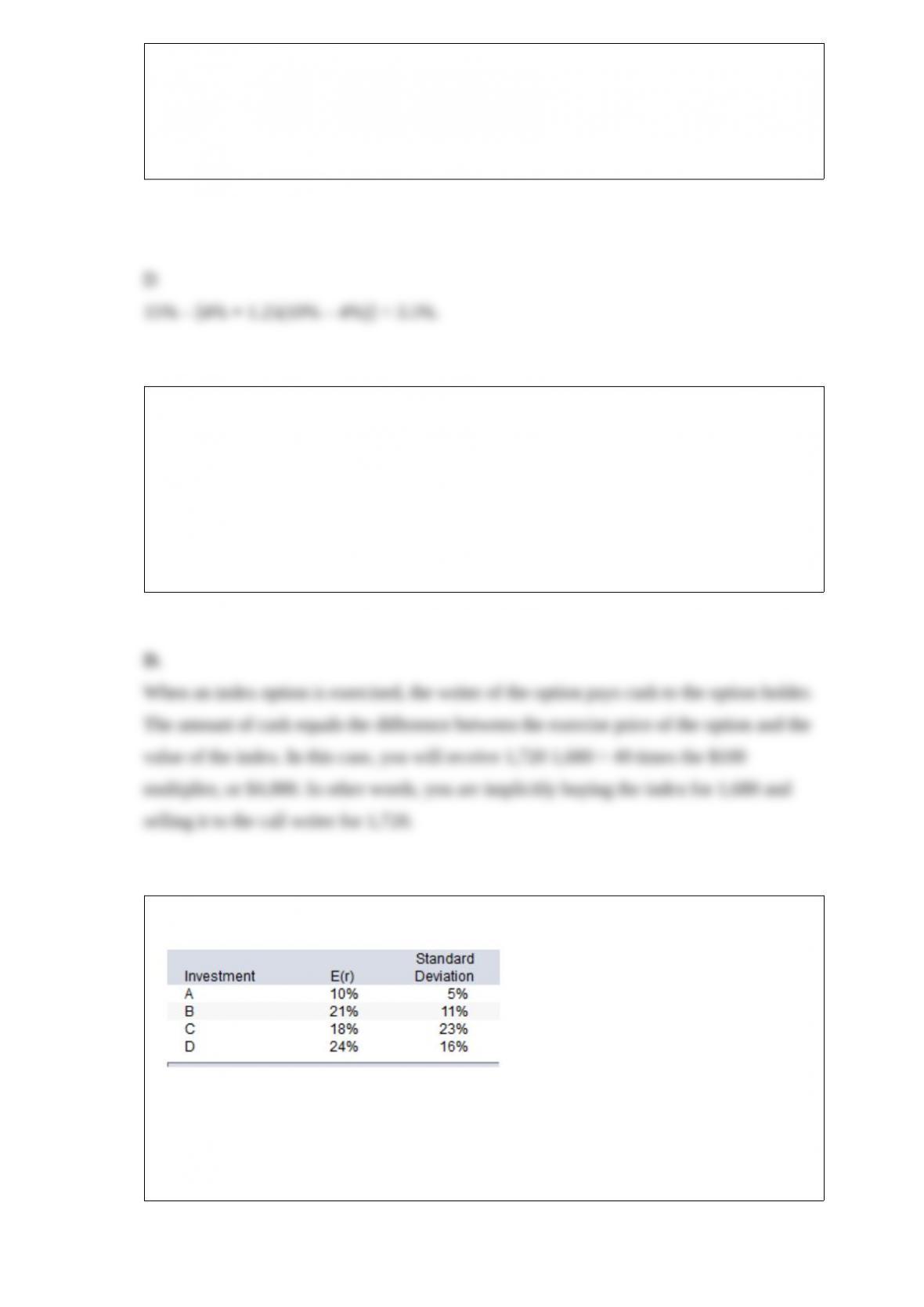

According to the mean-variance criterion, which of the statements below is correct?

A. Investment B dominates investment A.

B. Investment B dominates investment C.

C. Investment D dominates all of the other investments.

D. Investment D dominates only investment B.

E. Investment C dominates investment A.

The time value of a put option is

I) the difference between the option’s price and the value it would have if it were

expiring immediately.

II) the same as the present value of the option’s expected future cash flows.

III) the difference between the option’s price and its expected future value.

IV) different from the usual time value of money concept.

A. I

B. I and II

C. II and III

D. II

E. I and IV

According to the Capital Asset Pricing Model (CAPM), a well diversified portfolio’s

rate of return is a function

Of

A. beta risk.

B. unsystematic risk.

C. unique risk.

D. reinvestment risk.

E. None of the options are correct.

In the single-index model represented by the equation ri = E(ri) + βiF + ei, the term ei

represents

A. the impact of unanticipated macroeconomic events on security i’s return.

B. the impact of unanticipated firm-specific events on security i’s return.

C. the impact of anticipated macroeconomic events on security i’s return.

D. the impact of anticipated firm-specific events on security i’s return.

E. the impact of changes in the market on security i’s return.

Fama and French (1992) found that

A. firm size had better explanatory power than beta in describing portfolio returns.

B. beta had better explanatory power than firm size in describing portfolio returns.

C. beta had better explanatory power than book to market ratios in describing portfolio

returns.

D. macroeconomic factors had better explanatory power than beta in describing

portfolio returns.

E. None of the options are correct.

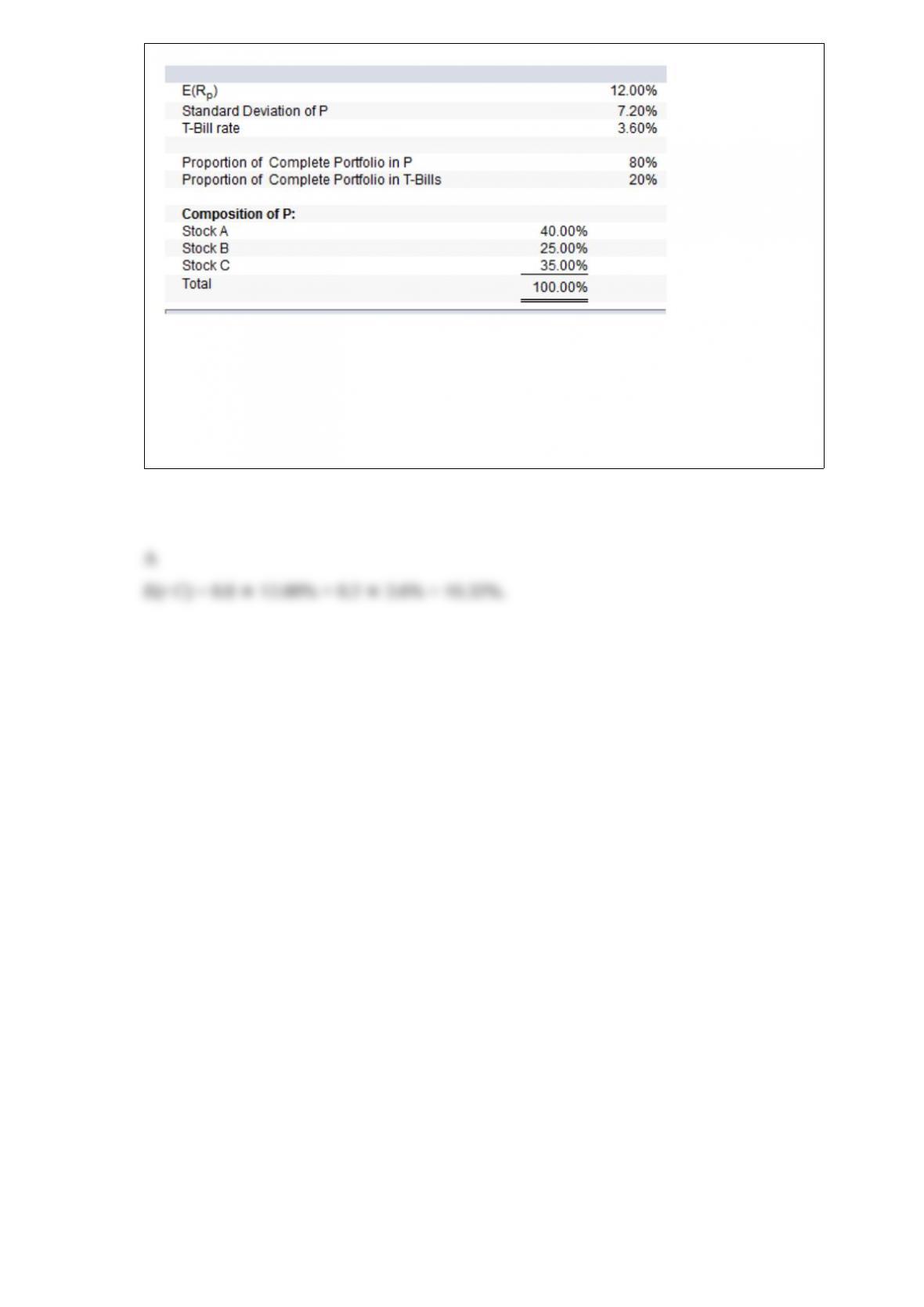

Your client, Bo Regard, holds a complete portfolio that consists of a portfolio of risky

assets (P) and T-Bills. The information below refers to these assets.

What is the expected return on Bo’s complete portfolio?

A. 10.32%

B. 5.28%

C. 9.62%

D. 8.44%

E. 7.58%