Recent evidence strongly suggests that economies of scope exist for both asset and

liability products, but not for off-balance-sheet products.

Answer:

Calculating the risk of a multi-asset trading portfolio requires the consideration of the

correlations of returns between the different assets.

Answer:

As compared to venture capital firms, private equity firms specialize in assisting

existing companies that have proven themselves in their industry.

Answer:

The total premium cost to an FI of hedging by buying put options is the price of each

put option times the number of put options purchased.

Answer:

Under FDICIA, the ability for regulators to show forbearance is limited by a set of

mandatory actions for each level of capital that an FI achieved.

Answer:

Although cloud computing is a technology that FIs can provide to business clients, the

FI itself seldom uses cloud computing in their own operations.

Answer:

Adjustable rate mortgages have interest rates that adjust periodically according to the

movement in some index.

Answer:

The securitization of mortgages involves the pooling of mortgage loans for sale in the

financial markets.

Answer:

In order to achieve a more stable revenue stream in a merger, the asset and liability

portfolios of the two institutions should have similar credit, interest rate, and liquidity

characteristics.

Answer:

CBOT catastrophe call spread options have variable payoffs that are capped at a level of

less than 100 percent of extreme losses.

Answer:

All tranches in a collateralized mortgage obligation (CMO) have the same prepayment

risk exposure.

Answer:

GNMA pass-throughs can assist an FI in resolving duration mismatch and illiquidity

risk problems.

Answer:

The current market value of an off-balance-sheet item is determined by finding the

current market value of the underlying item.

Answer:

Broker-dealers make very few adjustments to the book value net worth to reach an

approximate market value net worth.

Answer:

The notational value of swaps that are held by commercial banks as of 2012 was over

$130 trillion.

Answer:

FIs typically are concerned about the value at risk of their trading portfolios.

Answer:

As of 2012, Commercial banks are not allowed to own or invest in mutual funds.

Answer:

When a Special Purpose Vehicle (SPV) creates asset-backed securities, the SPV retains

ownership of the original assets.

Answer:

Fedwire is a wire transfer network operated through the Federal Reserve System to

assist banks in making financial transactions among themselves, on behalf of

themselves and customers.

Answer:

The DI manager can change the pricing on NOW accounts by changing both implicit

and explicit interest payments.

Answer:

A problem exists with the net stable funds ratio (NSFR) in that it does not include

off-balance-sheet activities.

Answer:

The Black-Scholes model does not work well to value bond options because of

violations of the underlying assumption of a constant variance of returns on the

underlying asset.

Answer:

Managing asset-side liquidity risk can involve either purchased liquidity management

or stored liquidity management.

Answer:

In a conventional interest rate swap agreement, the fixed-rate payer is attempting to

transform the variable-rate nature of its liabilities into fixed-rate liabilities.

Answer:

A lending decision to a firm in a foreign country should involve both a credit risk

analysis and a sovereign risk analysis.

Answer:

The risk-adjusted asset values of OBS market contracts or derivative instruments are

determined in a manner similar to the risk-adjusted asset values of contingent guarantee

claims.

Answer:

The front-end or back-end loads charged by some mutual funds often are combined

with 12b-1 fees.

Answer:

Swap transactions are homogeneous in nature so that the contracts can be easily traded

in the secondary market for swaps.

Answer:

The chief compliance officer of a mutual fund reports directly to the senior executives

of the fund management company.

Answer:

In the early 2000s the market risk capital requirement uniformly was a large proportion

of the total risk capital requirements for the largest US banks.

Answer:

The numbers provided are in millions of dollars and reflect market values:

What is

the weighted average duration of the liabilities of the FI?A. 5.00 years.

B. 5.35 years.

C. 5.70 years.

D. 6.05 years.

E. 6.40 years.

Answer:

Open-end mutual funds guarantee A. investors a minimum rate of return.

B. investors a minimum Net Asset Value (NAV).

C. to redeem investors’ shares upon demand at the daily Net Asset Value (NAV).

D. to earn the rate of return promised in the prospectus.

E. that there will be no load charges.

Answer:

What is the 10-day VAR of Sumitomo’s trading portfolio if the correlation among assets

is assumed to be -1.0?A. -$100,000.

B. -$316,228.

C. -$1,106,797.

D. -$1,204,161.

E. -$1,264,911.

Answer:

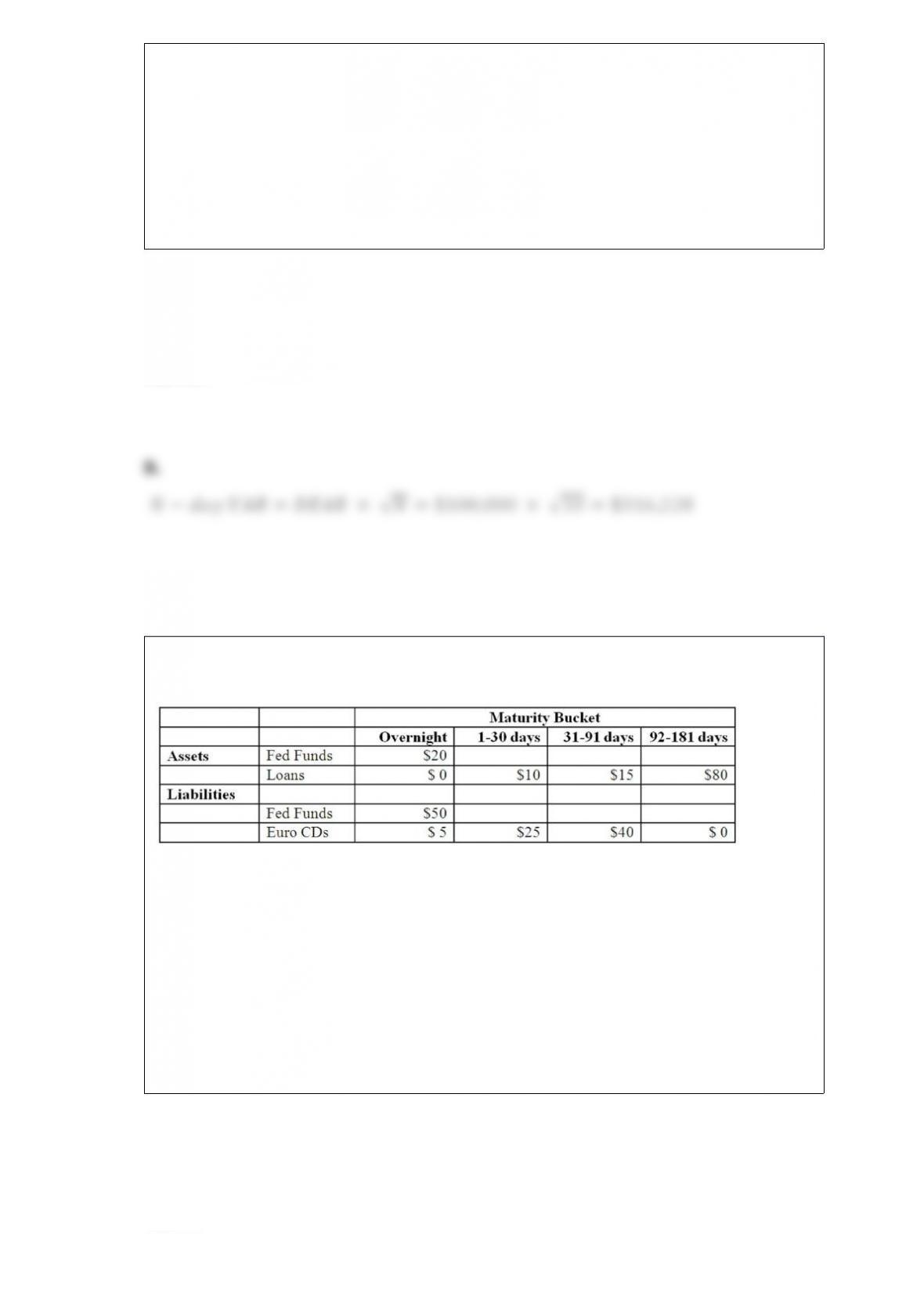

The following information details the current rate sensitivity report for Gotbucks Bank,

Inc. ($million).

How

will a decrease of 25 basis points in all interest rates affect Gotbuck’s net interest

income over a planning period of 91 days? A. +$0.1875 million.

B. +$0.1250 million.

C. -$0.1375 million.

D. +$0.0625 million.

E. 0

Answer:

Suppose that the doubling of a bank’s deposit funding allows the bank to triple its loan

output. What can you conclude about the bank’s production technology? A. It exhibits

economies of scale using the production approach.

B. It exhibits diseconomies of scale using the production approach.

C. It exhibits diseconomies of scale using the intermediation approach.

D. It exhibits economies of scale using the intermediation approach.

E. It exhibits neither economies nor diseconomies of scale.

Answer:

Credit Unions were generally less affected than other depository institutions by the

recent financial crisis becauseA. they had relatively more assets in consumer loans than

other DIs.

B. they had relatively more residential mortgages.

C. they hold more government and agency securities, on average.

D. they hold less government and agency securities, on average.

E. Answers A and C only.

Answer:

The process of providing custody and escrow services, clearance and settlement

services, and research and other advisory services by a securities firm involves the

function of A. mergers and acquisitions.

B. market making.

C. investment banking.

D. back-office functions.

E. cash management services.

Answer:

The DEAR of a bank’s trading portfolio has been estimated at $5,000. It is assumed that

the daily earnings are independently and normally distributed.

What is the 10-day VAR? A. $5,000.

B. $10,000.

C. $15,811.

D. $22,361.

E. $50,000.

Answer:

Market risk measurement considers the return-risk ratio of traders, which may allow a

more rational compensation system to be put in place. Thus market risk measurement

(MRM) aids in A. regulation.

B. resource allocation.

C. management information.

D. setting limits.

E. performance evaluation.

Answer:

What is the approximate yield on a 20-year 10 percent annual coupon LDC bond selling

at 75 cents on the dollar? (choose the closest answer) A. 10 percent.

B. 40 percent.

C. 14 percent.

D. 25 percent.

E. Cannot be determined.

Answer:

What is float? A. Overnight payments via CHIPS or Fedwire.

B. Encoding, endorsing, microfilming, and handling customers’ checks.

C. Time it takes a check to clear at a bank.

D. Management of multiple currency and security portfolios for trading and investment

purposes.

E. Interval between the dispatch of a bill and actual payment by the consumer.

Answer:

The following are protective mechanisms that have been developed by regulators to

promote the safety and soundness of the banking system EXCEPT A. encouraging

banks to rely more on deposits rather than debt or capital as a cushion against failure.

B. encouraging banks to limit lending to a single customer to no more than 10% of

capital.

C. the provision of deposit insurance.

D. the periodic monitoring of banks.

E. encouraging banks to produce timely accounting statements and reports.

Answer:

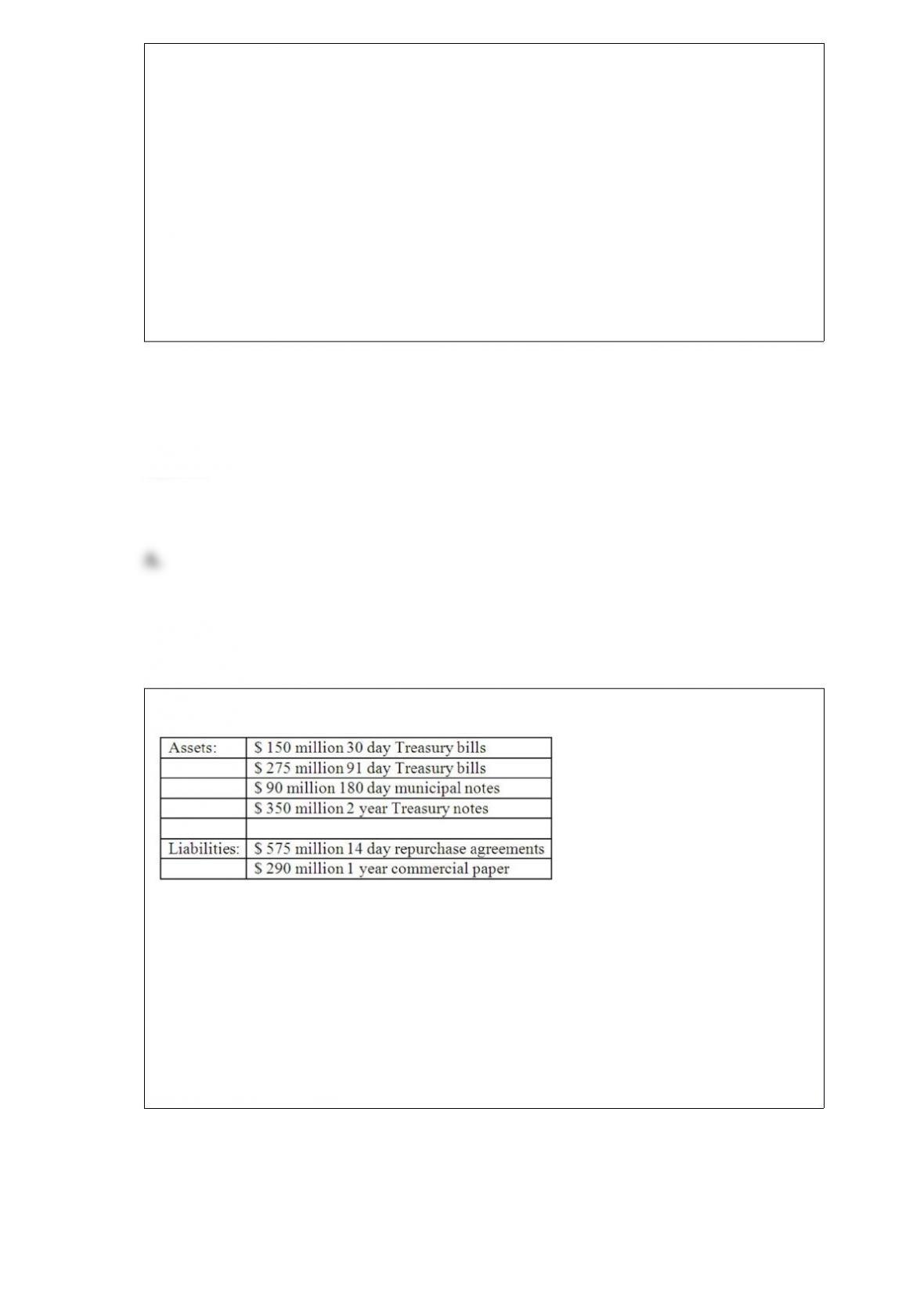

The following are the assets and liabilities of a government security dealer.

Use the repricing model to

determine the funding gap for a maturity bucket of 30 days. A. -$425 million.

B. -$95 million.

C. -$10 million.

D. -$475 million.

E. +$150 million.

Answer:

What will be the cost of using a strategy of purchased liquidity management to meet the

expected decline in deposits? Assume that the bank intends to keep $2 million in cash

as liquidity precaution. A. $10,000.

B. $15,000.

C. $30,000.

D. $40,000.

E. $50,000.

Answer:

The Securities Investor Protection Corporation (SIPC) protects investors against losses

of up to ____ on securities firm failures. A. $100,000

B. $200,000

C. $500,000

D. $1,000,000

E. $25,000,000

Answer:

In calculating the net capital for a securities firms, which of the following is NOT an

adjustment to the book value of net worth? A. The market value of net worth is

calculated on a day-to-day basis.

B. A series of adjustments are made to reflect unrealized profits and losses,

subordinated liabilities, deferred taxes, options, and futures.

C. The amount of securities that cannot be publicly sold are subtracted.

D. All assets not readily converted into cash are subtracted.

E. Haircuts to reflect potential market value fluctuations in asset values are deducted.

Answer:

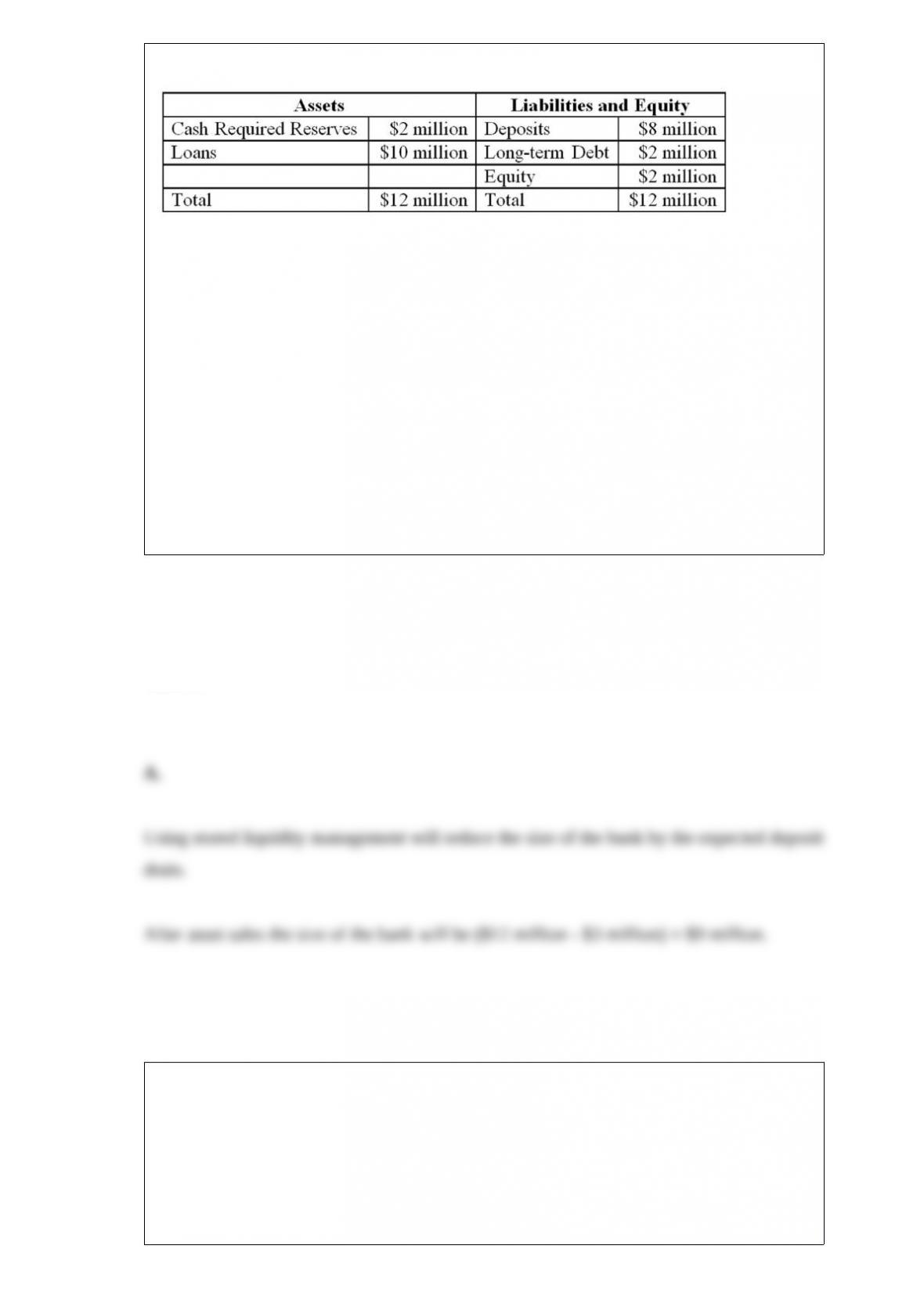

The

average interest earned on the loans is 6 percent and the average cost of deposits is 5

percent. Rising interest rates are expected to reduce the deposits by $3 million.

Borrowing more debt will cost the bank 5.5 percent in the short term.

What will be the size of the bank if a stored liquidity management strategy is adopted?

A. $9 million.

B. $11 million.

C. $12 million.

D. $14 million.

E. $15 million.

Answer:

The credit risk on swaps is considered to be A. more than the credit risk on loans.

B. less than the credit risk on loans.

C. same as the credit risk on loans.

D. is negligible compared to the credit risk on loans.

E. less likely to cause an FI to fail than is interest rate risk.

Answer:

If the bank receives a quote of $0.1975/€ for one-year forward rates for the Euro (to buy

and to sell), what is the arbitrage profit for the bank if it uses $1,000,000 as the notional

amount? A. $5,000.

B. $16,500.

C. $19,350.

D. $22,000.

E. $25,675.

Answer:

What should be the trading price of the BP futures contract at the end of the year in

order for the FI to be perfectly hedged? That is, the FI earns its original anticipated

spread without any effects of exchange rate changes? A. $1.60/≤.

B. $1.61/≤.

C. $1.62/≤.

D. $1.63/≤.

E. $1.64/≤.

Answer:

The following question are based on material in Appendix 8B

Which theory of term structure argues that individual investors have specific maturity

preferences? A. The unbiased expectations theory.

B. The liquidity premium theory.

C. The loanable funds theory.

D. The market segmentation theory.

E. None of the above.

Answer:

Allright Insurance has total assets of $140 million consisting of $50 million in 2-year, 6

percent Treasury notes and $90 million in 10-year, 7.2 percent fixed-rate Baa bonds.

These assets are funded by $100 million 5-year, 5 percent fixed rate GICs and equity.

The duration of the T-notes, Baa bonds, and GICs is 1.93 years, 6.9 years, and 4.5 years

respectively. What is the leverage-adjusted duration gap for Allright? A. 1.99 years.

B. 5.13 years.

C. 0.63 years.

D. 1.91 years.

E. 1.0 year.

Answer:

The largest liability on FDIC-insured savings institutions’ balance sheet as of year-end

2012 was A. commercial paper.

B. small time and savings deposits.

C. repurchase agreements.

D. FHLBB advances.

E. cash.

Answer:

Customer loans are classified on a DI’s balance sheet as A. assets, because the DI’s

major asset is its client base.

B. liabilities, because the customer may default on the loan.

C. assets, because the DI earns servicing fees on the loan.

D. liabilities, because the DI must transfer funds to the borrower at the initiation of the

loan.

E. assets, because DIs originate and monitor loan portfolios.

Answer:

What is the most important factor determining bankruptcy, according to the Altman

Z-score model? A. Working capital to assets ratio.

B. Retained earnings to assets ratio.

C. Earnings before interest and taxes to assets ratio.

D. Market value of equity to book value of long-term debt ratio.

E. Sales to assets ratio.

Answer:

Which of the following partially explains why cash management services have not

attracted customers in Europe to the degree that they have in the US?A. Prevalence of

nationwide branching and banking in Europe.

B. Prevalence of interregional banking restrictions in Europe.

C. Prohibitive charges imposed for the use of domestic telephone lines in Europe.

D. Prohibitive charges imposed on such services in Europe.

E. None of the above.

Answer:

A bond is scheduled to mature in five years. Its coupon rate is 9 percent with interest

paid annually. This $1,000 par value bond carries a yield to maturity of 10 percent.

Calculate the percentage change in this bond’s price if interest rates on comparable risk

securities increase to 11 percent. Use the duration valuation equation.A. +4.25 percent

B. -4.25 percent

C. +8.58 percent

D. -3.93 percent

E. -3.84 percent

Answer:

The merger bid premium usually is defined asA. the difference between the price paid

for the company and the market value immediately prior to the merger announcement.

B. the ratio of the purchase price of a target bank’s equity to its book value.

C. the difference between the market value immediately prior to the merger

announcement and the book value of the company.

D. All of the above.

E. Answers A and B only.

Answer:

Which of the following is NOT considered a trading activity of securities firms? A.

Position trading.

B. Pure arbitrage.

C. Liquidity trading.

D. Risk arbitrage trading.

E. Program trading.

Answer:

Which of the following observations concerning mortgages is NOT valid? A. They

may refer to loans secured by lien on residential houses.

B. They are a minor component in finance company portfolios.

C. Mortgage-backed securities are created by securitization.

D. Home equity loans are examples of second mortgages.

E. The interest on a mortgage loan secured by a primary residence is not tax deductible

to the homeowner.

Answer:

In a loan participation A. the holder (buyer) is not a party to the underlying credit

agreement, so the initial contract between the loan seller and the borrower remains in

place after the sale.

B. the holder (buyer) is a party to the underlying credit agreement, so the initial

contract between the loan seller and the borrower remains in place after the sale.

C. the holder (buyer) can vote only on material changes to the loan contract such as

changes in interest rate or collateral backing the loan.

D. Answers A and C only.

E. Answers B and C only.

Answer:

Separate accounts business of a life insurance company represents A. policies written

that cover individuals as a group.

B. liabilities owed to other life insurance companies as a result of reinsurance.

C. the cumulative cash value paid to policyholders if the policies are terminated before

maturity.

D. a fund established separately from the other funds of the insurance company and

invested without regard to the usual diversification restrictions.

E. the cumulative price that the company may repurchase policies from existing

customers.

Answer:

The Euromoney Index for a given country currently is based on the A. spread of the

required interest rate on that country’s debt over LIBOR.

B. a number of economic and political factors specifically weighted according to their

relative importance in determining country risk problems.

C. a combined economic and political risk survey of economists and political analysts

presented on a 100-point scale.

D. surveys of the loan officers of major multinational banks.

E. historical default rates of that country’s loans.

Answer:

What is the concentration limit (as a % of capital) for secured loans made by this bank?

A. 10 percent.

B. 20 percent.

C. 33 percent.

D. 40 percent.

E. 50 percent.

Answer: