In the banking environment, economic and legal firewalls often have been designed to

separate the risks of investment bank affiliate activities from commercial banks.

Answer:

The three government agencies that sponsor the creation of mortgage-backed, pass

through securities are: GNMA, FNMA, and FDIC.

Answer:

The deficit realized by the PBGC in 1992 was a result of risk-taking by fund

administrators.

Answer:

All call options are eventually exercised and the underlying asset must be delivered.

Answer:

If a trader in charge of an investment portfolio of an FI generates returns that are higher

than other traders at the FI, she should be rewarded with higher compensation.

Answer:

Passbook savings accounts are less liquid than demand deposit accounts.

Answer:

Portfolio risk can be reduced through diversification only if the returns of the loans in

the portfolio are negatively correlated.

Answer:

Trading activity and investor confidence in foreign debt increased in the early 2000s.

Answer:

The rate of change in duration values is less than the rate of change in maturity.

Answer:

Currently the reserve maintenance period begins 30 days after the end of the reserve

computation period.

Answer:

Savers increasingly favor investments that closely imitate diversified investments in the

direct securities markets over the transformed financial claims offered by traditional

FIs.

Answer:

The risk that the sale price of an asset will be less than the purchase price of an asset is

called liquidity risk.

Answer:

The credit union industry avoided much of the financial distress of the 1980s because of

the short maturity and relatively lower credit risk of their assets.

Answer:

The National Securities Markets Improvement Act of 1996 exempts mutual funds from

oversight by state securities regulators and reduced their regulatory burden.

Answer:

Historically, regulations have encouraged the expansion of bank offices domestically.

Answer:

Losses among FIs that actively traded mortgage-backed securities reached over $3

trillion world-wide by mid-2009.

Answer:

The reason an FI receives a fee when purchasing foreign currencies to allow customers

to complete international transactions is because the FI assumes some FX risk.

Answer:

Offices of foreign banks may be examined by the Federal Reserve under the FBSEA of

1991.

Answer:

Duration is related to maturity in a nonlinear manner through the current yield to

maturity of the asset.

Answer:

Property-casualty underwriting risk only exists when the premiums generated on a

given insurance line are less than the claims (losses) on the line.

Answer:

In the U.S., banks can hold cash and government securities to meet reserve

requirements.

Answer:

The minimum average daily reserves required in a maintenance period is a percentage

of the daily average demand deposits held by a bank during the computation period.

Answer:

The mortality rate is the past default experience of all loans, regardless of quality.

Answer:

Daylight overdraft risk occurs because banks often provide immediate credit to

customers for deposits, even though the funds may not arrive until later in the day.

Answer:

Hedging selectively only a portion of the balance sheet is an attempt to increase the

return of the FI by accepting some level of interest rate risk.

Answer:

The reserve computation period for determining required reserves covers the 14 days of

a two-week period that runs from Monday to Monday.

Answer:

Pricing deposit insurance premiums to reflect increases in risk-taking by financial

institutions is one method to reduce incentives to take risks.

Answer:

Deposits with low withdrawal risk typically are the lowest cost deposits for a DI.

Answer:

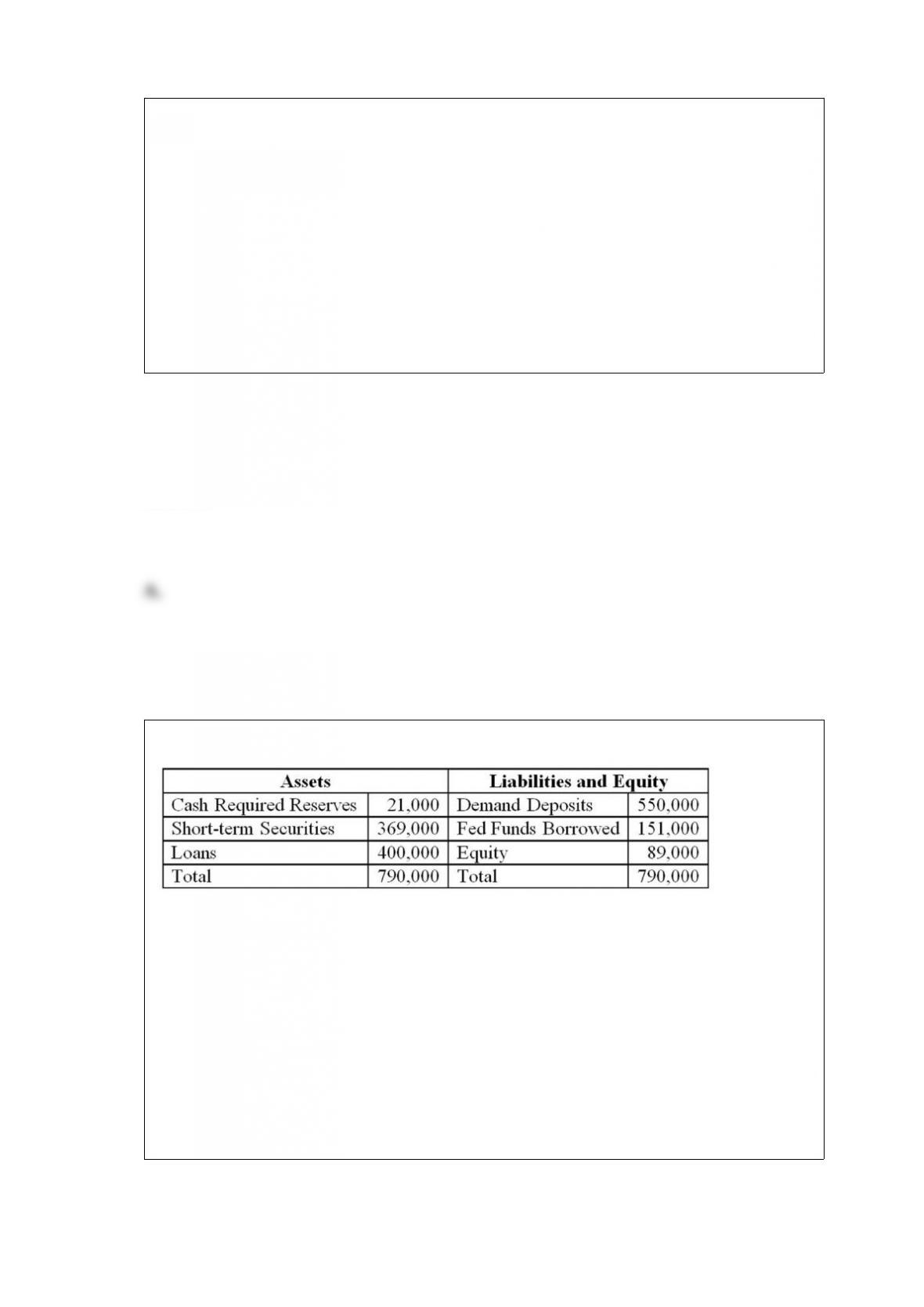

If the FI bought call options on bonds with a face value of $50 million, what is the

minimum amount of the stockholder’s potential TRUE net worth?A. $10 million.

B. $70 million.

C. $110 million.

D. $790 million.

E. $850 million.

Answer:

In exchange for the loss of some present value of the interest and principal on a loan

after a rescheduling, the lender avoids the permanent loss that would result from a

default.

Answer:

How would you characterize the FI’s risk exposure to fluctuations in the yen/dollar

exchange rate? A. The FI is net short in the yen and therefore faces the risk that the yen

will rise in value against the U.S. dollar.

B. The FI is net short in the yen and therefore faces the risk that the yen will fall in

value against the U.S. dollar.

C. The FI is net long in the yen and therefore faces the risk that the yen will fall in

value against the U.S. dollar.

D. The FI is net long in the yen and therefore faces the risk that the yen will rise in

value against the U.S. dollar.

E. The FI has a balanced position in the Japanese yen.

Answer:

Which of the following is NOT a source of foreign exchange risk? A. Trading foreign

currencies.

B. Making domestic-currency loans to foreign corporations.

C. Buying foreign-issued securities.

D. Issuing foreign currency-denominated debt.

E. Making foreign currency loans.

Answer:

Regulatory forbearance refers to a policy of A. allowing insolvent banks to continue to

operate.

B. foreclosing real estate properties in the event on non-payments of mortgages.

C. strict regulation of banks, closing them down as soon as they are insolvent.

D. rescheduling of all loans of a client in the event of non-payment.

E. Answers B and C only.

Answer:

Investment companies are successful in attracting business away from banks and

insurance companies primarily because they A. guarantee higher rates of return on

savers’ funds.

B. remove interest rate risk for the saver.

C. have no liquidity risk.

D. give savers cheaper access to the direct securities markets.

E. offer lower loan rates.

Answer:

The cumulative probability of repayment of BBB corporate debt over the next two

years isA. 99.84 percent.

B. 92.10 percent.

C. 4.45 percent.

D. 95.70 percent.

E. 7.90 percent.

Answer:

Which of the following is not a category of capital under Basel III? A. Tier III capital.

B. Tier II capital.

C. Common Equity Tier I.

D. Total risk-based capital.

E. Tier I capital.

Answer:

For reserve calculation purposes, the period that begins on a Thursday and ends on a

Wednesday 14 days later is known as A. the reserve maintenance period.

B. the reserve adjustment period.

C. the reserve computation period.

D. the contemporaneous accounting period.

E. None of the above.

Answer:

Standby letters of credit are classified as A. on-balance-sheet assets.

B. off-balance-sheet assets.

C. off-balance-sheet liabilities.

D. on-balance-sheet liabilities.

E. equity capital.

Answer:

What was the objective of the FDIC Improvement Act (FDICIA) of 1991? A.

Returning the banking industry to record profit levels.

B. Restructure the savings association deposit insurance fund and transfer its

management to FDIC.

C. To deny deposit insurance coverage to funds obtained through deposit brokers.

D. To restructure the bank deposit insurance fund and prevent its potential insolvency.

E. To enforce the capital standards on insured depository institutions.

Answer:

By late 2012, the number of commercial banks in the U.S. was approximately A. 2,200.

B. 4,680.

C. 6,170.

D. 8,100.

E. 12,700.

Answer:

Which of the following did NOT occur in the life insurance industry during the most

recent financial crisis? A. Low equity values reduced asset-based fees on separate

account assets.

B. Losses were incurred on holdings of commercial mortgage-backed securities and

commercial loans.

C. Asset-based fees declined on products such as variable annuities and pension fund

assets that were tied to equity returns.

D. Low interest rates and harsh economic conditions caused many policyholders to

terminate or surrender their policies.

E. Historically low interest rates caused increased demand for whole life policies.

Answer:

Insurance policy benefits are classified on an insurance company’s balance sheet as A.

liabilities, because the insurance company may have to pay out the benefits.

B. assets, because policy benefits are valuable to the company.

C. liabilities, because customers may fall behind on their premium payments.

D. assets, because policy benefits are fully covered by premium payments.

E. liabilities, because insurance companies must maintain a capital base to cover the

payments of benefits.

Answer:

Which of the following methods measure loan concentration risk by tracking credit

ratings of firms in particular sectors or ratings class for unusual downgrades? A.

Migration analysis.

B. Concentration limits.

C. Loan loss ratio-based model.

D. Moody’s Analytics portfolio manager model.

E. Loan volume-based model.

Answer:

If the bank’s expected net deposit drain is +4 percent, what is the bank’s expected

liquidity requirement? A. $7,560.

B. $6,040.

C. $16,000.

D. $22,000.

E. $14,760.

Answer:

Which of the following insurance products protects a lender against a borrower’s death

prior to repayment of the debt?A. Credit life.

B. Universal life.

C. Whole life.

D. Endowment life.

E. Variable life.

Answer:

The establishment of a global or international presence by an FI can be achieved in all

but which of the following ways? A. Selling financial services from a domestic office

to a domestic customer who has commercial activities in a foreign country.

B. Selling financial services to a foreign customer through subsidiary companies in a

foreign country.

C. Selling financial services through a branch, agency, or representative office.

D. Selling financial services from domestic offices to foreign customers.

E. Two of the above do not qualify an FI as achieving an international presence.

Answer:

Identify a major reason behind the increase in domestic underwriting activity during the

1990s. A. Enhanced non-trading profits.

B. High long-term interest rates.

C. Low long-term dividend rates.

D. Growth in the asset-backed securities market.

E. Decreased securitization of debt.

Answer:

The risk that many borrowers in a particular country fail to repay their loans as a result

of a recession in that country relates to A. credit risk.

B. sovereign risk.

C. currency risk.

D. liquidity risk.

E. interest rate risk.

Answer:

As of 20, the amount of mortgage-backed securities outstanding was approximately A.

$2.9 trillion.

B. $5.1 trillion.

C. $7.9 trillion.

D. $11.0 trillion.

E. $15.0 trillion.

Answer:

Losses in asset values due to adverse changes in interest rates are borne initially by the

A. equity holders of an FI.

B. liability holders of an FI.

C. regulatory authorities.

D. taxpayers.

E. insured depositors.

Answer:

What is the end of year profit or loss on the bank’s cash position if in one year both

Canadian bond rates increase to 7.538 percent and the exchange rate falls to US $0.765

per Canadian dollar? (Assume no change in U.S. interest rates.) A. Loss of US

$12,000.

B. Loss of US $75,000.

C. Profit of C $9,000.

D. Profit of US $50,000.

E. Loss of C $119,800.

Answer:

The McCarran-Ferguson Act of 1945 A. separated commercial banking from insurance

activities.

B. mandated federal insurance company charters.

C. stipulated that insurance companies are to be regulated at the state level.

D. initiated a national insurance guaranty fund.

E. limited insurance company assets to low risk government securities.

Answer:

This is an accrual class of a CMO that makes a payment to bondholders only when

preceding CMO classes have been retired. A. Class A bonds.

B. Class B bonds.

C. Class C bonds.

D. Class Z bonds.

E. None of the above.

Answer:

Which of the following is an out-of-the-money counterparty? A. Counterparty in a loan

commitment contract.

B. FI that trades in securities prior to their actual issue.

C. Counterparty that is currently at an advantage in terms of cash flows.

D. FI that guarantees to underwrite the performance of the buyer of the guaranty.

E. Counterparty that is currently at a disadvantage in terms of cash flows.

Answer:

In terms of valuation, a 12-year interest rate swap can be can be considered in terms of

A. a series of option contracts.

B. a zero-coupon bond.

C. a U.S. Treasury STRIP.

D. bond-equivalent valuation.

E. securitization of a derivative contract.

Answer:

Assume 50 percent of the loan is drawn and that there are reserve requirements of 10

percent on demand deposits. What should the bank charge as back-end fees if they

require an expected return of 13.63 percent? Do not take future values of fees or interest

income received.A. 5 basis points.

B. 10 basis points.

C. 15 basis points.

D. 20 basis points.

E. 25 basis points.

Answer:

Choose among the following major banking laws.

A. The McFadden Act of 1927

B. The Glass-Steagall Act of 1933

C. The Depository Institutions Deregulation and Monetary Control Act (DIDMCA) of

1980

D. The Garn-St Germain Depository Institutions Act of 1982

E. The Competitive Equality in Banking Act of 1987

F. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989

G. The Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991

H. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994

I. Financial Services Modernization Act of 1999

This legislation replaced FSLIC with FDIC-SAIF.

Answer:

Why are passbook savings generally less liquid than demand deposits and NOW

accounts? A. They are noncheckable.

B. They usually involve physical presence at the institution for withdrawal.

C. The DI has the legal power to delay payment for as long as one month.

D. They tend to pay higher interest rates than demand deposits and NOW accounts.

E. All of the above.

Answer:

Why is the default risk much more serious for forward contracts than for futures

contracts? A. Because forward contracts are nonstandard contracts.

B. Forward contracts are entered into bilaterally by the negotiating parties.

C. For forwards, all cash flows are required to be paid at one time on contract maturity.

D. Forwards are essentially OTC arrangements with no external guarantees in case of

default.

E. All of the above.

Answer:

Rediscounted bankers’ acceptances are classified as A. on-balance-sheet assets.

B. off-balance-sheet assets.

C. off-balance-sheet liabilities.

D. on-balance-sheet liabilities.

E. equity capital.

Answer:

Millon National Bank has 10 million British pounds (£) in one-year assets and £8

million in one-year liabilities. In addition, it has one-year liabilities of 4 million euros

(€). Assets are earning 8 percent and both liabilities are being paid at a rate of 8 percent.

All interest and principal will be paid at the end of the year.

What is the net interest income in dollars if the spot prices at the end of the year are

$1.50/£ and €1.65/$? A. $46,060.61.

B. $320,000.

C. $1,200,000.

D. $266,666.67.

E. $720,000.

Answer:

When the U.S. dollar declines against European currencies, it is A. potentially harmful

for European banks only.

B. potentially harmful for U.S. banks only.

C. potentially harmful for those banks that have financed U.S. dollar assets with

liabilities denominated in European currencies.

D. potentially harmful for those banks that have financed European currency assets

with U.S. dollar liabilities.

E. irrelevant for global banks.

Answer:

What is the market share of Bank 1? A. 12.5 percent.

B. 37.5 percent.

C. 25.0 percent.

D. 62.5 percent.

E. 50.0 percent.

Answer: