Which one of the following stock index futures has a multiplier of 50 Hong Kong

dollars times the index?

A. FTSE 100

B. Hang Seng

C. Nikkei

D. DAX-30

E. FTSE 100 and Hang Seng

The critical variable in the determination of the success of the active portfolio is

A. alpha/systematic risk.

B.alpha/nonsystematic risk.

C. gamma/systematic risk.

D. gamma/nonsystematic risk.

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 100 stocks in order to construct a mean-variance efficient

portfolio constrained by 100 investments. They will need to calculate _____________

expected returns and ___________ variances of returns.

A. 100; 100

B. 100; 4950

C. 4950; 100

D. 4950; 4950

What should the purchase price of a 2-year zero-coupon bond be if it is purchased at the

beginning of year 2 and has face value of $1,000?

A. $877.54

B. $888.33

C. $883.32

D. $893.36

E. $871.80

Analysts may use regression analysis to estimate the index model for a stock. When

doing so, the slope of the regression line is an estimate of

A. the α of the asset.

B. the β of the asset.

C. the σ of the asset.

D. the δ of the asset.

Rosenberg and Guy found that ___________ helped to predict firms’ betas.

A. debt/asset ratios

B. market capitalization

C. variance of earnings

D. all of the options

E. None of the options are correct.

Assume that stock market returns do not resemble a single-index structure. An

investment fund analyzes 125 stocks in order to construct a mean-variance efficient

portfolio constrained by 125 investments. They will need to calculate ____________

covariances.

A. 125

B. 7,750

C. 15,625

D. 11,750

The smallest component of the money market is

A. repurchase agreements.

B. small-denomination time deposits.

C. savings deposits.

D. money market mutual funds.

E. commercial paper.

Consider two perfectly negatively correlated risky securities A and B. A has an expected

rate of return of 12%

and a standard deviation of 17%. B has an expected rate of return of 9% and a standard

deviation of 14%.

The weights of A and B in the global minimum variance portfolio are _____ and _____,

respectively.

A. 0.24; 0.76

B. 0.50; 0.50

C. 0.57; 0.43

D. 0.45; 0.55

E. 0.76; 0.24

A declining GDP indicates a(n) ______ economy with ______ opportunity for a firm to

increase sales.

A.-stagnant; little

B. stagnant; ample

C. expanding; little

D. expanding; ample

E. stable; no

Portfolio A consists of 400 shares of stock and 400 calls on that stock. Portfolio B

consists of 500 shares of stock. The call delta is 0.5. Which portfolio has a higher dollar

exposure to a change in stock price?

A. Portfolio B

B. Portfolio A

C. The two portfolios have the same exposure.

D. Portfolio A if the stock price increases and portfolio B if it decreases

E. Portfolio B if the stock price increases and portfolio A if it decreases

The scope and purpose section of an Investment Policy Statement for individual

investors typically consists of defining the

A. return, distribution, and risk requirements.

B. process for review of the IPS.

C. appropriate metrics for risk measurement.

D. relevant constraints.

E. context, investor, and structure.

The invoice price of a bond that a buyer would pay is equal to

A. the asked price plus accrued interest.

B. the asked price less accrued interest.

C. the bid price plus accrued interest.

D. the bid price less accrued interest.

E. the bid price.

You are considering acquiring a common stock that you would like to hold for one year.

You expect to receive both $1.25 in dividends and $32 from the sale of the stock at the

end of the year. The maximum price you would pay for the stock today is _____ if you

wanted to earn a 10% return.

A. $30.23

B. $24.11

C. $26.52

D. $27.50

E. None of the options are correct.

As diversification increases, the standard deviation of a portfolio approaches

A. 0.

B. 1.

C. infinity.

D. the standard deviation of the market portfolio.

E. None of the options are correct.

If you believe in the _______ form of the EMH, you believe that stock prices only

reflect all information that can be derived by examining market trading data, such as the

history of past stock prices, trading volume or short interest.

A. semistrong

B. strong

C. weak

D. All of the options are correct.

E. None of the options are correct.

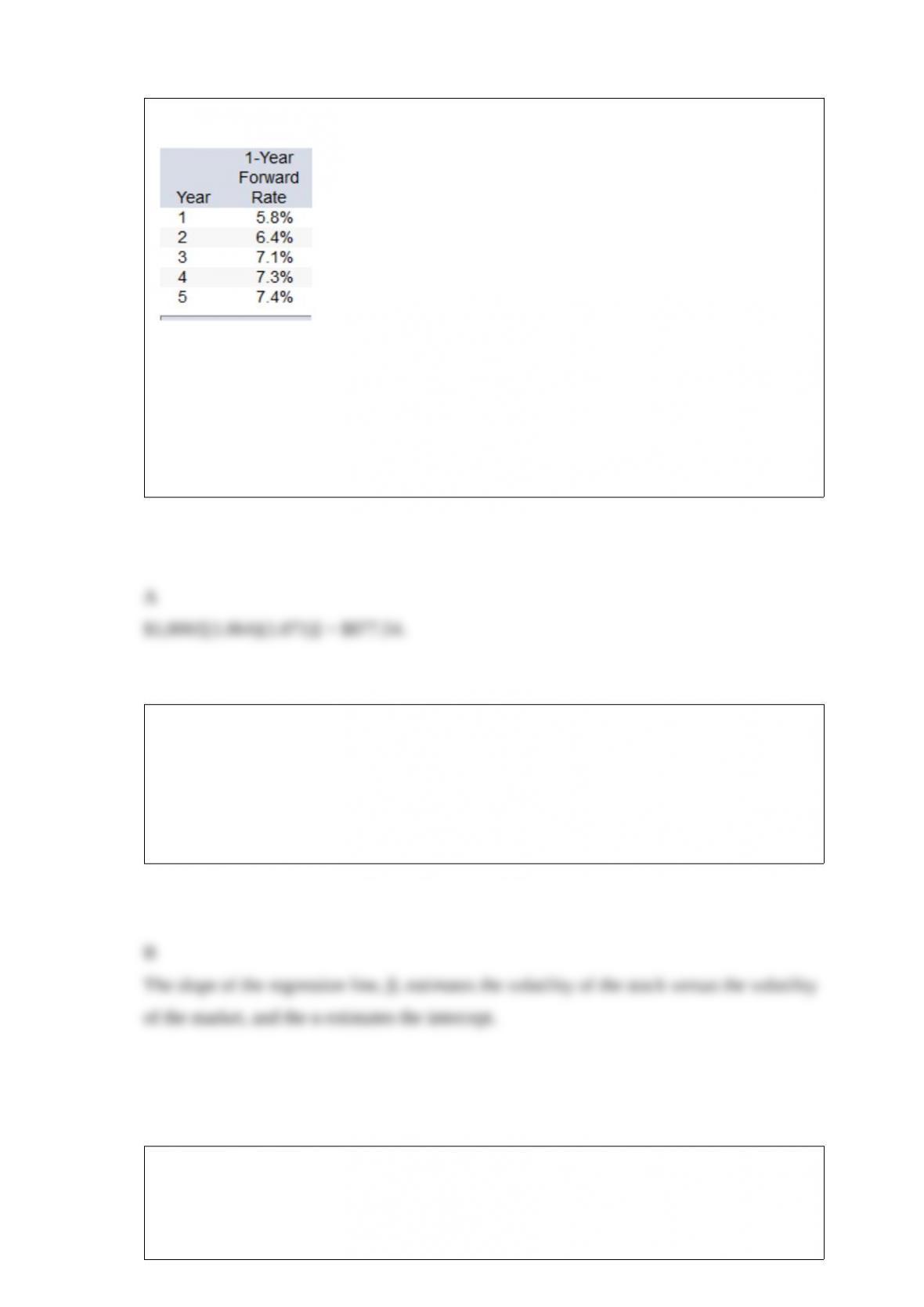

Consider the following:

What should be the proper futures price for a 1-year contract?

A. 1.703 A$/$

B. 1.654 A$/$

C. 1.638 A$/$

D. 1.778 A$/$

E. 1.686 A$/$

According to Michael Porter, there are five determinants of competition. An example of

_____ is when competitors seek to expand their share of the market.

A. threat of entry

B.-rivalry between existing competitors

C. pressure from substitute products

D. bargaining power of buyers

E. bargaining power of suppliers

Suppose you held a well-diversified portfolio with a very large number of securities,

and that the single index model holds. If the σ of your portfolio was 0.22 and σM was

0.19, the β of the portfolio would be approximately

A. 1.34.

B. 1.16.

C. 1.25.

D. 1.56.

Which of the following combinations will result in a sharply-increasing yield curve?

A. Increasing future expected short rates and increasing liquidity premiums

B. Decreasing future expected short rates and increasing liquidity premiums

C. Increasing future expected short rates and decreasing liquidity premiums

D. Increasing future expected short rates and constant liquidity premiums

E. Constant future expected short rates and increasing liquidity premiums

Goodie Corporation produces goods that are very mature in their product life cycles.

Goodie Corporation is expected to have per share FCFE in year 1 of $2.00, per share

FCFE of $1.50 in year 2, and per share FCFE of $1.00 in year 3. After year 3, per share

FCFE is expected to decline at a rate of 1% per year. An appropriate required rate of

return for the stock is 10%. The stock should be worth __________ today.

A. $9.00

B. $101.57

C. $10.57

D. $22.22

E. $47.23

The amount that an investor allocates to the market portfolio is negatively related to

I) the expected return on the market portfolio.

II) the investor’s risk aversion coefficient.

III) the risk-free rate of return.

IV) the variance of the market portfolio.

A. I and II.

B. II and III.

C. II and IV.

D. II, III, and IV.

E. I, III, and IV.

The type of municipal bond that is used to finance commercial enterprises, such as the

construction of a new building for a corporation, is called

A. a corporate courtesy bond.

B. a revenue bond.

C. a general-obligation bond.

D. a tax-anticipation note.

E. an industrial-development bond.

Treasury bills are commonly viewed as risk-free assets because

A. their short-term nature makes their values insensitive to interest rate fluctuations.

B. the inflation uncertainty over their time to maturity is negligible.

C. their term to maturity is identical to most investors’ desired holding periods.

D. their short-term nature makes their values insensitive to interest rate fluctuations,

and the inflation

uncertainty over their time to maturity is negligible.

E. the inflation uncertainty over their time to maturity is negligible, and their term to

maturity is identical to most

investors’ desired holding periods.

If a stock index futures contract is overpriced, you would exploit this situation by

A. selling both the stock index futures and the stocks in the index.

B. selling the stock index futures and simultaneously buying the stocks in the index.

C. buying both the stock index futures and the stocks in the index.

D. buying the stock index futures and selling the stocks in the index.

E. None of the options are correct.

The beta of a stock has been estimated as 1.8 using regression analysis on a sample of

historical returns. A commonly-used adjustment technique would provide an adjusted

beta of

A. 1.20.

B. 1.53.

C. 1.13.

D. 1.0.

You have been given this probability distribution for the holding-period return for

Cheese, Inc. stock:

Assuming that the expected return on Cheese’s stock is 14.35%, what is the standard

deviation of these

returns?

A. 4.72%

B. 6.30%

C. 4.38%

D. 5.74%

E. None of the options are correct.

Ideally, clients would like to invest with the portfolio manager who has

A. a moderate personal risk-aversion coefficient.

B. a low personal risk-aversion coefficient.

C.the highest Sharpe measure.

D. the highest record of realized returns.

E. the lowest record of standard deviations.

Consider a risky portfolio, A, with an expected rate of return of 0.15 and a standard

deviation of 0.15, that lies

on a given indifference curve. Which one of the following portfolios might lie on the

same indifference curve for

a risk averse investor?

A. E(r) = 0.15; Standard deviation = 0.20

B. E(r) = 0.15; Standard deviation = 0.10

C. E(r) = 0.10; Standard deviation = 0.10

D. E(r) = 0.20; Standard deviation = 0.15

E. E(r) = 0.10; Standard deviation = 0.20

The emerging stock market exhibiting the highest local currency return in 2015 was

A.-Russia

B. China.

C. Singapore.

D. Mexico.

E. Brazil.

What is the relationship between the price of a straight bond and the price of a callable

bond?

A. The straight bond’s price will be higher than the callable bond’s price for low interest

rates.

B. The straight bond’s price will be lower than the callable bond’s price for low interest

rates.

C. The straight bond’s price will change as interest rates change, but the callable bond’s

price will stay the same.

D. The straight bond and the callable bond will have the same price.

E. There is no consistent relationship between the two types of bonds.