Operating ROA is calculated as __________, while ROE is calculated as _________.

A. EBIT/total assets; net profit/total assets

B. net profit/total assets; EBIT/total assets

C. EBIT/total assets; net profit/equity

D. net profit/EBIT; sales/total assets

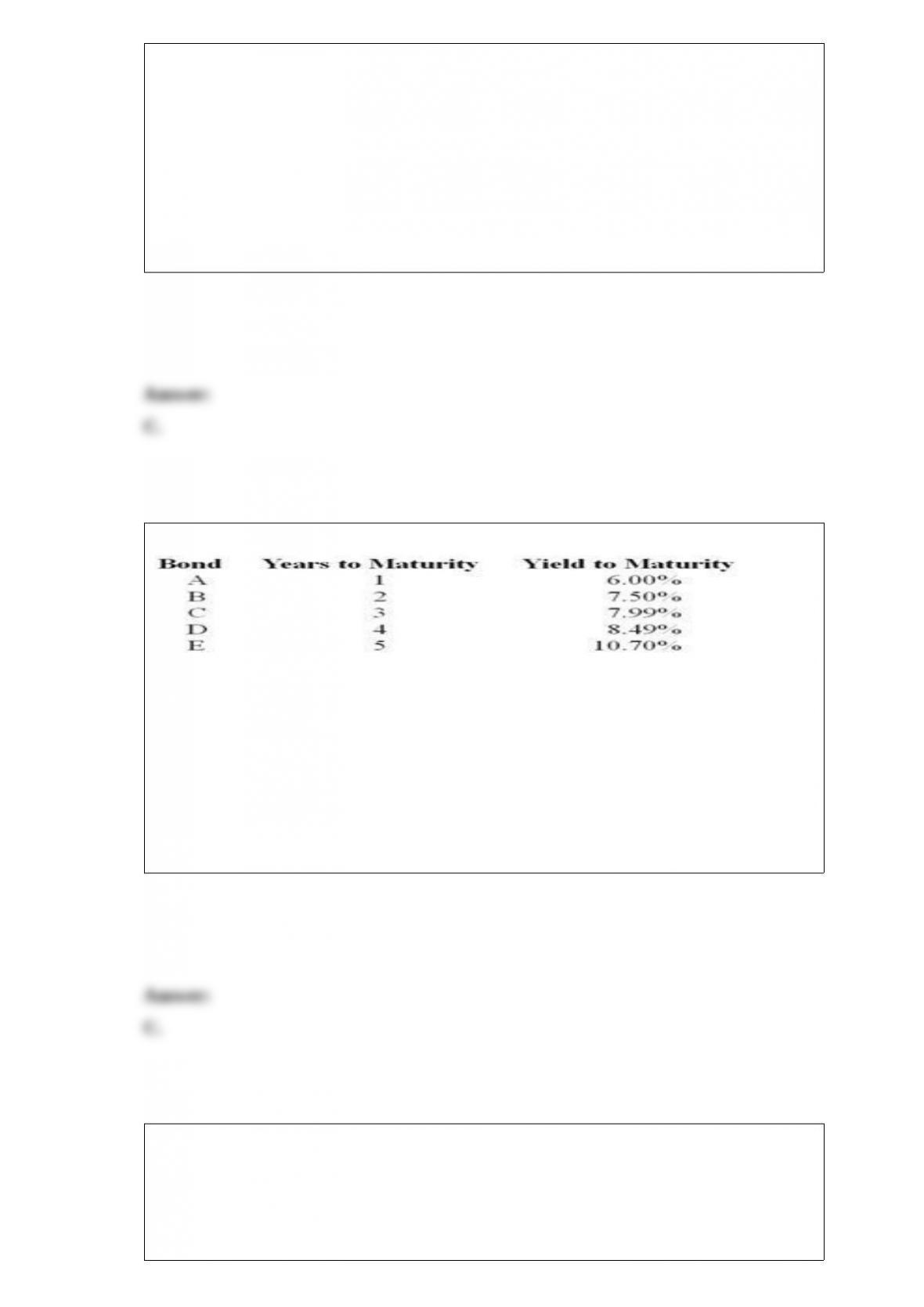

$1,000 par value zero-coupon bonds (ignore liquidity premiums)

The expected 2-year interest rate 3 years from now should be _________.

A. 9.55%

B. 11.4%

C. 14.89%

D. 13.3%

You are considering adding a new security to your portfolio. To decide whether you

should add the security, you need to know the security’s:

I. Expected return

II. Standard deviation

III. Correlation with your portfolio

A. I only

B. I and II only

C. I and III only

D. I, II, and III

Which one of the following will increase the value of a put option?

A.

a decrease in the exercise price

B.

a decrease in time to expiration of the put

C.

an increase in the volatility of the underlying stock

D.

What strategy is designed to ensure a value within the bounds of two different stock

prices?

A. collar

B. covered Call

C. protective put

D. straddle

Which of the following variables is not associated with the Sharpe ratio?

A. standard deviation

B. rate of return

C. beta

D. risk free rate

Standard deviation of portfolio returns is a measure of ___________.

A. total risk

B. relative systematic risk

C. relative nonsystematic risk

D. relative business risk

A life insurance firm wants to minimize its interest rate risk, and it is planning on

paying out $250,000 in 5 years. Which one of the following investments best matches

its goal?

A. high-yield utility stocks

B. 5-year zero-coupon bonds

C. 10-year coupon bonds

D. money market investments rolled over as needed

WEBS are _____________.

A. mutual funds marketed internationally on the Internet

B. synthetic domestic stock indexes

C. equity indexes that replicate the price and yield performance of foreign stock

portfolios

D. single stock investments in a foreign security

The only money exchanged by both the long and short at the creation of a futures

contract is called the ___________.

A. spot price

B. futures price

C. margin

D. collateral

Ace Ventura, Inc., has expected earnings of $5 per share for next year. The firm’s ROE

is 15%, and its earnings retention ratio is 40%. If the firm’s market capitalization rate is

10%, what is the present value of its growth opportunities?

A. $25

B. $50

C. $75

D. $100

A firm has a tax burden of .7, a leverage ratio of 1.3, an interest burden of .8, and a

return-on-sales ratio of 10%. The firm generates $2.28 in sales per dollar of assets.

What is the firm’s ROE?

A. 12.4%

B. 14.5%

C. 16.6%

D. 17.8%

You short-sell 200 shares of Rock Creek Fly Fishing Co., now selling for $50 per share.

If you want to limit your loss to $2,500, you should place a stop-buy order at ____.

A. $37.50

B. $62.50

C. $56.25

D. $59.75

The current stock price of National Paper is $69, and the stock does not pay dividends.

The instantaneous risk-free rate of return is 10%. The instantaneous standard deviation

of National Paper’s stock is 25%. You want to purchase a call option on this stock with

an exercise price of $70 and an expiration date 73 days from now.

Using the Black-Scholes OPM, the call option should be worth __________ today.

A. $2.50

B. $2.94

C. $3.26

D. $3.50

An individual who goes short in a futures position _____.

A. commits to delivering the underlying commodity at contract maturity

B. commits to purchasing the underlying commodity at contract maturity

C. has the right to deliver the underlying commodity at contract maturity

D. has the right to purchase the underlying commodity at contract maturity

Assume that both X and Y are well-diversified portfolios and the risk-free rate is 8%.

Portfolio X has an expected return of 14% and a beta of 1. Portfolio Y has an expected

return of 9.5% and a beta of .25. In this situation, you would conclude that portfolios X

and Y _________.

A. are in equilibrium

B. offer an arbitrage opportunity

C. are both underpriced

D. are both fairly priced

Limiting your investments to the top six countries in the world in terms of market

capitalization may make sense for _________ investor but probably does not make

sense for ________ investor.

A. an active; a passive

B. a passive; an active

C. a security selection expert; a market timer

D. a fundamental; a technical

The price of a stock fluctuates between $43 and $60. If the time frame referenced

encompasses the primary trend, the $43 price may be considered the ___________.

A. intermediate trend level

B. minor trend level

C. resistance level

D. support level

A bond portfolio manager notices a hump in the yield curve at the 5-year point. How

might a bond manager take advantage of this event?

A. Buy the 5-year bonds, and short the surrounding maturity bonds.

B. Buy the 5-year bonds, and buy the surrounding maturity bonds.

C. Short the 5-year bonds, and short the surrounding maturity bonds.

D. Short the 5-year bonds, and buy the surrounding maturity bonds.

Which type of risk is most significant for bonds?

A. maturity risk

B. default risk

C. interest rate risk

D. reinvestment rate risk

In the United States in 2014, there were approximately _______ mutual funds offered

by fewer than _______ fund complexes.

A. 12,000; 600

B. 7,000; 100

C. 8,000; 800

D. 9,000; 300

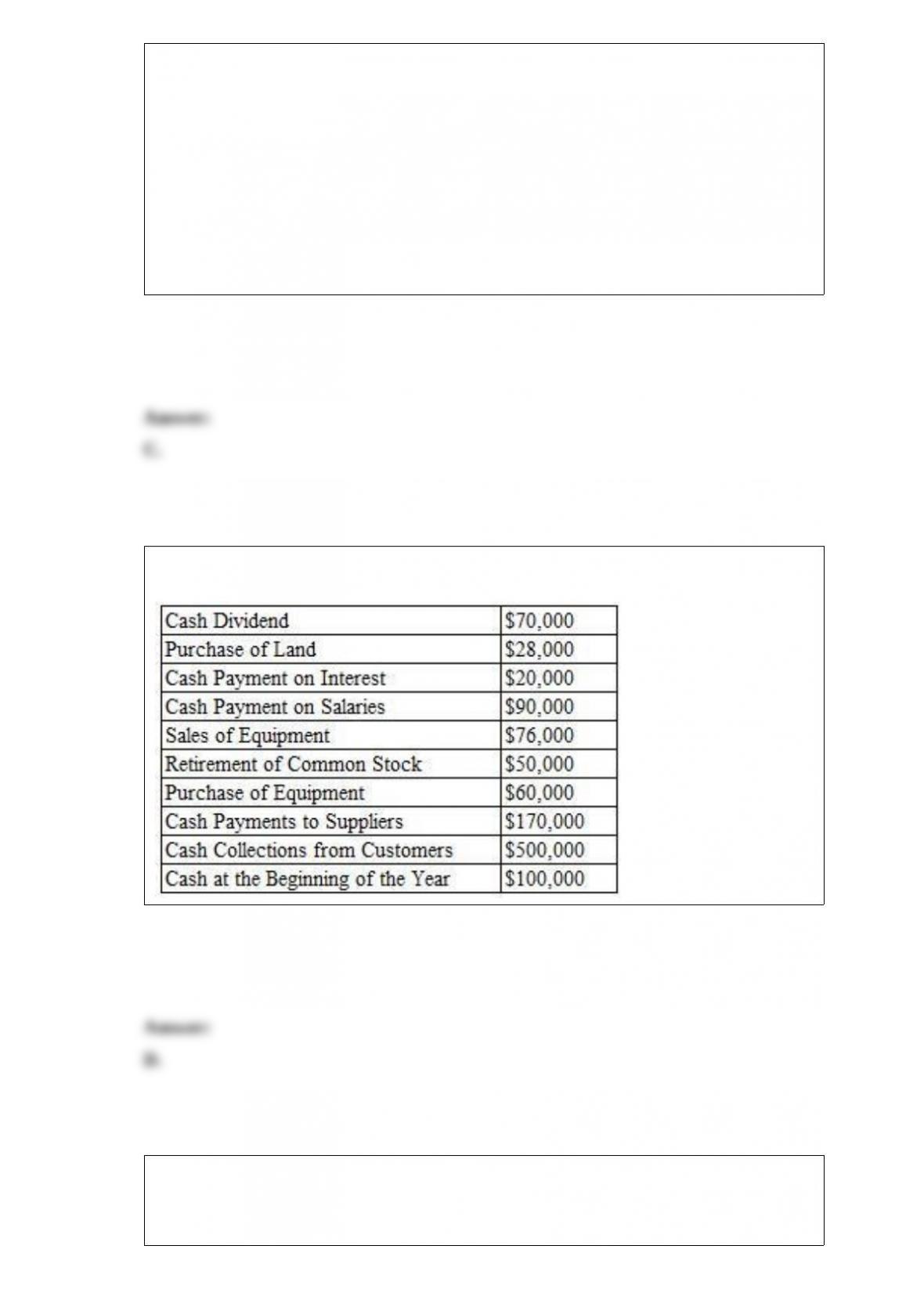

Use the following cash flow data of Haven Hardware for the year ended December 31,

2015.

What is the cash

at the end of

2015 for Haven

Hardware?

A. $6,000

B. $94,000

C. $736,000

D. $188,000

Estimates of a stock’s intrinsic value calculated with the free cash flow methodology

depend most critically on _______.

A. the terminal value used

B. whether one uses FCFF or FCFE

C. the time period used to estimate the cash flows

D. whether the firm is currently paying dividends

Longer-term American-style options with maturities of up to 3 years are called

__________.

A. warrants

B. LEAPS

C. GICs

D. CATs

A stock has a beta of 1.3. The systematic risk of this stock is ____________ the stock

market as a whole.

A. higher than

B. lower than

C. equal to

D. indeterminable compared to

The _________ is the difference between the actual call price and the intrinsic value.

A. stated value

B. strike value

C. time value

D. binomial value

Duration facilitates the comparison of bonds with differing ___________.

A. default risks

B. conversion ratios

C. maturities

D. yields to maturity

Analysis of bond returns over a multiyear horizon based on forecasts of the bond’s yield

to maturity and reinvestment rate of coupons is called

______.

A. multiyear analysis

B. horizon analysis

C. maturity analysis

D. reinvestment analysis

When technical analysts say a stock has good “relative strength,” they mean that in the

recent past __________.

A. it has performed well compared to its closest competitors

B. it has exceeded its own historical high

C. trading volume in the stock has exceeded the normal trading volume

D. it has outperformed the market index

What is the VaR of a $10 million portfolio with normally distributed returns at the 5%

VaR? Assume the expected return is 13% and the standard deviation is 20%.

A. 13%

B. -13%

C. 19.90%

D. -19.90

The measure of risk used in the capital asset pricing model is ___________.

A. specific risk

B. the standard deviation of returns

C. reinvestment risk

D. beta

All of the following ratios are related to efficiency except _______.

A. total asset turnover

B. fixed-asset turnover

C. average collection period

D. cash ratio