What is the gain or loss on the futures position using T-Bonds (Duration = 9 years, $96

per $100 face value) if the shock to interest rates is 1 percent [i.e. ΔR/(1 + R) = 0.01

and ΔRf/(1 + Rf) = 0.011]?A. $16,320,960 loss.

B. $16,312,320 gain.

C. $15,552,750 gain.

D. $15,552,750 loss.

E. $13,252,250 gain.

Answer:

Soft dollars is a term often used in reference to the portion of a fee or commission that

is allocated to A. research and other advisory services.

B. custody and escrow services.

C. clearance and settlement services.

D. banking services.

E. back office services.

Answer:

The qualified thrift lender test is designed to ensure that A. a floor is set for the

mortgage related assets held by savings institutions.

B. a ceiling is set on the mortgage related assets held by commercial banks.

C. savings associations are covered by risk-based deposit insurance premiums.

D. an interest rate ceiling is imposed on small savings and time deposits at savings

institutions.

E. regulators could close thrifts and banks faster.

Answer:

Millon National Bank has 10 million British pounds (£) in one-year assets and £8

million in one-year liabilities. In addition, it has one-year liabilities of 4 million euros

(€). Assets are earning 8 percent and both liabilities are being paid at a rate of 8 percent.

All interest and principal will be paid at the end of the year.

What is the net interest income in dollars if the spot prices at the end of the year are

$1.35/£ and €1.35/$ and the liabilities instead cost 7 percent instead of 8 percent? A.

$1,080,000.

B. $116,592.59.

C. $100,567.45.

D. $112,677.94.

E. $120,009.76.

Answer:

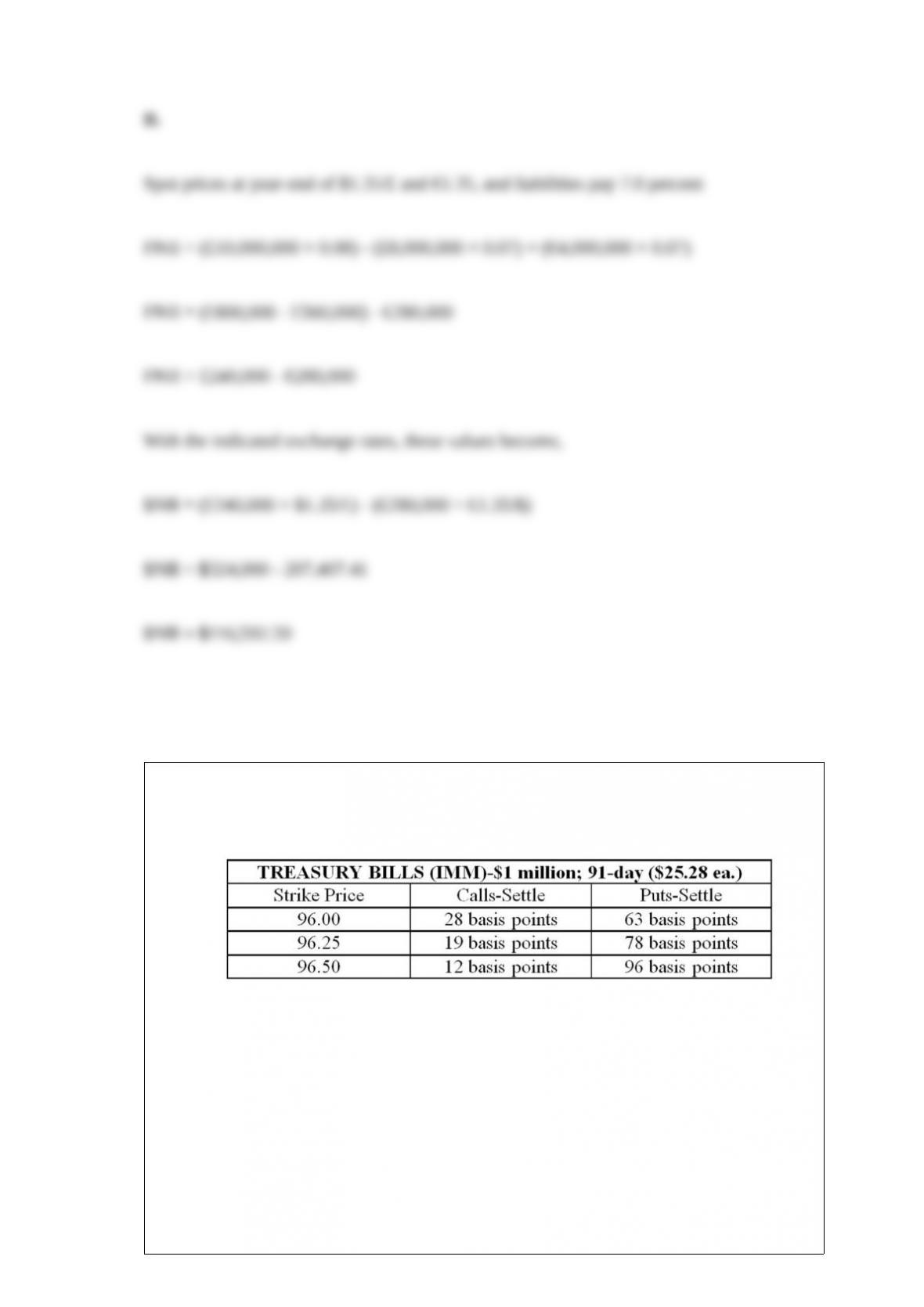

A bank with total assets of $271 million and equity of $31 million has a leverage

adjusted duration gap of +0.21 years. Use the following quotation from the Wall Street

Journal to construct an at-the-money futures option hedge of the bank’s duration gap

position. If

91-day Treasury bill rates increase from 3.75 percent to 4.75 percent, what will be the

profit/loss per contract on the bank’s futures option hedge? A. A loss of $556.10 per put

option contract.

B. A profit of $556.10 per put option contract.

C. A loss of $1,971.84 per call option contract.

D. A profit of $1,971.84 per call option contract.

E. A profit of $2,528 per put option contract.

Answer:

The dominant form of institutional venture capital firms operate as A. Corporation.

B. Subsidiary of a financial company.

C. Bank holding company.

D. Limited partnership.

E. General partnership.

Answer:

An advantage of the historic or back simulation model for quantifying market risk

includes A. calculation of a standard deviation of returns is not required.

B. all return distributions must be symmetric and normal.

C. the systematic risk of the trading positions is known.

D. there is a high degree of confidence when using small sample sizes.

E. None of the above.

Answer:

When comparing banks and mutual funds, A. mutual funds have more liquidity risk

than banks because all shareholders share the loss of value on a pro rata basis.

B. mutual funds have less liquidity risk than banks because all shareholders share the

loss of value on a pro rata basis.

C. mutual funds have more liquidity risk than banks because all shareholders have the

ability to withdraw their money on a first-come first basis.

D. mutual funds have less liquidity risk than banks because all shareholders have the

ability to withdraw their money on a first-come first basis.

E. mutual funds have the same liquidity risk as banks because both shareholders and

depositors share the fall in the loss of value on a pro rata basis.

Answer:

The fastest growing type of swap is A. a commodity swap.

B. a credit swap.

C. a currency swap.

D. an equity swap.

E. an interest rate swap.

Answer:

Consider a mutual fund with 100 shareholders who each invested $10 for a total of

$1,000. If the assets of the mutual fund are worth $900, what is the net asset value for

each one of the mutual fund shares? A. $0.9.

B. $9.

C. $90.

D. $10.

E. $0.10.

Answer:

Life insurance guaranty fundsA. are sponsored by state insurance regulators.

B. involve a permanent reserve fund similar to the FDIC’s bank deposit reserve.

C. require uniform contributions from each state when there is a failure of an insurance

company.

D. make policyholder payments immediately in the event of an insurance company

failure.

E. are regulated by the Federal Reserve Bank.

Answer:

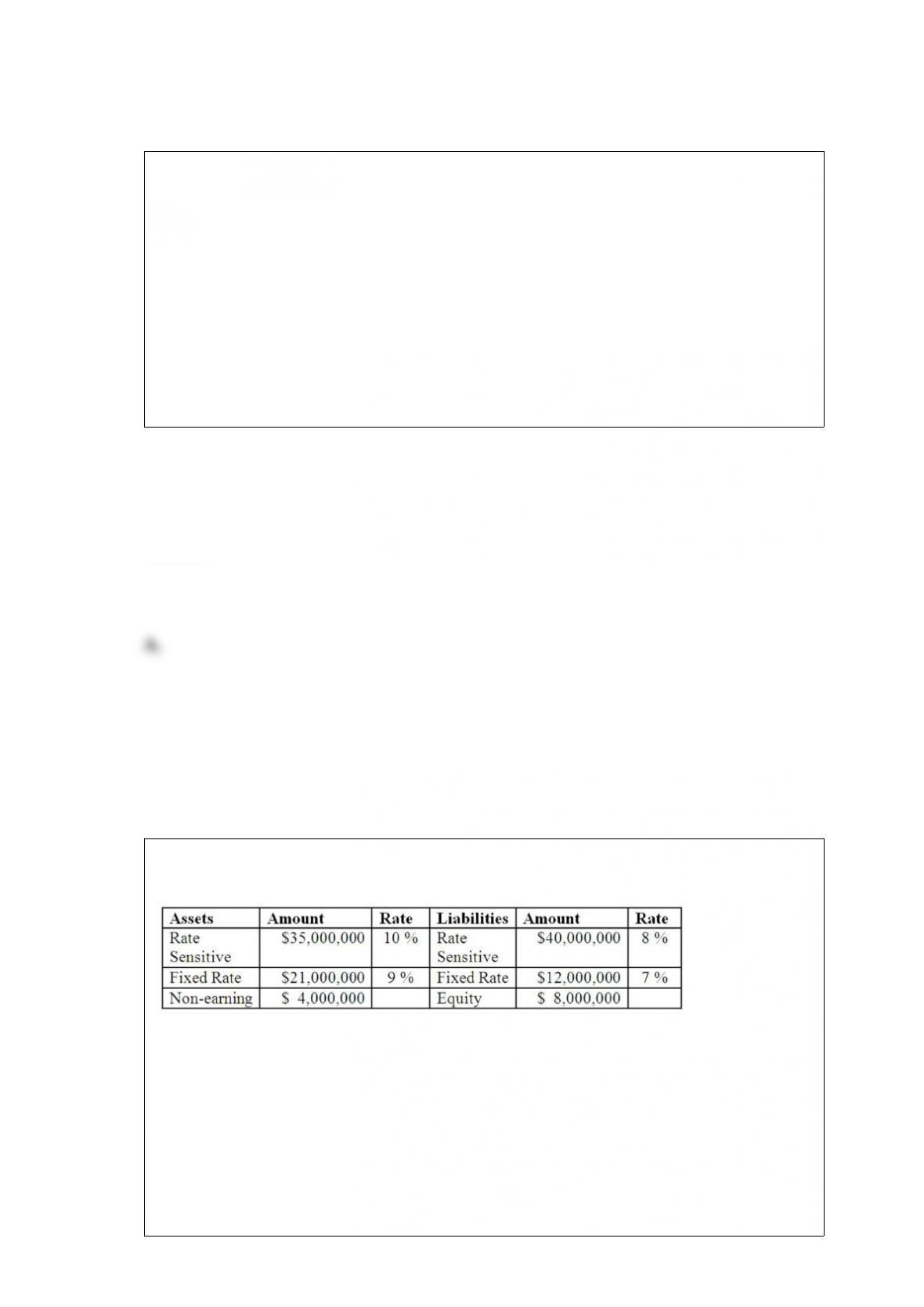

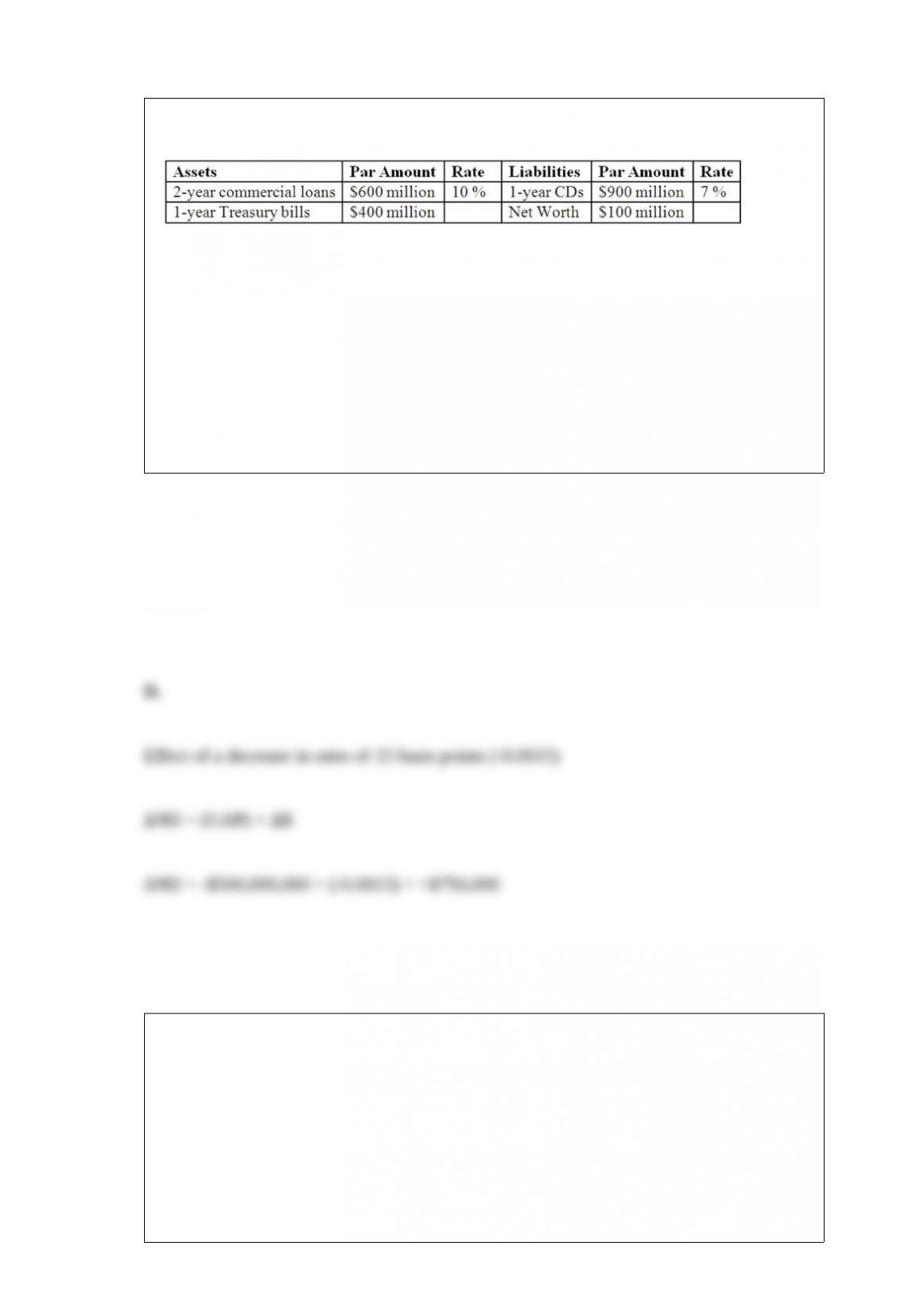

The balance sheet of ARGH Insurance shows the following fixed and rate sensitive

assets and liabilities.

What is the

repricing gap for the FI? A. $0.

B. $5,000,000.

C. $9,800,000.

D. -$5,000,000.

E. -$8,000,000.

Answer:

If the current (spot) rate for one-year British pound futures is currently at $1.58/≤ and

each contract size is ≤62,500, how many contracts are required to be purchased or sold

in order to fully hedge against the pound exposure? (Assume no basis risk). A. Sell

1,600 BP futures.

B. Buy 1,600 BP futures.

C. Sell 1,712 BP futures.

D. Buy 2,560 BP futures.

E. Buy 1,712 BP futures.

Answer:

Through August 2012, which of the following approximates the amount of funds paid

back to the U.S. Treasury as part of the TARP Capital Purchase Program? A. $192

billion.

B. $120 billion.

C. $234 billion.

D. $26 billion.

E. $19 billion.

Answer:

Two countries are identical in all respects except that country A’s rate of growth of the

domestic money supply (MG) is 33 percent, while country B’s MG is 25 percent, and

country A’s variance of export revenue (VAREX) is 3.75 percent, while country B’s

VAREX is 10 percent. Based only on these two variables, compare the prices of debt

issued by country A to the price of debt issued by country B if both issues have the

same maturity and coupon payments. Both debt issues are trading in the secondary

market. A. Country B’s debt is priced higher because the probability of rescheduling is

lower for country A than for B.

B. Country A’s debt is priced higher because the probability of rescheduling is lower

for country A than does country B.

C. Country B’s debt is priced lower because country B has a lower probability of

rescheduling than does country A.

D. Country A’s debt is priced lower because country A has a higher probability of

rescheduling than does country B.

E. Both debt issues have the same price.

Answer:

Buyers are willing to purchase rescheduled LDC and EM debt because of A. political

pressure.

B. the potential for capital gains.

C. tax considerations.

D. side payments from FIs.

E. misinformation.

Answer:

The covariance of the change in spot exchange rates and the change in futures exchange

rates is 0.6060, and the variance of the change in futures exchange rates is 0.5050. What

is the estimated hedge ratio for this currency? A. 0.306.

B. 0.694.

C. 1.440.

D. 1.200.

E. 0.833.

Answer:

Which type of loans are securitized most often? A. Residential mortgages.

B. Credit card loans.

C. Auto loans.

D. Student loans.

E. Commercial and industrial (C&I) loans.

Answer:

Which of the following is the major weakness of the linear probability model? A. The

model is based on past data of the borrower.

B. Measurement of the loan risk is difficult.

C. Estimated probabilities of default may lie outside the interval 0 to 1.

D. Neither the market value of a firm’s assets nor the volatility of the firm’s assets is

directly observed.

E. None of the above is a weakness of the linear probability model.

Answer:

Rising interest rates will cause the market value ofA. call options on bonds to increase.

B. put options on bonds to decrease.

C. call options on bonds to decrease.

D. bond futures to increase.

E. Answers A and B only.

Answer:

If the exchange rate had fallen from $1.60/≤1 at the beginning of the year to $1.50/≤1 at

the end of the year when the FI needed to repatriate the principal and interest on the

loan. What would be the dollar loan amount repatriated at the end of the year? A. $6.25

million.

B. $11.6 million.

C. $7.25 million.

D. $6.625 million.

E. $10.875 million.

Answer:

Restrictions on branching occurred initially at the state level becauseA. money center

banks feared a loss of correspondent business.

B. small unit banks feared a loss of business from the larger branching banks.

C. improved communications and customer needs.

D. All of the above.

E. Answers A and B only.

Answer:

The following information is from First Yaupon Savings Association.

If all

interest rates decrease by 15 basis points, what is the expected impact on the FI’s net

interest income? (Hint: Use the repricing model to answer this question.)A. +$150,000.

B. -$150,000.

C. -$750,000.

D. +$750,000.

E. No change.

Answer:

Using standard deviations, which bank is in a better position if the average earnings on

the assets of Bank A is 11 percent and Bank B is 12 percent (ignore all other factors)?

A. Bank B, because its earnings of 12 percent is higher than Bank A’s 11 percent while,

its standard deviation is lower.

B. Bank B, because its earnings of 12 percent is higher compared to Bank A’s 11

percent, while its standard deviation is higher.

C. Bank B, because its earnings of 12 percent is higher compared to Bank A’s 11

percent, while its standard deviation is the same.

D. Bank A, because although its earnings of 11 percent is lower compared to Bank B’s

12 percent, its standard deviation is significantly lower.

E. Bank A, because although its earnings of 11 percent is lower compared to Bank B’s

12 percent, its standard deviation is the same.

Answer:

Given the expected one-year rates in one year, what are the possible bond prices in one

year? A. $912.40 and $922.32.

B. $857.27 and $866.93.

C. $734.90 and $751.56.

D. $896.06 and $905.80.

E. $802.92 and $820.47.

Answer:

An FI funds a $5 million residential mortgage in 2012 by allocating capital and by

issuing demand deposits. The mortgage represents a loan-to-value of 70 percent. The

demand deposits have a reserve requirement of 10 percent and a deposit insurance

premium of 23 basis points.

What is the minimum capital requirement on the mortgage in order for the institution to

be adequately capitalized? A. $0.

B. $400,000.

C. $200,000.

D. $500,000.

E. $5,000,000.

Answer:

Which of the following is NOT characteristic of the consumer loans at U.S. banks? A.

Non revolving consumer loans is the largest class of loans.

B. Credit card loans often have default rates between four and eight percent.

C. Usury ceilings affect the rate structure for consumer loans.

D. Consumer loans differ widely with respect to collateral, rates, maturity, and

noninterest fees.

E. Revolving consumer loans include new and used automobile loans, mobile home

loans, and fixed-term consumer loans.

Answer:

Which of the following items is not considered to be an advantage of using back

simulation over the RiskMetrics approach in developing market risk models? A. Back

simulation is less complex.

B. Back simulation creates a higher degree of confidence in the estimates.

C. Asset returns do not need to be normally distributed.

D. The correlation matrix does not need to be calculated.

E. A worst-case scenario value is determined by back simulation.

Answer:

Retirement funds under management of mutual funds manage approximately what

percentage of the mutual fund assets. A. One-tenth

B. One-quarter

C. One-half

D. Three-quarters

E. Zero.

Answer:

Revolving loans are credit lines A. that allow the borrower to borrow the repeat credit

only after the first loan is repaid.

B. that specify a maximum size and a maximum period of time over which the

borrower can withdraw funds.

C. whose interest rate adjusts with movements in an underlying market index interest

rate.

D. on which a borrower can both draw and repay many times over the life of the loan

contract.

E. that include new and used automobile loans, mobile home loans, and fixed-term

consumer loans.

Answer:

The primary difference between Basel I and the proposed Basel III in converting OBS

values to on-balance-sheet credit equivalent amounts isA. the use of credit ratings in

Basel III to assign credit risk weights on the OBS activities.

B. the use of six weight classes by Basel III rather than four classes.

C. the use of the underlying counterparty activity in Basel II to assign credit risk

weights on the OBS activities.

D. All of the above.

E. Answers A and C only.

Answer:

Which of the following is an example of microhedging asset-side portfolio risk? A.

When an FI, attempting to lock in cost of funds to protect itself against a rise in

short-term interest rates, takes a short position in futures contracts on CDs.

B. FI manager trying to pick a futures contract whose underlying deliverable asset is

not matched to the asset position being hedged.

C. When an FI hedges a cash asset on a direct dollar-for-dollar basis with a forward or

futures contract.

D. When an FI manager wants to insulate the value of the institution’s bond portfolio

fully against a rise in interest rates.

E. When an FI manager wishes to use futures or other derivative securities to hedge the

entire balance sheet duration gap.

Answer:

How does purchased liquidity management affect profitability? A. By its impact on the

interest rate sensitivity of assets.

B. By its impact on the interest rate sensitivity of liabilities.

C. By determining the default risk of investment securities.

D. By its impact on the cost of purchased funds.

E. By enhancing the liquidity of assets held.

Answer:

What is essentially understood to be insurance for property-casualty insurance

companies? A. Policy reserves.

B. Conditional reserve funds.

C. Reinsurance.

D. Unearned premiums.

E. Surplus notes.

Answer:

National-chartered commercial banks are most likely to be regulated by A. the FDIC

only.

B. the FDIC and the Federal Reserve System.

C. the Federal Reserve System only.

D. the FDIC, the Federal Reserve System, and the Comptroller of the Currency.

E. the Federal Reserve System and the Comptroller of the Currency.

Answer: